UV-Curable Bio-based Polymers Market Size (2024 – 2030)

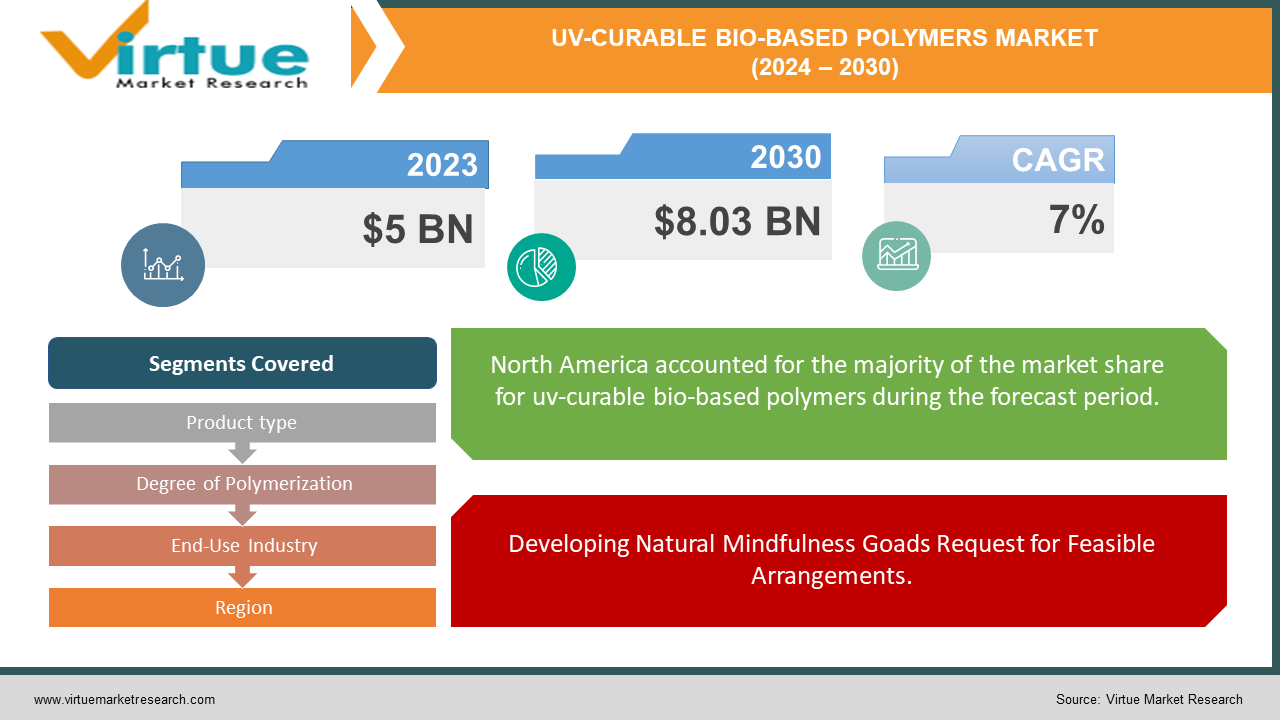

The market for UV-Curable bio-based polymers market was estimated to be worth USD 5 billion in 2023 and is expected to increase to USD 8.03 billion by 2030, with a projected compound annual growth rate (CAGR) of 7% from 2024 to 2030.

The UV-Curable Bio-based Polymers showcase is seeing a critical surge in requests owing to its naturally neighborly nature and flexible applications over different businesses. These polymers, inferred from renewable sources such as plant-based materials, offer a feasible elective to routine petroleum-based polymers, adjusting with worldwide endeavors towards diminishing carbon impression and advancing green advances. With developing mindfulness concerning the natural effect of conventional polymers, there's a striking move towards UV-curable bio-based polymers, driven by exacting controls and expanding shopper inclinations for eco-friendly items. These polymers discover broad applications in coatings, cement, inks, and 3D printing, among others, catering to assorted businesses such as bundling, car, hardware, and healthcare. Besides, headways in UV-curing innovation, coupled with continuous inquiries about and improvement activities, are advanced moving to advertise development, advertising upgraded execution, solidness, and cost-efficiency. As supportability gets to be progressively necessary to commerce procedures, the UV-Curable Bio-based Polymers showcase is balanced for significant extension, showing profitable openings for producers, providers, and end-users alike.

Key Insights:

Adoption of UV-curable bio-based polymers has increased across multiple industries, with the packaging sector accounting for the largest market share of 40%, followed by electronics (25%), automotive (20%), and healthcare (15%).

Technological advancements in UV-curing systems have led to improved efficiency and performance, with the introduction of next-generation LED UV curing technology resulting in a 20% increase in curing speeds and a 15% reduction in energy consumption.

Rising consumer awareness regarding environmental sustainability has driven demand for UV-curable bio-based polymers, with 70% of consumers expressing a preference for eco-friendly packaging materials, contributing to market growth.

Global UV-Curable Bio-based Polymer Market Drivers:

Developing Natural Mindfulness Goads Request for Feasible Arrangements.

One of the essential drivers of worldwide UV-curable bio-based Polymer advertising is the expanding natural awareness among shoppers and businesses alike. With rising concerns approximately climate alter and plastic contamination, there's a developing request for maintainable choices for routine petroleum-based polymers. UV-curable bio-based polymers, determined from renewable sources such as plant-based materials, offer a reasonable arrangement by decreasing dependence on fossil powers, minimizing carbon impression, and advancing circular economy standards. This move towards eco-friendly materials is driving advertising development and cultivating development within the advancement and appropriation of UV-curable bio-based polymers over different applications.

Administrative Activities Advance Selection of Green Advances.

Administrative activities and approaches pointed at diminishing natural effects are playing a critical part in driving the appropriation of UV-curable bio-based Polymers. Governments around the world are actualizing exacting controls and motivating forces to advance the utilization of renewable and feasible materials in fabricating forms. Motivating forces such as charge credits, appropriations, and obtainment inclinations for green items are empowering businesses to move towards UV-curable bio-based polymers, adjusting with supportability objectives and administrative compliance prerequisites. These administrative drivers are fortifying showcase requests and making openings for producers to capitalize on the developing drift towards green innovations.

Mechanical Headways Upgrade Execution and Flexibility.

Mechanical progressions in UV-curable bio-based polymer definitions and handling methods are driving advertise development by improving execution and flexibility. Persistent investigation and advancement endeavors have driven developments in UV-curable gum chemistry, coming about in polymers with moved-forward mechanical properties, grip quality, and solidness. In addition, progressions in UV-curing gear and forms have empowered the advancement of custom-tailored arrangements for particular applications, extending from coatings and cement to 3D printing materials. These mechanical progressions are expanding the application scope of UV-curable bio-based polymers over businesses and driving showcase entrance into modern portions.

Global UV-Curable Bio-based Polymer Market Restraints and Challenges:

Constrained Accessibility and Tall Taken a Toll of Crude Materials.

One of the key challenges confronting the worldwide UV-Curable Bio-based Polymer advertise is the constrained accessibility and taking toll of crude materials determined from renewable sources. Bio-based feedstocks such as plant-based tars and oils are vulnerable to variances in agrarian yields, climate conditions, and competing employments, leading to supply deficiencies and cost instability. Furthermore, the handling and refining of bio-based crude materials frequently include complex and resource-intensive fabricating forms, contributing to higher generation costs compared to petroleum-based partners. These challenges in crude fabric sourcing and fetched competitiveness posture obstructions to showcase the development and appropriation of UV-curable bio-based polymers, especially in price-sensitive businesses and developing markets.

Execution Confinements and Compatibility Issues.

Another restriction within the worldwide UV-Curable Bio-based Polymer advertises is the execution impediments and compatibility issues related to bio-based definitions. Whereas UV-curable bio-based polymers offer natural preferences and supportability benefits, they may show second-rate mechanical properties, grip quality, or chemical resistance compared to ordinary petroleum-based polymers. Besides, compatibility issues with existing UV-curing frameworks added substances, and substrates can ruin the appropriation of UV-curable bio-based polymers in certain applications or businesses. Tending to these execution impediments and compatibility challenges requires continuous investigation and advancement endeavors to make strides in polymer details, upgrade handling procedures, and optimize fabric properties to meet industry guidelines and execution prerequisites.

Administrative and Certification Obstacles.

Administrative and certification obstacles pose extra challenges to the worldwide UV-curable bio-based Polymer advertise, especially concerning compliance with natural directions and certification guidelines. Whereas bio-based polymers are seen as naturally inviting options to ordinary plastics, guaranteeing compliance with rigid controls, certifications, and labeling prerequisites can be complex and time-consuming. Varieties in administrative systems and certification plans over diverse locales and markets assist in compounding the challenge, requiring producers to explore a labyrinth of measures and rules to illustrate item supportability and administrative compliance. Overcoming these administrative and certification obstacles requires collaboration between industry stakeholders, administrative bodies, and standard-setting organizations to set up clear rules, harmonize benchmarks, and streamline certification forms for UV-curable bio-based polymers.

Global UV-Curable Bio-based Polymer Market Opportunities:

Natural Concerns and Controls.

Rising open mindfulness concerning natural supportability is pushing directions toward greener options. Bio-based polymers offer a compelling arrangement, as they are inferred from renewable assets and regularly brag biodegradability compared to conventional petroleum-based alternatives.

Mechanical Progressions.

Inquire about an improvement in bio-based monomers determined from mechanical byproducts like lignin are opening entryways for cost-effective and high-performance UV-curable bio-based polymers. These progressions permit for the creation of polymers with properties that meet the requests of different applications.

Vitality Productivity and Quick Curing.

UV-curing innovation itself presents a major advantage. Compared to conventional curing strategies, UV-curing offers quicker preparation times and lower vitality utilization. This adjusts superbly with the bio-based viewpoint, making a maintainable arrangement.

UV-CURABLE BIO-BASED POLYMERS MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

7% |

|

Segments Covered

|

By Product type, Degree of Polymerization, End-Use Industry, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

BASF SE, DSM, Allnex Group, Arkema Group, Covestro AG, DIC Corporation, Evonik Industries AG, IGM Resins,. Sartomer (Arkema Group), Dymax Corporation, Eternal Materials Co., Ltd., Lambson Limited

|

UV-Curable Bio-based Polymers Market Segmentation: By Product Type

-

UV-curable bio-based Resins

-

UV-curable bio-based Monomers

-

UV-curable bio-based Oligomers

Whereas fragmenting the UV-curable bio-based polymer advertise by item sort offers profitable bits of knowledge, centering on UV-curable bio-based tars gives the foremost impactful point of view for starting an investigation. Not at all like monomers and oligomers, which are building blocks, gums speak to the ultimate defined item. By analyzing gum properties and execution, producers and potential clients pick up a clear understanding of the bio-based polymer's appropriateness for particular applications like coatings, blocks of cement, or 3D printing. This information can at that point be utilized to optimize the underlying monomers and oligomers for way better execution within the last gum item. Moreover, understanding the request for different bio-based tar sorts acts as a compass for advertising patterns, permitting producers to concentrate their endeavors on creating and creating bio-based tars with the most noteworthy potential for victory.

UV-Curable Bio-based Polymers Market Segmentation: By Degree of Polymerization

-

Low Molecular Weight Bio-based Polymers

-

Medium Molecular Weight Bio-based Polymers

-

High Molecular Weight Bio-based Polymers

Digging into the UV-curable bio-based polymer advertise through the focal point of the degree of polymerization (DP) uncovers that medium atomic weight alternatives may be the foremost deliberately noteworthy for introductory examination. Not at all like moo DP polymers that will need craved functionalities or tall DP choices that can be challenging for UV curing, medium DP polymers offer a sweet spot. They give a great adjustment between the mechanical properties required for different applications and the proficient handling empowered by UV curing. This permits for more exact fitting of fabric properties like thickness and quality, making bio-based materials appropriate for a more extensive extent of employment. Besides, the great stream characteristics of medium DP polymers make them perfect for high-volume generation strategies like inkjet printing and roller coating, possibly driving a broader showcase reach and impactful victory for these economical bio-based arrangements.

UV-Curable Bio-based Polymers Market Segmentation: By End-Use Industry

-

Packaging

-

Automotive

-

Electronics

-

Printing & Publishing

-

Healthcare

-

Construction

-

Others

Analyzing the UV-curable bio-based polymer showcase through the focal point of end-use businesses uncovers that centering on the printing & distributing division at first could be the foremost key move. This built-up industry as of now has the framework for UV-curable advances, permitting for a smoother move to bio-based choices by adjusting existing hardware and forms. Besides, the printing & distributing industry is encountering a developing natural thrust, making bio-based polymers with their potential for moved forward recyclability an idealize fit. These feasible materials can cater to a wide extend of applications inside the segment, from inks and varnishes to utilitarian coatings, advertising a wide showcase reach. Moreover, victory in this segment can act as a springboard for more extensive selection. The built-up hones and center on quality inside printing & distributing can give important experiences and clear the way for the acknowledgment of bio-based polymers in other businesses like bundling and gadgets, eventually quickening the, in general, advertise the development of this feasible arrangement.

UV-Curable Bio-based Polymers Market Segmentation: Regional Analysis

-

North America

-

Europe

-

Asia-Pacific

-

South America

-

Middle East & Africa

Analyzing the UV-curable bio-based polymer showcase through the focal point of end-use businesses uncovers that centering on the printing & distributing division at first could be the foremost key move. This built-up industry as of now has the framework for UV-curable advances, permitting for a smoother move to bio-based choices by adjusting existing hardware and forms. Besides, the printing & distributing industry is encountering a developing natural thrust, making bio-based polymers with their potential for moved forward recyclability an idealize fit. These feasible materials can cater to a wide extend of applications inside the segment, from inks and varnishes to utilitarian coatings, advertising a wide showcase reach. Moreover, victory in this segment can act as a springboard for more extensive selection. The built-up hones and center on quality inside printing & distributing can give important experiences and clear the way for the acknowledgment of bio-based polymers in other businesses like bundling and gadgets, eventually quickening the, in general, advertise the development of this feasible arrangement.

COVID-19 Impact Analysis on the Global UV-Curable Bio-based Polymers Market:

The worldwide UV-curable bio-based polymer advertise is on the rise, driven by natural concerns, innovative headways, and a center on real-world execution information. Analyzing the showcase through diverse focal points uncovers a few key experiences centering on medium atomic weight bio-based gums for their adjusted properties and productive handling, and focusing on the built-up printing & distributing industry at first to use existing foundation and natural center. Topographically, North America leads the showcase, but Asia-Pacific appears solid potential. Whereas the COVID-19 widespread caused starting disturbances, it moreover highlighted the potential of these bio-based polymers for cleanliness and maintainability, clearing the way for long-term showcase development.

Latest Trends/ Developments:

The most recent patterns within the UV-curable bio-based polymer showcase highlight a center on high-performance and economical arrangements. Investigate and improvement endeavors are coordinated towards utilizing bio-based monomers inferred from mechanical byproducts like lignin, advertising cost-effective alternatives without relinquishing execution. Furthermore, there's a developing accentuation on medium atomic weight bio-based tars for their flexibility in fitting properties and proficient UV curing. This center on maintainability amplifies to target markets, with the printing & distributing industry being a prime candidate due to its existing UV-cure foundation and natural thrust for eco-friendly materials. In general, advertising is encountering a surge in development and a vital focus on, clearing the way for more extensive appropriation of these bio-based arrangements.

Key Players:

-

BASF SE

-

DSM

-

Allnex Group

-

Arkema Group

-

Covestro AG

-

DIC Corporation

-

Evonik Industries AG

-

IGM Resins

-

Sartomer (Arkema Group)

-

Dymax Corporation

-

Eternal Materials Co., Ltd.

-

Lambson Limited