Super Engineering Plastics Market Size (2024 – 2030)

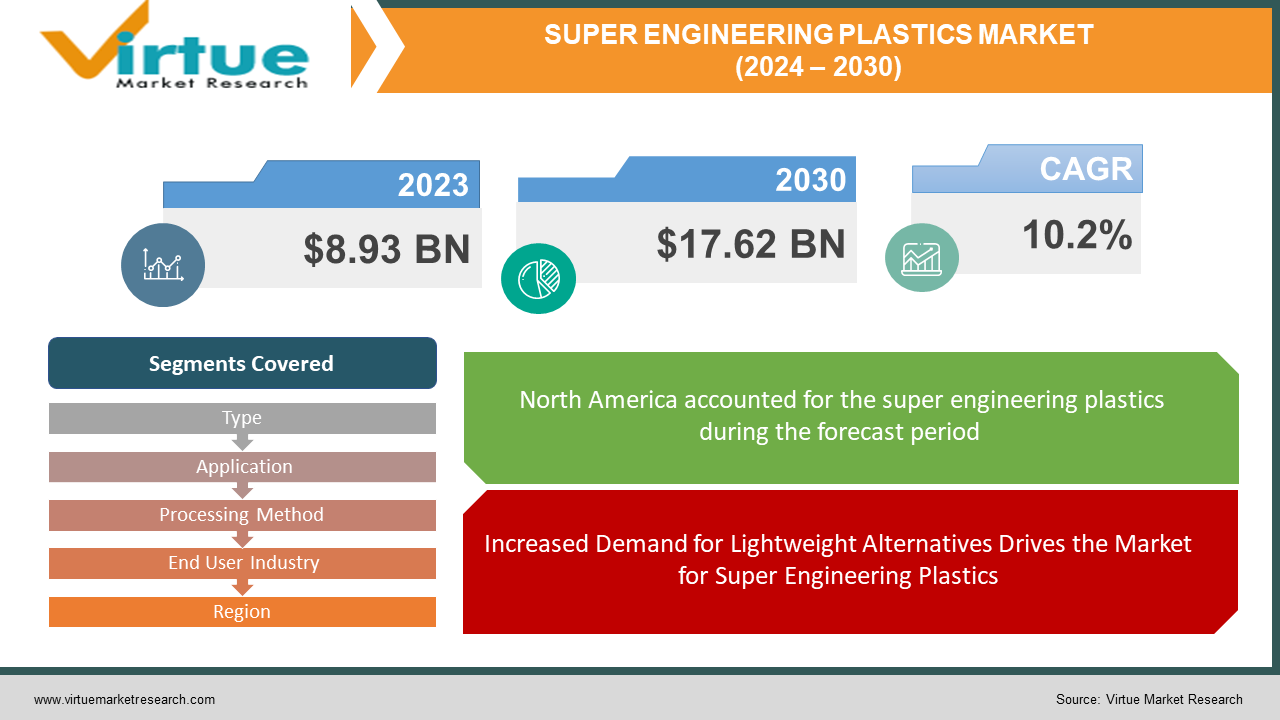

The market for global super engineering plastic market is expanding quickly; it was estimated to be worth USD 8.93 billion in 2023 and is expected to increase to USD 17.62 billion by 2030, with a projected compound annual growth rate (CAGR) of 10.2% from 2024 to 2030.

As super-engineered plastics navigate the complex realm of cutting-edge materials, the global market for these materials is growing and evolving drastically. Super engineering polymers are a vital component of many industries, such as aerospace, automotive, healthcare, and electronics, due to their exceptional mechanical, chemical, and thermal properties. This business is expanding due to the increasing need for lightweight, high-performance materials that can withstand harsh environments. It also encourages innovation and efficiency in product design and production processes. To introduce new formulations and enhance the overall performance of super-engineering plastics, major players in the market are focusing on research and development. The market is impacted by international campaigns that support sustainable practices, with an increased emphasis on the impact on the environment and recyclability. The expectation is that the global super-engineering plastics market will expand gradually as long as technology continues to advance and offer solutions that enhance the performance of contemporary industrial applications.

Key Market Insights:

Significant market insights enable decision-makers to fully understand the dynamics that shape an industry. These insights address key factors such as market size, trends, drivers, issues, and opportunities that impact the competitive environment. The growing need for high-performance materials, advancements in polymer science technology, and expanding applications across a range of industries are key insights from the Global Super Engineering Plastics Market. Market players closely monitor these insights to be strategic and competitive as they adapt to shifting regulatory landscapes and customer expectations. Moreover, having a solid understanding of regional variations and global economic factors enhances one's ability to navigate the complexities of the super-engineered plastics industry. Important market insights essentially serve as a compass, guiding industry participants toward growth and sustainability in a rapidly evolving business environment.

Global Super Engineering Plastics Market Drivers:

Increased Demand for Lightweight Alternatives Drives the Market for Super Engineering Plastics.

The need for lightweight materials is growing in many different industries, which is driving a significant upswing in the global super-engineered plastics market. It's interesting to note that these high-performance polymers are currently the preferred material in sectors like electronics, aviation, and automotive where having materials that combine strength and low weight is essential. Super-engineering plastics are essential to fulfilling the industry's demand for enhanced performance and efficiency, as seen by the way the market has responded to this need, positioning them as a major player in the global lightweight materials scene.

Advancements in Technology Push Super Engineering Plastics to the Front.

The continual technical advancements in polymer research are driving a revolutionary age in the advanced materials field, which is being experienced by the global super engineering plastics market. Research and development efforts have produced novel formulations that give these plastics increased chemical resistance, mechanical strength, and thermal stability. Thanks to this technological capability, super-engineering plastics are positioned as cutting-edge solutions, meeting the ever-evolving demands of industries searching for materials with better characteristics and performance.

The market landscape for super-engineering plastics is shaped by sustainability.

Due to stakeholders' increased focus on recyclable material development and ecologically responsible manufacturing methods, the worldwide super engineering plastics market is evolving. The way the market has responded to this sustainability initiative shows how committed the industry is to addressing environmental issues as more people engage in eco-friendly activities. Because of their exceptional qualities and potential for recycling, super-engineering plastics are in a unique position to impact the future of material innovation by meeting industry and regulatory sustainability expectations.

Global Super Engineering Plastics Market Restraints and Challenges:

Managing Affordability: Rising Production Costs Are a Barrier to the Growth of the Super Engineering Plastics Market.

The high cost of manufacture is one of the main challenges facing the market for super engineered polymers. Production costs rise because these materials require sophisticated manufacturing processes and state-of-the-art technologies. This limits the wide application of super engineering polymers across multiple industries and calls into question their cost. Manufacturers must strike a careful balance between maintaining the quality of their products and looking into more cost-effective ways to make them in order to meet this challenge.

Green Obstacles: Handling Environmental Sustainability and Regulatory Compliance in the Super Engineering Plastics Environment.

Strict legislation governing safety and environmental standards poses a serious threat to the market for super-engineered polymers. Adequate funds must be set aside for research and development to ensure adherence to these regulations, which cover material composition, disposal protocols, and recycling guidelines. To ensure the sustainability and environmental responsibility of highly engineered polymers, industry players must strike a balance between innovation and compliance with evolving regulatory frameworks.

Breaking the Mould: Super Engineering Plastics Face Difficulties with Market Saturation and Competition.

Super engineering plastics are seriously threatened by other materials such as metals, composites, and traditional engineering plastics. One challenge is persuading industries of the new materials' enhanced performance; another is overcoming market saturation in certain applications. The industry must carefully position itself against competing materials by emphasising unique features, toughness, and adaptability while exploring untapped markets to sustain growth.

Global Super Engineering Plastics Market Opportunities:

Boosting Efficiency: Super Engineering Plastics Acquire Popularity in the Aerospace and Automotive Industries.

The market for super-engineered plastics has a lot of potential due to the expanding needs of the automotive and aerospace industries. These industries are increasingly looking for lightweight, high-performance materials to increase vehicle and airplane fuel efficiency. Super-engineering plastics' exceptional mechanical properties and heat resistance put them in a perfect position to meet these demands. Super engineered polymers offer a feasible route for market expansion as automakers continue to focus on reducing vehicle weight and improving overall performance in structural, interior, and engine parts.

Super Engineering Plastics Thrive in Electronic and Electrical Innovations: Wired for Success.

The rapid development of electronic devices and electrical components offers super engineering plastics a significant future. With the advancement of consumer electronics, telecommunications, and electrical equipment, there is an increasing need for materials with superior electrical insulation, flame resistance, and dimensional stability. Super engineering plastics are perfect for applications such as electrical device housing, insulators, and connections because of their unique combination of properties. Manufacturers who offer specialised solutions for electrical and electronic applications might profit from the increasing technological integration that is occurring across multiple industries.

Green Horizons: Super Engineering Plastics Grab Chances for Eco-Friendly Remedies.

In light of rising environmental consciousness and a shift towards sustainability, super-engineered plastics have a great opportunity to promote themselves as ecologically friendly alternatives. Producing recyclable or bio-based super engineering plastics will allow manufacturers to satisfy the growing market for eco-friendly goods. This has the dual advantage of meeting legal obligations related to environmental standards and consumer demands for items that are more sustainable and green. Companies who invest in R&D to create environmentally friendly formulas may gain a competitive edge in the marketplace.

SUPER ENGINEERING PLASTICS MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

10.2% |

|

Segments Covered

|

By Type, Application, Processing Method, End User Industry, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Toray, DIC, Solvay, Celanese, Kureha , SK Chemical, Tosoh, Sumitomo Chemical, SABIK, Evonik

|

Super Engineering Plastics Market Segmentation: By Type

The global super engineering plastics market is large in terms of material kinds, and it includes important sectors like polyamide-imide (PAI), polyphenylene sulphide (PPS), polyetheretherketone (PEEK), and polyimides (PI). Each variety exhibits distinct qualities that satisfy specific industry requirements. PPS is widely used in industrial, automotive, and electrical applications because of its well-known chemical resistance and flame-retardant properties. Because of its exceptional mechanical strength and ability to withstand high temperatures, PEEK is extensively utilised in the electronics, medical, and aerospace industries. Polyimides are ideal for application in the electronics, automotive, and aerospace industries due to their exceptional heat stability.

PAI delivers a strength-to-temperature resistance ratio that is perfect for demanding technical applications by combining the best features of polyamides and polyimides. In the super engineering plastics market, this segmentation fosters creativity and application diversity by allowing businesses to choose materials tailored to their specific requirements. One of the best super engineering polymers on the market is polyetheretherketone, or PEEK, because of its efficiency and versatility. PEEK is a material that possesses exceptional mechanical properties, including strong chemical resistance, wear resistance, and high tensile strength. Its resistance to temperatures as high as 260°C (500°F) makes it useful in high-stress industries including aerospace, automotive, and medical equipment. PEEK's biocompatibility is one of the main reasons it is utilised in many medical implants.

Super Engineering Plastics Market Segmentation: By Application

-

Injection Molding

-

Extruded

-

Molded

Based on the many production processes that are employed to transform these innovative materials into finished products, the super engineering plastics market is split into distinct divisions. Extrusion, injection moulding, and moulded applications are the three primary categories. Injection moulding is a commonly employed technique that proves particularly effective for intricate and intricate shapes. Utilising a mould to hold molten, highly designed polymers, this process yields incredibly accurate and consistent parts. On the other hand, extrusion creates profiles, sheets, and tubes continuously by forcing the material through a specially constructed die.

Moulds can be used for a wider range of shaping processes than just extrusion and injection moulding. Industries can select the optimal manufacturing method based on the complexity, production volume, and intended end product thanks to this segmentation. Among all the applications, Injection Moulding is one of the most effective ways to manufacture highly designed polymers. Because of its precision and versatility, injection moulding is particularly useful for producing small, delicate parts. Because this technique enables producers to achieve precise tolerances and homogeneity in the final product, it is effective in industries requiring complicated designs, such as electronics and automotive.

Super Engineering Plastics Market Segmentation: By Processing Method

-

Injection Molding

-

Blow Molding

-

Extrusion

The key processes for producing and developing these cutting-edge materials are defined by a market segmentation based on the processing techniques employed by the super engineering plastics industry. In this specific context, extrusion, blow moulding, and injection moulding are common processes. Injection moulding is a popular technique for complex designs and large-scale production since it entails pumping molten super engineering polymers into a mould to make precise and accurate components. In contrast, blow moulding involves the inflation of a heated plastic tube within a mould to create hollow objects.

Injection moulding is among the most practical processing techniques for super-engineered polymer sculpture. When it comes to generating elaborate, precise, and complex parts with a high level of consistency and precision, this technique excels. Its versatility makes it perfect for a wide range of applications, particularly in industries like the automotive, electronics, and medical device sectors where precision and complexity are essential. Injection moulding allows for the creation of intricate designs and tight tolerances, ensuring that the final product meets stringent quality standards.

Super Engineering Plastics Market Segmentation: By End User Industry

-

Automotive

-

Electrical & Electronics

-

Aerospace

-

Medical

To reflect the diverse variety of businesses using these state-of-the-art materials, the market for super engineering plastics is segmented into end-user industries. Super engineered polymers are employed in lightweight structural, engine, and interior components in the automotive industry, which is one of the key markets. The electrical and electronics industry benefits from the materials' superior electrical insulation, flame resistance, and durability for applications such as connections, housings, and insulators. Because super-engineered polymers can be utilised for structural components, engine parts, and aircraft interiors, the aerospace industries benefit from their exceptional mechanical strength and thermal resistance. Because these materials are biocompatible, meaning they may be used in implants and medical equipment, the medical industry uses them.

Super-designed polymers are most helpful in the aerospace industry out of all the end-user industries. These materials fully fulfil the stringent standards of aeronautical applications due to their great mechanical strength, lightweight, and temperature resistance. Aeroplane engine parts, interior parts, and structural components are made in large quantities using super-engineered polymers, especially Polyetheretherketone (PEEK) and Polyimides (PI). These materials' ability to withstand extreme conditions, like high temperatures, makes them crucial for extending the lifespan and functionality of aircraft components.

Super Engineering Plastics Market Segmentation: Regional Analysis

-

North America

-

Asia-Pacific

-

South America

-

Europe

-

Middle East & Africa

The market for super engineered plastics is deliberately distributed among several regions, each of which enhances the company's overall image. Europe holds a sizable 30% market share, largely due to its strong manufacturing base and focus on technical advancements. Asia-Pacific is not far behind, with a noteworthy 20% market share, indicating the region's prominence as a manufacturing powerhouse in sectors such as aerospace, automotive, and electronics. With a 20% market share, North America is heavily represented in industries like automobiles and medical devices. South America, the Middle East, and Africa make up emerging markets with the capacity to grow, with a combined share of 5%. This distribution demonstrates how the market for super engineering plastics is global and how various geographical areas have distinct effects on the industry's dynamics. As industries look for novel materials and demand changes, regional disparities in market share are anticipated to shift, opening up opportunities for cross-continental collaboration and innovation.

COVID-19 Impact Analysis on the Global Super Engineering Plastics Market:

The exceptional consequences of the COVID-19 pandemic have created major obstacles for the global market for super-designed polymers. The outbreak caused supply chain disruptions, which delayed production and reduced the availability of raw materials. Lockdowns and travel restrictions implemented in some countries also led to a decrease in production activities and a slowdown in end-user industry demand, particularly in the electronics, automotive, and aerospace sectors. Due to the uncertainty surrounding the extent and duration of the epidemic, prudent spending and delayed investment decisions affected the overall dynamics of the market. But the crisis also made clear how important resilience and flexibility are to supply chain management. Superengineering plastics are expected to see growth as industries gradually recover and adapt to the new normal. The ongoing need for high-performance materials in essential applications will drive this expansion. Companies that can better their product offerings, respond to changing consumer needs, and adjust to the challenges posed by the pandemic will likely perform better in the post-COVID-19 environment.

Latest Trends/ Developments:

Several notable trends and changes are influencing the edible mushroom market in Latin America. One noteworthy trend in the area is the growing adoption of plant-based diets as a flexible and healthful alternative to meat. This is consistent with the broader movement towards selecting more sustainably produced and healthier meals. Intriguing and delicious options are needed for menus in homes and restaurants as a result of the growing interest in exotic mushroom species among foodies. Growing environmental consciousness has also led to advancements in cultivation technologies in the sector, with a focus on sustainable and organic farming practices. Furthermore, the mushroom sector has adopted additional e-commerce channels as a result of the COVID-19 pandemic. In the face of worldwide unpredictability, businesses are strengthening their resilience by localising production, diversifying their suppliers, streamlining their supply chains, and developing strategic alliances. It is advisable to consult recent industry publications and news sources for up-to-date information on the newest advancements and to gain real-time insights into the ever-changing super engineering plastics market.

Key Players:

-

Toray

-

DIC

-

Solvay

-

Celanese

-

Kureha

-

SK Chemical

-

Tosoh

-

Sumitomo Chemical

-

SABIK

-

Evonik

The global super engineering plastics market is dominated by major players such as Toray, DIC Corporation, Solvay, Celanese, Kureha, SK Chemicals, Tosoh, Sumitomo Chemical, SABIC, and Evonik. Every company contributes to the market's vibrancy by utilising its expertise and broad product offering to promote innovation and set industry standards. The innovative materials from Toray, the specialist polymers from Solvay, and the global presence of SABIC work together to shape the competitive landscape and propel advancements in the high-performance plastics industry.