Silicon Solar Cells Market Size (2023– 2030)

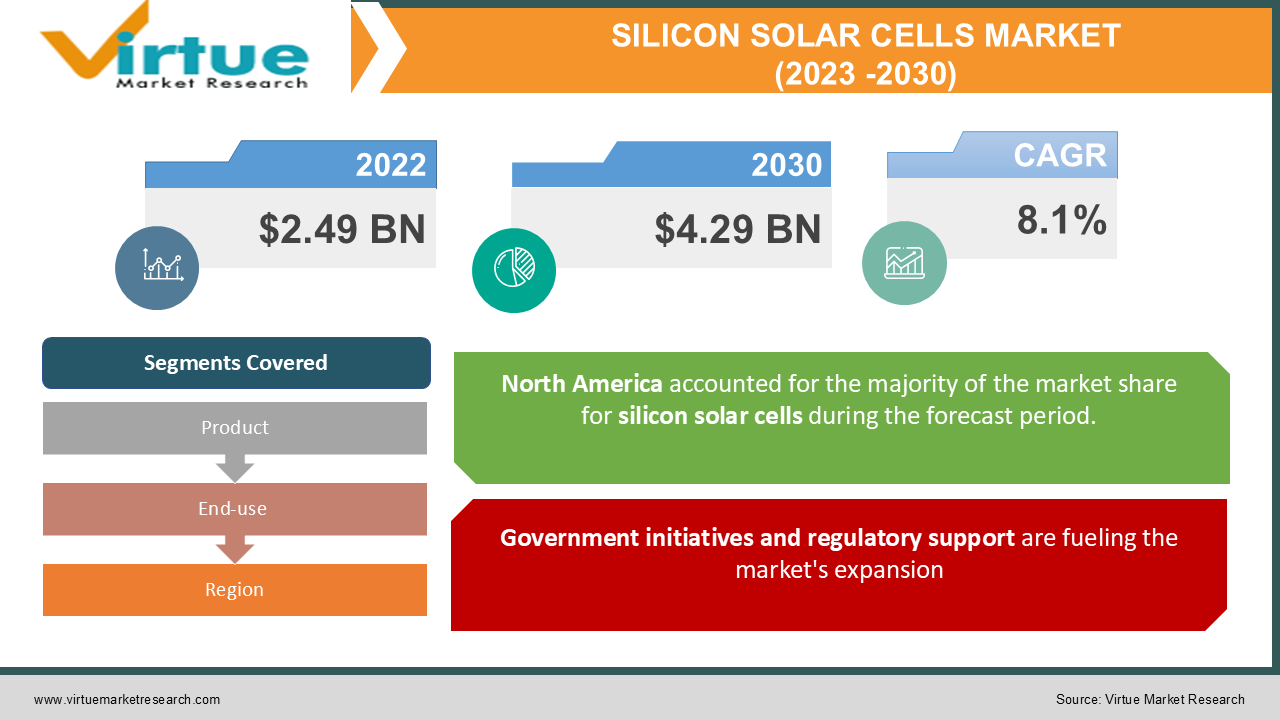

The Global Silicon Solar Cells Market was valued at USD 2.49 billion in 2022 and is projected to reach a market size of USD 4.29 billion by the end of 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 8.1%.

INDUSTRY OVERVIEW

Photovoltaic (PV) cell manufacturing peaked globally in 2008 at more than 7.9 GWp (Wp, peak power under normal test conditions)1, with an average yearly growth rate of more than 40% over the previous ten years. However, it has been calculated that less than 0.1 per cent of the world's total electricity production is produced by all PV systems combined. Nevertheless, it is anticipated that the output of PV cells would continue to expand significantly for many years. Crystalline silicon PV cells have been produced for more than 60 years, have the longest manufacturing history, and today make up the majority of solar cells produced—up to 90% of them. With 26 per cent of the earth's crust made up of silicon, it is one of the most abundant and environmentally safe commodities on the planet. The silicon solar cell occupies a significant place among the numerous types of solar cells used in the PV industry due to the resource's availability and safety. By its capability for mass manufacturing, silicon PV cells are the most likely contender to satisfy this need, with a global annual PV cell output of 100 GWp anticipated to be reached by about 2022.

Among the various silicon-based semiconductor products, the crystalline silicon PV cell is one. The PV cell is simply a diode with a semiconductor structure, and in the early years of solar cell production, numerous approaches for crystalline silicon cells were developed based on silicon semiconductor devices. The development of large-scale integrated circuits and numerous other silicon-based semiconductor applications, as well as the fusion of equipment and technologies created for PV cells, aided advancement in both disciplines. Increased energy conversion efficiency in solar cells was aided by process technologies like photolithography, and mass-production techniques like wire-saw slicing of silicon ingots, which were developed for the PV sector, were also easily transferable to other silicon-based semiconductor devices. The value of a PV cell, however, is substantially lower than that of other silicon-based semiconductor devices per unit area. Therefore, it is necessary to develop manufacturing processes like silver-paste screen printing and fire for contact creation to reduce costs and boost the output of crystalline silicon solar cells. Higher solar cell efficiencies are just as crucial for achieving "grid parity" with current mains grid energy rates as reduced material and production costs. For solar cell makers, the most critical technological challenge at the moment is the production of high-efficiency solar cells with low process costs. Reducing the price of high-purity crystalline silicon substrate production is one way to lower the price of silicon solar cell modules.

For the past several years, there has been a high demand for renewable energy. But because of a weak economy and an excess of subpar cells, the solar cell market is presently at a temporary plateau. The current predicament may be resolved by lowering manufacturing costs and increasing the conversion efficiency of the cell. To lower the cost of manufacture, new materials such as compound semiconductor thin films have been investigated. To increase the cell's efficiency, structural alterations have also been investigated. Even while thin silicon films and PERL-structured silicon solar cells have achieved efficiency records of 24.7 per cent and 13.44 per cent, respectively, mass manufacture of these cells is still prohibitively costly. Solar cells made of crystalline and amorphous silicon have dominated the solar industry and currently account for more than half of the market. Due to their important position in the solar industry, they will continue to be so in the future photovoltaic (PV) market.

COVD-19 IMPACT ON THE SILICON SOLAR CELLS MARKET

A drop in the photovoltaic market is anticipated, mostly as a result of COVID-19. Lockdowns have been enacted by the governments of numerous significant economies to stop the COVID-19 virus's spread. Manufacturing operations have been severely impacted by the lockout. For instance, the Chinese government declared a lockdown for more than 30 days in January 2020 to address COVID-19. The production and supply chain has suffered greatly as the bulk of PV modules are made in China. For instance, China provides around 80% of the components for India's solar value chain. Because no large ship container firms were operating out of Chinese ports or shipping products from China to other nations, the lockout had a significant impact on China's industrial capacity. In March and April 2020, this led to interruptions in the supply chain. Furthermore, manpower shortages and supply chain delays in the PV business were brought on by lockdown measures taken in other nations. Due to travel limitations, businesses were unable to get the necessary workforce for their operations. Although the industry is anticipated to be affected in 2020, a recovery is anticipated to start in 2021 and be complete by 2022.

MARKET DRIVERS:

Government initiatives and regulatory support are fueling the market's expansion

Governments in various locations are continually drafting laws to make grid connections for solar installations convenient. Solar energy is being actively promoted by nations including China, Canada, the US, and France. For instance, in July 2019, the Canadian government unveiled the Climate Action Incentive Fund (CAIF), a C$150 million (about USD 111 million) incentive programme to support the battle against climate change. With financing ranging from C$20,000 (USD 14,672) to C$250,000 (USD 183,400), firms proposing to establish renewable energy projects, including solar, are eligible to receive up to 25% of project-related expenditures. During the anticipated period, the expansion of the photovoltaic market is anticipated to be fueled by such efforts and benevolent government policies.

Technological developments in the production of solar cells are positively impacting the market growth

Over the past few years, the solar business has experienced several quick technical advancements. The most recent solar material with a suitable crystal structure for light absorption is called perovskite. Additionally, perovskite cells outperform traditional PV cells in lower lighting levels, on overcast days, or indoors, allowing for higher conversion efficiencies. The fundamental advantage of using perovskite to create solar cells is that it is an affordable, plentiful material that has the potential to provide inexpensive solar electricity. Due to its ability to be generated in very thin layer topologies with high levels of transparency, perovskite solar cells are well suited for several cutting-edge uses, such as building integrated photovoltaic (BIPV) projects and flexible panel designs.

MARKET RESTRAINTS:

Insufficiently qualified labour for PV installation and maintenance may hamper the market development

A wide range of trained personnel is needed for photovoltaic installation, from Ph.D.-level researchers in R&D through technicians who need specific training and certification to a large number of additional specialists for supporting all facets of the solar industry. To manage the adoption and implementation, the industry lacks sufficient numbers of skilled installers. One of the biggest problems in the PV sector has been the lack of adequately qualified labour. However, end-users of the technology expect recognised standards, quality control, and certification of abilities throughout the whole development phase of a PV installation.

The scarcity of operational land may impede the market growth

Large tracts of land are needed to install solar or PV systems for utility applications. According to some estimates, utility-scale PV systems need about 5 acres of land per kilowatt (depending on the technology and sunshine availability), which suggests that the need for usable land will increase in the upcoming years. This might raise issues with habitat loss and land degradation in some areas. The likelihood of solar projects sharing land with agricultural activities is far less likely than it is for wind generation. A significant obstacle is finding usable land, particularly in emerging nations like China and India, which are important PV markets.

SILICON SOLAR CELLS MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2022 - 2030

|

|

Base Year

|

2022

|

|

Forecast Period

|

2023 - 2030

|

|

CAGR

|

8.1%

|

|

Segments Covered

|

By Product, End-use and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

HANWHA Q CELLS CO., LTD., SOLARWORLD AG, JA SOLAR HOLDINGS CO., LTD., YINGLI SOLAR, SHARP CORPORATION, JINKO SOLAR CANADIAN SOLAR INC., CHINA SUNERGY, TRINA SOLAR LIMITED, SUNPOWER CORPORATION

|

This research report on the Silicon Solar Cells Market has been segmented and sub-segmented based on Product, By END-USE and By Region.

SILICON SOLAR CELLS MARKET – BY PRODUCT

- Monocrystalline

- Multicrystalline

Based on the product, the silicon solar cells are segmented into, Monocrystalline and Multicrystalline. From 2023 - 2030, multi-crystalline silicon cells are anticipated to increase at the quickest rate of over 25.0 per cent. Market expansion is anticipated to be fueled by technological manufacturing process simplicity that results in reduced production costs compared to competitors. Additionally, rising demand for these cells is anticipated throughout the projection period due to reduced beginning costs and higher efficiency in both residential and commercial applications. To decrease solar cell efficiency loss, industry participants are concentrating on micro features like crystallisation and individual solar cell production procedures. Fraunhofer ISE, a German research organisation, has achieved notable multi-crystalline solar cell efficiency, converting 22.3% of incident solar energy into electricity.

SILICON SOLAR CELLS MARKET - BY END-USE

- Utility-Scale

- Commercial

- Residential

Based on the end-use, the silicon solar cells are segmented into Utility-Scale, Commercial and Residential. During the projected period, the residential application market is anticipated to develop at the greatest CAGR. This is explained by the recent decrease in the price of PV systems. PV systems are put on rooftops or other locations where there is enough sunshine to meet the home's electrical demands in residential applications. Governments in several nations, including those in India, China, and the US, provide financial incentives and tax breaks to homeowners who install PV systems, which is anticipated to drive the market's expansion for these systems in residential applications throughout the forecast period.

SILICON SOLAR CELLS MARKET - BY REGION

- North America

- Europe

- The Asia Pacific

- Latin America

- The Middle East

- Africa

By region, the Silicon Solar Cells Market is grouped into North America, Europe, Asia Pacific, Latin America, The Middle East and Africa. In 2021, the demand for solar cells in Europe exceeded 45% of the installed capacity worldwide. Over the projected period, growth is anticipated to be boosted by the availability of favourable government regulations and incentives related to PV installations. The market is anticipated to be driven by rising demand for these cells in the commercial and utility sectors. Over the projection period, declining PV prices are anticipated to expand the market for crystalline silicon modules. Moreover, the demand for thin film solar cells in residential and commercial applications is anticipated to rise as a result of technical developments aimed at enhancing operational efficiency.

In 2021, it was anticipated that North America's solar cell demand exceeded 20 GW. The industry is anticipated to gain from an increase in PV installations as a result of consumers' growing knowledge of the financial advantages of renewable energy systems in this area. However, a lack of federal incentives and subsidies after 2020 is anticipated to result in fewer installations from the residential and commercial sectors, which is anticipated to impede growth.

China's photovoltaic industry received investments totalling 80.8 billion yuan in the previous year, which supports the forecast for the sector. Chinese PV companies are aggressively entering growing markets by acquiring international manufacturers and constructing factories abroad, favourably affecting the size of the solar cell industry. By 2022, the Indian government hopes to generate 50 GW of electricity using solar technology. The market share will increase with increased government programmes and investment in sustainable energy.

SILICON SOLAR CELLS MARKET - BY COMPANIES

Some of the major players operating in the Silicon Solar Cells Market include:

- HANWHA Q CELLS CO., LTD.

- SOLARWORLD AG

- JA SOLAR HOLDINGS CO., LTD.

- YINGLI SOLAR

- SHARP CORPORATION

- JINKO SOLAR

- CANADIAN SOLAR INC.

- CHINA SUNERGY

- TRINA SOLAR LIMITED

- SUNPOWER CORPORATION

NOTABLE HAPPENING IN THE SILICON SOLAR CELLS MARKET

PARTNERSHIP- For the sale of 9.2 MW of its Hi-MO4 modules, LONGi and Swedish distributor Senergia came into a contract in April 2020. In accordance with the agreement, there will be around 25,000 PV modules total, divided into 23,400 370 W and 1,320 440 W pieces.

PRODUCT LAUNCH- New Ga-doped wafer-based PV modules were launched by JA Solar in March 2020. Ga-doped silicon wafer technology is anticipated to boost stability and power generating capabilities.