Semiconductor Market Size (2024 – 2030)

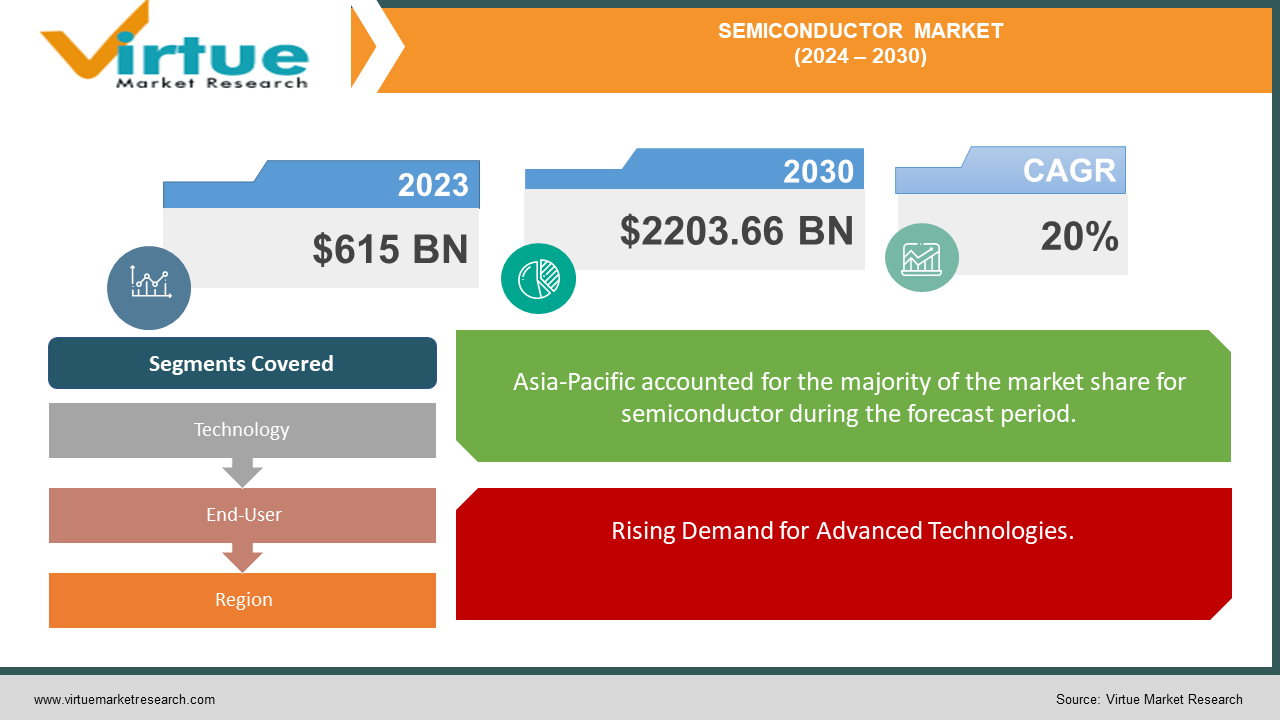

The Global Semiconductor Market was valued at USD 615 billion in 2023 and is projected to reach a market size of USD 2203.66 billion by the end of 2030. The market is anticipated to expand at a compound annual growth rate (CAGR) of 20% between 2024 and 2030.

The Global Semiconductor Market plays a pivotal role in powering the digital world, with semiconductors serving as the fundamental building blocks for a wide range of electronic devices, from smartphones to automobiles. This market is driven by the ever-growing demand for advanced technologies such as artificial intelligence (AI), the Internet of Things (IoT), 5G networks, and autonomous vehicles, all of which rely heavily on semiconductor components. As industries increasingly adopt digitalization, the need for high-performance, energy-efficient chips has surged. Additionally, the ongoing transition toward renewable energy and electric vehicles has fueled the demand for specialized semiconductor solutions. However, the market faces challenges such as supply chain disruptions and geopolitical tensions that impact production and pricing. Governments and corporations worldwide are investing heavily in expanding semiconductor manufacturing capabilities to mitigate these risks and meet growing demand. As a result, the semiconductor market is expected to see robust growth, with continuous innovation in chip design, manufacturing processes, and material advancements.

Article: The Next Semiconductor Battle Isn’t Nodes, It’s Packaging, Memory, and Materials

Key Market Insights:

Memory chips represent nearly 30% of the total semiconductor market, with demand driven by cloud computing and data centers.

5G deployment is expected to increase semiconductor sales by 8% annually over the next five years.

The shift to electric vehicles (EVs) could increase semiconductor demand by 50% by 2025, as EVs require more advanced electronic components.

Global semiconductor production capacity is projected to grow by 6% annually, fueled by investments in new fabrication plants.

The United States aims to increase its semiconductor manufacturing capacity by 30% through government incentives and private-sector investments.

Global Semiconductor Market Drivers:

Rising Demand for Advanced Technologies.

The increasing integration of advanced technologies such as artificial intelligence (AI), 5G, the Internet of Things (IoT), and autonomous vehicles is a key driver of the global semiconductor market. These technologies require highly efficient and powerful semiconductor chips to function effectively, resulting in an exponential rise in demand for next-generation semiconductors. AI applications, for instance, rely heavily on advanced computing capabilities, necessitating high-performance chips capable of handling complex tasks like data analysis and machine learning. Similarly, the rollout of 5G technology requires specialized semiconductors to enable faster, more reliable wireless communication. IoT devices, ranging from smart home systems to industrial machinery, further expand the need for chips with enhanced connectivity and low power consumption. As industries continue to digitize, the growing reliance on these technologies is set to significantly boost semiconductor demand, fueling market expansion.

Electric Vehicles and Renewable Energy Transition

The transition toward electric vehicles (EVs) and renewable energy is another major driver of the global semiconductor market. EVs require a wide range of semiconductor components for battery management systems, power electronics, sensors, and autonomous driving features. As governments and consumers increasingly prioritize sustainable energy solutions, the demand for EVs has surged, directly impacting semiconductor requirements. Additionally, renewable energy technologies such as solar and wind power systems depend on semiconductors for efficient energy conversion and storage. With the global push for clean energy and decarbonization, the need for advanced semiconductor technologies in EVs and renewable energy infrastructure is projected to grow rapidly. This shift is expected to create substantial opportunities for semiconductor manufacturers in the coming years.

Global Semiconductor Market Restraints and Challenges:

The Global Semiconductor Market faces significant restraints and challenges that could hinder its growth. One of the primary challenges is the ongoing supply chain disruption, exacerbated by geopolitical tensions, trade restrictions, and the COVID-19 pandemic. These disruptions have led to semiconductor shortages, impacting industries such as automotive, consumer electronics, and telecommunications, which heavily rely on a steady supply of chips. Additionally, the semiconductor industry is highly capital-intensive, with the development of new fabrication plants and advanced manufacturing processes requiring substantial investments. This limits the ability of smaller players to compete with established industry giants. Intellectual property (IP) protection and the complexity of semiconductor design also pose challenges, as companies face risks related to IP theft and design flaws. Furthermore, the rapid pace of technological advancements in semiconductors necessitates continuous innovation, which can strain research and development (R&D) budgets and timelines. Environmental concerns related to the energy consumption of semiconductor manufacturing processes and the disposal of electronic waste further add to the challenges. These factors collectively create a complex landscape for the semiconductor market, requiring strategic planning and global collaboration to overcome the barriers to growth.

Global Semiconductor Market Opportunities:

The Global Semiconductor Market presents significant opportunities driven by advancements in emerging technologies like artificial intelligence (AI), 5G, and the Internet of Things (IoT). As industries increasingly adopt automation, demand for high-performance chips and processors continues to rise. The automotive sector, with the growing trend towards electric vehicles (EVs) and autonomous driving, is another major contributor to semiconductor demand, requiring chips for advanced driver-assistance systems (ADAS) and electric powertrains. Additionally, the shift towards cloud computing and data center expansion is fueling the need for more efficient, powerful semiconductors. Increased government support and incentives in key markets, such as the U.S. and China, further bolster industry growth, with a focus on strengthening domestic chip manufacturing to reduce global supply chain vulnerabilities. Moreover, semiconductor innovations in areas like quantum computing and advanced memory solutions offer untapped potential. As demand for miniaturized, energy-efficient components grows, companies with expertise in these areas can capture a larger market share.

SEMICONDUCTOR MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

20% |

|

Segments Covered

|

By Technology, End-User, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Intel Corporation, Samsung Electronics Co., Ltd., Taiwan Semiconductor Manufacturing Company (TSMC), Qualcomm Technologies, Inc., Broadcom Inc., NVIDIA Corporation, Texas Instruments Incorporated, Advanced Micro Devices, Inc. (AMD), Micron Technology, Inc., STMicroelectronics N.V.

|

Global Semiconductor Market Segmentation: By Technology

In 2023, based on market segmentation by Technology, CMOS (Complementary Metal-Oxide-Semiconductor) had the highest share of the Global Semiconductor Market. Advancements in manufacturing processes for Complementary Metal-Oxide-Semiconductor (CMOS) technology have significantly enhanced the performance and efficiency of semiconductors. Continuous improvements in CMOS fabrication techniques have enabled the production of smaller, more powerful transistors, thereby increasing the density of components on a chip and allowing for greater functionality and performance within the same physical space. This miniaturization is crucial as it supports the growing demand for high-performance semiconductors driven by the proliferation of mobile devices and Internet of Things (IoT) applications. The expanding use of smartphones, tablets, and IoT devices necessitates semiconductors that are not only high-performing but also energy-efficient—areas where CMOS technology excels. Additionally, CMOS technology remains relatively cost-effective compared to alternative semiconductor technologies, which helps to keep production costs manageable and makes it accessible to a broad spectrum of manufacturers. This cost efficiency, combined with its technological advancements, positions CMOS as a dominant technology in the semiconductor industry, capable of meeting the escalating demands of modern electronic applications while maintaining economic viability.

Global Semiconductor Market Segmentation: By End-User

In 2023, based on market segmentation by Ens-User, Original Equipment Manufacturers (OEMs) had the highest share of the Global Semiconductor Market. Original Equipment Manufacturers (OEMs) are the predominant players in the global semiconductor market, accounting for the largest share due to their extensive integration of semiconductors into a wide range of products, including smartphones, computers, automobiles, and consumer electronics. As primary end-users of semiconductor components, OEMs drive substantial demand, influencing the market's overall dynamics. Their purchasing power is significant, shaping the industry's trends and technological developments. While Contract Manufacturers (CMs) and Design Houses also contribute to the market by providing manufacturing and design services, respectively, OEMs hold a crucial position due to their direct consumption of semiconductors in the production of finished products. The market share held by OEMs can vary based on economic conditions, technological progress, and industry-specific trends, but their role remains central in dictating semiconductor demand and shaping the market landscape. As technology evolves and new applications emerge, OEMs continue to be the key drivers of semiconductor innovation and market growth.

Global Semiconductor Market Segmentation: By Region

-

North America

-

Europe

-

Asia-Pacific

-

South America

-

Middle East and Africa

In 2023, based on market segmentation by Region, Asia-Pacific had the highest share of the Global Semiconductor Market. The Asia-Pacific region holds a dominant position in the global semiconductor market, bolstered by its world-class manufacturing capabilities and substantial government support. The region boasts advanced semiconductor manufacturing facilities that ensure the efficient production of high-quality chips, meeting the growing demands of various industries. Governments across Asia-Pacific have played a crucial role by implementing supportive policies, offering incentives, and making strategic investments to boost the semiconductor sector. Additionally, the increasing demand for electronic devices and products within the region has driven market growth, further solidifying Asia-Pacific's role as a key player in the semiconductor industry. While North America and Europe remain significant contributors to the market, Asia-Pacific's robust manufacturing infrastructure, supportive government actions, and burgeoning domestic markets position it as a leading force in the semiconductor landscape. This strong foundation is expected to sustain and potentially enhance the region's influence in the global semiconductor market in the coming years.

COVID-19 Impact Analysis on the Global Semiconductor Market.

The COVID-19 pandemic significantly impacted the Global Semiconductor Market, causing both disruptions and opportunities. Initially, supply chain interruptions, particularly in key manufacturing hubs like China, led to severe production slowdowns and shortages of critical semiconductor components. Lockdowns and restrictions further exacerbated supply constraints, affecting industries dependent on chips, including automotive and electronics. However, the pandemic also accelerated digital transformation across various sectors, driving demand for semiconductors. The surge in remote work, online education, and entertainment services spurred increased sales of laptops, smartphones, data centers, and networking equipment, all of which require advanced semiconductor technologies. Additionally, healthcare applications such as telemedicine, digital health platforms, and medical devices saw rising demand for specialized chips. Despite initial challenges, semiconductor manufacturers adapted by investing in capacity expansion and diversifying supply chains to reduce reliance on single regions. The pandemic also highlighted the need for resilient, flexible semiconductor supply chains, prompting governments to implement policies aimed at boosting domestic chip production and self-sufficiency. This reshaped market dynamics, positioning the semiconductor industry for robust growth in the post-pandemic era.

Latest trends / Developments:

The Global Semiconductor Market is witnessing several key trends and developments, driven by advancements in technology and evolving industry needs. One of the most significant trends is the growing demand for semiconductors in electric vehicles (EVs) and autonomous driving systems, as the automotive sector shifts towards electrification and intelligent mobility. Another notable trend is the adoption of 5G technology, which requires advanced semiconductors for network infrastructure and mobile devices, enabling faster communication and connectivity. Additionally, the rise of artificial intelligence (AI) and machine learning (ML) applications across industries is pushing the demand for more powerful, specialized chips. The ongoing expansion of data centers and cloud computing, fueled by increased digitalization, also requires high-performance semiconductors. Furthermore, miniaturization and energy efficiency remain critical as semiconductor manufacturers focus on producing smaller, more power-efficient chips for portable devices and IoT applications. Innovations in quantum computing and advanced packaging technologies, such as 3D chip stacking, are also gaining traction, offering improved performance and integration capabilities. Lastly, geopolitical tensions and supply chain vulnerabilities have led to increased investments in domestic semiconductor manufacturing, with governments implementing policies to boost local production and reduce reliance on global supply chains.

Key Players:

-

Intel Corporation

-

Samsung Electronics Co., Ltd.

-

Taiwan Semiconductor Manufacturing Company (TSMC)

-

Qualcomm Technologies, Inc.

-

Broadcom Inc.

-

NVIDIA Corporation

-

Texas Instruments Incorporated

-

Advanced Micro Devices, Inc. (AMD)

-

Micron Technology, Inc.

-

STMicroelectronics N.V.