Targeted Therapy-based Non-Hodgkin Lymphoma Treatment Market Size (2024 – 2030)

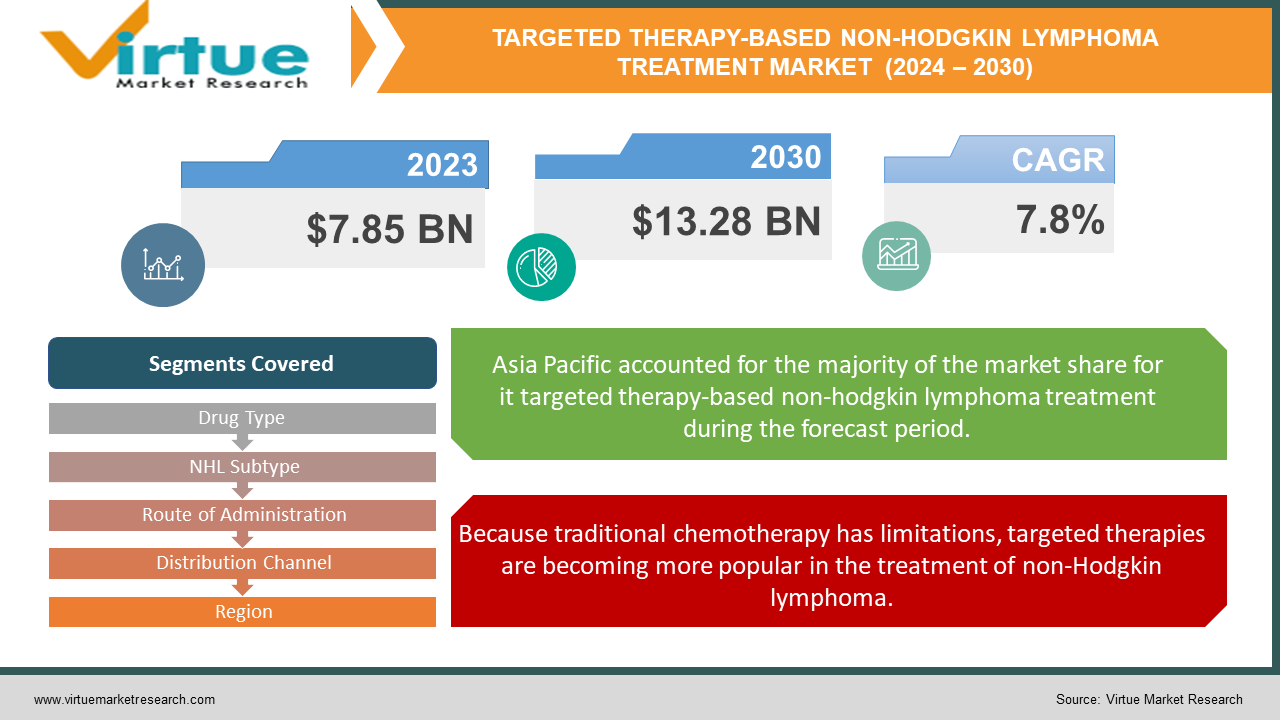

The Global Targeted Therapy-based Non-Hodgkin Lymphoma Treatment Market was valued at USD 7.85 billion in 2023 and is projected to reach a market size of USD 13.28 billion by 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 7.8%.

One possible method of treating non-Hodgkin lymphoma is through targeted treatments. Compared to typical chemotherapy, these medicines offer a more targeted approach by taking advantage of certain weaknesses present in cancer cells. Small molecule medications and monoclonal antibodies are two different kinds. Rituximab is one example of a monoclonal antibody that functions like an assassin by binding to proteins on the surface of cancer cells and designating them for the immune system to destroy. Ibrutinib and other small-molecule medications interfere with internal signalling pathways that support the development and survival of cancer cells. Targeted therapies are frequently used in conjunction with other treatments, which may increase their efficacy and lessen their negative effects. They are not a foolproof treatment for NHL, and like other medications, they can have adverse effects that differ from one another. It's important to explore risks and advantages with your doctor if you're thinking about targeted treatment for NHL.

Key Market Insights:

At a compound annual growth rate of 7.8%, the non-Hodgkin lymphoma (NHL) targeted therapy market is projected to reach USD 16.64 billion by 2032 on a global scale. The increasing incidence of NHL worldwide, increased funding for the discovery and development of innovative targeted treatments, and the expanding need for safer and more efficient treatment alternatives are the main drivers of this expansion.

By 2032, the targeted treatment market for NHL is expected to generate USD 9.6 billion from the B-cell lymphoma type segment. The high frequency of B-cell lymphomas and the efficacy of targeted therapy in the treatment of various NHL subtypes account for this dominance.

In 2023, North America accounted for the biggest revenue share of targeted treatments in the treatment of NHL, with a market share of approximately 35.4%. This dominance can be ascribed to elements such as the widespread adoption of pricey targeted medicines, the high prevalence of NHL, and the robust healthcare infrastructure.

Because of its efficacy, immunotherapy is seen as a developing therapeutic option for the treatment of NHL. Because targeted treatments can target certain disease vulnerabilities and may have better side effect profiles than standard chemotherapy, they are still anticipated to play an important role in the treatment of cancer.

Global Targeted Therapy-based Non-Hodgkin Lymphoma Treatment Market Drivers:

Because traditional chemotherapy has limitations, targeted therapies are becoming more popular in the treatment of non-Hodgkin lymphoma.

Due to the shortcomings of conventional chemotherapy, there is a growing need for tailored medicines for the treatment of non-Hodgkin lymphoma (NHL). Chemotherapy is a useful treatment, but it also frequently has serious side effects that can drastically lower a patient's quality of life. These adverse effects might include everything from weariness and nerve damage to nausea and hair loss. Here's where tailored medicines show great promise. Targeted medicines operate like snipers, carefully targeting weaknesses unique to cancer cells, in contrast to the wide approach of chemotherapy. This targeted assault may increase therapy effectiveness while reducing the frequency and intensity of adverse effects. Patients may benefit from better treatment results as a result, possibly leading to an improved quality of life both during and after therapy. The growing market for targeted treatments in the treatment of non-Hodgkin lymphoma is largely due to this shift in preference towards them, which is motivated by the need for both lower toxicity and increased efficacy.

A ray of hope for subtypes that are incurable Targeted Treatments for Non-Hodgkin Lymphoma: Meeting Unmet Needs

Even though targeted medicines have completely changed the way NHL is treated, there are still a lot of unmet medical needs for NHL subtypes. Aggressive subtypes are very difficult to treat and frequently don't have any choices. The market for tailored therapy enters the picture at this point and offers some optimism. Pharmaceutical firms are aggressively developing innovative targeted medicines especially tailored to solve therapy gaps, motivated by a mission to improve patient outcomes. The distinct vulnerabilities of these difficult NHL subtypes are the focus of these next-generation medicines. The market could dramatically enhance NHL treatment options and give hope to patients who had few alternatives in the past by effectively developing tailored medicines for these neglected patient populations. The market for targeted therapies is expanding due in large part to this emphasis on unmet medical needs, which is pushing the envelope in treatment and providing hope for many NHL patients.

Global Targeted Therapy-based Non-Hodgkin Lymphoma Treatment Market Restraints and Challenges:

Although there are obstacles, the worldwide market for targeted treatments for non-Hodgkin lymphoma (NHL) appears promising. Exorbitant expenses restrict patient access, particularly in areas where healthcare finances are tight. The release of these potentially life-saving therapies is delayed by strict constraints. Furthermore, the variety of NHL subtypes makes the creation of treatments that work for everyone difficult. Although tailored medicines provide benefits over conventional methods, they are not infallible. Resistance can grow over time, and some patients might not react at all. Even while side effects from chemotherapy are often less severe, they can still happen. The market is anticipated to expand despite these obstacles because of things like the growing prevalence of NHL, higher funding for research, and patient demand for new treatment alternatives. The process of removing obstacles is in progress. Pharmaceutical firms are working on better treatments with the intention of surpassing resistance and increasing efficacy while lowering prices. Regulatory agencies are looking for methods to speed up approvals without sacrificing security. Additionally, healthcare organisations are looking for ways to increase patient access, such as value-based pricing and more extensive insurance coverage. Targeted treatments hold the potential to transform the treatment of NHL and greatly enhance patient outcomes by surmounting these obstacles.

Global Targeted Therapy-based Non-Hodgkin Lymphoma Treatment Market Opportunities:

Exciting potential abound in the worldwide market for targeted therapeutics for non-Hodgkin lymphoma (NHL). First off, there is a substantial unmet medical need for efficient therapies for NHL subtypes. This offers a fantastic opportunity for businesses to create tailored treatments to fill in these gaps. Second, targeted medicines that are customised to each patient's specific genetic composition and cancer mutations are made possible by advances in precision medicine. Treatments that are more effective and have fewer adverse effects may result from this customised approach. The integration of targeted medicines with other treatments, like as immunotherapy or chemotherapy, is a viable avenue for improving treatment results. Moreover, the growing incidence of NHL in emerging nations opens new markets. This promise may be realised by working together to create cost-effective targeted medicines, establish insurance coverage channels, and improve healthcare infrastructure. Finally, the development of even more potent tailored therapeutics for NHL may be sped up by the application of technology innovations like artificial intelligence and big data. By taking advantage of these chances, the market for NHL-targeted therapies has the potential to develop significantly and contribute significantly to global patient outcomes improvements.

TARGETED THERAPY-BASED NON-HODGKIN LYMPHOMA TREATMENT MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

7.8% |

|

Segments Covered

|

By Drug Type, NHL Subtype, Route of Administration, Distribution Channel, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

AbbVie Inc., AstraZeneca, Bayer AG, Bristol Myers Squibb Company, CELGENE CORPORATION (Bristol Myers Squibb Company), Genentech, Inc. (F. Hoffmann-La Roche Ltd), Kite Pharma, Inc. / Gilead Sciences, Inc., Kyowa Kirin Co., Ltd., Merck & Co., Inc., Novartis AG, Sanofi, Teva Pharmaceutical Industries Ltd., Janssen Pharmaceuticals, Inc., Spectrum Pharmaceuticals, Inc., Takeda Pharmaceutical Company Limited

|

Global Targeted Therapy-based Non-Hodgkin Lymphoma Treatment Market Segmentation: By Drug Type

-

Monoclonal Antibodies

-

Small Molecule Drugs

Monoclonal antibodies are the undisputed champions in the targeted therapy market for Non-Hodgkin Lymphoma (NHL), boasting the largest and fastest growing segment. Their rise to prominence is fueled by their ability to precisely target cancer cells, proven effectiveness, generally milder side effects, and continuous development of even better versions. While small molecule drugs remain important, monoclonal antibodies are leading the charge in the fight against NHL with targeted therapies.

Global Targeted Therapy-based Non-Hodgkin Lymphoma Treatment Market Segmentation: By NHL Subtype

As the biggest and fastest-growing subset of Non-Hodgkin Lymphoma (NHL), Diffuse Large B-Cell Lymphoma (DLBCL) dominates the targeted treatment market. The reason for this dominance is that DLBCL is the most prevalent NHL subtype, reacts favourably to current treatments like Rituximab, and has generated a lot of interest in further research for more precisely targeted therapies. Although other subtypes also reap benefits, DLBCL's dominant position in this targeted therapy industry is cemented by its prevalence, treatment response, and continued research.

Global Targeted Therapy-based Non-Hodgkin Lymphoma Treatment Market Segmentation: By Route of Administration

Although intravenous (IV) distribution is still the norm, the subcutaneous (sub-q) portion of the targeted treatment market for non-Hodgkin lymphoma (NHL) is growing at an exponential rate. Convenience, maybe shorter hospital stays, and a potentially improved patient experience because of simpler administration and less pain are all benefits of this rapidly expanding approach. Nonetheless, there are now obstacles such as restricted drug supply in sub-q formulations and possible injection site responses. Alongside traditional IV administration, sub-q delivery is set to become a major force as additional treatment choices become accessible sub-q and healthcare practitioners gain confidence with this method.

Global Targeted Therapy-based Non-Hodgkin Lymphoma Treatment Market Segmentation: By Distribution Channel

-

Hospital Pharmacies

-

Retail Pharmacies

-

Online Pharmacies

A clear leader in the distribution channels for targeted treatments for non-Hodgkin lymphoma (NHL) is unclear due to the market's complexity. Hospital pharmacies are now the best because of their knowledge, connections to healthcare specialists, and safety procedures. Future expansion of retail pharmacies may be possible if laws are loosened, more pharmacists receive training, and copay assistance programmes proliferate. Strict restrictions and safety concerns impose constraints on online pharmacies, impeding their potential for substantial expansion.

Global Targeted Therapy-based Non-Hodgkin Lymphoma Treatment Market Segmentation: By Region

-

North America

-

Asia-Pacific

-

Europe

-

South America

-

Middle East and Africa

Due to a combination of variables, the Asia-Pacific region is quickly rising to the top of the Non-Hodgkin Lymphoma (NHL) targeted treatment market. This market is developing because of an increasing number of people who are at risk for NHL, better access to diagnostics and healthcare facilities, more public knowledge of the illness, and developments in the economy that make these pricey medicines more affordable.

COVID-19 Impact Analysis on the Global Targeted Therapy-based Non-Hodgkin Lymphoma Treatment Market:

The market for targeted therapies for non-Hodgkin lymphoma (NHL) was affected by the COVID-19 pandemic. Healthcare concentrated on COVID-19, clinical studies stagnated, and supply systems broke. Then again, opportunities came. The emphasis on healthcare systems may have raised awareness of the NHL and enhanced access to care through telemedicine. Most critically, more research is being done to create safer, more focused treatments for NHL patients with impaired immune systems. The market's ability to overcome these obstacles and seize these new opportunities will determine its destiny.

Recent Trends and Developments in the Global Targeted Therapy-based Non-Hodgkin Lymphoma Treatment Market:

Targeted therapeutics for non-Hodgkin lymphoma (NHL) are seeing rapid innovation in the worldwide market. The emergence of precision medicine, which customises therapies based on each patient's specific genetic composition for better outcomes and fewer adverse effects, is a significant development. To enhance results, researchers are also looking at potent combos of targeted medicines with other medical interventions like immunotherapy. Targeted medicines are also being developed to address unmet medical requirements in certain NHL sub-types, providing much-needed hope to a great number of patients. The search for even more potent tailored medicines is accelerating because of technological innovations like artificial intelligence and big data. There is a new market potential because of the rising NHL burden in developing nations, where efforts are being made to enhance healthcare infrastructure, offer inexpensive medications, and broaden insurance coverage. In addition to interfering with clinical trials and perhaps postponing diagnosis, the COVID-19 pandemic has accelerated the use of telemedicine, which may ultimately increase patient access. Furthermore, the pandemic's emphasis on susceptible groups has accelerated the development of tailored treatments that reduce immunosuppression. The market for targeted therapies in NHL has the potential to transform treatment and greatly enhance patient outcomes by leveraging these promising developments and navigating current obstacles.

Key Players:

-

AbbVie Inc.

-

AstraZeneca

-

Bayer AG

-

Bristol Myers Squibb Company

-

CELGENE CORPORATION (Bristol Myers Squibb Company)

-

Genentech, Inc. (F. Hoffmann-La Roche Ltd)

-

Kite Pharma, Inc. / Gilead Sciences, Inc.

-

Kyowa Kirin Co., Ltd.

-

Merck & Co., Inc.

-

Novartis AG

-

Sanofi

-

Teva Pharmaceutical Industries Ltd.

-

Janssen Pharmaceuticals, Inc.

-

Spectrum Pharmaceuticals, Inc.

-

Takeda Pharmaceutical Company Limited