Robotics for Energy Sector Market Size (2024-2030)

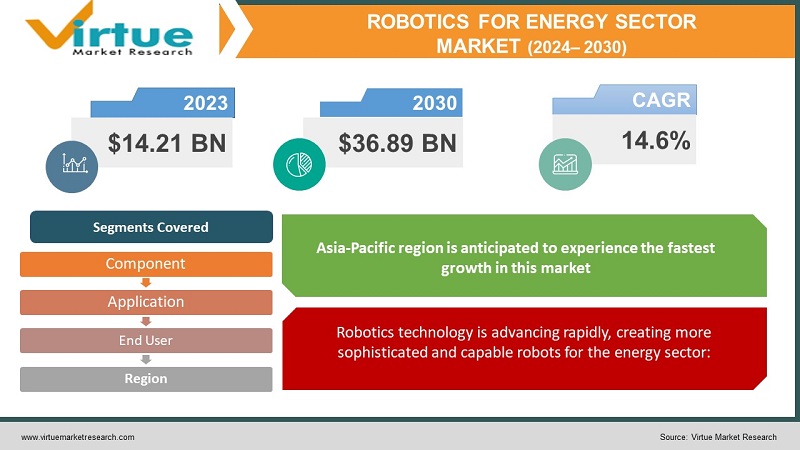

The Global Robotics for Energy Sector Market was valued at USD 14.21 Billion and is projected to reach a market size of USD 36.89 Billion by the end of 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 14.6%.

Robotics is revolutionizing the energy industry by improving different facets of energy source production, distribution, trading, and consumption. Energy sources like sunlight, air, and water are limitless and pure but erratic and sporadic. To balance supply and demand, they need energy storage and grid control systems. Although, a reliable and plentiful source of energy, fossil fuels are also scarce and polluting. Robotics can benefit energy sources in several ways, including lowering labor costs, enhancing performance, safeguarding assets, boosting customer engagement, forecasting energy demand and prices, and maximizing operation and maintenance. The high initial investment, the lack of standards and regulations, the ethical and social ramifications of automation, the cybersecurity risks of data breaches and hacking, the environmental effects of robot disposal and recycling, the need for a skilled workforce, and the lack of education are some of the challenges that robotics also faces in the energy sector.

Global Robotics for Energy Sector Market Drivers:

Various energy users are adopting robotics technology more as a result of the demand for cheaper, more effective maintenance and operation of energy systems:

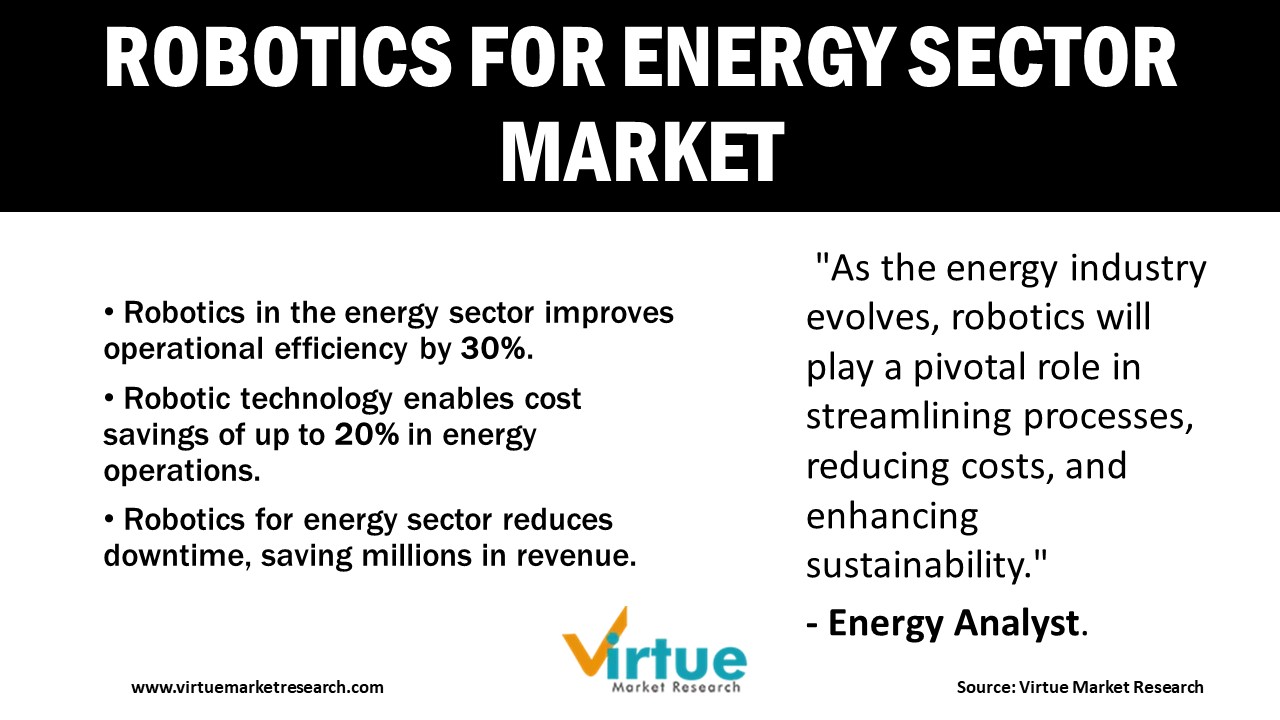

Robotics technology is quickly altering the energy industry by improving the effectiveness, safety, and affordability of energy-related applications. As a result of the creation of new kinds of robots intended for energy-related jobs like maintaining solar panels and keeping an eye on the flow of oil and gas, the market for robotics in the energy sector is growing. Robotics technology is predicted to advance at a rate that will help more and more people, businesses, and governments worldwide satisfy their energy needs while simultaneously improving the sustainability and environmental friendliness of the energy system.

Robotics technology is advancing rapidly, creating more sophisticated and capable robots for the energy sector:

In several ways, robot technology can reduce the cost of producing and distributing energy. Robots can enhance productivity and decrease the demand for manual labor by performing activities more quickly and effectively than humans, which results in cost and time savings. Robots can complete activities in hazardous or difficult locations, protecting workers and lowering the likelihood of accidents, which can help employers save money on insurance and compensation. Robots can monitor and manage energy systems in real-time, decreasing disruptions and increasing system efficiency, saving money on lost revenue and maintenance expenses.

Global Robotics for Energy Sector Market Challenges:

Some energy users may find it hard to pay for the development and use of robot technology in the energy sector:

It can be challenging for some energy sector businesses, particularly smaller ones with tighter budgets, to pay for robot technology. Hardware, software, maintenance, training, and other expenses, such as altering the infrastructure, can all be included in these expenditures. While governments and business organizations provide funding and other resources to enterprises that wish to employ robot technology, other businesses are searching for alternative methods to pay for it to meet these problems. It is envisaged that more businesses will be able to adopt robot technology and profit from increased productivity by overcoming the high costs.

COVID-19 Impact on Global Robotics for Energy Sector Market:

The COVID-19 outbreak has had a contradictory impact on the world market for robotics in the energy sector. While the epidemic has brought about difficulties including a halt in uptake and supply chain interruptions, it has also opened up fresh possibilities for expansion and innovation. The epidemic has brought attention to the significance of remotely monitoring and managing energy systems, which has increased demand for robots with remote control capabilities. The epidemic has sped up the creation of brand-new categories of robots that are intended for energy-related applications, such as those that can carry out jobs in risky or challenging situations. The need for robotics technology in the energy industry is likely to increase over time.

ROBOTICS FOR ENERGY SECTOR MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

14.6%

|

|

Segments Covered

|

By Component, Application, End User, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

ABB Ltd., Fanuc Corporation, Kuka AG, Yaskawa Electric Corporation, Clearpath Robotics Inc., Baker Hughes Company, Schlumberger Limited, National Oilwell Varco, Inc., Aker Solutions ASA, TechnipFMC plc

|

Global Robotics for Energy Sector Market Segmentation:

Global Robotics for Energy Sector Market Segmentation: By Component

Due to the expanding usage of AI and ML technologies in the energy industry, software is projected to be the market category with the greatest growth. As hardware elements like sensors, actuators, and manipulators are crucial for the functioning of robots in the energy sector, hardware is projected to have the lion's share of the market. Overall, it is anticipated that the market for robotics in the energy sector will keep expanding due to the demand for more effective and economical maintenance and operation of energy systems.

Global Robotics for Energy Sector Market Segmentation: By Application

- Solar panel installation

- Wind turbine maintenance

- Hydroelectric power plant operation

- Exploration

- Remotely operated vehicles

- Autonomous underwater vehicles

- Unmanned aerial vehicles

- Unmanned ground vehicles

The usage of UAVs is perhaps the market segment that is growing the fastest. This is because UAVs are being used more frequently in the energy sector for activities including inspection, monitoring, and mapping. In addition to other uses, UAVs can inspect pipelines, power lines, and wind turbines more quickly and affordably than conventional techniques. The utilization of ROVs is perhaps the market segment that has the biggest market share. This is because the energy industry makes extensive use of ROVs for jobs like offshore drilling rig maintenance and underwater inspection. Because they can operate in challenging and dangerous conditions, ROVs are a crucial tool for the energy industry.

Global Robotics for Energy Sector Market Segmentation: By End-user

- Solar energy Industry

- Wind Energy Industry

- Hydroelectric Power Industry

- Oil and gas industry

- Coal mining Industry

- Others

The adoption of robot technology by solar energy companies is projected to be the market category with the highest growth. This is because solar energy systems are being used more widely around the world, which is driving up the demand for robots that can efficiently and affordably inspect and repair solar panels. The employment of robotics technology by wind energy companies is probably the most dominating market segment. This is precisely wind energy—now the most widely utilized renewable energy source—that requires routine maintenance and inspection to function safely and optimally. In this industry, oil and gas businesses constitute a significant end-user segment as well, notably for jobs like pipeline inspection and maintenance. Another significant end-user group in this sector is utility firms, notably for jobs like operating and maintaining power plants. Utility businesses are in charge of running and maintaining vital infrastructure, which can considerably benefit from the application of robot technology. Additionally, significant end-user markets in this industry include coal mining firms and hydroelectric power companies, particularly for duties like mine inspection and maintenance and dam inspection and maintenance, respectively.

Global Robotics for Energy Sector Market Segmentation: By Region

- North America

- Europe

- Asia-Pacific

- South America

- Middle East and Africa.

The Asia-Pacific region is anticipated to experience the fastest growth in this market sector since countries like China and India are utilizing renewable energy systems at an accelerated rate. North America is likely to hold the highest share of this market due to the extensive usage of robotics technology in the non-renewable energy business, particularly in the United States. Europe is a sizable market for robotics in the energy sector, especially for renewable energy systems. Emerging markets for robotics in the energy sector include Latin America, the Middle East, and Africa. Energy sectors have significant growth potential in these regions.

Key Players:

- ABB Ltd.

- Fanuc Corporation

- Kuka AG

- Yaskawa Electric Corporation

- Clearpath Robotics Inc.

- Baker Hughes Company

- Schlumberger Limited

- National Oilwell Varco, Inc.

- Aker Solutions ASA

- TechnipFMC plc