Counter-UAS Systems Market

In 2025, the Global Counter-UAS Systems Market was valued at approximately USD 3,214 million and is projected to reach around USD 8,472 million by 2030, expanding at a CAGR of about 21.4% during 2026–2030.

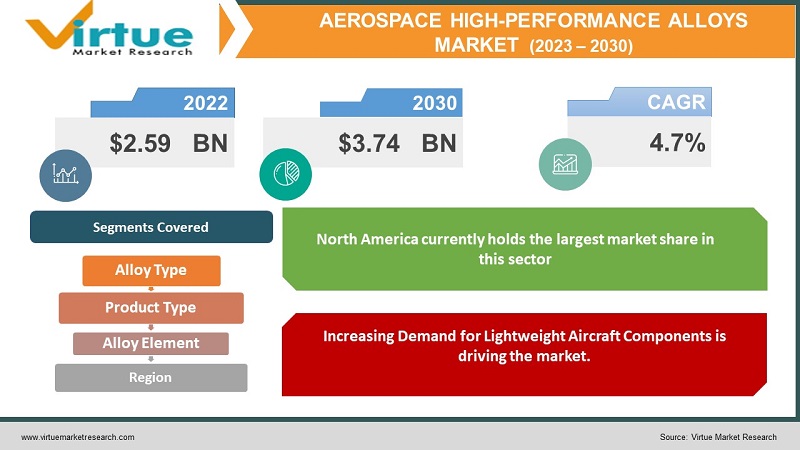

Explore reportGlobal Aerospace High-Performance Alloys Market was estimated to be worth USD 2.59 Billion in 2022 and is projected to reach a value of USD 3.74 Billion by 2030, growing at a CAGR of 4.7% during the forecast period 2023-2030.

CLICK HERE To Request Free Sample

The extremely demanding aviation industry demands materials that can survive harsh environments and offer exceptional performance. High-performance alloy is a key element used in the construction of airplanes. These alloys are perfect for important aircraft applications due to their remarkable strength, strong corrosion resistance, and stability at high temperatures. The supply of materials that adhere to the stringent requirements of the industry depends heavily on the market for aerospace high-performance alloys. The necessity for strong yet lightweight materials in the aircraft sector has led to a large increase in the market for aerospace high-performance alloys throughout time. These alloys are used in a variety of aviation parts, including fasteners, landing gears, engine parts, and airframe structures. High-performance alloys play a vital role in the aircraft industry's ongoing efforts to increase performance, decrease emissions, and improve fuel efficiency.

The market for aerospace high-performance alloys is escalating significantly due to the aerospace industry's need for strong, lightweight, and corrosion-resistant materials. The market is propelling as a result of the growth of the commercial aviation sector, rising defense spending, and technological advancements. There are concerns about high production costs and a scarcity of raw resources, though. But it is projected that ongoing industry collaborations and R&D projects will address these problems and propel the market for aerospace high-performance alloys even further.

Global Aerospace High-Performance Alloys Market Drivers:

Increasing Demand for Lightweight Aircraft Components is driving the market

The rising need for lightweight airplane parts is one of the main factors boosting the worldwide aerospace high-performance alloys market. The aerospace sector is concentrated on increasing overall performance, decreasing emissions, and increasing fuel efficiency. The achievement of these goals depends heavily on the use of lightweight materials. Aluminum and titanium alloys, which are high-performance alloys with exceptional strength-to-weight ratios, are perfect for airplane structures, engine parts, and other crucial components. These alloys aid in lowering the weight of the aircraft as a whole, which reduces fuel consumption and increases operational effectiveness. Additionally, lighter materials have a higher payload capacity, which enables airlines to transport more people or goods. The demand for lightweight aerospace components is anticipated to fuel the aerospace high-performance materials market as sustainability and cost-effectiveness become more important considerations.

Defense Modernization Programs and Geopolitical Tensions are fuelling the demand for these in the global market

Geopolitical unrest and defense modernization initiatives are two key factors driving the worldwide aerospace high-performance alloys market. Governments all across the world are making investments to modernize and improve their defense capabilities. This covers the creation of cutting-edge military vehicles, weaponry, and unmanned aerial vehicls (UAVs). In these applications, high-performance alloys are essential because they offer the extraordinary strength, toughness, and corrosion resistance needed for challenging defense conditions. In combat aircraft, where dependability and performance are of the utmost importance, the demand for advanced alloys is particularly acute. Additionally, rising defense spending as a result of rising geopolitical tensions in many countries is boosting demand for high-performance alloys. The aerospace high-performance alloys market is predicted to profit from the continued defense spending as nations aim to improve their military capabilities.

Global Aerospace High-Performance Alloys Market Challenges:

The high cost of production and a lack of raw materials are two of the most urgent challenges the worldwide aerospace high-performance alloys market is now facing. The production of high-performance alloys necessitates intricate manufacturing procedures that demand specialized tools and knowledge, driving up the cost of items. Additionally, due to supply chain concerns, some raw materials, such as the extensively used aerospace metals nickel and titanium, may be in short supply. The market's overall profitability and growth for aerospace high-performance alloys are impacted because firms are unable to maintain a trustworthy and affordable supply chain due to the high cost and restricted supply of these raw materials.

Global Aerospace High-Performance Alloys Market Opportunities:

Technology advances and improvements present a significant market opportunity for aerospace high-performance alloys worldwide. To create new alloys with improved characteristics, cost-effectiveness, and environmental sustainability, manufacturers are investing in research and development operations. Complex alloy component fabrication is now possible thanks to improvements in manufacturing processes like additive manufacturing and 3D printing. The market for aerospace high-performance alloys is experiencing substantial development potential due to partnerships between aerospace firms and material suppliers that are driving innovation and breaking down technical hurdles.

The COVID-19 epidemic has had a detrimental effect on the world market for aerospace high-performance alloys. Due to travel limitations and decreased passenger demand, aircraft manufacturing and deliveries experienced a major reduction, which hurt the aviation industry. The market suffered as a result of the decline in demand for high-performance alloys used in airplane construction. The market for high-performance alloys was further impacted by the delays or cancellations of new aircraft orders brought on by the financial difficulties experienced by airlines and aerospace manufacturers. Positively, the epidemic brought attention to the significance of robust and sustainable supply networks. This has led aerospace firms to broaden their sources of supply and give preference to local or regional vendors, potentially opening doors for domestic providers of high-performance alloys. The aerospace industry's digital transition, including the use of sophisticated manufacturing technology, has also been pushed by the crisis. As a result, alloy production procedures might become more effective and productive, which would have a long-term favorable effect on the market.

Global Aerospace High-Performance Alloys Market Recent Developments:

AEROSPACE HIGH-PERFORMANCE ALLOYS MARKET REPORT COVERAGE:

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2022 - 2030 |

|

Base Year |

2022 |

|

Forecast Period |

2023 - 2030 |

|

CAGR |

4.7% |

|

Segments Covered |

By Alloy Type, Product Type, Alloy Eleement, and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regional Scope |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Key Companies Profiled |

Alcoa, Allegheny Technologies, Aperam, Carpenter Technology, Haynes International, High-Performance Alloys Inc., NBM Metals, Outokumpu, Precision Castparts, ThyssenKrup, VSMPO |

Segmentation Analysis

Market Segmentation for High-Performance Alloys in Aerospace by Alloy Type: Cast iron and Wrought Iron are the two market segments that can be separated for aeronautical high-performance alloys. Due to their great strength, good ductility, and corrosion resistance, wrought iron alloys are widely employed in the aircraft sector. These alloys are mostly used in vital parts like fasteners, landing gears, and airframe structures. The great thermal stability of cast iron alloys, on the other hand, makes them suited for high-temperature applications in jet engines and turbine parts. While both wrought iron and cast iron alloys make up a sizeable portion of the aerospace high-performance alloys market, wrought iron is anticipated to account for the majority of sales due to its pervasive use in a variety of aircraft structures. However, the cast iron category is anticipated to develop the fastest due to the rising need for alloys that can withstand high temperatures in cutting-edge engine technology.

High-Performance Alloys in Aerospace Market Segmentation by Product Type: The market for aerospace high-performance alloys can be divided into three groups: iron base, cobalt base, and nickel base alloys. Iron base alloys are frequently used in the aircraft industry due to their excellent mechanical properties, high strength, and corrosion resistance. Cobalt base alloys can be used to create essential engine components due to their exceptional high-temperature strength and resistance to thermal fatigue. For applications like turbine blades and exhaust systems, nickel base alloys are ideal because they combine high strength, corrosion resistance, and heat resistance. Nickel base alloys are anticipated to command the largest market share among these sectors due to their extensive use in several aerospace applications. The market for cobalt base alloys is expected to develop at the quickest rate due to the rising need for improved engines and propulsion systems that call for alloys that can withstand high temperatures.

Market segmentation for high-performance alloys used in aerospace by alloy component: Based on the alloy components used, which include aluminum, titanium, and magnesium, the market for aerospace high-performance alloys can be divided into different submarkets. Due to their lightweight qualities, good mechanical strength, and corrosion resistance, aluminum alloys are frequently used in the aerospace sector and are appropriate for a variety of aircraft components. For crucial applications including airframes, engine parts, and landing gear, titanium alloys are recognized for their high strength-to-weight ratio, outstanding corrosion resistance, and capacity to sustain high temperatures. Magnesium alloys are employed largely in lightweight structures, especially in parts of aircraft interiors, and have outstanding strength-to-weight ratios. Titanium alloys are anticipated to hold the biggest market share due to their widespread use in structural and engine components. Due to the rising need for lightweight materials and fuel-efficient aircraft designs, magnesium alloys are projected to be the market category with the quickest growth.

Global market segmentation for high-performance alloys used in aerospace: The market for aircraft high-performance alloys can be divided into five geographical regions: North America, Europe, Asia Pacific, South America, and the Middle East & Africa. North America currently holds the largest market share in this sector as a result of the region's considerable aerospace high-performance alloy producers, defense contractors, and technical advancements. Europe is also a large market for aerospace high-performance alloys because of the existence of well-known aerospace industry players and increased defense spending. The Asia Pacific region is anticipated to see the quickest market growth because of the quickly growing aerospace sector in countries like China and India, rising defense budgets, and rising air passenger traffic. In addition to North America, Europe, and Asia Pacific, the Middle East and Africa and South America are experiencing an escalation in the aerospace sector, providing prospects for the aircraft high-performance alloys market.

Global Aerospace High-Performance Alloys Market Key Players

Global Aerospace High-Performance Alloys Market was estimated to be worth USD 2.59 Billion in 2022 and is projected to reach a value of USD 3.74 Billion by 2030, growing at a CAGR of 4.7% during the forecast period 2023-2030.

The Global Aerospace High-Performance Alloys Market drives the Increasing Demand for Lightweight Aircraft Components.

The Segments under the Global Aerospace High-Performance Alloys Market by the Product type are Iron Base, Cobalt Base, and Nickel Base.

China, Japan, South Korea, Singapore, and India are the most dominating countries in the Asia Pacific region for the Global Aerospace High-Performance Alloys Market

Alcoa, Allegheny Technologies, and Aperam are the three major leading players in the Global Aerospace High-Performance Alloys Market

Joining thousands of companies around the world committed to making the Excellent Business Solutions.

Specify your preferred Countries, Segments, or timeframes

Unlock Country Level Outlook, Trends, Cross-country Comparability, or supply Chain Variations.

Analyst Support

Every order comes with Analyst Support.

Customization

We offer customization to cater your needs to fullest.

Verified Analysis

We value integrity, quality and authenticity the most.