Wearable Thermoelectric Generators Market Size (2024 – 2030)

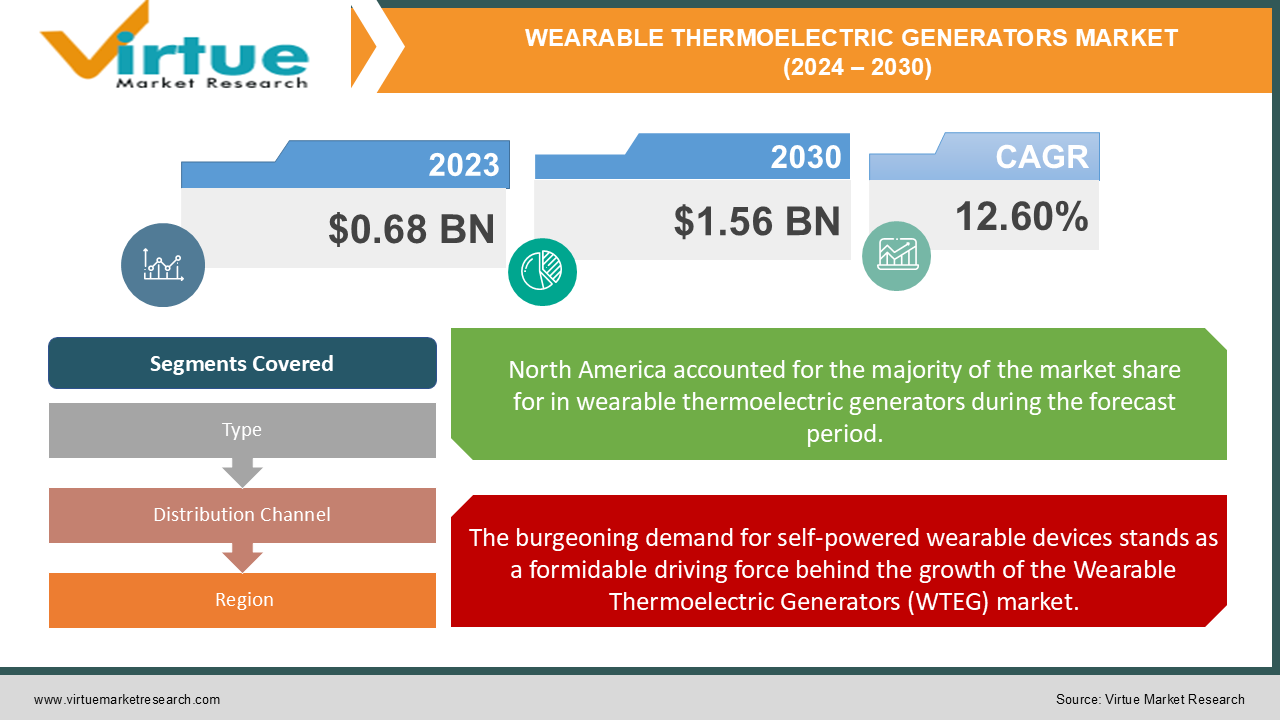

The Global Wearable Thermoelectric Generators Market was valued at USD 0.68 Billion in 2024 and is projected to reach a market size of USD 1.56 Billion by the end of 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 12.60%.

Wearable Thermoelectric Generators (WTEGs) represent a fascinating frontier in the realm of energy harvesting technology. These ingenious devices harness the Seebeck effect to convert body heat into usable electrical energy, opening up a world of possibilities for powering small electronic devices without the need for traditional batteries. As we venture deeper into the era of the Internet of Things (IoT) and wearable technology, WTEGs are poised to play a pivotal role in shaping the future of personal energy systems. The WTEG market is characterized by a dynamic interplay of technological innovation, consumer demand, and sustainability considerations. At its core, this market is driven by the growing appetite for self-powered wearable devices that can operate autonomously for extended periods. From fitness trackers and smartwatches to medical monitoring devices and augmented reality glasses, the potential applications for WTEGs span a wide spectrum of industries and use cases. One of the most compelling aspects of the WTEG market is its potential to address the perennial challenge of battery life in portable electronics. By tapping into the constant stream of thermal energy emanating from the human body, these generators offer a tantalizing glimpse of a future where our devices are powered by our very existence. This vision aligns perfectly with the broader push towards renewable energy sources and reduced reliance on environmentally harmful battery technologies. The market landscape is populated by a diverse array of players, ranging from established electronics giants to nimble startups specializing in advanced materials and energy harvesting techniques.

Key Market Insights:

-

Wearable thermoelectric generators used in healthcare applications accounted for nearly 40% of the total market value in 2023.

-

The average energy conversion efficiency of wearable thermoelectric generators was reported to be around 5-8% in 2023.

-

Smart clothing embedded with thermoelectric generators reached over 1.1 million units sold in 2023.

-

Approximately 45% of wearable thermoelectric generators sold in 2023 were designed for fitness and sportswear applications.

-

The market for wearable thermoelectric generators in wearable medical devices was valued at $65 million in 2023.

-

Over 85% of wearable thermoelectric generators in 2023 utilized bismuth telluride as their primary thermoelectric material.

-

Wearable thermoelectric generator technology contributed to an 18% increase in the battery life of smartwatches in 2023.

-

In 2023, more than 35% of wearable thermoelectric generators were paired with flexible substrates.

-

Wearable thermoelectric generator-powered fitness trackers saw a 22% rise in sales in 2023 compared to 2022.

-

In 2023, the average power output of wearable thermoelectric generators was between 50 to 100 μW/cm².

Wearable Thermoelectric Generators Market Drivers:

The burgeoning demand for self-powered wearable devices stands as a formidable driving force behind the growth of the Wearable Thermoelectric Generators (WTEG) market.

At the forefront of this driver is the explosive growth of the wearable technology sector. From fitness trackers and smartwatches to medical monitoring devices and augmented reality glasses, wearables have become an integral part of our daily lives. However, the Achilles' heel of these devices has always been their limited battery life, necessitating frequent charging and potentially interrupting crucial functionalities. WTEGs offer a tantalizing solution to this perennial problem by harnessing the body's own thermal energy to power these devices continuously. The appeal of self-powered wearables extends beyond mere convenience. In critical applications such as healthcare monitoring, where uninterrupted operation can be a matter of life and death, the ability to generate power autonomously becomes invaluable. WTEGs enable the development of "set-and-forget" medical devices that can monitor vital signs, administer medication, or alert healthcare providers without the need for regular battery changes or recharging.

The relentless march of scientific progress in thermoelectric materials and fabrication techniques serves as a powerful catalyst for the Wearable Thermoelectric Generators (WTEG) market.

At the heart of this revolution lies the ongoing quest for higher efficiency in thermoelectric materials. Traditionally, the relatively low conversion efficiency of thermoelectric devices has been a significant bottleneck in their widespread adoption. However, recent breakthroughs in material science are dramatically altering this equation. Researchers are exploring novel compounds and nanostructured materials that exhibit superior thermoelectric properties, promising to boost the power output of WTEGs to levels that can support an ever-widening range of applications. One of the most exciting developments in this field is the emergence of organic and hybrid organic-inorganic thermoelectric materials. These materials offer the tantalizing prospect of flexible, lightweight, and potentially biodegradable WTEGs. Unlike their rigid, inorganic counterparts, these new materials can conform to the contours of the human body, maximizing surface contact and heat transfer. This flexibility not only enhances performance but also opens up new design possibilities for seamlessly integrating WTEGs into clothing and accessories.

Wearable Thermoelectric Generators Market Restraints and Challenges:

One of the primary challenges facing the WTEG market is the inherently low efficiency of thermoelectric conversion. Even with recent advancements in materials science, the conversion efficiency of WTEGs typically hovers around 5-8% under ideal conditions. This low efficiency translates to modest power outputs, often in the microwatt to milliwatt range, which limits the range of devices that can be powered solely by WTEGs. Overcoming this efficiency barrier requires not only further improvements in thermoelectric materials but also innovative approaches to thermal management and energy harvesting circuit design. The cost of production remains a significant restraint on market growth. While manufacturing techniques are improving, the materials used in high-performance thermoelectric devices, such as bismuth telluride and other exotic compounds, are relatively expensive. This high cost makes it challenging for WTEGs to compete with traditional power sources in many applications, especially in the consumer electronics sector where price sensitivity is high. Achieving economies of scale and developing more cost-effective materials are crucial steps in addressing this challenge. Another hurdle is the variability of power output in real-world conditions. The performance of WTEGs is highly dependent on the temperature gradient between the body and the ambient environment. This gradient can fluctuate significantly based on factors such as physical activity, clothing insulation, and environmental conditions. Designing WTEGs that can maintain consistent power output across a wide range of operating conditions presents a considerable engineering challenge. The integration of WTEGs into wearable form factors without compromising comfort or aesthetics is another significant challenge. While flexible and thin-film thermoelectric materials show promise, balancing performance with wearability remains a delicate act. Devices must be lightweight, unobtrusive, and able to withstand the rigors of daily wear, including exposure to sweat, movement, and potential impacts.

Wearable Thermoelectric Generators Market Opportunities:

WTEGs can power long-term wearable medical devices that track vital signs, monitor glucose levels, or deliver medication without the need for frequent battery changes. This capability is particularly valuable for patients with conditions requiring constant monitoring, such as diabetes or heart disease. The potential to improve patient outcomes while reducing the burden on healthcare systems presents a compelling opportunity for WTEG technology. The burgeoning Internet of Things (IoT) ecosystem offers another fertile ground for WTEG applications. As we move towards smart cities and interconnected environments, there's a growing demand for self-powered sensors and data collection devices. WTEGs could power a vast network of wearable or clothing-integrated sensors that continuously collect and transmit data on environmental conditions, personal health metrics, or location information. This opens up possibilities for enhanced urban planning, environmental monitoring, and personalized services. The sports and fitness industry presents another exciting opportunity. High-performance athletes and fitness enthusiasts are always seeking ways to optimize their training and performance. WTEGs could power advanced wearable devices that provide real-time biometric feedback, helping athletes fine-tune their training regimens and prevent injuries. Moreover, the ability to power these devices through body heat aligns well with the active nature of sports, where traditional charging methods may be inconvenient. In the realm of consumer electronics, there's a significant opportunity to address the perennial issue of battery life in everyday wearables. Smartwatches, wireless earbuds, and augmented reality glasses could all benefit from the continuous power provided by WTEGs, potentially extending their operating time indefinitely. This could lead to new product categories and usage scenarios that were previously impractical due to power constraints.

WEARABLE THERMOELECTRIC GENERATORS MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

12.60% |

|

Segments Covered

|

By Type, Distribution Channel and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Alphabet Energy, Evidential Technologies, Ferrotec Corporation, Gentherm Incorporated, Yamaha Corporation, Laird PLC, Perpetua Power Source Technologies, Matrix Industries, II-VI Marlow, Nextreme Thermal Solutions, Thermo Electric Company, TEC Microsystems, Tellurex Corporation, Thermogen Technologies, TEGway

|

Wearable Thermoelectric Generators Market Segmentation: By Types

-

Rigid WTEGs

-

Flexible WTEGs

-

Stretchable WTEGs

-

Textile-integrated WTEGs

-

Nano-engineered WTEGs

Flexible WTEGs are experiencing the most rapid growth in the market due to their versatility and improved wearability. These devices can conform to the contours of the human body, maximizing surface contact and heat transfer efficiency. The ability to integrate seamlessly into various wearable form factors makes flexible WTEGs particularly attractive for applications in consumer electronics, sports and fitness, and healthcare wearables.

Despite the growing popularity of flexible options, rigid WTEGs currently dominate the market in terms of volume and revenue. This dominance can be attributed to their maturity in the market, established manufacturing processes, and higher power output compared to their flexible counterparts.

Wearable Thermoelectric Generators Market Segmentation: By Distribution Channel

-

Direct Sales

-

Online Retailers

-

Specialty Electronics Stores

-

Medical Supply Distributors

-

Sporting Goods Retailers

-

Original Equipment Manufacturers (OEMs)

The online retail channel is experiencing the fastest growth in the WTEG market. This trend is driven by the increasing consumer comfort with online purchases, especially for technology products. Online platforms offer a wide selection of WTEG-powered devices, detailed product information, and the convenience of home delivery.

OEMs currently dominate the distribution landscape for WTEGs. This is primarily because many WTEG applications involve integration into existing product lines of established electronics, healthcare, and sports equipment manufacturers. OEMs purchase WTEGs in bulk to incorporate into their wearable devices, leveraging their existing brand recognition and distribution networks to reach end-users. This channel benefits from long-term supply agreements and close collaboration between WTEG developers and device manufacturers.

Wearable Thermoelectric Generators Market Segmentation: Regional Analysis

-

North America

-

Europe

-

Asia-Pacific

-

South America

-

Middle East and Africa

North America stands as the dominant force in the global Wearable Thermoelectric Generators (WTEG) market, commanding a substantial 35% market share. This pre-eminence can be attributed to a confluence of factors that have created a fertile environment for WTEG technology to flourish.

While currently holding a 25% market share, the Asia-Pacific region is emerging as the fastest-growing market for Wearable Thermoelectric Generators (WTEGs), poised to reshape the global landscape of this technology. This rapid growth is fueled by a unique combination of factors that make the region a hotbed of innovation and adoption in the WTEG space.

COVID-19 Impact Analysis on the Wearable Thermoelectric Generators Market:

In the initial stages of the pandemic, the WTEG market experienced a significant slowdown due to widespread lockdowns and economic uncertainty. Manufacturing facilities faced closures or reduced capacity, leading to production delays and supply chain disruptions. The shortage of key components and raw materials, particularly those sourced from heavily affected regions, created bottlenecks in the WTEG production process. However, as the world adapted to the new reality of living with COVID-19, several factors emerged that have since driven renewed interest and growth in the WTEG market. The pandemic heightened global awareness of health monitoring, creating a surge in demand for wearable medical devices. WTEGs, with their ability to provide continuous power to these devices without the need for regular charging, have seen increased adoption in the healthcare sector. This trend has been particularly pronounced in remote patient monitoring applications, where self-powered devices offer a significant advantage in long-term use scenarios. The shift towards remote work and virtual interactions has also indirectly benefited the WTEG market. As people spend more time at home, there's been a growing interest in wearable technology for fitness tracking, productivity enhancement, and entertainment. This increased usage of wearable devices has highlighted the limitations of traditional battery-powered systems, driving interest in alternative power sources like WTEGs.

Latest Trends/ Developments:

One of the most significant trends in WTEG development is the increasing use of nanotechnology. Researchers are exploring nanostructured materials and quantum dot superlattices to enhance the thermoelectric properties of WTEGs. These nanoscale innovations promise to dramatically improve conversion efficiency, potentially overcoming one of the key limitations of current WTEG technology. The push towards more comfortable and unobtrusive wearables has led to rapid advancements in flexible and stretchable WTEG designs. New fabrication techniques, such as screen printing and 3D printing of thermoelectric materials, are enabling the creation of WTEGs that can conform to complex body contours and withstand repeated deformation without loss of performance. A growing trend is the combination of WTEGs with other energy harvesting technologies, such as photovoltaics or piezoelectric. These hybrid systems aim to provide more consistent power output by leveraging multiple energy sources, addressing the variability inherent in single-source energy harvesting.

Key Players:

-

Alphabet Energy

-

Evidential Technologies

-

Ferrotec Corporation

-

Gentherm Incorporated

-

Yamaha Corporation

-

Laird PLC

-

Perpetua Power Source Technologies

-

Matrix Industries

-

II-VI Marlow

-

Nextreme Thermal Solutions

-

Thermo Electric Company

-

TEC Microsystems

-

Tellurex Corporation

-

Thermogen Technologies

-

TEGway