3D Print Management Software Market Size (2025 – 2030)

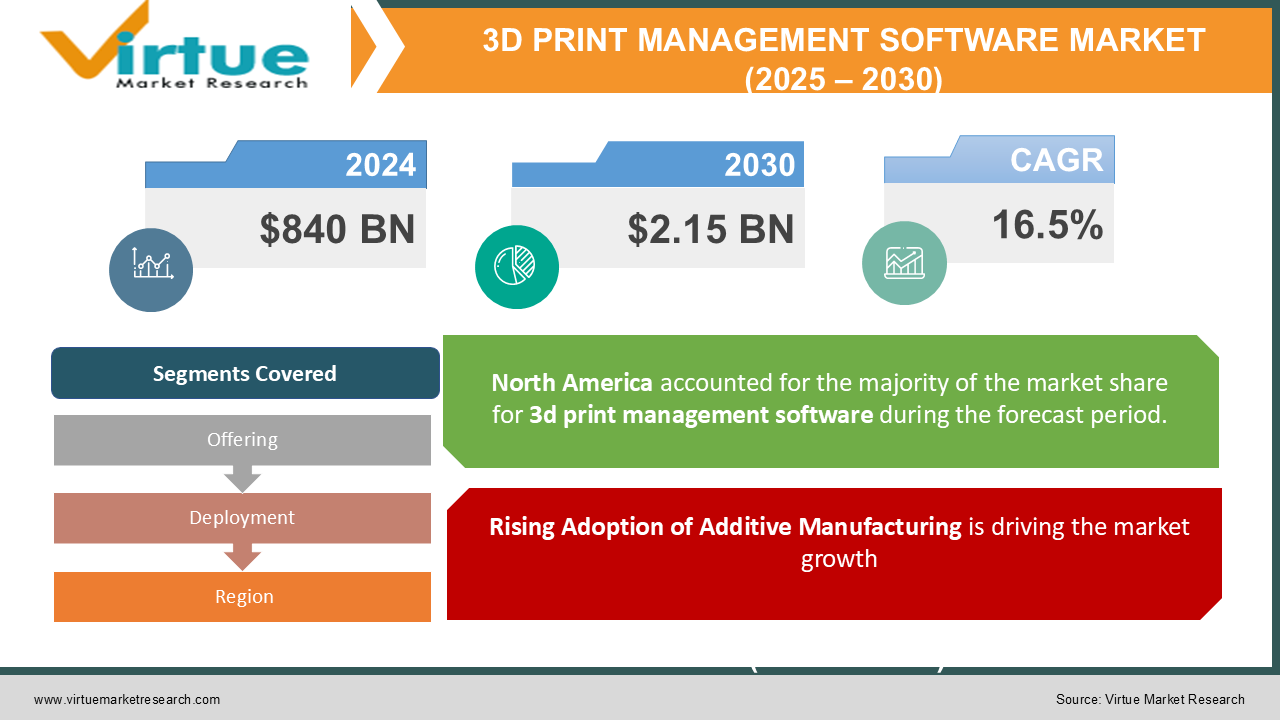

The Global 3D Print Management Software Market was valued at USD 840 billion in 2024 and is projected to grow to USD 2.15 billion by 2030, expanding at a robust CAGR of 16.5% during the forecast period.

3D print management software solutions streamline, automate, and optimize additive manufacturing workflows. They support industries by offering tools for design, print queue management, resource allocation, and security in 3D printing processes.

The rising adoption of additive manufacturing across automotive, aerospace, healthcare, and consumer goods sectors, coupled with increasing complexity in 3D printing workflows, is fueling the demand for efficient management software. Additionally, the growing trend of integrating IoT and AI into 3D printing ecosystems is driving innovation in the software segment.

Key Market Insights

-

Design software solutions dominate the market, accounting for over 40% of revenue in 2024, owing to their critical role in creating accurate 3D models.

-

The cloud-based deployment segment is projected to grow at a CAGR of 18.2%, driven by increasing demand for remote accessibility and scalability.

-

The healthcare industry is a prominent end-user, utilizing 3D print management software for customized prosthetics, implants, and surgical tools.

-

North America holds the largest market share, contributing over 38% of global revenue, supported by advancements in technology and a strong industrial base.

-

Integration of artificial intelligence (AI) and machine learning (ML) into print management software is enhancing process automation and predictive maintenance.

-

Small and medium-sized enterprises (SMEs) are increasingly adopting these solutions due to declining costs and improved accessibility.

-

Strategic collaborations between software developers and hardware manufacturers are enhancing interoperability in 3D printing workflows.

Global 3D Print Management Software Market Drivers

1. Rising Adoption of Additive Manufacturing is driving the market growth

The rapid adoption of 3D printing across industries such as aerospace, automotive, and healthcare is driving demand for management software. Additive manufacturing offers unparalleled customization, faster prototyping, and reduced production costs, necessitating software solutions for streamlined workflows.

3D print management software helps manufacturers optimize material usage, ensure consistent quality, and reduce downtime by automating tasks such as design validation, print queue scheduling, and performance monitoring. This growing reliance on 3D printing technologies is boosting the demand for comprehensive management tools.

2. Growing Need for Workflow Optimization is driving the market growth

The increasing complexity of 3D printing workflows, involving multiple printers, materials, and teams, is driving the need for efficient management software. Organizations are adopting these solutions to reduce errors, improve collaboration, and enhance overall productivity.

Workflow software enables real-time tracking of print jobs, automated resource allocation, and integration with enterprise resource planning (ERP) systems, ensuring seamless operations and faster time-to-market. The push for Industry 4.0 adoption further underscores the importance of optimized workflows.

3. Technological Advancements in 3D Printing Ecosystems is driving the market growth

Advancements in IoT, AI, and cloud computing are revolutionizing the 3D printing landscape. The integration of these technologies into print management software is enabling features such as predictive maintenance, real-time analytics, and remote monitoring.

For instance, AI-powered algorithms can predict printer failures, optimize design parameters, and enhance print quality, while IoT connectivity allows seamless communication between printers, software, and other devices. These technological innovations are driving the adoption of advanced 3D print management solutions.

Global 3D Print Management Software Market Challenges and Restraints

1. High Initial Costs and Complexity is restricting the market growth

The deployment of 3D print management software involves significant initial costs, including licensing fees, infrastructure upgrades, and employee training. These expenses can be a barrier for small and medium-sized enterprises (SMEs), limiting market penetration.

Additionally, the complexity of integrating software with existing 3D printing hardware and workflows poses challenges for organizations. Ensuring interoperability across different systems requires technical expertise and ongoing maintenance, adding to the overall cost.

2. Data Security and Intellectual Property Concerns is restricting the market growth

The increasing digitization of manufacturing processes has raised concerns about data security and intellectual property protection. 3D printing workflows involve the sharing of sensitive design files and proprietary information, making them vulnerable to cyberattacks and data breaches.

Organizations must invest in robust security software and adopt best practices to mitigate risks, which can be costly and time-consuming. These challenges highlight the need for secure and reliable 3D print management solutions.

Market Opportunities

The Global 3D Print Management Software Market presents significant growth opportunities driven by industry trends and evolving demands. The expansion of 3D printing technologies into emerging economies like India, China, and Brazil is creating a surge in demand for affordable and scalable management solutions. The rising demand for customized products, from healthcare prosthetics to automotive components, is driving the development of specialized software solutions tailored to industry-specific requirements. The growing preference for cloud-based deployment models is enabling remote access, scalability, and cost efficiency, making them attractive to SMEs and large enterprises alike. Collaborations between software developers, 3D printer manufacturers, and end-users are fostering innovation and improving software hardware compatibility. The push for sustainable manufacturing practices is driving demand for software solutions that optimize material usage, reduce waste, and enhance energy efficiency in 3D printing workflows. These factors collectively contribute to a dynamic and evolving 3D print management software market with substantial growth potential in the coming years.

3D PRINT MANAGEMENT SOFTWARE MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2024 - 2030

|

|

Base Year

|

2024

|

|

Forecast Period

|

2025 - 2030

|

|

CAGR

|

16.5% |

|

Segments Covered

|

By Offering, Deployment, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Materialise NV, Autodesk, Inc., Stratasys Ltd., Dassault Systèmes, Siemens PLM Software, 3D Systems Corporation, Ultimaker BV, MakerBot Industries, LLC, Markforged, Inc., HP Inc.

|

3D Print Management Software Market Segmentation - By Offering

-

Design Software

-

Workflow Software

-

Security Software

Design software holds a leading position in the 3D print management software market due to its critical role in the 3D printing process. This category encompasses a wide range of software tools, from Computer-Aided Design (CAD) software used to create intricate 3D models to specialized software for 3D sculpting and modeling. These tools are essential for translating design concepts into precise digital representations that can be accurately interpreted by 3D printers. The ability to create complex geometries, optimize designs for printability, and simulate the printing process within the software environment significantly enhances the overall efficiency and success of 3D printing projects. As the complexity and sophistication of 3D printing applications continue to grow, the demand for powerful and intuitive design software is expected to remain a key driver of market growth.

3D Print Management Software Market Segmentation - By Deployment

Cloud-based solutions are experiencing rapid growth, driven by their inherent advantages. Their scalability allows businesses to easily adjust their computing resources as needed, accommodating fluctuations in demand and ensuring optimal performance. This scalability translates to significant cost-effectiveness, as businesses only pay for the resources they utilize, eliminating the need for large upfront investments in hardware and infrastructure. Furthermore, cloud-based solutions empower remote work and collaboration, enabling employees to access data, applications, and services from anywhere with an internet connection. This flexibility enhances productivity, improves work-life balance, and fosters a more agile and responsive workforce. The ability to access and utilize resources on-demand, coupled with the inherent scalability and cost-effectiveness, positions cloud-based solutions as a cornerstone of modern business operations across various industries.

3D Print Management Software Market Segmentation - By Region

-

North America

-

Europe

-

Asia-Pacific

-

Latin America

-

Middle East & Africa

North America dominates the 3D print management software market, holding over 38% of global revenue, driven by its advanced manufacturing sector, strong adoption of Industry 4.0 practices, and significant investments in R&D. Europe is a key market, particularly strong in the automotive and aerospace industries, with countries like Germany, France, and the UK leading the adoption of 3D print management software for prototyping, production, and research. The Asia-Pacific region exhibits the fastest growth, spearheaded by China, Japan, and India, fueled by a burgeoning manufacturing sector and government initiatives promoting additive manufacturing. Latin America witnesses steady growth, driven by increasing 3D printing adoption in the healthcare and automotive sectors, with Brazil and Mexico as key contributors. The Middle East & Africa region experiences growth due to rising investments in advanced manufacturing and infrastructure development, supported by government initiatives and industry collaborations fostering the adoption of 3D print management software.

COVID-19 Impact Analysis

The COVID-19 pandemic accelerated the adoption of 3D printing technologies, particularly in the healthcare sector. 3D print management software played a critical role in enabling rapid production of essential medical supplies, such as face shields, ventilator components, and diagnostic tools.

The shift toward remote work and digital transformation during the pandemic highlighted the importance of cloud-based solutions, further driving demand for 3D print management software. Post-pandemic, the focus on supply chain resilience and localized manufacturing is expected to sustain market growth.

Latest Trends/Developments

The integration of AI and IoT is revolutionizing 3D printing workflows, enabling advanced features such as predictive maintenance, real-time monitoring, and automated decision-making. Manufacturers are increasingly developing software solutions that optimize resource usage and minimize environmental impact, aligning with global sustainability goals. The healthcare sector is a major driver of demand for specialized software solutions to manage complex workflows in the production of prosthetics, implants, and surgical tools. Open-source software platforms are gaining traction, offering cost-effective and customizable solutions for a wide range of 3D printing applications. Furthermore, collaborative ecosystems, fostered by partnerships between software developers, hardware manufacturers, and end-users, are accelerating innovation and expanding the scope of 3D print management solutions.

Key Players

-

Materialise NV

-

Autodesk, Inc.

-

Stratasys Ltd.

-

Dassault Systèmes

-

Siemens PLM Software

-

3D Systems Corporation

-

Ultimaker BV

-

MakerBot Industries, LLC

-

Markforged, Inc.

-

HP Inc.