Asia Pacific Smoothies Market

The Asia Pacific smoothies’ market is expected to grow from approximately USD 4.5 billion in 2025 to around USD 8.5 billion in 2030, at a compound annual growth rate of around 12.8% during 2025-2030.

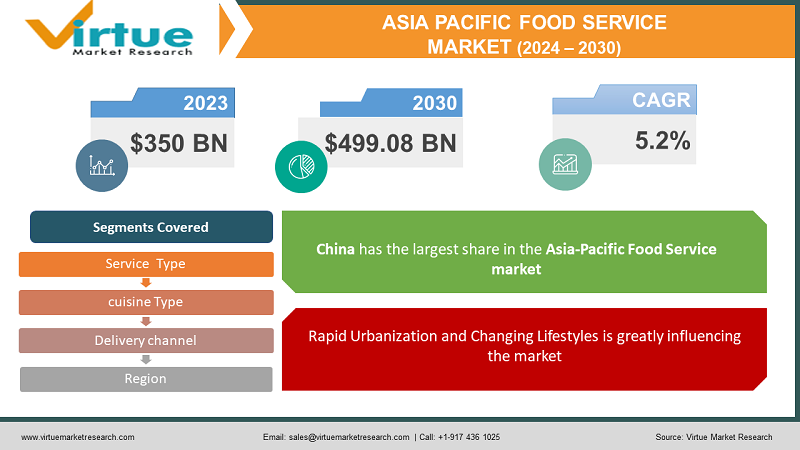

Explore reportThe Asia Pacific Food Service Market was valued at USD 350 Billion and is projected to reach a market size of USD 499.08 Billion by the end of 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 5.2%.

The Asia-Pacific food service market stands as a vibrant and dynamic landscape, characterized by diverse culinary preferences, rapid urbanization, and evolving consumer demands. With a burgeoning population and increasing disposable income, the region witnesses a flourishing restaurant industry, encompassing a wide array of cuisines from traditional to global offerings. The market thrives on innovation, with food delivery services, cloud kitchens, and technology-driven solutions reshaping the dining experience. Key factors driving this market include a growing appetite for convenience, a shift towards healthier eating habits, and a rising preference for experiential dining, making it a hub for culinary experimentation and market expansion.

Key Market Insights:

Asia Pacific Food Service market drivers:

Rapid Urbanization and Changing Lifestyles is greatly influencing the APAC Food service market towards a positive trajectory.

As urbanization accelerates across the Asia-Pacific region, lifestyles are evolving, leading to a surge in demand for convenient and diverse dining options. Urban dwellers, especially millennials and the working population, seek quick, varied, and on-the-go food choices due to time constraints. This trend has fueled the growth of food delivery services, quick-service restaurants, and ready-to-eat meal options, catering to the fast-paced urban lifestyle.

Increasing Disposable Income and Consumer Spending in Asia Pacific is propelling the food service market in the region.

Rising disposable incomes in several Asia-Pacific countries have resulted in higher consumer spending on dining out and exploring diverse culinary experiences. As people's purchasing power increases, there's a growing inclination towards premium dining experiences, international cuisines, and unique food concepts. This factor has contributed to the expansion of high-end restaurants, food festivals, and gourmet dining establishments, driving the market towards more sophisticated and diverse offerings to meet varied consumer preferences and demands.

Asia Pacific Food Service Market Restraints and Challenges:

Regulatory Complexity and Compliance faced by businesses in food service market pose hindrance.

The region comprises diverse countries, each with its own set of regulations, licensing requirements, and food safety standards. Navigating through these varying regulations poses a challenge for multinational food service chains and local businesses alike. Adhering to these standards while ensuring consistency across different locations becomes complex, often requiring substantial resources and expertise to maintain compliance.

Supply Chain Disruptions and Sustainability is a major issue in APAC Food Service market.

The food service industry heavily relies on a complex supply chain involving farmers, distributors, and logistics. Issues such as climate change impacts, natural disasters, or geopolitical tensions can disrupt this supply chain, leading to price fluctuations, shortages, or quality inconsistencies. Additionally, ensuring sustainability throughout the supply chain, including sourcing ethically produced ingredients and managing food waste, presents a persistent challenge, especially as consumer expectations for sustainable practices continue to rise. Balancing cost-effectiveness with sustainable practices remains a key challenge in this market.

Opportunities in the Asia Pacific Food Service market:

The Asia-Pacific food service market presents immense opportunities driven by several factors, including the region's growing middle-class population, urbanization, and changing consumer preferences. Emerging economies within the region offer a fertile ground for expansion, witnessing a surge in demand for diverse cuisines, quick-service restaurants, and innovative dining experiences. Moreover, the increasing adoption of digital technologies, such as online food delivery platforms and mobile ordering, presents avenues for market players to tap into the evolving consumer behavior and preferences. Additionally, the rising focus on health-conscious eating habits and sustainable food practices opens doors for businesses to introduce healthier menu options and environmentally friendly practices, creating a competitive edge and meeting the changing demands of consumers in the Asia-Pacific region.

|

REPORT METRIC |

DETAILS |

||

|

Market Size Available |

2022 - 2030 |

||

|

Base Year |

2022 |

||

|

Forecast Period |

2023 - 2030 |

||

|

CAGR |

5.2% |

||

|

Segments Covered |

By Service Type, cuisine Type, Delivery channel, and Region |

||

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

||

|

Regional Scope |

|

||

|

Key Companies Profiled |

McDonald's Corporation, Yum! Brands (KFC, Pizza Hut, Taco Bell), Starbucks Corporation, Domino's Pizza, Restaurant Brands International (Burger King, Tim Hortons), Jollibee Foods Corporation, Darden Restaurants, Inc. (Olive Garden, LongHorn Steakhouse), SSP Group, Lotte Food Co., Ltd., Ajinomoto Co., Inc. |

Asia Pacific Food Service Market Segmentation:

The largest segment by service type in the Asia-Pacific food service market is the Quick Service Restaurants (QSR) category having market share of 39% in 2023. QSRs dominate due to their convenience, affordability, and fast-paced service, aligning well with the region's bustling urban lifestyles and evolving consumer preferences. These establishments offer speedy, on-the-go meals, catering to a diverse customer base, including working professionals, students, and families seeking quick yet satisfying dining experiences. The QSR model's adaptability to incorporate diverse cuisines, coupled with the rapid expansion of international QSR chains, further bolsters its position as the largest service type segment in the Asia-Pacific food service market. The fastest-growing segment is Quick Service Restaurants (QSR) expected to grow at a rate of 11.2% during the forecast period. This rapid growth can be attributed to changing consumer lifestyles favoring convenience and speed without compromising on quality. QSRs cater to the on-the-go dining culture, offering affordable and quickly accessible meals. The integration of technology in QSRs, such as mobile ordering, drive-thru services, and online delivery platforms, has further boosted their popularity, especially among younger demographics seeking convenient dining options amidst busy schedules. The ability of QSRs to adapt menus to include healthier choices and accommodate diverse tastes while ensuring swift service has fueled their exponential growth in the Asia-Pacific region.

In the Asia-Pacific food service market, the largest segment by cuisine type is typically the Asian Cuisine category covering 38% of revenue share in 2023. This dominance stems from the region's rich cultural heritage and a massive local consumer base that favors and resonates deeply with their traditional culinary offerings. Asian cuisine holds a significant advantage due to its widespread popularity among both local residents and international tourists. The diverse range of flavors, cooking styles, and dishes within Asian cuisine caters to varied tastes while reflecting the authentic flavors and cultural identities of different countries across the region. In the Asia-Pacific food service market, the fastest-growing segment by cuisine type is Fusion and Specialty Cuisine. This surge is primarily attributed to the evolving consumer palates seeking unique dining experiences that blend diverse culinary traditions. Fusion cuisine offers a creative amalgamation of flavors, techniques, and ingredients from various cultures, appealing to a broad spectrum of consumers eager for innovative and adventurous dining options. The trend towards globalization and cultural exchange fosters an environment where Fusion and Specialty Cuisine stand out for their ability to cater to diverse tastes.

In the Asia-Pacific food service market, the largest segment by delivery channel is typically the Dine-in Restaurants. This is primarily due to the cultural significance of dining out as a social activity across many Asian countries. Dine-in restaurants offer not just food but an experience, allowing customers to enjoy meals in a communal setting while emphasizing hospitality and ambiance. Furthermore, in many Asian cultures, sharing meals with family, friends, or colleagues holds great importance, making dine-in restaurants a preferred choice for gatherings, celebrations, and business meetings. Despite the rise of other convenient options like online food delivery services or takeaways, the intrinsic cultural value placed on dining in restaurants contributes to its sustained prominence in the Asia-Pacific market. The fastest-growing segment by delivery channel is Online Food Delivery Services anticipated to grow with a CAGR of 7.9% during 2024-2030. This growth is primarily fueled by changing consumer lifestyles, increased internet penetration, and the convenience offered by digital platforms. The shift towards online ordering and delivery has been accelerated by the COVID-19 pandemic, as consumers seek safer, contactless dining options. The availability of diverse cuisines, promotional offers, and the ease of ordering through mobile apps or websites have contributed to the rapid expansion of online food delivery services. The trend is further supported by restaurants partnering with delivery aggregators, enhancing their reach and accessibility to a broader customer base, making it a pivotal and swiftly growing channel.

Within the Asia-Pacific food service market, China stands out as the largest region having market share of 36% in 2023. This dominance is attributed to several factors, including its vast population, robust economic growth, and rich culinary traditions. China's burgeoning middle class and urbanization have fueled a thriving dining-out culture, leading to increased demand for various food service options. Rapid urban development and changing lifestyles have contributed to a diverse landscape of restaurants, from traditional eateries to international chains, catering to a broad spectrum of consumer preferences. The continuous innovation in dining experiences, coupled with the adoption of technology-driven solutions, has further propelled China's food service market. India emerges as the fastest-growing region in this market. India's food service market is experiencing rapid expansion due to several factors. The country's growing urban population, rising disposable income, and changing lifestyles have fueled an increased demand for dining out and diverse culinary experiences. Moreover, the presence of a young demographic inclined towards exploring different cuisines and dining trends contributes significantly to this growth. The evolving food delivery landscape, supported by the widespread adoption of online food ordering platforms, has further accelerated the market's growth in India. This convergence of demographic trends, shifting consumer preferences, and technological advancements positions India as the fastest-growing region in the Asia-Pacific food service market.

The COVID-19 pandemic significantly impacted the Asia-Pacific food service market, causing widespread disruptions across the industry. Stringent lockdowns, social distancing measures, and restrictions on dining-in severely affected traditional restaurant operations, leading to closures and reduced foot traffic. However, this crisis accelerated the adoption of digital technologies, with a rapid shift towards online food delivery services, contactless dining options, and virtual kitchens. As restrictions eased, there was a gradual recovery in dine-in activities, albeit with altered consumer behaviors focusing on safety, hygiene, and convenience. The pandemic highlighted the importance of resilience and adaptability within the food service industry, prompting a greater emphasis on innovation, flexible business models, and enhanced hygiene standards to regain consumer confidence and navigate the evolving landscape.

Latest Trends/Developments:

Key Players:

The Asia Pacific Food Service Market was valued at USD 350 Billion and is projected to reach a market size of USD 499.08 Billion by the end of 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 5.2%.

Rapid Urbanization and Changing Lifestyles along with Increasing Disposable Income and Consumer Spending are the main drivers propelling the Asia Pacific Food Service Market.

Based on cuisine type, the Asia Pacific Food Service Market is segmented into Asian Cuisine, Western Cuisine, Fusion and Specialty Cuisine, Local and Traditional Cuisine

China is the most dominant region for the Global Asia Pacific Food Service Market.

McDonald's Corporation, Yum! Brands, Starbucks Corporation, Domino's Pizza are the key players operating in the Global Asia Pacific Food Service Market

Joining thousands of companies around the world committed to making the Excellent Business Solutions.

Specify your preferred Countries, Segments, or timeframes

Unlock Country Level Outlook, Trends, Cross-country Comparability, or supply Chain Variations.

Analyst Support

Every order comes with Analyst Support.

Customization

We offer customization to cater your needs to fullest.

Verified Analysis

We value integrity, quality and authenticity the most.