Digital Front Door & Patient Engagement Market Size (2024 – 2030)

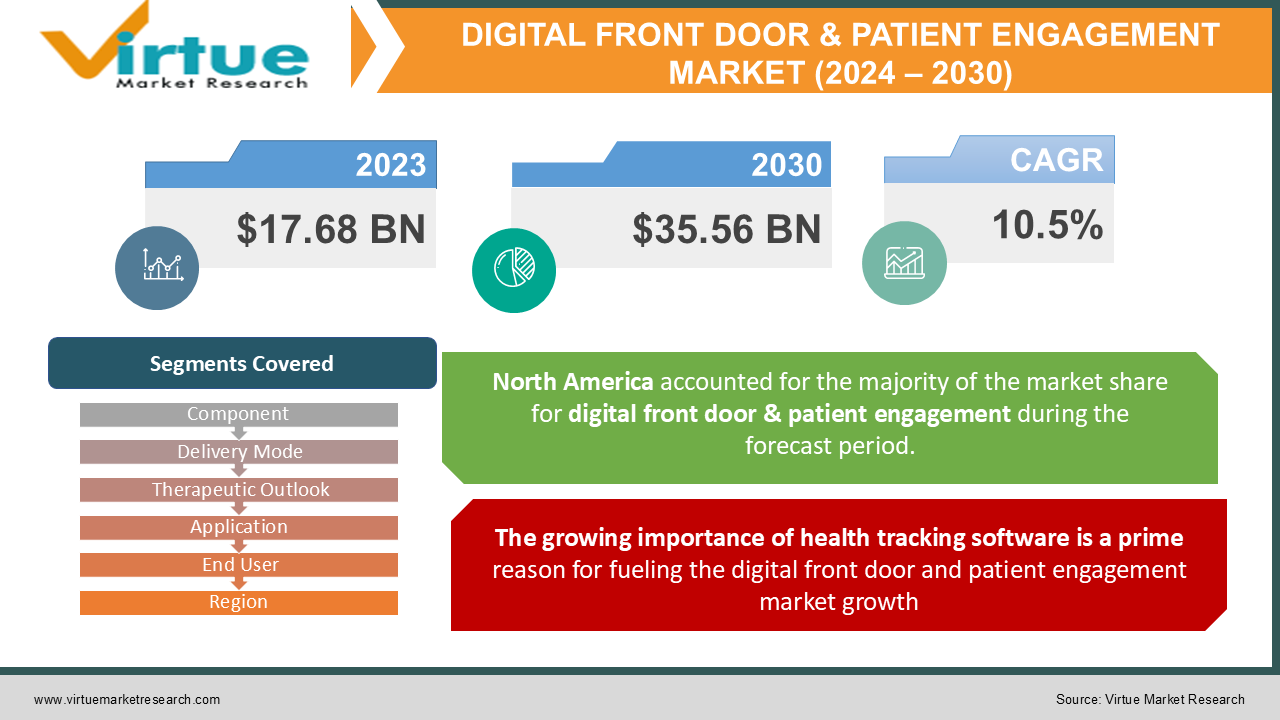

IThe Global Digital Front Door & Patient Engagement Market was valued at USD 17.68 Billion and is projected to reach a market size of USD 35.56 Billion by the end of 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 10.5%. The market is growing due to the implementation of developing government policies and healthcare programmes that encourage patient-centric treatment, higher demand for patient engagement products in the post-pandemic period, and greater use of medical-health applications.

INDUSTRY OVERVIEW

The virtual mechanism by which a patient interacts with her healthcare practitioner is referred to as the digital front door and patient engagement. Because they include automated communications, these patient engagement solutions are more than just engaging solutions. Aside from that, the procedure is crucial in assuring patient happiness. Patient engagement solutions save patient data and allow a group of healthcare practitioners to contact their patients via an online patient portal. Furthermore, computers, software, and services collect patient information, and technology improves the app's quality and ensures its safety.

Patient engagement solutions cover a wide range of services, as well as healthcare information technology and hardware. These services are used to encourage patients to take an active role in their health. These platforms use a patient-centered healthcare delivery system to enhance health outcomes and provide value-based treatment, which will drive the global patient engagement solutions market forward throughout the projected period. Over the forecast period, the worldwide patient engagement solutions market will expand due to the implementation of government legislation and efforts promoting patient-centric care, as well as a growth in demand for patient engagement solutions and the usage of mobile health apps. As the worldwide burden of chronic illnesses and the senior population has risen, patient engagement solutions have become increasingly popular.

MARKET DRIVERS:

The growing importance of health tracking software is a prime reason for fueling the digital front door and patient engagement market growth

As the incidence of health-related problems grows, health monitoring is becoming increasingly extremely popular. In today's technologically advanced world, patients have access to data that can help them obtain tailored care and maintain track of their health. People are increasingly keeping track of their health data, and many of them share it with their health and fitness coaches and physicians to stay on track. During the projected period, the high demand for health and fitness tracking gadgets will also aid in the expansion of the patient engagement solutions market.

Implementation of government regulations and initiatives to promote patient-centric care thus propelling the digital front door and patient engagement market

Governments all around the world are enacting various legislations and policies to encourage the usage of patient engagement technology. According to the agreement, the European Union (EU) Health Ministry will endeavor to develop an eHealth platform for simple access to electronic health data across Europe in 2020, and eHealth will be incorporated into the Europe Vision 2020. The Patient Protection and Affordable Care Act (PPACA) or Affordable Care Act (ACA), which was signed into law in March 2010, has increased the number of stakeholders in the United States who use patient engagement solutions. This is predicted to have a positive influence on worldwide market revenue growth.

MARKET RESTRAINTS:

The high cost of patient engagement solutions deployment is hampering the market growth

Healthcare information technology systems are high-priced software systems. Moreover, the cost of software upgrades and operational expenditures may outweigh the product's cost. Maintenance and support services, such as software upgrades and modifications, are recurring expenditure that makes up more than half of the total cost of ownership. End-users must be taught to optimize the productivity of various healthcare information technology solutions, which raises the system's cost due to a lack of internal information technology knowledge in the healthcare business. As a result, the high cost of the digital front door & patient engagement solutions are impeding market expansion.

Concerns regarding data security and privacy are a major reason restraining the market growth

Problems with the security and privacy of patient health data are preventing information from being shared among healthcare professionals. As a consequence, patient engagement projects in various healthcare institutions are impeded, and potential end users' acceptance of patient engagement solutions is constrained. As a result, data security will be a key hurdle for the patient engagement solutions market to expand throughout the forecast period.

DIGITAL FRONT DOOR & PATIENT ENGAGEMENT MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

10.5%

|

|

Segments Covered

|

Component, By Delivery Mode, By Therapeutic Outlook, By Application, By End User, and By Region. |

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Cerner Corporation (Oracle), NXGN Management, LLC, Epic Systems Corporation, Allscripts Healthcare, LLC, McKesson Corporation, ResMed, Klara Technologies, Inc., Koninklijke Philips N.V., Athenahealth Inc., CPSI

|

Segmentation Analysis

DIGITAL FRONT DOOR & PATIENT ENGAGEMENT MARKET - BY COMPONENT

- Hardware

- Software

- Services

Based on components, the digital front door & patient engagement market is segmented into Hardware, Software, and services. Among these, the software segment dominated the market. Since patient engagement solutions are mostly software-based, the software category accounted for 49 percent of revenue share in 2021. The increasing usage of medical health applications and remote tracking devices is projected to help the category flourish. Besides this, the services segment is poised to grow substantially over the forecast period of 2023 - 2030. The services segment is anticipated to expand at a CAGR of 17%. The increasing use of digital health solutions by medical institutions, clinics, and hospitals is likely to boost demand for education, consulting, and implementation services, propelling the market forward.

DIGITAL FRONT DOOR & PATIENT ENGAGEMENT MARKET – BY DELIVERY MODE

- Web-based

- Cloud-based

- On-premise

Based on delivery mode, the digital front door & patient engagement market is segmented into Web-Based, Cloud-Based, and On-premise. Among these, the cloud-based segment contributed significantly to market share. During the projection period, the cloud-based solution segment is predicted to grow at the quickest rate. Increased acceptance of cloud-based solutions due to their flexibility, scalability, and affordability is driving revenue growth in this market. Cloud-based solutions help healthcare professionals improve productivity, streamline operations, and communicate and integrate data in real-time across several locations or systems. This is encouraging market participants to create cutting-edge cloud-based patient interaction solutions, which would help the category increase in revenue.

DIGITAL FRONT DOOR & PATIENT ENGAGEMENT MARKET – BY THERAPEUTIC OUTLOOK

- Chronic Diseases

- Women’s Health

- Fitness

- Mental Health

Based on the therapeutics outlook, the digital front door & patient engagement market is segmented into Chronic Diseases, Women’s health, fitness, and mental health. The chronic disease category accounted for the greatest revenue share in 2021, owing to an increase in the elderly community in major city centers, the incidence of chronic diseases, and the use of digital technologies prompted by the COVID-19 pandemic. Patient engagement solutions make chronic illness management easier by facilitating disease prevention and detection, as well as treating the condition with or without the intervention of a doctor. Given the significant health and wellness initiatives taken by big players, as well as the expansion of product portfolio to include mental health, weight management, pregnancy, and growing research activities in this sector, the health and wellness segment is estimated to register a faster revenue CAGR over the forecast period. UbiCare, for example, works with medical institutions to cut costs while also enhancing treatment quality and results with the help of engaging more and more patients. Pregnancy Messaging Updates for young parents have been added to the company's solution's new design to improve its offers.

DIGITAL FRONT DOOR & PATIENT ENGAGEMENT MARKET – BY APPLICATION

- Social Management

- Health Management

- Home Healthcare Management

- Financial Health Management

Based on application, the digital front door & patient engagement market is segmented into Social Management, Health Management, Home Healthcare Management, and Financial Health Management. In 2021, the home healthcare management category generated the most revenue and is projected to expand at a CAGR of 17% over the forecast period. Patients can use home health management to keep track of their appointments, make payments online, and communicate with their home healthcare personnel. This segment's high revenue share may be due to patients' growing understanding of the complexity of their ailments, as well as their desire to actively participate in maintaining their health. Chronic disease patients must be continuously checked and kept up to date on how to manage their conditions. As a result of rising healthcare consumerism, people are becoming more involved in their treatment planning, tracking, and optimization.

DIGITAL FRONT DOOR & PATIENT ENGAGEMENT MARKET - BY END-USER

- Payers

- Providers

- Individual users

Based on end-users, the digital front door & patient engagement market is segmented into Payers, Providers, and Individual users. In 2021, the providers’ sector accounted for over 50.0 percent of the market. In the following years, it is likewise predicted to have the highest CAGR. This is due to the growing need for engaging care and patient education for chronic illness management. Providers are considered to be the first point of contact for treatment and consultation o numerous health conditions. Because of greater usage of routine care processes and patient portals for information access and essential health decision-making, caregivers are adopting patient engagement systems. In 2021, the Payers category had the second-largest revenue share. This segment's revenue has been attributed to the growing usage of patient and customer engagement solutions that encourage broader coverage and facilitate value-based care delivery. Payers, such as insurance companies and other organizations that finance medical treatments, want to keep track of their patients and engage with them during the treatment process. This is predicted to promote the adoption of patient engagement solutions and, as a result, the segment's revenue growth.

DIGITAL FRONT DOOR & PATIENT ENGAGEMENT MARKET - BY REGION

- North America

- Europe

- The Asia Pacific

- Latin America

- The Middle East

- Africa

Based on region, the digital front door & patient engagement market is grouped into North America, Europe, Asia Pacific, Latin America, The Middle East, and Africa. Because of the presence of major market players in the region, increased acceptance of medical and electronic health records (EHR), and significant investments in Digital Door & Patient engagement software by big businesses, the North American patient engagement solutions market generated the highest revenue share in 2021. Additionally, greater awareness, in combination with increased government financing in the healthcare business and the development of current technology, is predicted to promote market revenue growth in the area.

Europe captured the second spot and emerged with the second-largest market share in the world. In the European area, the Digital Door & Patient Engagement Solutions market is predicted to increase significantly over the forecast period. The key stimulus for corporate growth is the need for efficient healthcare delivery and advancements in healthcare solutions. Furthermore, governmental financing schemes like the NHS in the United Kingdom and Dossier Medical Personnel regulations have a strong influence on industry growth in the region throughout the projection period.

Over the projected period, the Asia-Pacific patient engagement solutions market is predicted to grow at a much quicker rate. The growing desire for cost-effective and high-quality treatment, as well as an aging population and increased prevalence of various chronic ailments, are driving the Asia-Pacific patient engagement solutions market. In addition, the recent COVID-19 pandemic in Asia-Pacific has resulted in a larger patient pool, especially in China and India. The rising need for precise and quick diagnosis and treatment of different health disorders, as well as increased patient volume, are likely to drive market revenue growth in Asia-Pacific.

DIGITAL FRONT DOOR & PATIENT ENGAGEMENT MARKET - BY COMPANIES

The market for front door & patient engagement market is fragmented due to the prevalence of many medium-sized companies operating in this field. Some of the prominent players operating in the digital front door & patient engagement market are:

- Cerner Corporation (Oracle)

- NXGN Management, LLC

- Epic Systems Corporation

- Allscripts Healthcare, LLC

- McKesson Corporation

- ResMed

- Klara Technologies, Inc.

- Koninklijke Philips N.V.

- Athenahealth Inc.

- CPSI

NOTABLE HAPPENING IN THE DIGITAL FRONT DOOR & PATIENT ENGAGEMENT MARKET

- PARTNERSHIP- In 2021, McKesson and Merck have established a strategic partnership that would allow the two companies to leverage the power of real-world evidence (RWE) to improve patient outcomes and cancer treatment quality.

- PARTNERSHIP- In December 2021, Northwell Health and Playback Health have established a deal to introduce Playback's patient engagement platform at certain medical centers, to increase mobility and communication of point-of-care medical data while adhering to health information security standards.

- PRODUCT LAUNCH - In June 2020, Athenahealth, Inc. announced Athena Telehealth, a new embedded healthcare provider that allows clinicians to perform proper telemedicine sessions with their patients, allowing them to improve patient care.

COVID-19 IMPACT ON THE DIGITAL FRONT DOOR & PATIENT ENGAGEMENT MARKET

The COVID-19 pandemic has had a long-term impact on public health as well as a significant economic impact on most countries. The COVID-19 epidemic has also raised the requirement for the social distance between doctors and patients, driving demand for virtual consultations via various telehealth and patient engagement technologies, as well as the necessity for accurate and rapid patient health record exchange. Several industry participants have included COVID-19-related elements into their current patient engagement solutions, which are being made accessible to consumers for free. Furthermore, as patient numbers have risen, the requirement for EMR and EHR platforms to manage sophisticated patient data has expanded. The second wave of COVID-19 has also affected several nations, resulting in full lockdowns. Due to social distance restrictions, the usage of patient engagement methods has continued to rise.