Smart Building Market Size (2024 – 2030)

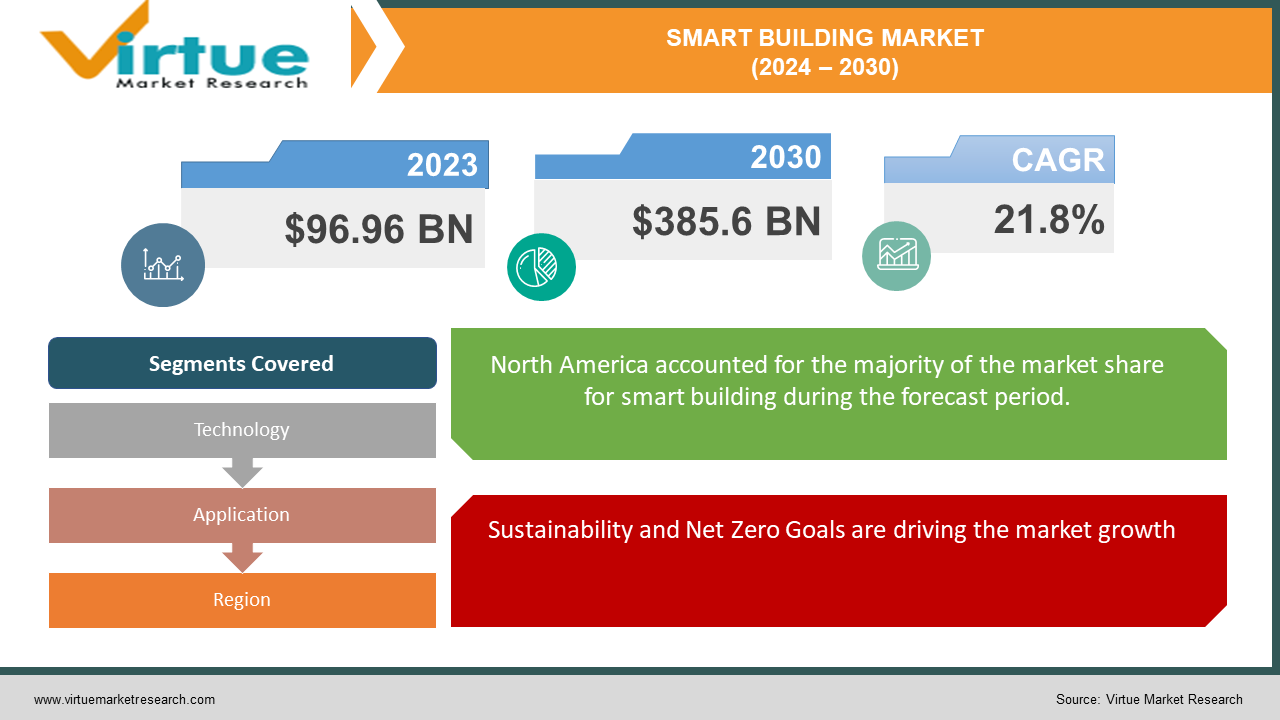

The Global Smart Building Market was valued at USD 96.96 billion in 2023 and will grow at a CAGR of 21.8% from 2024 to 2030. The market is expected to reach USD 385.6 billion by 2030.

The Smart Building Market refers to the global market for technologies and services that enable intelligent and connected buildings. These buildings utilize various technologies like IoT, AI, and cloud computing to automate and optimize building systems, leading to improved energy efficiency, enhanced occupant comfort, and increased operational efficiency. The market encompasses a wide range of solutions, including Building Automation Systems (BAS), lighting control systems, HVAC systems, security and access control systems, and energy management systems. Rising energy costs and environmental concerns are driving the adoption of smart building solutions that optimize energy consumption and reduce carbon footprint.

Key Market Insights:

This market is currently dominated by the commercial building segment and the North American region ( market share 32.1%), but other regions like Asia Pacific and Europe are experiencing significant growth.

The proliferation of IoT, cloud computing, and artificial intelligence (AI) is enabling the development of sophisticated smart building systems and services.

Growing government regulations and incentives aimed at promoting sustainability and energy efficiency are accelerating smart building adoption.

Smart buildings offer improved comfort, convenience, and safety for occupants, leading to increased productivity and well-being.

Global Smart Building Market Drivers:

Increased Demand for Energy Efficiency is driving the market growth

The rising tide of energy costs and climate change concerns is driving a significant shift towards smart building technologies. These innovative solutions offer a powerful arsenal for optimizing energy consumption, leading to tangible reductions in carbon footprint and operational expenses. Smart building systems provide real-time data on energy usage across various building functions like heating, ventilation, and lighting. This granular insight empowers building managers to identify and address inefficiencies, such as unoccupied spaces being unnecessarily heated or cooled. Additionally, smart automation can dynamically adjust systems based on real-time occupancy and weather conditions, further minimizing energy waste. By implementing these intelligent strategies, smart buildings can achieve significant energy savings, translating to substantial cost reductions and a smaller environmental impact.

Sustainability and Net Zero Goals are driving the market growth

The global push for sustainability and net-zero emissions has placed smart buildings at the forefront of the solution. These intelligent systems offer a powerful toolset for optimizing energy usage, minimizing waste, and improving resource management, contributing significantly to environmental goals. By leveraging real-time data and automation, smart buildings can drastically reduce energy consumption, leading to lower carbon footprints and operational costs. Additionally, smart water management systems and waste reduction strategies further enhance the sustainability profile of a building. Furthermore, the adoption of smart solutions can contribute to achieving coveted green building certifications, enhancing a building's value and attractiveness to tenants who increasingly prioritize environmentally responsible spaces.

Growing Focus on Building Management and Occupant Comfort is driving the market growth

Building management and occupant comfort are intricately linked in the realm of smart buildings. These intelligent systems offer a plethora of features that enhance the overall experience for both building managers and occupants. Personalized temperature control allows individuals to adjust their immediate environment for optimal comfort, while smart lighting systems automatically adapt to ambient conditions or occupancy levels, creating a more energy-efficient and user-friendly space. Additionally, air quality monitoring systems provide real-time data on indoor air quality, ensuring a healthy and comfortable environment for occupants. For building managers, the benefits are equally significant. Centralized control systems offer a unified platform for managing and monitoring various building functions, streamlining operations, and reducing manual workload. Real-time data insights gleaned from smart sensors and devices enable proactive maintenance and problem identification, minimizing downtime and ensuring smooth building operations. By prioritizing both occupant comfort and efficient building management, smart buildings create a win-win scenario for all stakeholders

Global Smart Building Market challenges and restraints:

High Initial Investment is restricting the market growth

The initial investment required for smart building technologies can be a significant hurdle, particularly for smaller businesses and organizations with limited budgets. This encompasses the cost of hardware like sensors and actuators, software platforms for management and control, installation and configuration services, and ongoing maintenance and support. While the long-term benefits of energy savings and operational efficiency are substantial, the initial financial outlay can be a barrier to entry, especially for smaller players who may lack the capital or resources to invest in these advanced systems. This challenge necessitates exploring alternative financing models, such as leasing or pay-as-you-go solutions, to make smart building technologies more accessible to a wider range of organizations.

Lack of Awareness and Expertise is restricting the market growth

Despite the potential benefits of smart buildings, a lack of awareness and expertise can significantly hinder their adoption. Many building owners and managers remain unfamiliar with the full range of smart building technologies and their capabilities. This lack of understanding creates hesitation and uncertainty about the potential return on investment and the technical complexities involved. Additionally, a shortage of skilled professionals who can design, install, and manage smart building systems poses a challenge. This limited expertise can lead to inefficient implementation, compatibility issues, and ongoing operational difficulties. Overcoming this barrier requires increased education and awareness campaigns, highlighting the tangible benefits of smart buildings and showcasing successful case studies. Additionally, fostering collaboration between technology providers, building owners, and educational institutions can bridge the knowledge gap and create a more skilled workforce for the smart building industry.

Market Opportunities:

The smart building market presents a plethora of exciting opportunities for technology providers and building owners alike. The increasing focus on energy efficiency, driven by rising costs and environmental concerns, creates a strong demand for smart solutions that optimize energy consumption. Advancements in technologies like IoT, AI, and cloud computing enable the development of sophisticated systems and services, further fueling market growth. Additionally, government regulations and incentives aimed at sustainability are pushing the adoption of smart buildings. Beyond these core drivers, opportunities lie in leveraging data-driven insights for building optimization, integrating AI for predictive maintenance and personalized experiences, and addressing cybersecurity concerns through robust security measures. Finally, the market is witnessing rising demand from non-traditional sectors like healthcare, offering further avenues for growth and innovation.

SMART BUILDING MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

21.8% |

|

Segments Covered

|

By Technology, Application, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Honeywell, Siemens, Schneider Electric, Johnson Controls, ABB, Cisco, Bosch, Legrand, Control4, Tridium

|

Smart Building Market Segmentation - By Technology

-

Building Automation Systems (BAS)

-

Lighting Control Systems

-

HVAC Systems

-

Security and Access Control Systems

-

Energy Management Systems

Building Automation Systems (BAS) currently hold the dominant position. BAS acts as the central nervous system, integrating and managing various smart building technologies like HVAC, lighting, and security systems. This centralized control allows for optimized energy consumption, improved occupant comfort, and enhanced operational efficiency. As the demand for intelligent buildings continues to rise, BAS is expected to remain the most crucial and widely adopted segment in the smart building market.

Smart Building Market Segmentation - By Application

-

Commercial Buildings

-

Residential Buildings

-

Industrial Buildings

The commercial building segment currently reigns supreme within the smart building market. This dominance is driven by several factors, including the increasing focus on energy efficiency and cost reduction in commercial real estate. Additionally, stringent government regulations and growing awareness of sustainability are pushing commercial building owners to adopt smart solutions. Hotels, healthcare facilities, and corporate offices are leading the charge, implementing smart technologies for improved operational efficiency, enhanced occupant comfort, and reduced environmental impact. This trend is expected to continue, solidifying the commercial building segment as the leading force in the smart building market.

Smart Building Market Segmentation - Regional Analysis

-

North America

-

Asia-Pacific

-

Europe

-

South America

-

Middle East and Africa

North America currently holds the dominant position in the smart building market, boasting a significant share of the global market. Other regions like Asia Pacific and Europe are catching up quickly, presenting exciting growth opportunities. Asia Pacific, with its rapidly developing economies and increasing urbanization, is expected to witness significant growth in the smart building market. Europe, with its strong focus on environmental sustainability, is also making strides in adopting smart building technologies.

COVID-19 Impact Analysis on the Global Smart Building Market

The COVID-19 pandemic had a significant impact on the global smart building market, initially causing a slowdown due to economic uncertainty and disruptions in construction and supply chains. However, the pandemic also highlighted the importance of building health, safety, and sustainability, leading to a renewed interest in smart building technologies that could address these concerns. The focus shifted towards features like improved air quality monitoring, touchless access control, and enhanced energy efficiency to create healthier and more sustainable building environments. Additionally, the rise of remote work and hybrid work models emphasized the need for flexible and adaptable building systems that could cater to changing occupancy patterns and space utilization needs. While the initial impact was disruptive, the long-term outlook for the smart building market remains positive. The growing awareness of the benefits of smart buildings, coupled with government initiatives and technological advancements, is expected to drive continued growth in the coming years. The pandemic has catalyzed the market, accelerating the adoption of smart building technologies and solidifying their role in creating healthier, more sustainable, and efficient buildings for the future.

Latest trends/Developments

The smart building market is buzzing with exciting developments. The integration of renewable energy sources like solar panels and wind turbines is gaining traction, contributing to energy independence and sustainability goals. Additionally, the concept of "Building-as-a-Service" (BaaS) is gaining momentum, offering flexible and pay-as-you-go models for accessing smart building technologies, making them more accessible to a wider range of organizations. Human-centric design is also taking center stage, with a focus on creating spaces that prioritize occupant comfort, well-being, and productivity. This includes features like personalized lighting, temperature control, and air quality monitoring, all tailored to individual needs and preferences. Furthermore, advancements in AI and machine learning are enabling predictive maintenance, anomaly detection, and automated building operations, leading to improved efficiency and reduced downtime. As the market evolves, the focus is shifting towards seamless integration of various smart building systems and devices, ensuring interoperability and maximizing the potential of these intelligent solutions.

Key Players

-

Honeywell

-

Siemens

-

Schneider Electric

-

Johnson Controls

-

ABB

-

Cisco

-

Bosch

-

Legrand

-

Control4

-

Tridium