Personal Cloud Market Size (2024-2030)

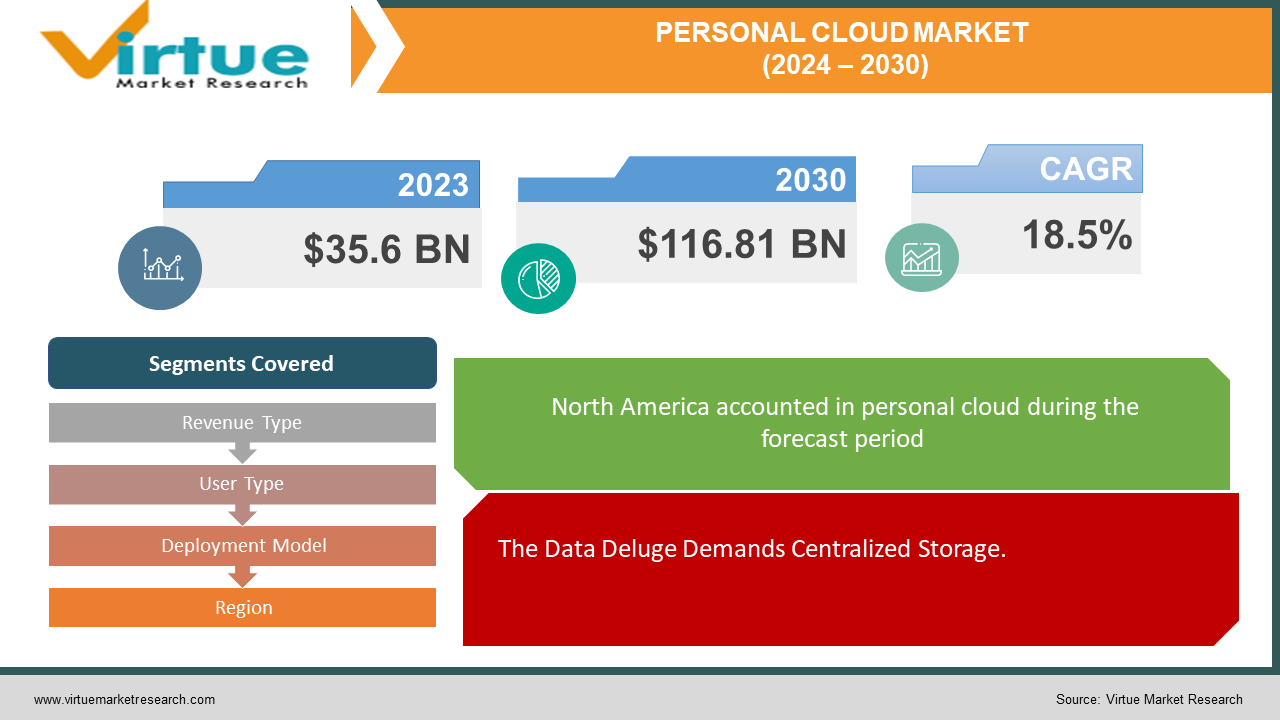

The Personal Cloud Market was valued at USD 35.6 billion in 2023 and is projected to reach a market size of USD 116.81 billion by the end of 2030. Over the cast period of 2024 – 2030, the figure for requests is projected to grow at a CAGR of 18.5%.

The personal cloud market is flourishing as individuals seek secure and accessible ways to store their exploding amount of digital data. This surge is fueled by factors like the ever-growing volume of photos, videos, and documents we create the multitude of devices we use daily, and the growing emphasis on data privacy. Personal cloud solutions come in various forms, with popular options like Dropbox and Google Drive offering remote storage on provider servers. Alternatively, Network-Attached Storage (NAS) devices act as centralized storage hubs on a home network, accessible to all connected devices. Tech-savvy users can even set up their servers for ultimate control. When choosing a personal cloud solution, factors like storage capacity, security features, ease of use, and cost all play a crucial role.

Key Market Insights:

Security is a key driver in the personal cloud market. As data privacy concerns rise, users are increasingly looking for safer alternatives to storing data on individual devices, which can be vulnerable. Personal cloud services provide a secure haven for this valuable information. The personal cloud market caters to a diverse range of needs with a variety of solutions available. Popular options include online storage services like Dropbox and Google Drive, offering remote storage on provider servers. Network-attached storage (NAS) devices act as centralized storage hubs on a home network, accessible to all connected devices. Tech-savvy users can even set up their servers for ultimate control.

The Personal Cloud Market Drivers:

The Data Deluge Demands Centralized Storage.

The digital age has transformed us into data creators. We capture countless photos and videos on high-resolution smartphones, accumulate work documents in various formats, and curate music libraries spanning decades. This data avalanche necessitates secure and accessible storage solutions. Traditional methods like external hard drives can become cumbersome, especially when juggling data across multiple devices. Personal cloud services offer a centralized hub, consolidating your data in one secure location accessible from anywhere with an internet connection. Imagine a virtual filing cabinet accessible from your phone, laptop, or even a friend's computer – that's the power of the personal cloud.

Mobile Mania necessitates Remote Access Anywhere.

Gone are the days of a single desktop computer managing all our digital needs. Today, we're a mobile society, constantly switching between smartphones, tablets, and laptops. This mobility presents a challenge: ensuring our data is readily available across all devices. Personal cloud services come to the rescue with seamless syncing capabilities. Any edits made to a file on one device are automatically reflected on all others connected to the cloud storage. This ensures you always have the latest version of your documents, photos, and other files at your fingertips, regardless of which device you're using. No more emailing yourself files or carrying around bulky external drives – your data becomes truly mobile with the personal cloud.

The Security Siege Fuels the Need for Robust Protection.

As our reliance on digital data grows, so do concerns about data privacy. The threat of cyberattacks and data breaches looms large, making users wary of storing sensitive information on individual devices vulnerable to loss or hacking. Personal cloud services act as a robust security fortress. Many platforms utilize encryption technologies to scramble your data, making it unreadable to unauthorized users. Imagine your data locked away in a digital vault, protected by strong encryption. Additionally, features like two-factor authentication and access controls add further layers of protection, ensuring only authorized individuals can access your valuable information. Peace of mind comes standard with personal cloud storage.

Cost-Conscious Considerations Lead to Cloud Storage.

Personal cloud storage can be surprisingly cost-effective compared to traditional methods. External hard drives require an upfront investment and may need frequent upgrades as your storage needs evolve. Personal cloud services often offer tiered storage plans, allowing you to choose the amount of space you need at a price that fits your budget. Think of it as paying for electricity – you only pay for what you use. Additionally, some cloud storage providers offer free base plans, making it an accessible option for everyone.

The Personal Cloud Market Restraints and Challenges:

The personal cloud market, despite its impressive growth, faces hurdles that can slow its full potential. A significant challenge is limited internet connectivity. Personal cloud services require robust and consistent internet connections to function smoothly. In areas with slow speeds, frequent outages, or limited access altogether, users can experience disruptions when uploading, downloading, or simply accessing their data.

Security and privacy concerns are another hurdle. While cloud providers offer security features, some users remain hesitant to entrust their data to a third party. Data breaches and privacy worries can deter potential users from adopting personal cloud solutions. Cost can also be a barrier. Tiered storage plans offer some flexibility, but for users requiring significant storage, personal cloud storage can become expensive. Free plans often come with limited storage, forcing users to pay for additional space as their data needs grow.

Integration issues arise when trying to seamlessly connect personal cloud services with other applications. This can create a fragmented user experience, requiring users to switch between platforms to manage their data. Finally, vendor lock-in can be an issue. Users who become heavily reliant on a specific cloud storage provider may face difficulties if they decide to switch services later. Transferring data between different cloud platforms can be complex and time-consuming. These challenges highlight the need for the personal cloud market to address user concerns about connectivity, security, cost, and flexibility to ensure continued growth.

The Personal Cloud Market Opportunities:

The personal cloud market, driven by our expanding digital needs, offers exciting avenues for growth and innovation. One key area lies in integrating with emerging technologies like Artificial Intelligence (AI). AI could revolutionize cloud storage by automatically categorizing and tagging files, making them more searchable and manageable. Additionally, AI-powered security features could provide even stronger data protection. Furthermore, focusing on user experience is crucial. Simpler interfaces, intuitive mobile apps, and seamless file sharing across devices will attract more users. The market can also expand by catering to specific user groups. Cloud storage solutions tailored for photographers, gamers, or families with unique needs can attract new customer segments. Hybrid cloud options, combining personal cloud storage with on-premises solutions, might appeal to users seeking a balance between cloud convenience and local data control. Partnerships and integrations with device manufacturers or software developers can broaden the reach of personal cloud services. Pre-installed cloud storage on new devices or seamless integration with popular productivity tools can be significant draws for new users. Finally, building trust with users through transparency about data handling practices, strong encryption protocols, and robust access controls will be critical differentiators in the market. By capitalizing on these opportunities, the personal cloud market can overcome existing challenges and thrive in the ever-changing digital landscape.

PERSONAL CLOUD MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

18.5% |

|

Segments Covered

|

By Revenue Type, User Type, Deployment Model, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Google, Microsoft, Apple, Dropbox, Amazon Web Services (AWS), Box, Seagate Technology, Western Digital, Synchronoss, Egnyte

|

Personal Cloud Market Segmentation: By Revenue Type

-

Direct Revenue

-

Indirect Revenue

The most dominant revenue segment in the personal cloud market is direct revenue, generated through user subscriptions for storage plans. This traditional model offers clear value to both users and providers. However, the fastest-growing segment is expected to be the freemium model. By offering free base plans with limited storage, providers attract new users who can then be converted to paying customers if their storage needs increase. This freemium approach allows users to try the service before committing and expands the overall market reach for personal cloud storage.

Personal Cloud Market Segmentation: By User Type

The dominant segment in the personal cloud market by User Type is Individual Users. This broad category encompasses everyone from personal users storing photos and documents to students and remote workers who need secure access to their files. The fastest-growing segment, however, is Small and Medium Enterprises (SMEs). As businesses look for affordable and scalable solutions for data storage, collaboration, and backup, they are increasingly turning to personal cloud services.

Personal Cloud Market Segmentation: By Deployment Model

-

Public Cloud

-

Private Cloud

-

Hybrid Cloud

By deployment model, the public cloud segment reigns supreme in the personal cloud market. Its affordability, scalability, and ease of use make it the most dominant choice for users seeking remote access to their data. However, the fastest-growing segment is likely the hybrid cloud. This model caters to users with diverse data security needs. It offers the flexibility of storing sensitive information on a private cloud while leveraging the public cloud's cost-effectiveness and scalability for less critical data.

Personal Cloud Market Segmentation: Regional Analysis

-

North America

-

Europe

-

Asia-Pacific

-

South America

-

Middle East and Africa

North America is the personal cloud market's frontrunner. Early technology adoption and a robust internet infrastructure have fueled high adoption rates. Major cloud storage providers hold a strong position, with users favoring established platforms offering a wide range of features.

In stark contrast to North America, data privacy is a top concern for European users. Personal cloud services that prioritize robust security features and transparent data handling practices are likely to find success in this market. While growth is expected, regulations and user preferences can vary significantly across individual European countries, requiring a nuanced approach from cloud service providers.

Asia-Pacific region boasts the fastest personal cloud market growth due to its booming digital population and rapidly expanding internet access. However, infrastructure development remains uneven across the vast region, leading to disparities in adoption rates. Price sensitivity is also a key factor, with users potentially favoring cost-effective storage solutions compared to feature-rich premium plans.

COVID-19 Impact Analysis on the Personal Cloud Market:

The COVID-19 pandemic acted as a major growth accelerator for the personal cloud market. Lockdowns and social distancing measures triggered a global shift towards remote work and online learning, dramatically increasing the need for accessible and secure data storage. Personal cloud services perfectly addressed this by allowing users to seamlessly access files and work documents from anywhere with an internet connection.

Furthermore, with traditional in-person collaboration becoming limited, the demand for cloud-based collaboration tools skyrocketed. Many personal cloud services offer features like file sharing, real-time document editing, and version control, facilitating efficient teamwork despite physical separation. The pandemic also highlighted the importance of secure and reliable data storage, leading to a significant increase in new user adoption across all age groups and demographics.

However, challenges emerged alongside this growth. Limited internet bandwidth in certain regions could disrupt seamless access to cloud storage. Additionally, concerns about data security and privacy during a time of heightened online activity remained a concern for some users.

Looking ahead, the long-term impact of COVID-19 is expected to be positive for the personal cloud market. The shift towards remote work and online collaboration is likely to continue, creating a sustained demand for personal cloud storage solutions. Cloud service providers who prioritize robust security features, user-friendly interfaces, and seamless integration with collaboration tools will be well-positioned to capitalize on this ongoing trend.

Latest Trends/ Developments:

The personal cloud market is pushing beyond basic storage, embracing innovative trends to enhance functionality and user experience. Integration with Artificial Intelligence (AI) is a major development. Imagine AI automatically organizing your files through automatic categorization and tagging, making them effortless to find. AI could even analyze your storage habits, suggesting data optimization or predicting future needs.

Security and privacy remain paramount. Cloud providers are developing advanced features like zero-knowledge encryption, where even the provider can't access your data without your key. Additionally, multi-factor authentication and access controls ensure only authorized users see your information.

Flexibility in storage options is a rising demand. Hybrid cloud models, combining personal cloud storage with on-premises solutions, are gaining traction. Similarly, multi-cloud solutions are emerging, allowing users to store data across multiple providers for enhanced security and redundancy.

Looking to the future, blockchain technology holds the potential to revolutionize data ownership and security. Blockchain could create an unalterable record of data ownership and access, potentially empowering users with greater control. Finally, user experience remains a key focus. Simplifying interfaces, offering seamless integration with popular tools, and ensuring features like real-time file sync across devices and offline access are all crucial for a smooth user experience. By embracing these advancements, personal cloud service providers can solidify their position in a competitive market and cater to the evolving needs of users in the digital age.

Key Players:

-

Google

-

Microsoft

-

Apple

-

Dropbox

-

Amazon Web Services (AWS)

-

Box

-

Seagate Technology

-

Western Digital

-

Synchronoss

-

Egnyte