Silicone Liquid Injection Molding Market Size (2024-2030)

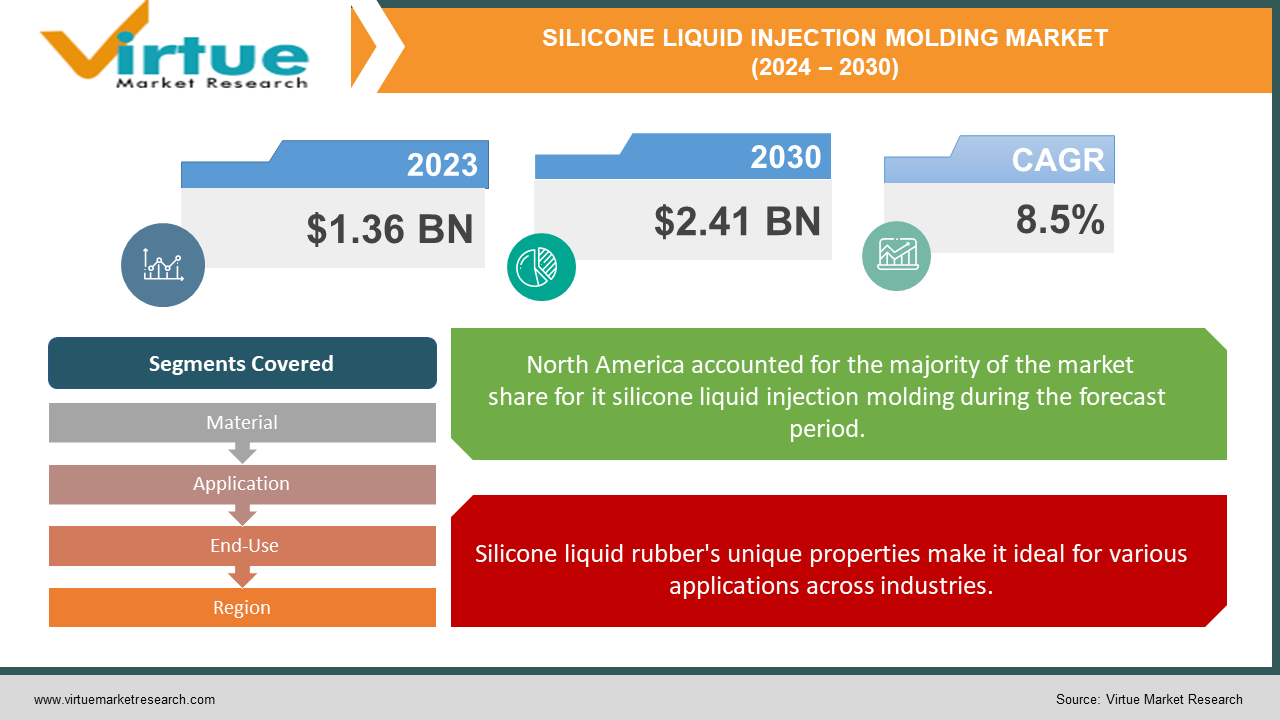

The Silicone Liquid Injection Molding Market was valued at USD 1.36 billion in 2023 and is projected to reach a market size of USD 2.41 billion by the end of 2030. Over the cast period of 2024 – 2030, the figure for requests is projected to grow at a CAGR of 8.5%.

The silicone liquid injection molding market is flourishing, driven by the rising demand for silicone liquid rubber (LSR) across diverse industries. LSR boasts impressive properties like high heat resistance, making it ideal for automotive parts. In the medical field, its biocompatibility and chemical resistance make it perfect for implants and catheters. LSR's safety and durability are valued in consumer goods, while its electrical insulation properties are crucial for miniaturized and reliable electronic devices.

Key Market Insights:

The silicone liquid injection molding market is experiencing significant growth, driven by the increasing demand for silicone liquid rubber (LSR) across various industries. LSR boasts exceptional properties that make it a versatile material. It can withstand high temperatures, making it ideal for automotive parts (gaskets, seals) that experience heat fluctuations. LSR is also chemically resistant, a crucial factor for medical devices (implants, catheters) that need to function flawlessly within the body. Additionally, LSR is biocompatible, meaning it doesn't harm human tissue, and this characteristic makes it perfect for consumer goods like baby bottle nipples and pacifiers.

This versatility of LSR is fueling market growth. The automotive industry, driven by the need for lightweight and fuel-efficient vehicles, is a key consumer of LSR. Similarly, the medical device sector, with its growing focus on minimally invasive surgeries and catering to an aging population, is heavily reliant on LSR. Consumer goods manufacturers are increasingly adopting LSR due to its safety and durability, while the electrical & electronics industry utilizes LSR to create miniaturized and reliable devices.

With these factors propelling demand, the silicone liquid injection molding market is expected to reach a value of US$2.41 Billion by 2030, growing at a steady rate of approximately 8.5% annually. This indicates a strong future for the market, as LSR continues to be a vital material across various sectors.

The Silicone Liquid Injection Molding Market Drivers:

Silicone liquid rubber's unique properties make it ideal for various applications across industries.

Silicone liquid rubber (LSR) stands out as a true game-changer due to its exceptional and multifaceted properties. Its remarkable ability to withstand high temperatures without warping or losing shape makes it an ideal material for automotive parts, particularly gaskets and seals that experience constant heat fluctuations within a vehicle's engine. Furthermore, LSR's exceptional chemical resistance allows it to remain unaffected by a wide range of chemicals, making it a critical material for medical devices like implants and catheters that need to function flawlessly within the human body for extended periods.

The automotive industry's focus on fuel efficiency is driving demand for LSR in lightweight car parts.

The automotive industry's relentless pursuit of fuel efficiency is a major driver for the silicone liquid injection molding market. As car manufacturers strive to create lighter vehicles that consume less fuel, the demand for components that can withstand high temperatures without adding excessive weight becomes paramount. Silicone liquid rubber, with its exceptional heat resistance and lightweight properties, perfectly addresses this need.

LSR's biocompatibility and chemical resistance make it perfect for medical devices used in minimally invasive surgeries.

The medical device sector is witnessing a significant rise in the use of LSR due to its biocompatibility and superior chemical resistance. As minimally invasive surgeries become increasingly popular due to their faster recovery times and reduced patient discomfort, the need for medical devices that can function flawlessly within the human body becomes even more critical. Silicone liquid rubber, with its biocompatible nature that minimizes the risk of rejection, and its exceptional chemical resistance that ensures it doesn't degrade when exposed to bodily fluids, perfectly meets these requirements.

The emphasis on safe and durable consumer goods is leading to a rise in LSR usage.

Consumer goods manufacturers are placing a heightened emphasis on safety and long-lasting durability, leading to a significant increase in the utilization of LSR. Since LSR is non-toxic and possesses exceptional resistance to wear and tear, it is ideally suited for a wide range of consumer products, particularly those intended for children or those that come into frequent contact with food. For instance, LSR's safety and biocompatibility make it a perfect choice for baby bottle nipples and pacifiers, while its durability ensures these products can withstand repeated use and sterilization. This focus on safety and long-lasting performance in the consumer goods sector is propelling the silicone liquid injection molding market forward.

The Silicone Liquid Injection Molding Market Restraints and Challenges:

The silicone liquid injection moulding market, despite its promising growth, faces certain challenges. A significant hurdle is the high cost of Molds. Unlike traditional moulding techniques, silicone liquid injection moulding requires specialized and expensive tooling. This high initial investment can be a burden for smaller manufacturers who may struggle to justify the upfront expense. Furthermore, the moulding process itself is more complex. This intricate procedure necessitates skilled labour and specialized equipment, which can add to overall production costs. Another challenge lies in the limited availability of LSR. While the material offers exceptional properties, the range of colours and specific property modifications may be restricted. This limitation can hinder design flexibility and may not always fulfil the precise needs of certain applications. Additionally, silicone liquid injection moulding often has longer cycle times compared to other techniques. This can be a disadvantage for high-volume production runs, impacting overall efficiency. Finally, there are some environmental concerns associated with the curing process for LSR, which can generate emissions. While LSR is generally considered sustainable, manufacturers are actively seeking solutions to minimize the environmental impact of this process. Addressing these restraints and challenges will be crucial for the silicone liquid injection moulding market to reach its full potential.

The Silicone Liquid Injection Molding Market Opportunities:

The future of the silicone liquid injection molding market is brimming with exciting possibilities that extend far beyond its current applications. The exceptional properties of LSR are constantly being explored by creative minds, with advancements anticipated in cutting-edge fields like microfluidics, wearable technology, and even high-performance aerospace components that require a unique blend of durability and lightweight design. Furthermore, the growing global focus on sustainability perfectly aligns with LSR's inherent recyclability. This eco-friendly characteristic positions LSR as a highly attractive material choice for manufacturers looking to reduce their environmental impact. We can expect to see significant investments in closed-loop systems for LSR waste, further solidifying its credentials as a responsible and sustainable material. Technological advancements are also poised to play a major role in the market's growth. Breakthroughs in mold design and automation have the potential to significantly reduce production costs and cycle times associated with silicone liquid injection molding. This would make the process more accessible for a wider range of manufacturers and applications, potentially unlocking entirely new avenues for LSR utilization. The potential integration with additive manufacturing (3D printing) opens doors for a future filled with even greater innovation. Imagine the possibilities of creating complex and customized LSR parts on-demand! This could revolutionize prototyping and production across various sectors, from medical devices to consumer electronics. Finally, the medical field stands to benefit immensely from LSR's biocompatibility. With the development of biocompatible LSR grades specifically tailored for implants and drug delivery systems, the future of healthcare holds immense promise.

SILICONE LIQUID INJECTION MOLDING MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

8.5% |

|

Segments Covered

|

By Material, Application, End-Use, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

The Dow Chemical Company (Dow), Wacker Chemie AG, Shin-Etsu Chemical Co., Ltd., Nusil Technology LLC, KCC Corporation, Zhejiang Xinan Chemical Industrial Group Co., Ltd., Simtec Silicone Parts, LLC, Momentive Performance Materials Inc., Stockwell Elastomerics Inc., Laur Silicone

|

Silicone Liquid Injection Molding Market Segmentation: By Material

Industrial grade is the most dominant segment in the Silicone Liquid Injection Molding Market by Material Grade. This grade offers a balance of cost and performance, making it suitable for various applications across industries. Medical grade is expected to be the fastest-growing segment due to the increasing demand for minimally invasive surgeries and biocompatible devices.

Silicone Liquid Injection Molding Market Segmentation: By Application

-

Automotive

-

Medical

-

Consumer Goods

-

Electrical & Electronics

The automotive industry currently holds the dominant position in the silicone liquid injection moulding market due to its extensive use of LSR for various car parts. However, the medical sector is anticipated to be the fastest-growing segment driven by the increasing demand for minimally invasive surgeries and biocompatible medical devices.

Silicone Liquid Injection Molding Market Segmentation: By End-Use

-

Automotive

-

Medical

-

Consumer Goods

-

Electrical & Electronics

-

Others

The silicone liquid injection moulding market is segmented by end-use sector, with the automotive industry currently holding the dominant position due to its reliance on LSR for heat-resistant parts. However, the medical sector is projected to be the fastest-growing segment, driven by the increasing popularity of minimally invasive surgeries and the need for biocompatible medical devices. This trend is expected to continue as the global population ages and healthcare advancements create new opportunities for LSR applications.

Silicone Liquid Injection Molding Market Segmentation: Regional Analysis

-

North America

-

Europe

-

Asia-Pacific

-

South America

-

Middle East and Africa

North America boasts a strong presence of established automotive and medical device manufacturers. This region actively invests in advanced technologies and prioritizes high-quality products, driving demand for LSR. The growing focus on minimally invasive surgeries and the aging population further contribute to the market's growth in North America.

Currently, the Asia-Pacific region reigns supreme as the largest market for silicone liquid injection moulding. This dominance can be attributed to the booming manufacturing and electronics industries in this region. China, a major manufacturing hub, is a significant consumer of LSR, while India's burgeoning market offers promising growth potential.

COVID-19 Impact Analysis on the Silicone Liquid Injection Molding Market:

The COVID-19 pandemic's impact on the silicone liquid injection molding market was a story of both challenge and adaptation. Initial disruptions arose from the global shutdown, causing a ripple effect on meticulously established supply chains for raw materials and LSR itself. This led to temporary shortages and price fluctuations, throwing a wrench into the production processes of some manufacturers. The automotive industry, a traditionally major consumer of LSR for car parts like gaskets and seals, also experienced a significant decline due to factory closures and a global reduction in consumer demand for new vehicles.

However, amidst these obstacles, the pandemic also presented unforeseen opportunities for the silicone liquid injection molding market. The surge in demand for medical devices like personal protective equipment (PPE) and diagnostic tools, which rely heavily on LSR's biocompatibility and chemical resistance for safe and reliable function, boosted the medical sector's use of LSR. Furthermore, heightened public awareness about hygiene led to a rise in LSR usage for consumer goods like medical gloves and hygiene products. This unexpected shift in consumer behavior presented a new avenue for market growth.

While the initial stages of the pandemic brought significant challenges, the market seems to be on the path to recovery. The long-term impact is expected to be positive, driven by several factors. The continued growth in the medical sector due to an aging population and advancements in healthcare is expected to maintain a steady demand for LSR in medical devices. Additionally, the resurgence of the automotive industry and its renewed demand for LSR in car parts will likely contribute to market growth. Overall, the COVID-19 pandemic's effect on the silicone liquid injection molding market has been complex, but the market's resilience and the rise of sectors like medical devices suggest a promising future. With continued innovation and adaptation, the silicone liquid injection molding market is poised to overcome these challenges and solidify its position as a key player in various industries.

Latest Trends/ Developments:

The world of silicone liquid injection molding is abuzz with innovation, constantly pushing the boundaries of what's possible. One exciting development lies in the realm of microfluidics and bioprinting. LSR's exceptional precision and control make it a game-changer, enabling the creation of miniaturized medical devices and intricate biological structures for vital research and drug discovery. This has the potential to revolutionize healthcare by facilitating the development of new diagnostic tools and personalized treatment options. Another significant trend is the advancement of biocompatible LSR grades. Researchers are constantly refining the material's properties, making it even more biocompatible and suitable for critical medical applications. This opens doors for the use of LSR in long-lasting implants and drug delivery systems, playing a crucial role in improving patient outcomes.

Sustainability is also a watchword in the industry. Manufacturers are actively exploring ways to minimize waste and develop closed-loop systems for LSR recycling. Additionally, the inherent recyclability of LSR is becoming a major selling point, aligning perfectly with the growing global focus on environmental responsibility. The potential integration with additive manufacturing (3D printing) is another exciting development with the power to transform the landscape. Imagine a future where complex LSR parts can be created on-demand through 3D printing, revolutionizing prototyping and production across various sectors. This could significantly reduce lead times and enable the creation of highly customized LSR components.

Finally, advancements in mold design and automation are leading to more efficient and cost-effective molding processes. This can significantly broaden the appeal of silicone liquid injection molding, making it more accessible to a wider range of manufacturers and applications. By embracing these trends and fostering continuous innovation, the silicone liquid injection molding market is poised to play a pivotal role in shaping the future of diverse industries. With its ever-evolving capabilities, LSR holds immense promise for driving progress and creating a better tomorrow.

Key Players:

-

The Dow Chemical Company (Dow)

-

Wacker Chemie AG

-

Shin-Etsu Chemical Co., Ltd.

-

Nusil Technology LLC

-

KCC Corporation

-

Zhejiang Xinan Chemical Industrial Group Co., Ltd.

-

Simtec Silicone Parts, LLC

-

Momentive Performance Materials Inc.

-

Stockwell Elastomerics Inc.

-

Laur Silicone