Asia Pacific Smoothies Market

The Asia Pacific smoothies’ market is expected to grow from approximately USD 4.5 billion in 2025 to around USD 8.5 billion in 2030, at a compound annual growth rate of around 12.8% during 2025-2030.

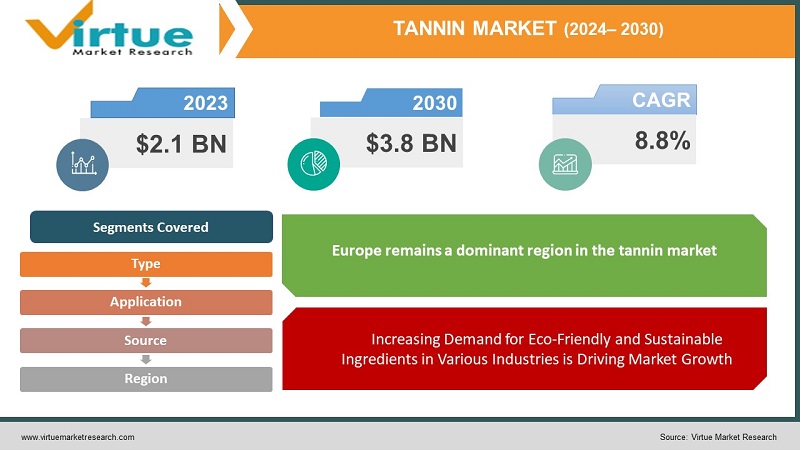

Explore reportIn 2023, the global tannin market was valued at USD 2.1 billion and is expected to reach USD 3.8 billion by 2030, growing at a CAGR of 8.8% during the forecast period.

The market’s expansion is driven by the rising adoption of plant-based tannins in leather processing, the increasing use of tannins in the food and beverage industry (especially in wine production), and growing applications in healthcare and pharmaceuticals due to their antioxidant and anti-inflammatory properties. Furthermore, advancements in extraction technologies and the development of innovative tannin-based products for industries such as cosmetics and adhesives are expected to drive further growth in the coming years.

Key Market Insights:

Condensed tannins, which are mainly derived from tree bark and plants, dominate the market, accounting for more than 55% of the total market share. They are widely used in the leather tanning and wine production industries.

The plant-based tannin segment is projected to witness the fastest growth due to increasing consumer preference for natural, sustainable, and eco-friendly products, especially in Europe and North America.

Leather tanning remains the largest application segment, representing more than 40% of the global market demand, as tannins are extensively used in processing leather to improve its durability and quality.

Wine production is a significant application, particularly in regions like Europe and South America, where tannins are used to enhance the taste, color, and stability of wines. The growing global demand for premium wines is contributing to the increased usage of tannins in this sector.

Asia-Pacific is expected to be the fastest-growing region, driven by the rapid expansion of industries such as leather, pharmaceuticals, and wine production in countries like China and India.

Global Tannin Market Drivers:

Global Tannin Market Challenges and Restraints:

Market Opportunities:

The Global Tannin Market presents several opportunities for growth, particularly in the cosmetics industry, the development of bio-based adhesives, and the increasing focus on sustainable packaging. The rising demand for natural and organic ingredients in skincare and cosmetic products offers significant growth potential for tannins. Tannins are known for their antioxidant and anti-aging properties, making them an ideal ingredient for anti-wrinkle creams, moisturizers, and sunscreens. The trend towards clean beauty and the avoidance of synthetic chemicals in cosmetics is expected to create new opportunities for tannin-based formulations in the global beauty industry. The development of bio-based adhesives for use in industries such as construction, automotive, and packaging presents a significant opportunity for the tannin market. Tannins can be used as natural adhesives due to their ability to form strong bonds with other materials. As industries seek to reduce their reliance on petrochemical-based adhesives and adopt more sustainable practices, tannin-based adhesives are gaining traction as a viable alternative. The increasing focus on sustainable packaging solutions in response to growing environmental concerns offers new opportunities for tannin-based products. Tannins can be used to develop biodegradable and recyclable packaging materials that reduce the environmental impact of plastic waste. The shift towards eco-friendly packaging in industries such as food and beverages, cosmetics, and consumer goods is expected to drive demand for tannin-based packaging solutions.

TANNIN MARKET REPORT COVERAGE:

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2023 - 2030 |

|

Base Year |

2023 |

|

Forecast Period |

2024 - 2030 |

|

CAGR |

8.8% |

|

Segments Covered |

By Type, Application, source, and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regional Scope |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Key Companies Profiled |

Tannin Corporation, Laffort SA, Sappi Limited, Tanac SA, Mimosa Extract Company (Pty) Ltd, Forestal Mimosa Ltd, Silvateam S.p.A, Naturex SA, W. ULRICH GmbH, Polson Ltd |

Tannin Market Segmentation:

Condensed tannins hold the largest market share due to their widespread use in leather tanning, wine production, and adhesive manufacturing. Hydrolyzable tannins are gaining popularity in pharmaceuticals and cosmetics due to their bioactive properties, while phlorotannins, derived from brown algae, are used in niche applications such as health supplements and personal care products.

Plant-based tannins dominate the market, with their extraction from sources like tree bark, leaves, and fruits being the most common. Brown algae-based tannins are emerging as a promising source, particularly in health supplements and pharmaceuticals, due to their antioxidant and anti-inflammatory properties.

The leather tanning segment remains the largest application, driven by the continued demand for leather products in the fashion, automotive, and furniture industries. Wine production is another significant application, especially in Europe and South America, while pharmaceuticals and cosmetics are expected to be the fastest-growing segments.

Tannin Market Segmentation Regional :

Europe remains a dominant region in the tannin market, due to the high demand for tannins in wine production and leather processing. Countries like France, Italy, and Spain are leading in wine production, driving the demand for tannins. Rapid industrialization and the growing leather and pharmaceutical industries in countries like China, India, and Japan are propelling the growth of the tannin market in the region. The wine industry, particularly in Argentina and Chile, is fueling the demand for tannins in this region. Moderate growth is expected as industries like leather processing and pharmaceuticals adopt tannin-based products.

The COVID-19 pandemic had a mixed impact on the global tannin market. The slowdown in industrial activities, particularly in the leather and wine industries, led to a temporary decline in demand for tannins. However, the market quickly rebounded as economies reopened and industries resumed production. In the pharmaceutical and healthcare sectors, the pandemic accelerated the adoption of tannin-based products due to their health benefits, such as immune-boosting and antioxidant properties. Post-pandemic, the market is expected to grow steadily, driven by increased demand for natural and sustainable products across various industries.

Latest Trends/Developments:

The growing focus on sustainability has led to the development of tannin-based adhesives for use in industries such as construction and automotive. New research is exploring the use of tannins in treating chronic diseases, including cancer and cardiovascular conditions, due to their antioxidant and anti-inflammatory properties. As the fashion industry moves towards cruelty-free products, vegan leather alternatives, which often use tannins in their production, are gaining popularity.

Key Players:

The Tannin Market was valued at USD 2.1 billion in 2023 and is projected to reach USD 3.8 billion by 2030, growing at a CAGR of 8.8%.

Key drivers include the increasing demand for natural and sustainable ingredients, the growing applications of tannins in pharmaceuticals and healthcare, and the rising demand for premium wines.

The market is segmented by type (hydrolyzable, condensed, phlorotannin), source (plant, brown algae), and application (leather tanning, wine production, pharmaceuticals, others).

Europe dominates the market, driven by the high demand for tannins in wine production and leather processing.

Leading players include Tannin Corporation, Laffort SA, Sappi Limited, and Tanac SA.

Joining thousands of companies around the world committed to making the Excellent Business Solutions.

Specify your preferred Countries, Segments, or timeframes

Unlock Country Level Outlook, Trends, Cross-country Comparability, or supply Chain Variations.

Analyst Support

Every order comes with Analyst Support.

Customization

We offer customization to cater your needs to fullest.

Verified Analysis

We value integrity, quality and authenticity the most.