Preventive Health Tools Market Size (2024 – 2030)

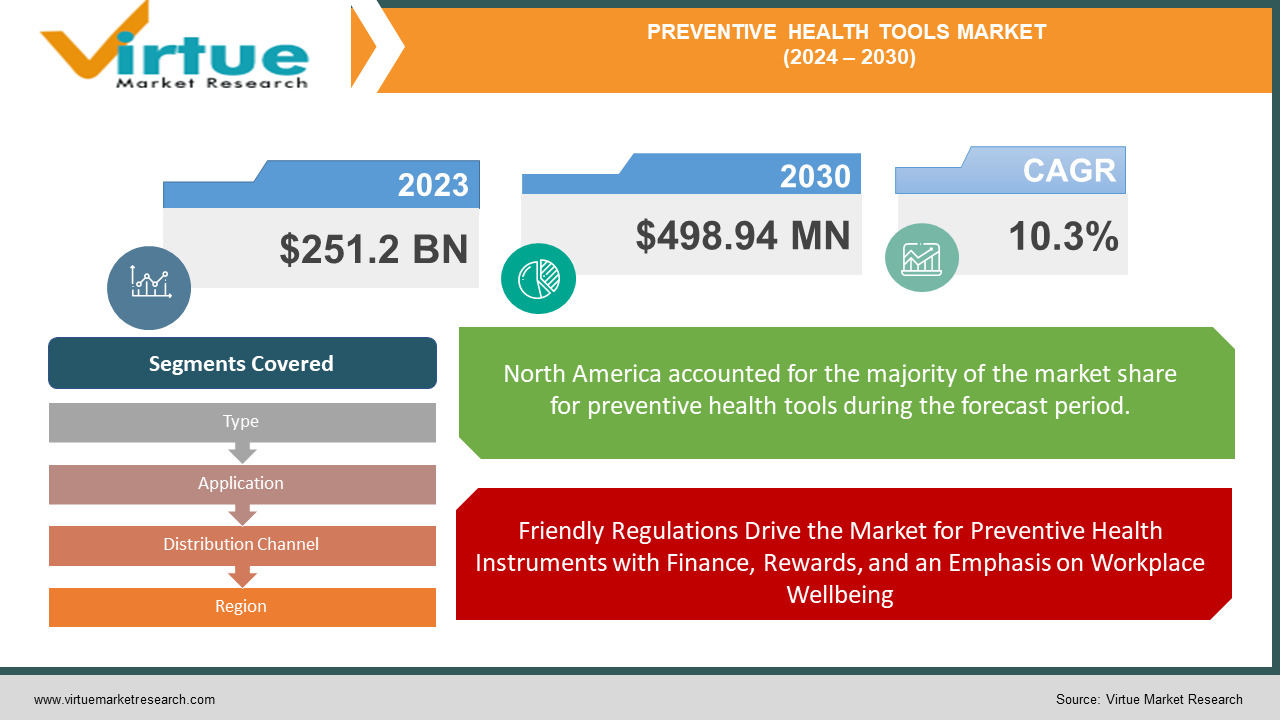

The Global Preventive Health Tools Market was valued at USD 251.2 billion in 2023 and is projected to reach a market size of USD 498.94 million by 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 10.3%.

With the help of preventive health tools, you can take control of your health. These tools include routine behaviours that provide a solid basis for your health, such as eating a balanced meal, exercising frequently, and getting enough sleep. Furthermore, immunisations protect you against infectious diseases by exposing your body to dormant or weakened strains of bacteria or viruses and teaching it how to fight them off. Screenings that are customised based on your age and risk factors work as early warning systems for any health issues, enabling prompt intervention and better treatment results. You may greatly improve your chances of living a longer, healthier life, possibly avoiding major health problems, and saving money on future medical bills by implementing these preventative practices. Consult your physician to develop a preventative health plan that is specific to your requirements.

Key Market Insights:

Around the world, 73% of customers are interested in tracking their health via wearable technology. This demonstrates the expanding market for wearables, smartphone applications, and other digital tools that assist users in tracking their activity levels, sleep habits, and other health-related data.

Adults 65 years of age and older are predicted to make up around 20% of the US population by 2030. This group places a high value on preventative care and has extra money to spend on the necessary supplies and services.

The COVID-19 pandemic hastened the uptake of remote patient monitoring and telemedicine. This pattern is anticipated to continue, with an increasing emphasis on instruments that facilitate the early identification of chronic illnesses like diabetes and heart disease.

In the US, 67% of major firms provide some kind of wellness programme. To save healthcare costs and enhance employee wellbeing, these programmes frequently include fitness challenges, wearable integration, and health screenings as incentives for preventative activities.

Global Preventive Health Tools Market Drivers:

Crisis of Chronic Illnesses Accelerates Increase in Tools for Preventive Health Market Early Detection and Management: Essential for a Future Healthier

The increasing burden of chronic illnesses presents a significant challenge to the state of world health. According to the World Health Organisation (WHO), chronic diseases including diabetes, cancer, heart disease, and chronic respiratory ailments are growing more common and cause over 70% of deaths worldwide. The market for preventative health instruments has a lot of potential because of this concerning trend. By giving people, the ability to manage their current chronic diseases and detect risk factors, these tools can empower people to take control of their health and perhaps prevent catastrophic illness. This might result in a market boom as consumers look for ways to manage or avoid chronic illnesses more effectively, which would eventually make people healthier and alleviate the burden on healthcare systems.

Friendly Regulations Drive the Market for Preventive Health Instruments with Finance, Rewards, and an Emphasis on Workplace Wellbeing

Governments throughout the world are becoming more involved in promoting preventative healthcare as they realise the financial and social costs associated with chronic illnesses. This results in a notable increase in the market for preventative health measures. Direct financing of initiatives promoting preventative health. To increase awareness and facilitate early diagnosis, these programmes may include free or heavily discounted testing for conditions including diabetes and cancer. Governments may introduce tax benefits for wellness and health-related items, lowering the cost of devices like activity trackers and nutritious food alternatives for a larger audience. Encouraging workplace wellness initiatives is an additional effective strategy. Governments may promote a preventative care culture in the workforce by offering incentives to corporations that provide exercise challenges, health screenings, and wearable integration. The market for preventive health technologies benefits from these initiatives, which ultimately aim to lower healthcare expenditures.

Global Preventive Health Tools Market Restraints and Challenges:

Cost is a significant obstacle, especially for those with low and moderate incomes, as some wearables, subscriptions, and screenings can be pricey. People may not understand the significance of these technologies or how to use them successfully if there is a lack of public knowledge and education about them and their advantages. Some consumers are also discouraged by data privacy worries about the acquisition of lifestyle data and personal health measurements. Healthcare practitioners seeking a comprehensive understanding of their patient's health face difficulties due to the lack of integration between preventive health technologies and traditional healthcare systems. Accessibility may be further restricted by insurance companies' limited reimbursement for certain exams and technologies. Strategies like creating more accessible tools, stepping up public education, putting strong data security in place, encouraging better healthcare system integration, and pushing for more insurance coverage for preventive health services are essential to overcoming these challenges and realising the market's full potential.

Global Preventive Health Tools Market Opportunities:

The market for preventative health solutions has a tonne of interesting prospects in store. AI-powered personalised medicine may develop unique treatment plans based on a patient's genetic makeup and needs, which may enable earlier illness identification and more focused therapies. Furthermore, an increasing emphasis on mental health creates opportunities for solutions that deal with anxiety, stress, and sleep problems. Another area that is prime for expansion is workplace wellness initiatives, as businesses look for ways to control the rising expenses of employee healthcare. There is a great deal of promise for better patient care and fewer hospital admissions with digital treatments, app-based therapies for chronic illnesses, and remote patient monitoring devices that measure vital signs. Finally, the growing accessibility of wearables and smartphones in underdeveloped nations opens a sizable new market for producers who can provide affordable and culturally appropriate preventive health instruments.

PREVENTIVE HEALTH TOOLS MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

10.3% |

|

Segments Covered

|

By Type, Application, Distribution Channel and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Abbott Laboratories (US), Apple (US), Calm (US), Clue (Germany), Empatica (Finland), Fitbit (US), Flo Health (US), Johnson & Johnson (US), Lilia (US), Livongo Health (US), Omron Healthcare (Japan), Oura Ring (Finland), Samsung (South Korea), Teladoc Health (US), Whoop (US)

|

Global Preventive Health Tools Market Segmentation: By Type

-

Early Detection & Screening Technologies

-

Chronic Disease Management Technologies

-

Vaccines

-

Advanced Technologies to Reduce Errors

Type-wise, the global market for preventive health tools is divided, with Early Detection & Screening Technologies now occupying the leading position. Health concerns can be identified early thanks to these techniques. However, Chronic Disease Management Technologies is the market sector expected to develop at the highest rate. The increased incidence of chronic diseases and the growing focus on efficient management to enhance patient well-being and lower healthcare costs are the main causes of this upsurge.

Global Preventive Health Tools Market Segmentation: By Application

-

Cardiovascular Disease Prevention

-

Cancer Screening and Prevention

-

Diabetes Management

-

Mental Health and Wellbeing

Through application segmentation, the worldwide market for preventive health tools covers a range of health issues. Because heart illness is so common, the market is now dominated by cardiovascular disease prevention. But as mental health becomes more widely acknowledged as a vital component of well-being, the market for products that address stress, anxiety, and sleep issues is expected to rise at the quickest rate.

Global Preventive Health Tools Market Segmentation: By Distribution Channel

The market for preventive health tools worldwide makes use of several distribution methods. Currently, hospitals and clinics set the standard by utilising direct patient engagement to increase sales and recommendations. But given the ease with which these tools can be obtained directly from brand websites and apps, as well as the increasing popularity of online buying, the future belongs to Direct-to-Consumer Brands.

Global Preventive Health Tools Market Segmentation: By Region

-

North America

-

Asia-Pacific

-

Europe

-

South America

-

Middle East and Africa

Geographically speaking, North America leads the worldwide market for preventive health tools because of its high healthcare expenditure, tech-savvy populace, and government assistance. However, the largest increase is expected to occur in the Asia-Pacific area. This is driven by a youthful population accustomed to digital health solutions, a growing middle class with disposable cash, and an increasing awareness of preventative actions.

COVID-19 Impact Analysis on the Global Preventive Health Tools Market:

The market for preventative health solutions saw mixed results from the COVID-19 epidemic. On the bad side, a decrease in routine examinations and screenings was brought on by lockdowns and fear of the virus, which could have exacerbated health consequences. Some tool shortages were also caused by interruptions in the supply chain. Furthermore, the emphasis on preventative care was momentarily diverted by overburdened healthcare institutions. But there were also advantages to the epidemic. The availability of preventative healthcare has expanded with the emergence of telehealth consultations and remote monitoring. Public health consciousness increased interest in cleanliness and immune-boosting products. Finally, the emphasis on mental health amid social isolation and stress increased demand for sleep, anxiety, and stress management products. Even though there was a big initial interruption, things should become better in the long run.

Recent Trends and Developments in the Global Preventive Health Tools Market:

Riding the trend of innovation is the global market for preventative health products. With its use in personalised risk assessment, chatbots for health coaching, and even AI-powered diagnostics, artificial intelligence is causing a stir. Period trackers, fertility monitors, and wearable breast health monitors are examples of femitech products that target women's health requirements. With engaging applications and wearable challenges, gamification is bringing fun into the realm of health maintenance. The market has sophisticated sleep monitors and applications for improved sleep hygiene because companies understand how important sleep is. Using meditation techniques and mindfulness applications, mental wellness is also prioritised. Employers are funding employee health initiatives that include on-site exams, workout challenges, and wearable technology. Predictive analytics and big data are being utilised to forecast possible health hazards and make well-informed decisions about preventative treatment.

Key Players:

-

Abbott Laboratories (US)

-

Apple (US)

-

Calm (US)

-

Clue (Germany)

-

Empatica (Finland)

-

Fitbit (US)

-

Flo Health (US)

-

Johnson & Johnson (US)

-

Lilia (US)

-

Livongo Health (US)

-

Omron Healthcare (Japan)

-

Oura Ring (Finland)

-

Samsung (South Korea)

-

Teladoc Health (US)

-

Whoop (US)