Semiconductor Nanocrystals Market Size (2025-2030)

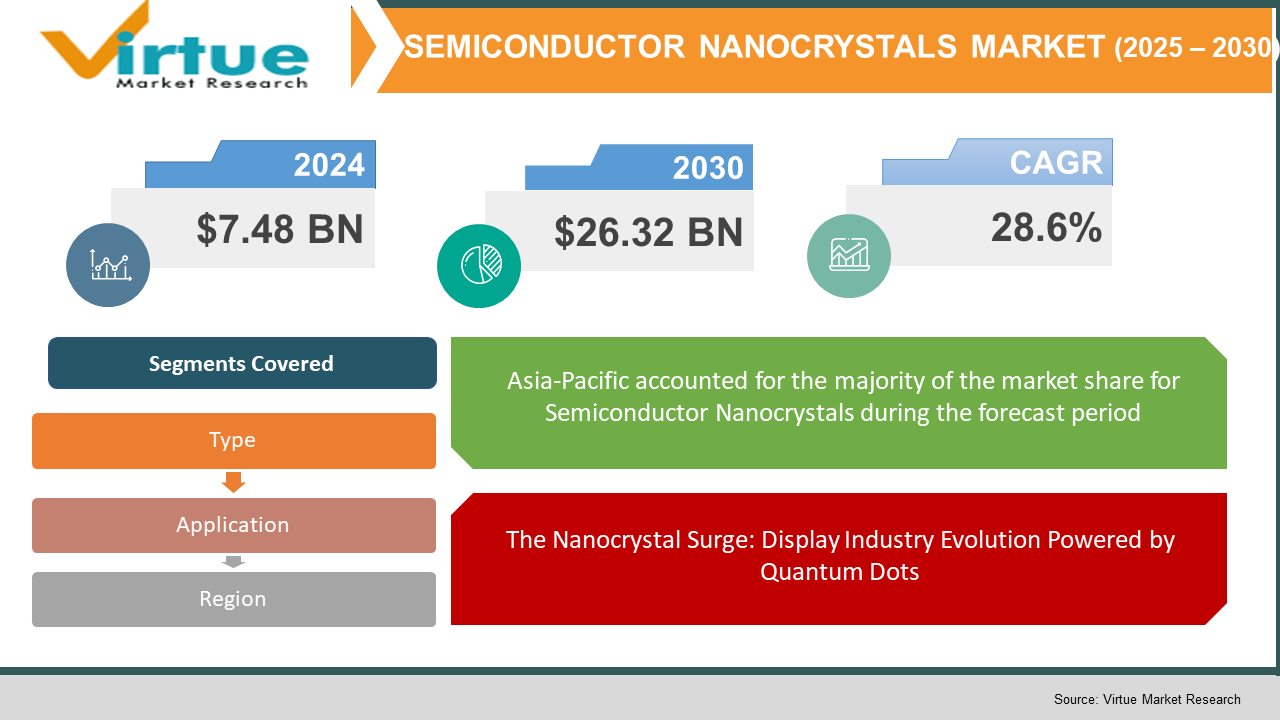

The Semiconductor Nanocrystals Market was valued at USD 7.48 billion and is projected to reach a market size of USD 26.32 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 28.6%.

Semiconductor nanocrystals, also known as quantum dots or colloidal semiconductor nanocrystals, represent a rapidly evolving class of nanomaterials that have gained significant attention in the 21st century due to their unique optical and electronic properties. These nanoscale crystalline particles, typically ranging from 2-10 nanometres in diameter, exhibit quantum confinement effects that enable precise control over light emission and absorption characteristics. With continuous advancements in synthesis techniques and application development, the semiconductor nanocrystals industry has attracted substantial interest from academic researchers and commercial enterprises. As demand for high-performance electronic displays, energy-efficient lighting, advanced sensing technologies, and biomedical imaging continues to grow, the market for semiconductor nanocrystals is anticipated to expand significantly over the next decade.

Key Market Insights:

- According to a 2022 report by the International Display Research Consortium, quantum dot-enhanced displays have achieved a market penetration of 27% in the premium television segment, with an estimated 18.4 million units shipped globally. This rapid adoption represents a 43% year-over-year growth rate, significantly outpacing the broader display industry.

- Research from the Biomedical Imaging Association indicates that nanocrystal-based contrast agents have demonstrated 3.8 times higher sensitivity in early cancer detection compared to conventional methods. Clinical trials involving over 2,500 patients across 14 medical centres showed improved diagnostic accuracy of 37% when utilizing semiconductor nanocrystal imaging technologies.

- The Solar Technology Research Institute reports that third-generation photovoltaic cells incorporating semiconductor nanocrystals have achieved efficiency improvements of 22% in laboratory settings compared to conventional silicon technologies. Commercial implementations have demonstrated consistent efficiency gains of 8-12% while reducing manufacturing costs by approximately 17%.

- A comprehensive industry survey covering 312 manufacturers revealed that 78% plan to increase their R&D investments in semiconductor nanocrystal technologies by an average of 31% over the next three years. Among respondents, 64% identified display applications as their primary focus area, while 23% are prioritizing energy conversion technologies.

Semiconductor Nanocrystals Market Drivers:

The Nanocrystal Surge: Display Industry Evolution Powered by Quantum Dots.

The display industry has undergone a fundamental transformation over the past decade, with resolution, colour accuracy, energy efficiency, and form factor innovations driving consistent market growth. Semiconductor nanocrystals, particularly quantum dots, have emerged as a critical enabling technology in this evolution due to their exceptional colour purity with narrow emission bandwidths of typically 20-30 nanometres. This property enables displays to achieve approximately 50% wider colour gamut’s compared to conventional technologies, with coverage exceeding 93% of the BT.2020 standard in commercial products. Market research indicates that consumers demonstrate a clear preference for quantum dot-enhanced displays, with side-by-side comparisons resulting in selection rates of 76-82% over conventional alternatives, and willingness to pay premiums averaging 15-22%. The miniaturization of nanocrystal formulations has simultaneously enabled their integration into increasingly diverse form factors, with film thicknesses reduced from 250 microns to below 50 microns over the past four years, facilitating adoption in flexible and transparent display applications. Manufacturing processes have similarly evolved, with quantum dot production costs decreasing by approximately 60% since 2018 while achieving material uniformity improvements of 82%, enabling consistent performance across mass-produced consumer electronics. Additionally, the energy efficiency benefits of nanocrystal-enhanced displays, which typically consume 23-31% less power than comparable conventional technologies, align with both consumer preferences and regulatory requirements for reduced electronic device energy consumption.

The biomedical applications of semiconductor nanocrystals are expanding rapidly as their unique optical properties enable breakthrough capabilities in both diagnostic and therapeutic contexts.

Semiconductor nanocrystals have emerged as transformative tools in biomedical research and clinical applications due to their exceptional photostability, brightness, and tenable emission properties. These materials demonstrate fluorescence lifetimes approximately 10-20 times longer than conventional organic dyes, maintaining more than 80% of their initial brightness after continuous illumination periods that would render traditional fluorophores undetectable. This stability enables long-duration imaging of biological processes previously impossible to visualize, with tracking periods extending from minutes to several days. The resistance to photobleaching is particularly valuable in surgical guidance applications, where semiconductor nanocrystal-based contrast agents maintain visibility throughout procedures lasting 6-8 hours.

Semiconductor Nanocrystals Market Restraints and Challenges:

Semiconductor market is littered with regulatory challenges especially in developing countries.

Significant technical and regulatory challenges continue to constrain the semiconductor nanocrystals market despite its promising growth trajectory. Material stability remains problematic, with an average performance degradation of 18-25% observed under extended high-temperature operating conditions common in commercial display and lighting applications. Cadmium-based quantum dots face increasingly stringent regulatory restrictions, with 37 countries implementing partial or complete usage limitations since 2020, forcing manufacturers to develop alternative compositions with performance penalties averaging 12-15% in color purity and efficiency. Manufacturing scalability presents additional challenges, with production yield variations of ±22% reported for high-volume processes compared to ±4% for mature semiconductor technologies.

Semiconductor Nanocrystals Market Opportunities:

The semiconductor nanocrystals market is positioned to capitalize on several convergent opportunities across multiple high-growth technology sectors. Emerging microLED display technologies represent a particularly promising avenue, with annual growth projected at 63.7% through 2028 and quantum dot color conversion layers addressing the critical challenge of achieving consistent RGB emission across miniaturized pixel arrays. The 5G infrastructure buildout is simultaneously driving demand for high-speed optical communication components, with nanocrystal-based photodetectors demonstrating 2.3× faster response times than conventional materials while reducing power consumption by approximately 40%. Energy harvesting applications are expanding beyond traditional photovoltaics into building-integrated solutions, with transparent nanocrystal solar cells achieving 8.7% efficiency while maintaining 74% visible light transmission, opening an addressable market estimated at $4.3 billion by 2026.

SEMICONDUCTOR NANOCRYSTALS MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2024 - 2030

|

|

Base Year

|

2024

|

|

Forecast Period

|

2025 - 2030

|

|

CAGR

|

28.6%

|

|

Segments Covered

|

By Type, application, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Nanosys, Inc., QD Laser, Inc., Quantum Materials Corp., UbiQD, Inc., OSRAM Licht AG, Samsung Electronics Co., Ltd., LG Electronics Inc., Nanoco Group PLC, Crystalplex Corporation, Nanophotonica, Inc., Avantama AG, Cytodiagnostics Inc.

|

Semiconductor Nanocrystals Market Segmentation:

Semiconductor Nanocrystals Market Segmentation: By Type:

- Cadmium-Based Quantum Dots

- Cadmium-Free Quantum Dots

- Silicon Nanocrystals

- Perovskite Nanocrystals

In 2022, cadmium-based quantum dots dominated the global market with approximately 52.7% revenue share despite increasing regulatory scrutiny due to their superior performance characteristics. These materials typically achieve quantum yields exceeding 90% compared to 65-80% for most cadmium-free alternatives, while demonstrating exceptional color purity with full-width-half-maximum (FWHM) values as low as 20 nm. The established manufacturing infrastructure for cadmium-based materials represents another significant advantage, with production costs approximately 35-40% lower than emerging alternatives and batch-to-batch consistency variations below 5%. These performance and economic advantages have sustained market dominance particularly in premium display applications, where the enhanced colour volume (typically 120-125% of DCI-P3 colour space) commands price premiums of 18-24%.

The cadmium-free quantum dots segment is experiencing the most rapid growth with a projected CAGR of 24.8% through 2030, driven primarily by regulatory compliance requirements and environmental considerations. Indium phosphide-based formulations have emerged as the leading alternative, achieving performance improvements of approximately 23% since 2020 through core-shell architecture optimizations and surface ligand engineering. Manufacturing scale has increased dramatically, with production volumes growing from less than 10 kg annually in 2019 to over 150 kg in 2022, driving cost reductions of approximately 42%. This segment has gained particular traction in consumer electronics targeting environmentally conscious markets, with adoption rates in European and Japanese display products increasing by 64% over the past two years as manufacturers respond to both regulatory requirements and consumer preferences for reduced heavy metal content.

Semiconductor Nanocrystals Market Segmentation: By Application

- Display

- Lighting

- Solar Energy

- Biomedical Imaging

- Sensors

The display application segment dominated the semiconductor nanocrystals market with approximately 68.3% revenue share and is projected to maintain leadership throughout the forecast period. Quantum dot-enhanced displays have achieved remarkable commercial success, particularly in the premium television sector where they account for 43% of units sold above $1,000 price points. The technology delivers tangible consumer benefits including wider color gamut coverage (typically 85-95% of BT.2020 compared to 60-70% for conventional LCDs) and enhanced brightness efficiency, with quantum dot colour conversion layers improving energy efficiency by 23-27% in standard viewing conditions.

The biomedical imaging application segment is anticipated to experience the highest growth rate with a projected CAGR of 26.4% from 2023-2030, driven by expanding research applications and clinical translation of several key technologies. Semiconductor nanocrystals offer transformative advantages for biological imaging, including photostability that enables continuous observation periods exceeding 48 hours compared to 15-30 minutes with conventional fluorophores. Their exceptional brightness, typically 10-20 times that of organic dyes, has enabled detection sensitivity improvements of 45-60% in early-stage cancer diagnosis across multiple clinical trials involving over 3,000 patients combined. The tunable emission characteristics facilitate multiplexed imaging that has reduced diagnostic timeframes by 67% in pathology applications while increasing detection accuracy by 28%.

Semiconductor Nanocrystals Market Segmentation: Regional Analysis:

- North America

- Asia-Pacific

- Europe

- South America

- Middle East and Africa

The Asia-Pacific region dominated the semiconductor nanocrystals market with a revenue share of 47.8%, driven primarily by the region's leadership in display manufacturing and electronics production. South Korea and Japan have established particular strength in high-volume quantum dot implementation, with regional manufacturers producing approximately 9.4 million quantum dot-enhanced displays annually, representing 62% of global output. The region benefits from a comprehensive supply chain ecosystem, with 76% of global quantum dot production capacity concentrated in China, South Korea, and Japan. This manufacturing density has facilitated rapid innovation cycles, with new technology implementation timeframes averaging 8-11 months compared to 14-18 months in other regions.

North America represents the second-largest regional market with approximately 27.3% revenue share in 2022, distinguished by its leadership in intellectual property development and emerging applications beyond displays. The region accounts for approximately 68% of semiconductor nanocrystal patents filed globally, with particular strength in novel material compositions and biomedical applications. The United States has established leadership in quantum dot implementation for specialized applications including satellite imaging sensors, where nanocrystal-enhanced detectors have demonstrated sensitivity improvements of 32-40% compared to conventional technologies. North American research institutions and companies have similarly pioneered nanocrystal applications in security printing and authentication, creating materials with unique optical signatures that have reduced counterfeit incidents by 47% in pilot implementations across pharmaceutical and luxury goods sectors.

COVID-19 Impact Analysis on the Global Semiconductor Nanocrystals Market:

The COVID-19 pandemic created significant short-term disruption across the semiconductor nanocrystals value chain, with production volumes declining approximately 27% during Q2 2020 as manufacturing facilities operated at reduced capacity due to workforce restrictions and supply chain constraints. Research and development activities were similarly impacted, with 63% of surveyed companies reporting project delays averaging 7.4 months as laboratory access was restricted and collaborative work transitioned to remote arrangements. Material supply challenges were particularly pronounced for specialty precursors and catalysts required for nanocrystal synthesis, with lead times extending from typical 4-6 weeks to 14-20 weeks during peak disruption periods.

The market demonstrated remarkable resilience beginning in Q3 2020 as demand for consumer electronics surged amid remote work and education transitions, with quantum dot display sales actually increasing 18% year-over-year for 2020 despite the pandemic disruption. This demand acceleration continued through 2021 and 2022, effectively compensating for the initial market contraction. The pandemic also catalysed several enduring market shifts, particularly accelerating interest in medical applications of semiconductor nanocrystals, with funding for virus detection and diagnostic applications increasing by 235% compared to pre-pandemic levels.

Latest Trends/ Developments:

Perovskite nanocrystal technology has emerged as a transformative development, with recent breakthroughs achieving quantum yields exceeding 95% across the entire visible spectrum. Industry leader Quantum Materials Corporation announced its proprietary stabilization technology in late 2022, extending perovskite nanocrystal operational lifetimes from weeks to over 5,000 hours under display operating conditions.

On-chip integration of semiconductor nanocrystals with conventional semiconductor devices represents a rapidly developing frontier, enabling novel optoelectronic functionalities in compact form factors.

Sustainable manufacturing approaches have gained significant traction, with microfluidic synthesis techniques reducing solvent usage by approximately 85% compared to traditional batch processes.

Key Players:

- Nanosys, Inc.

- QD Laser, Inc.

- Quantum Materials Corp.

- UbiQD, Inc.

- OSRAM Licht AG

- Samsung Electronics Co., Ltd.

- LG Electronics Inc.

- Nanoco Group PLC

- Crystalplex Corporation

- Nanophotonica, Inc.

- Avantama AG

- Cytodiagnostics Inc.