Sanitary Napkin Market Size (2025-2030)

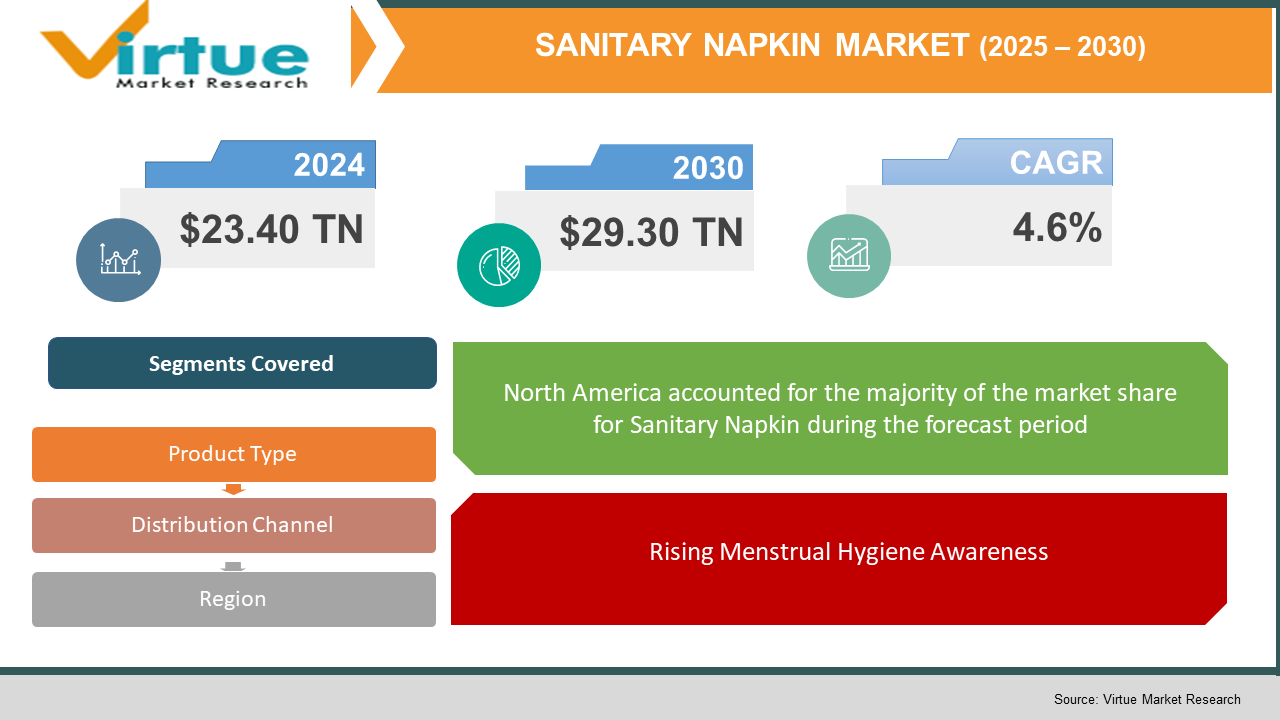

The Sanitary Napkin Market was valued at USD 23.40 billion and is projected to reach a market size of USD 29.30 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 4.6%.

The sanitary napkin market plays a vital role in women’s health and hygiene, serving as an essential product for menstrual care. It encompasses a variety of products, including disposable and reusable pads, pantyliners, and maternity pads. Consumer preferences in this market are influenced by factors such as comfort, absorbency, skin sensitivity, and sustainability. Increasing awareness of menstrual hygiene, especially in developing regions, has expanded the demand for sanitary products.

The market is also being impacted by social taboos and cultural sensitivities, which vary widely across regions. In recent years, online platforms and direct-to-consumer models have become more prominent, helping to reach previously underserved populations.

Key Market Insights:

Environmental concerns and government initiatives are propelling the demand for biodegradable sanitary napkins in India. The Indian biodegradable sanitary napkin market was valued at about USD 30 million in 2024 and is projected to reach around USD 170 million by 2030. This growth is driven by increased consumer awareness of sustainability and supportive policies promoting eco-friendly alternatives.

The reusable sanitary napkin segment is witnessing significant growth due to rising accessibility and affordability. Educational programs focusing on menstrual health and continual advancements in manufacturing techniques are key factors driving this market expansion.

Government programs and policies are playing a crucial role in improving menstrual hygiene awareness and accessibility. For instance, India's Swachh Bharat Mission-Urban (SBM-U) 2.0, launched on July 25, 2024, includes initiatives to reduce plastic waste and promote eco-friendly alternatives like biodegradable sanitary napkins. Such efforts are fostering a supportive environment for adopting sustainable menstrual products.

Sanitary Napkin Market Drivers:

Rising Menstrual Hygiene Awareness

Growing education initiatives, both by governments and NGOs, are helping dismantle taboos surrounding menstruation. Increased public awareness campaigns have led to improved acceptance and demand for sanitary napkins, especially in rural and underserved areas. Schools and workplaces are also becoming more proactive in offering menstrual hygiene support, driving regular usage among younger women.

Product Innovation and Sustainability Trends

Manufacturers are investing heavily in research to create thinner, more absorbent, and skin-friendly sanitary napkins. The rise in demand for biodegradable and organic pads reflects a broader consumer shift toward environmentally conscious choices. These innovations not only attract eco-conscious users but also open new premium market segments.

Expansion of Distribution Channels

The availability of sanitary napkins through a wide range of retail outlets—pharmacies, supermarkets, and especially e-commerce platforms—has made these products more accessible. Online platforms offer discreet purchasing options and subscription services, increasing regular usage. This diversified access is crucial in expanding reach to remote and conservative areas.

Sanitary Napkin Market Restraints and Challenges:

Cultural Taboos and Social Stigma

In many regions, menstruation remains a deeply stigmatized topic, limiting open discussions and education around menstrual hygiene. This social discomfort often prevents women, especially in rural or conservative areas, from adopting or consistently using sanitary napkins. As a result, market penetration remains low despite increasing product availability.

High Cost and Affordability Issues

Sanitary napkins are still considered a luxury by many low-income populations, especially in developing countries. Limited disposable income forces many women to resort to unhygienic alternatives like cloth or paper. This cost barrier significantly restricts the market’s potential reach among economically disadvantaged groups.

Environmental Concerns Over Disposable Pads

Most disposable sanitary napkins contain plastic and take hundreds of years to decompose, raising serious environmental concerns. Improper disposal and lack of waste management infrastructure contribute to growing landfill waste. These ecological challenges are prompting regulatory scrutiny and consumer pushback in some regions.

Sanitary Napkin Market Opportunities:

The sanitary napkin market presents several promising opportunities driven by evolving consumer needs, technological advancements, and increasing awareness. One major opportunity lies in the expansion into rural and semi-urban regions, where penetration remains low but awareness is steadily rising. Governments and NGOs are actively promoting menstrual hygiene in these areas, creating a favorable environment for market growth. Another key opportunity is the rising demand for biodegradable and reusable sanitary products, especially among environmentally conscious consumers.

Startups and established brands alike can capitalize on this by developing innovative, sustainable alternatives. Digital and e-commerce platforms also open up new channels to reach younger, tech-savvy users with convenience and discretion. Personalization and subscription-based models are gaining traction, offering consumers customized solutions and long-term value. Additionally, the integration of smart materials and skin-sensitive technology provides room for premium product development. Collaborations with educational institutions and public health campaigns can further expand brand visibility and trust. Overall, the market is ripe for innovation, inclusion, and sustainability-focused growth.

SANITARY NAPKIN MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2024 - 2030

|

|

Base Year

|

2024

|

|

Forecast Period

|

2025 - 2030

|

|

CAGR

|

4.6%

|

|

Segments Covered

|

By Product Type, Distribution Channel and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Kao Corporation (Laurier), Hengan International Group Company Limited, Essity Aktiebolag (Libresse), Ontex Group NV (iD, Lille), Natracare (Bodywise UK Ltd) etc.

|

Sanitary Napkin Market Segmentation:

Sanitary Napkin Market Segmentation: by Product Type

- Disposable Sanitary Napkins

- Reusable Sanitary Napkins (Cloth Pads)

- Ultra-thin Pads

- Maxi Pads

- Pantyliners

- Maternity Pads

With a 65% share, disposable sanitary napkins dominate the global market due to their convenience, ease of use, and widespread availability. They are the preferred choice for daily use among urban and semi-urban consumers. Their popularity is especially high in developing countries where government initiatives often distribute these for free or at subsidized rates.

Ultra-thin pads are increasingly popular among young and working women who prioritize discretion and comfort. These pads offer high absorbency despite being lightweight and are widely marketed as modern, lifestyle-friendly options. Their market share continues to grow as manufacturers invest in advanced materials and sleek packaging. They share about 10% to 12% of the market.

Sanitary Napkin Market Segmentation: by Distribution Channel

- Offline Channels (Supermarkets/Hypermarkets, Pharmacies/Drug Stores, Convenience Stores)

- Online Channels (E-commerce Platforms, Direct-to-Consumer (DTC) Brand Websites)

Offline Channels share almost 75% of the market share. These large retail chains are key players in urban and semi-urban regions, offering a wide variety of brands and product types. Their strong shelf visibility, bulk purchasing options, and promotions attract cost-conscious consumers. They are particularly popular in developed markets and metropolitan areas. Pharmacies provide trusted access to sanitary napkins, especially for first-time or health-conscious customers. They are often seen as more private and discreet, appealing to women in conservative communities. Many stock specialty or medicated pads are recommended by healthcare providers. Convenience stores serve immediate or last-minute needs, especially in urban centers. Though their product variety is limited, they benefit from strategic locations and extended hours. Their role is more prominent in countries like Japan, South Korea, and the U.S.

Online Channels share 30% of the market. Platforms like Amazon, Flipkart, and Shopee offer a wide assortment of sanitary napkins with the benefit of home delivery and user reviews. These channels are increasingly preferred by younger consumers for privacy and ease of access. Flash sales, bundles, and digital marketing campaigns further drive growth. Emerging and premium brands are leveraging their own websites to control customer experience, offer subscriptions, and build loyalty. DTC platforms allow for customization, eco-conscious branding, and detailed product education. This segment is small but rapidly growing, especially among Gen Z and millennial users.

Sanitary Napkin Market Segmentation: Regional Analysis

- North America

- Asia-Pacific

- Europe

- South America

- Middle East and Africa

North America is a mature market with high consumer awareness and strong demand for premium and organic sanitary napkins. Ultra-thin and biodegradable products are popular due to environmental concerns. The region benefits from advanced retail infrastructure and growing e-commerce penetration. This region shares 18% of the market.

Asia-Pacific holds the largest share globally, driven by populous countries like India and China. Rising disposable incomes, government initiatives, and increased awareness support strong demand. Both urban and rural markets contribute, with disposables dominating and eco-friendly products gaining momentum. This region shares about 50% of the market.

COVID-19 Impact Analysis on the Global Sanitary Napkin Market:

COVID-19 had a mixed impact on the sanitary napkin market. Initially, lockdowns and supply chain disruptions caused shortages and limited product availability, especially in rural and remote areas. Many manufacturers faced challenges in raw material sourcing and logistics, which temporarily slowed production and distribution. Consumer buying behavior also shifted, with panic buying and stockpiling of essential hygiene products observed in urban centers.

On the other hand, increased hygiene awareness during the pandemic led to a stronger focus on personal care and sanitation, indirectly benefiting the market in the long run. The surge in e-commerce helped bridge distribution gaps as more consumers turned to online shopping to avoid physical stores. However, economic hardships and reduced incomes in many regions impacted affordability, leading some consumers to switch to lower-cost alternatives like cloth pads or homemade options.

Healthcare disruptions also affected menstrual health education programs, slowing awareness campaigns in some areas. Overall, while COVID-19 posed short-term challenges, it accelerated digital transformation and highlighted the importance of menstrual hygiene, setting the stage for future growth once normalcy returned.

Latest Trends/ Developments:

The sanitary napkin market is witnessing a strong shift toward eco-friendly and biodegradable products made from materials like bamboo and organic cotton, driven by growing environmental awareness. Technological advancements have led to ultra-thin pads that offer high absorbency and comfort, meeting consumer demands for discreet and effective solutions. E-commerce growth has fueled subscription-based and direct-to-consumer sales models, providing personalized and convenient delivery options. Innovations are also emerging with smart sanitary napkins featuring sensors to monitor menstrual health in real-time. Companies are expanding into emerging markets by offering localized, affordable products and tailoring marketing strategies to diverse cultural needs. Social media and influencers play a crucial role in educating consumers and shaping brand preferences, promoting transparency and menstrual hygiene awareness. Governments worldwide are supporting the market through subsidies, tax exemptions, and public health campaigns to improve accessibility and reduce stigma. Additionally, product customization is becoming more popular, with brands offering varied sizes, absorbency levels, and special features to meet individual preferences.

Key Players:

- MProcter & Gamble (Always)

- Kimberly-Clark Corporation (Kotex)

- Unicharm Corporation (Sofy)

- Johnson & Johnson (Stayfree)

- Edgewell Personal Care Company (Playtex)

- Kao Corporation (Laurier)

- Hengan International Group Company Limited

- Essity Aktiebolag (Libresse)

- Ontex Group NV (iD, Lille)

- Natracare (Bodywise UK Ltd)