Global Tow Prepreg Market Size (2024-2030)

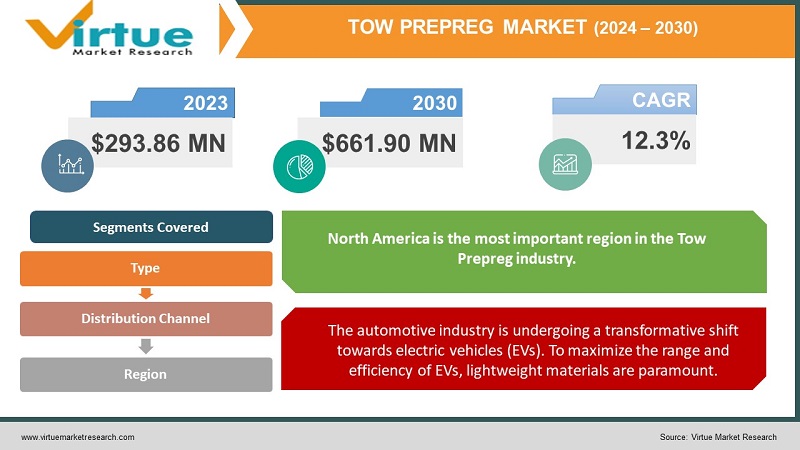

The Global Tow Prepreg Market was valued at USD 293.86 Million in 2023 and is projected to reach a market size of USD 661.90 Million by the end of 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 12.3%.

Within the composite materials industry, the tow prepreg market is a dynamic and quickly developing area. With its composition of glass or carbon reinforcing fibers pre-impregnated with a resin binder, tow prepreg provides special benefits for producing high-performance composite parts. The market for tow prepreg is being driven by an industry-wide obsession with finding lightweight, high-strength materials. Because of their remarkable strength-to-weight ratios, these materials are perfect for situations where reducing weight is crucial. The use of tow prepreg for missile systems, spacecraft structures, and aircraft parts is leading the aerospace and defense industries. Increased payload capacity, better fuel economy, and higher overall performance are all correlated with the ability to produce lightweight, high-performance parts.

Key Market Insights:

Carbon Fiber Prepregs hold a 70% market share due to their exceptional strength-to-weight ratio. Glass Fiber Prepregs hold a 20% market share, offering a cost-effective alternative. Aramid Fiber Prepregs (Kevlar) holds a 10% market share for specific applications requiring high impact resistance.

Epoxy Resins hold an 85% market share, valued for their versatility and mechanical properties. Phenolic Resins hold a 15% market share, offering superior fire resistance but with trade-offs in performance.

Aerospace & Defence holds a 40% market share, utilizing tow prepreg for lightweight, high-strength aircraft components. Automotive holds a 25% market share, adopting tow prepreg for car parts to improve fuel efficiency.

The average Cost of Carbon Fiber Tow Prepreg is $50 - $100 per kilogram (USD) (as of 2024). The estimated Material Cost for a Typical Aircraft Wing is $1 million - $5 million (USD) (using carbon fiber tow prepreg).

Tow Prepreg Market Drivers:

For decades, the aerospace and defense sector has been at the forefront of pushing the boundaries of material science. The relentless pursuit of lighter, stronger, and more durable materials is a constant battle in this industry.

Reducing aircraft weight directly translates to improved fuel efficiency. Lighter aircraft require less fuel to achieve the same level of performance, leading to significant cost savings for airlines and a reduction in environmental impact. Tow prepreg's exceptional strength-to-weight ratio allows for the creation of lightweight yet robust aircraft components, contributing directly to this goal. A lighter aircraft translates to a higher payload capacity. This is crucial for both commercial and military applications. Commercial airlines can carry more passengers and cargo, leading to increased revenue potential. Military aircraft can carry additional weapons, surveillance equipment, or personnel, enhancing their operational capabilities. Lighter aircraft generally exhibit improved maneuverability due to their lower inertia. This is particularly critical for military aircraft engaged in combat situations or high-performance maneuvers. Additionally, the weight reduction can contribute to increased aircraft range, allowing for longer flight times without refueling.

The automotive industry is undergoing a transformative shift towards electric vehicles (EVs). To maximize the range and efficiency of EVs, lightweight materials are paramount.

Battery packs are one of the heaviest components in an EV. Utilizing tow prepreg for battery enclosures can significantly reduce weight, translating to increased driving range on a single charge. Lightweight yet strong components like chassis parts and underbody panels can be constructed using tow prepreg, contributing to overall weight reduction. Tow prepreg's ability to be molded into complex shapes makes it ideal for creating aerodynamic components like spoilers and diffusers, which can improve an EV's energy efficiency. As mentioned earlier, weight reduction is critical for EVs. Tow prepreg's lightweight properties can significantly contribute to extending the driving range of EVs on a single charge. A lighter vehicle generally exhibits better handling and performance. By reducing the weight of key components, tow prepreg can enhance the overall driving experience of EVs.

Tow Prepreg Market Restraints and Challenges:

Carbon fiber is the primary choice for tow prepreg due to its exceptional strength-to-weight ratio. However, it is significantly more expensive compared to traditional materials like steel or aluminum. This high cost can be a barrier for manufacturers, especially for budget-conscious applications. Working with tow prepreg requires specialized equipment and skilled labor. The process itself can be intricate, involving precise handling, layup techniques, and stringent curing procedures. This complexity adds to the overall manufacturing cost, further hindering wider adoption. Research and development efforts focused on creating new, more cost-effective carbon fiber variants would be a game-changer. Additionally, exploring alternative high-performance fibers with lower production costs could offer broader application possibilities. Working with tow prepreg demands a skilled workforce with a deep understanding of composite materials, handling procedures, and quality control measures. A lack of such skilled labor can hinder production capacity and potentially lead to inconsistencies in product quality.

Tow Prepreg Market Opportunities:

Because tow prepreg is biocompatible and can be tailored for strength and flexibility, it is perfect for making lightweight prosthetics and medical implants. Patients may experience increased comfort and movement as a result. The need for thin, light electronics creates opportunities for tow prepreg applications. Because of its excellent strength-to-weight ratio, components for mobile phones, laptop casings, and other consumer electronics may be made thin and strong. Tow prepreg can be used to create lightweight and high-strength components for bridges, buildings, and other infrastructure projects. This can potentially lead to improved load-bearing capacity and reduced construction time. The ever-increasing focus on sustainability presents a significant opportunity for tow prepreg. Its ability to create lightweight components in various industries, such as automotive and aerospace, translates to reduced fuel consumption and lower greenhouse gas emissions. Incorporating AI and machine learning into the manufacturing process can optimize production parameters, streamline quality control, and potentially lead to the development of innovative tow prepreg applications.

TOW PREPREG MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2022

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

12.3%

|

|

Segments Covered

|

By Type, , Distribution Channel and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Hexcel Corporation , Toray Industries, Inc. , Solvay Group , SGL Carbon SE , Teijin Limited , Mitsubishi Chemical Corporation , TCR Composites, Inc. , ENEOs Holdings, Inc. , Porcher Industries , Red Composites Ltd , Vitech Composites , Axiom Materials

|

Tow Prepreg Market Segmentation:

Tow Prepreg Market Segmentation: By Type:

- Carbon Fiber Prepregs

- Glass Fiber Prepregs

- Aramid Fiber Prepregs

Carbon fiber reigns supreme in the tow prepreg market, accounting for roughly 70% of the total share. Carbon fibers boast exceptional strength and stiffness while remaining remarkably lightweight. This translates to significant weight reduction in finished products, making them ideal for applications where every gram counts, such as aerospace and high-performance vehicles Carbon fibers exhibit outstanding tensile strength, compressive strength, and fatigue resistance. These properties make them suitable for components that experience high loads and stresses. Carbon fibers retain their shape exceptionally well under varying temperature and pressure conditions. This dimensional stability is critical for components requiring precise tolerances.

Aramid fibers, most notably Kevlar, are carving a niche in the tow prepreg market, holding an estimated 10% share and experiencing the fastest growth rate among fiber types. Despite its impressive impact resistance, Kevlar remains lightweight and offers good flexibility. This combination makes it suitable for creating protective gear that doesn't restrict movement. Kevlar's strength and thermal stability make it suitable for components in industrial settings where puncture resistance or protection against heat is crucial.

Tow Prepreg Market Segmentation: By Distribution Channel:

- Direct Sales

- Distributors and Resellers

- E-commerce Platforms

Direct Sales channel involves direct interaction between tow prepreg manufacturers and end-user industries. This approach is typically preferred for large-volume orders, complex technical requirements, and close collaboration on project specifications. Tow prepreg is often used in critical applications within industries like aerospace and defense. The complex nature of these applications necessitates close collaboration between manufacturers and end-users. Direct sales facilitate this collaboration, allowing for in-depth discussions about project specifications, material selection, and technical support.

The tow prepreg distribution landscape is likely to witness a dynamic interplay between established channels and the evolving e-commerce segment. Manufacturers may adopt hybrid models, utilizing direct sales for large, complex projects while leveraging e-commerce platforms to reach a broader customer base for smaller orders. E-commerce platforms will likely invest in features that address current limitations, such as offering in-depth product information, technical support resources, and potentially even online configuration tools for tow prepreg selections. Closer collaboration between manufacturers, distributors, and e-commerce platforms can create a more efficient and user-friendly distribution network for the tow prepreg market.

Tow Prepreg Market Segmentation: Regional Analysis:

- North America

- Europe

- Asia-Pacific

- South America

- The Middle East & Africa

With a market share of between 30 and 35 percent, North America is the most important region in the Tow Prepreg industry. Furthermore, the region's emphasis on technological innovation and developments has aided in the creation of innovative composite materials, such as tow prepregs. North America—which consists of the US and Canada—has made a name for itself in the Tow Prepreg industries. A strong manufacturing industry and the presence of significant aerospace and defense industries are responsible for this region's dominance. The aerospace, automotive, and wind energy industries' requirement for lightweight, high-performance materials is what drives the need for tow prepregs in North America. The region's dedication to technical improvements and innovation contributes to the market's growth.

The Asia-Pacific region is considered the fastest-growing market for tow prepregs. With a market share of approximately 25-30%, the region's rapid industrialization, rising demand for lightweight and high-performance materials, and increasing investments in infrastructure development have fueled the growth of the Tow Prepreg market. China has emerged as a major contributor to this growth, driven by its focus on manufacturing, infrastructure development, and commitment to reducing carbon emissions.

COVID-19 Impact Analysis on the Tow Prepreg Market:

Restrictions on movement and border closures hampered the smooth flow of raw materials like carbon fiber and epoxy resins. This shortage of critical inputs led to production slowdowns and price fluctuations for tow prepreg manufacturers. Disruptions in global shipping and air cargo transportation added another layer of complexity. Delays and increased transportation costs further disrupted the timely delivery of tow prepreg to end-user industries. The aviation industry faced a significant decline in passenger and cargo travel due to travel restrictions. This led to a slowdown in aircraft production and a subsequent decrease in demand for tow prepreg, typically used in aircraft components. The automotive industry experienced production shutdowns and a decline in overall vehicle demand during the initial phase of the pandemic. This impacted the demand for tow prepreg used in lightweight car parts, contributing to a market contraction. Lockdowns and social distancing measures dampened participation in recreational activities. This resulted in a decreased demand for sporting goods like bicycles and skis, which utilize tow prepreg for high-performance components. The pandemic highlighted the need for essential medical equipment, such as ventilators and personal protective equipment (PPE). Tow prepreg's lightweight properties and potential for rapid prototyping opened doors for its exploration in these areas.

Latest Trends/ Developments:

While epoxy resins dominate the tow prepreg market, thermoplastics offer distinct advantages. Thermoplastic tow prepregs are faster to cure, offer superior recyclability, and can potentially be welded together, simplifying fabrication processes. Advancements in high-performance thermoplastics like PEEK (polyetheretherketone) and PEKK (polyether ketone ketone) are making them increasingly viable alternatives to epoxy-based tow prepregs. Sustainability is a key concern, and the development of bio-based fibers like those derived from flax, bamboo, or even cellulose offers a promising alternative. While bio-based fibers may not yet match the performance of high-end carbon fibers, advancements in processing techniques and composite design hold promise for their future potential. Developing bio-based or partially bio-derived resins can significantly reduce the environmental footprint of tow prepreg production. Research is ongoing to create high-performance bio-resins with properties comparable to traditional epoxies. Exploring the feasibility of incorporating recycled carbon fibers or other materials into tow prepregs can minimize waste and promote a more circular economy. Technical challenges remain, but advancements in sorting and processing technologies offer promising possibilities.

Key Players:

- Hexcel Corporation

- Toray Industries, Inc.

- Solvay Group

- SGL Carbon SE

- Teijin Limited

- Mitsubishi Chemical Corporation

- TCR Composites, Inc.

- ENEOs Holdings, Inc.

- Porcher Industries

- Red Composites Ltd

- Vitech Composites

- Axiom Materials