Smart Faucet Market Size (2024-2030)

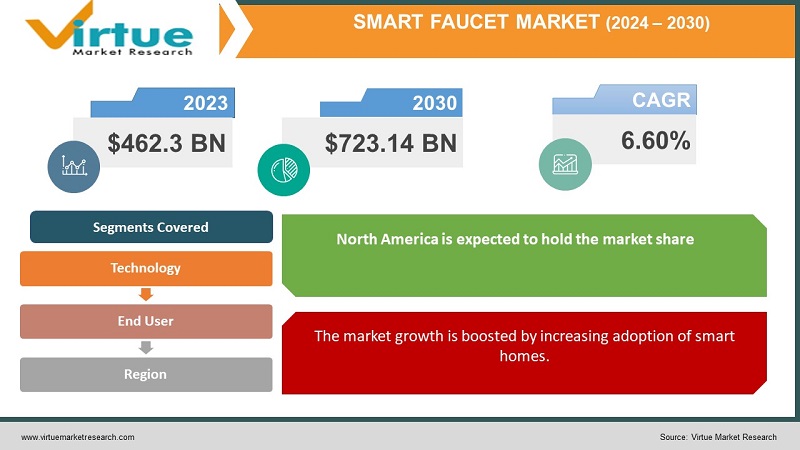

The Smart Faucet Market was valued at USD 462.3 billion in 2023 and is projected to reach a market size of USD 723.14 billion by the end of 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 6.60%.

The global smart plumbing market is expected to witness significant growth in the near future due to the growing adoption of smart home systems, increasing focus on user-friendliness, and increasing for smart faucet services. Also, this industry has been fueled by the growing need to conserve water and the growing awareness of the environmental impact of water pollution. The smart faucet market has experienced significant growth in recent years as consumers increasingly seek products that are not only functional, but also high-tech. Using smart apps, voice commands or motion sensors, smart faucets can be controlled. Among the many benefits they provide is increased hygiene, quality and water conservation.

Key Market Insights:

Booming at a 6.60% CAGR, the smart faucet market is witnessing strong growth, which is increasing the demand for advanced home automation solutions. With a focus on water conservation and the combination of high-end technologies, more and more resources are being achieved very quickly. The market is driven by features such as contactless operation, sensor control, and compatibility with smart environments. Increasing awareness about the quality and cleanliness of water, along with the growing trend for luxury and convenience in residential and commercial settings, is driving the market expansion. In addition, the integration of the Internet of Things (IoT) enables users to monitor and control water consumption through mobile applications, increasing the interest of smart pipes. The leading players are constantly innovating to introduce efficient and attractive designs, creating a competitive landscape. As smart homes expand, the smart faucet market is expected to see steady growth, offering both environmental benefits and a better user experience.

Smart Faucet Market Drivers:

The market for smart faucets are growing due to water conservation.

The growing demand for water conservation is one of the main factors driving the growth of the smart faucets market. In many parts of the world, water scarcity is becoming a major problem, so people are looking for ways to use less water. By automatically turning off water when not needed and providing real-time information on water consumption, smart faucets can reduce water consumption. This is very important in countries where water scarcity is a major problem, such as those prone to drought, and in areas where water is a valuable and expensive resource, such as in some parts of Europe. Many features of smart faucets can help save water.

The market growth is boosted by increasing adoption of smart homes.

The growing use of smart homes is the second major factor driving the growth of the smart faucets market. Consumer interest in automating their homes and controlling voice-activated devices or smartphones is increasing due to technological advancements. For a seamless, automated experience, smart faucets can be integrated with other intelligent home appliances such as voice assistants and lighting controls. In developed countries such as the United States and Europe, the use of luxury homes has increased in recent years.

Smart Faucet Market Restraints and Challenges:

The market is hampered by the high cost of smart faucets.

One of the main challenges of smart faucets is their cost. Compared to traditional faucets, smart faucets are more expensive. This high price can be a deterrent for many buyers, especially those who have not yet been convinced of the benefits of smart faucets. Additionally, installation costs can be high if the faucet needs to be modified to accommodate the smart faucet. While long-term savings from water savings can offset initial costs, consumers may be reluctant to invest in products they perceive to be too expensive.

The growth of the market is restrained by the compatibility of smart faucets.

Another important challenge for smart faucets is compatibility. Good faucets often require different types of faucets, and may not fit all sinks or countertops. This limits the options available to consumers and makes it difficult to upgrade their existing sink or countertop with smart appliances. In addition, smart faucets may not be compatible with all home systems or voice assistants, which can cause confusion for consumers.

Smart Faucet Market Opportunities:

The smart faucet market offers significant opportunities related to changing consumer preferences, technological advancements, and increased focus on sustainable living. With the growing awareness of water conservation, smart faucets offer attractive solutions by combining features such as automatic shut-off, speed control and time monitoring. Market growth opportunities also come from the integration of artificial intelligence (AI) and machine learning algorithms, enabling faucets to adapt to user behavior and optimize water consumption. The growing trend of smart home adoption is creating relationships, driving the opportunity for plumbing to become an integral part of the connected environment. In addition, partnerships with home automation platforms and partnerships with major water management companies can improve market penetration. The growing business sector, including restaurants and companies, represents another way for the adoption of smart faucets, driven by the demand for a solution that does not touch and clean. As technology advances, the smart faucet market is poised for continued growth and various opportunities in the residential and commercial sectors.

SMART FAUCET MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

6.60%

|

|

Segments Covered

|

By Technology, end user, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

LIXIL Group Corporation, Kohler Co., GROHE AG, TOTO Ltd., Sloan Valve Company, Masco Corporation, Jaquar Group, Pfister, Delta Faucet Company, Oras Group

|

Smart Faucet Market Segmentation:

Smart Faucet Market Segmentation: By Technology:

- Touchless Technology

- Hybrid Technology

- Voice-Activated Technology

- Manual Override Technology

In 2023, based on the Technology, Touchless technology is the most popular and widely accepted technology in smart faucets, accounting for a large share of the market. Touchless technology will continue to dominate the smart faucet market due to the increasing demand for touchless hygiene solutions. This hybrid technology segment is also expected to grow, driving the need to accommodate diverse user preferences and business settings. Voice-activated technology is an emerging segment, and its adoption is likely to grow as consumers become more familiar with smart home technology. The manual control technology segment is expected to have a small market share, resulting in users who need flexibility between contactless and manual modes of operation.

Touchless technology has become a game-changer in the global smart faucet market, redefining the user experience and redefining hygiene standards. The growing demand for hands-free solutions, fuelled by increasing health and hygiene awareness, is a key factor driving the growth of touchless technology in smart faucets. The combination of sensors and infrared technology allows users to use faucets without physical contact, reducing the risk of germ transmission and improving overall hygiene. Besides public health concerns, the growing affinity for smart home solutions and the convenience they offer is contributing to the growing adoption of touchless smart devices. The technology is not only compatible with modern lifestyles, but also addresses water conservation concerns with features such as automatic shut-off. As a result, touchless technology serves as a key enabler in the continued growth of the global faucet market, with innovative, performance-focused and employee welfare.

Voice-activated technology has become a transformative force, having a major impact on the global smart faucet market. The convenience and hands-free functionality offered by voice-activated systems, such as voice-activated water, has been a key driver of adoption. Factors contributing to the growth of voice-controlled technology in the smart faucet market include the increasing adoption of smart home environments, the rise of virtual assistants such as Amazon's Alexa and Google Assistant, and increasing improvements focusing on cleanliness and contactless communication. Consumers are drawn to the seamless control and customization options provided through voice commands, creating an engaging user experience. As voice technology continues to improve, the smart pipe market is seeing increasing demand, especially in the home environment. The advantage of being able to control water flow and temperature is consistent with a wide range of home automation systems. This combination of voice-activated technology not only improves user comfort, but also positions smart faucets as essential elements of a modern, integrated home.

Smart Faucet Market Segmentation: By End User

As smart home technology is widely adopted and kitchen and bathroom renovations become popular, the residential sector is expected to hold the market share. Rising water bills and increasing focus on sustainability are other factors driving the demand for smart faucets in the residential market. The demand for cleanliness, automation and water conservation in businesses, institutions and companies can drive the growth of the business market. Due to their hygienic design and the need to stop the transmission of germs, touchless smart faucets are especially popular in the professional market. Also, increasing use of automation and smart technology in the business environment is expected to increase the use of smart pipes in this market.

The business sector plays an important role in the growth of the global smart faucets market, with many factors contributing to its expansion. The increased attention to cleanliness and non-touch solutions, especially in public spaces such as hotels, restaurants and offices, has promoted the rapid adoption of smart devices. The hospitality industry, in particular, is seeing an increase in demand for these high-tech light fixtures aimed at improving the user experience and ensuring cleanliness. Additionally, integrating smart faucets into business environments fits sustainability goals, contributing to water conservation efforts. The growing trend of smart homes and the integration of IoT in the business space is increasing the market. As business prioritizes quality and environmental services, the impact of smart faucets on the global market is great, making the relationship between technological innovation and business infrastructure development.

Smart Faucet Market Segmentation: Regional Analysis:

- North America

- Asia-Pacific

- Europe

- South America

- Middle East and Africa

Due to increasing adoption of smart home technology and concerns about personal hygiene in public spaces, North America is expected to hold the market share. Due to strict regulations of water conservation and growing concern about public hygiene, Europe is also expected to contribute to the market. Due to its growing population, urbanization, and increasing interest in water conservation and personal hygiene, the Asia Pacific region is expected to witness the fastest market growth. The need for water safety and cleanliness, as well as the increasing adoption of smart home technology, contribute to moderate growth forecasts for the rest of the world. Overall, the smart faucets market is expected to grow significantly across all regions due to the convenience, water conservation and hygiene benefits offered by smart faucets.

The Asia Pacific region is a central player shaping the state of the global smart faucets market, with a combination of growing factors influencing its dynamics. Emerging cities, rising disposable income, and increased awareness of water conservation practices in countries such as China, India, and Japan are driving the adoption of water pipes. These countries are seeing the rise of smart home infrastructure, creating fertile ground for the integration of advanced water conservation technologies. The impact of smart faucets in the Asia Pacific region transcends regional boundaries, affecting the global market. As the regional economy continues to grow, the demand for innovative and sustainable solutions in residential and commercial environments is driving the quality pipe market. In addition, collaborations and partnerships between regional and international players are helping to leverage the various opportunities presented by the Asia Pacific market, thus shaping the evolution of smart faucets globally.

COVID-19 Impact Analysis on the Smart Faucet Market:

The impact of the COVID-19 pandemic on the smart faucet industry has been overwhelming. While the pandemic has reduced production and disrupted supply chains, it has increased the demand for hygiene and contactless solutions in public and private spaces. The demand for touch-free and automatic faucets has increased as people become more aware of the dangers of transmitting germs from commonly handled surfaces. In addition, as more people spend more time at home and look for ways to make their homes more comfortable and convenient, the pandemic has spurred the development of smart home technologies, such as smart pipes. However, the economic impact of the pandemic has also led to a reduction in consumer spending, which may affect the growth of the smart faucets market in the near future.

Latest Trends/ Developments:

The smart faucet market is awash with innovation, moving from drain to drain. Voice-activated faucets like Moen's Flo allow for hands-free control, while Kohler's Sensate faucet has a temperature sensor that displays the temperature of the water on an LED ring. Sanitizing using non-touch models like Delta's Trinsic Touch2O®, prevents the spread of germs. Stability is eliminated by micro-detection and water-saving features such as Grohe Smart Control, which reduce volume by up to 70%. Beyond wet, luxury showers like TOTO's Neorest NX feature a hairdryer and Chroma therapy for a spa experience. As technology integrates into everyday devices, the smart faucet market is poised to boom.

Key Players:

- LIXIL Group Corporation

- Kohler Co.

- GROHE AG

- TOTO Ltd.

- Sloan Valve Company

- Masco Corporation

- Jaquar Group

- Pfister

- Delta Faucet Company

- Oras Group

- January 2022 – Moen launches a smart faucet that will work completely hands-free, using gestures to control temperature and flow.