Organosilicon Polymers Market Size (2024 – 2030)

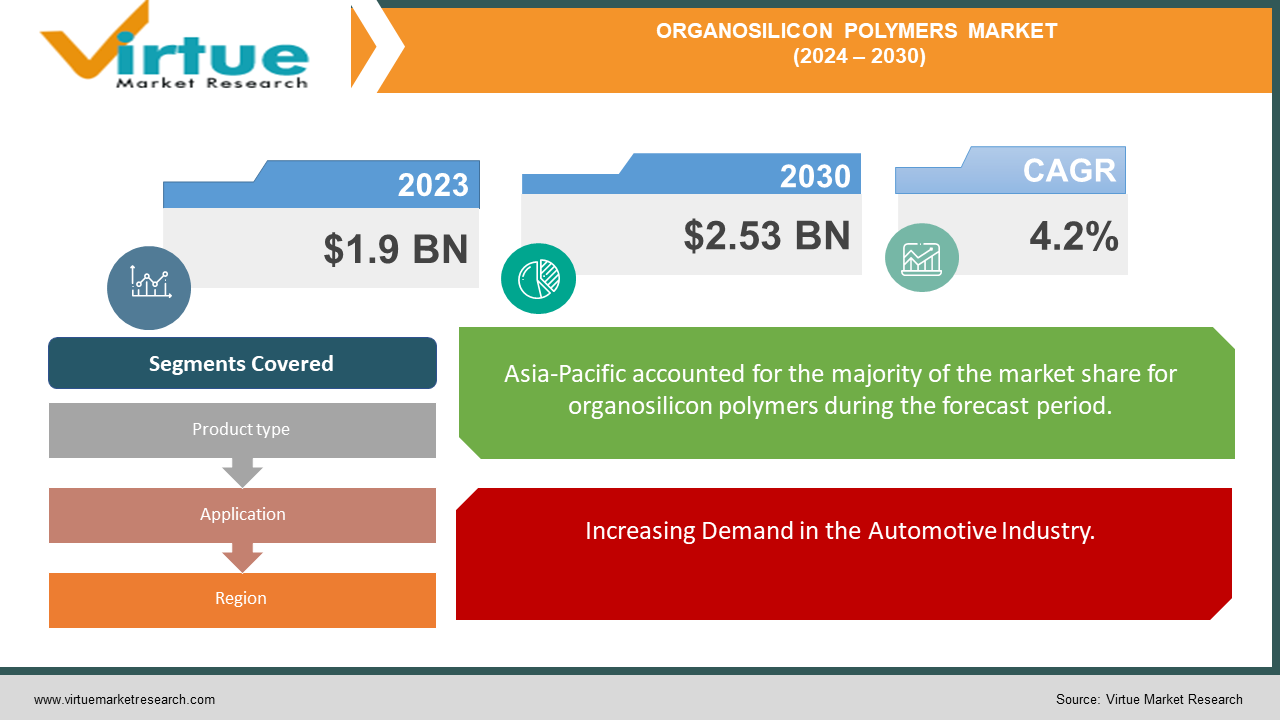

The Global Organosilicon Polymers Market was valued at USD 1.9 billion in 2023 and is projected to reach a market size of USD 2.53 billion by the end of 2030. The market is anticipated to expand at a compound annual growth rate (CAGR) of 4.2% between 2024 and 2030.

The Organosilicon Polymers Market is experiencing significant growth driven by their versatile applications and superior properties. These polymers, known for their unique silicon-oxygen backbone, offer exceptional thermal stability, flexibility, and resistance to weathering, making them indispensable in various industries. In the automotive sector, they enhance durability and performance in sealants, gaskets, and coatings, while in electronics, their dielectric properties are crucial for advanced applications. The construction industry benefits from their use in sealants and adhesives, ensuring the longevity and resilience of structures. Additionally, the healthcare sector leverages its biocompatibility for medical devices and implants. The demand is further bolstered by ongoing research and innovation, leading to advanced formulations with enhanced properties. Environmental concerns are also addressed through the development of eco-friendly variants. The market is witnessing a surge in demand from emerging economies, driven by rapid industrialization and urbanization. Key players are focusing on strategic collaborations, mergers, and acquisitions to strengthen their market position and expand their product portfolio. With continuous advancements and increasing applications across various sectors, the Organosilicon Polymers Market is poised for robust growth in the coming years.

Key Market Insights:

Asia-Pacific accounted for over 40% of the market share in 2022, making it the largest regional market due to rapid industrialization and urbanization in countries like China and India.

The automotive industry represents approximately 25% of the total demand for organosilicon polymers, driven by their application in sealants, gaskets, and coatings.

Electronics applications hold around 20% of the market share, leveraging the polymers' dielectric properties for advanced electronic devices.

The construction sector utilizes about 30% of organosilicon polymers, particularly in sealants and adhesives, ensuring the durability and resilience of structures.

Biocompatible organosilicon polymers used in the healthcare industry account for approximately 10% of the market, with growing applications in medical devices and implants.

Eco-friendly variants of organosilicon polymers are expected to see a growth rate of 7.2% annually, reflecting the increasing demand for sustainable materials.

North America holds around 25% of the market share, with significant contributions from the automotive and construction industries.

Europe represents about 20% of the market, driven by stringent regulations and a focus on sustainable development.

Research and development activities constitute approximately 8% of the total investment in the organosilicon polymers market, underlining the emphasis on innovation and advanced formulations.

Organosilicon Polymers Market Drivers:

Increasing Demand in the Automotive Industry.

The Organosilicon Polymers Market is witnessing robust growth driven by the automotive industry’s increasing demand for high-performance materials. These polymers are prized for their exceptional thermal stability, flexibility, and resistance to harsh environmental conditions, making them ideal for a range of automotive applications such as sealants, gaskets, and coatings. With the automotive industry continually evolving towards more advanced and efficient vehicles, the need for materials that can withstand extreme temperatures and chemical exposures has never been greater. Additionally, the push for lightweight materials to enhance fuel efficiency and reduce emissions is accelerating the adoption of organosilicon polymers. The integration of these polymers in electric vehicles (EVs) for components such as battery housings and insulation also presents significant growth opportunities. As automotive manufacturers strive to meet stringent environmental regulations and consumer expectations for durability and performance, the demand for organosilicon polymers is set to surge, propelling the market forward.

Rapid Urbanization and Industrialization in Emerging Economies.

The rapid pace of urbanization and industrialization in emerging economies is a significant driver for the Organosilicon Polymers Market. Countries such as China, India, and Brazil are experiencing unprecedented growth in infrastructure development, leading to increased demand for high-performance construction materials. Organosilicon polymers, known for their durability, weather resistance, and flexibility, are becoming integral in construction applications, including sealants, adhesives, and coatings. The expansion of manufacturing sectors in these regions also fuels the demand for organosilicon polymers in various industrial applications. Furthermore, the growing middle-class population in these countries is driving the demand for consumer goods and electronics, where organosilicon polymers play a crucial role due to their excellent dielectric properties and thermal stability. Government initiatives to boost industrial growth and infrastructure development are further amplifying this demand. As emerging economies continue to develop, the increasing need for advanced materials to support their growth trajectories is expected to significantly propel the organosilicon polymers market.

Organosilicon Polymers Market Restraints and Challenges:

The Organosilicon Polymers Market faces several restraints and challenges that could impede its growth trajectory. One of the primary challenges is the high cost of production associated with these advanced polymers. The intricate manufacturing processes and the need for specialized raw materials contribute to their elevated prices, which can be a deterrent to widespread adoption, especially in cost-sensitive industries. Additionally, the market is subject to stringent regulatory frameworks regarding the use of chemicals, which vary across regions. Compliance with these regulations requires significant investment in research and development, further escalating costs. Environmental concerns also pose a challenge, as the production and disposal of organosilicon polymers can have adverse ecological impacts if not managed properly. Moreover, the market faces competition from alternative materials that offer similar properties at lower costs, such as organic polymers and other synthetic materials. These alternatives can limit the market penetration of organosilicon polymers. Lastly, the market's reliance on a few key industries, such as automotive and construction, makes it vulnerable to economic downturns in these sectors. Addressing these challenges requires continuous innovation, cost-reduction strategies, and adherence to evolving environmental and regulatory standards to sustain growth and competitiveness in the market.

Organosilicon Polymers Market Opportunities:

The Organosilicon Polymers Market presents significant growth opportunities driven by their unique properties and broad application spectrum. These polymers, known for their exceptional thermal stability, flexibility, and resistance to weathering, are increasingly in demand across various industries. In the automotive sector, their use in manufacturing lightweight, durable components supports the shift towards fuel-efficient and electric vehicles. The electronics industry leverages organosilicon polymers for their excellent dielectric properties and thermal stability, crucial for high-performance electronic devices and advanced packaging solutions. Additionally, the construction industry benefits from their use of sealants and coatings that enhance durability and energy efficiency. The healthcare sector also explores these polymers for medical devices and implants due to their biocompatibility and flexibility. With growing investments in research and development, new and innovative applications continue to emerge, further expanding market potential. The shift towards sustainable and eco-friendly materials also boosts demand, as organosilicon polymers can be engineered to meet stringent environmental regulations. As industries increasingly prioritize high-performance materials that offer longevity and resilience, the organosilicon polymers market is poised for robust growth, driven by technological advancements and expanding application areas.

ORGANOSILICON POLYMERS MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

4.2% |

|

Segments Covered

|

By Product type, Application, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Dow Corning Corporation, Wacker Chemie AG, Shin-Etsu Chemical Co., Ltd., Momentive Performance Materials Inc., Elkem ASA, Evonik Industries AG, KCC Corporation, Gelest, Inc., Innospec Inc., Silchem Inc.

|

Organosilicon Polymers Market Segmentation: By Product Type

-

Silicone oil

-

Silicone rubber

-

Silicone resin

-

Silicone emulsion

The Global Organosilicon Polymers Market by Product Type, Silicone Rubber market share last year and is poised to maintain its dominance throughout the forecast period. Silicone rubber's unique combination of heat resistance, flexibility, water repellency, and electrical insulation underscores its versatility and suitability for diverse applications across the automotive, construction, healthcare, electronics, and aerospace industries. As a mature market, silicone rubber technology benefits from extensive research and development, resulting in optimized products and processes. Strong demand drivers include the growth of the automotive industry, increased construction activities, and advancements in electronics. However, the market faces potential challenges and future trends that could impact its trajectory. Competition from silicone oils and resins in specific applications may affect silicone rubber's market share, while fluctuations in raw material costs can influence profitability and market competitiveness. Moreover, sustainability concerns are prompting the industry to develop eco-friendly silicone rubber products to comply with stringent environmental regulations. Despite these challenges, silicone rubber remains a dominant player in the organosilicon polymers market. Its continued dominance will depend on its ability to adapt to changing market conditions, leverage technological advancements, and meet evolving consumer preferences, ensuring it remains a preferred material in a wide array of high-performance applications.

Organosilicon Polymers Market Segmentation: By Application

-

Coatings

-

Elastomers

-

Foams

-

Adhesives & Sealants

The Global Organosilicon Polymers Market by Application, Coatings market share last year and is poised to maintain its dominance throughout the forecast period. Silicone coatings are integral to various industries, including automotive, construction, marine, and industrial, due to their diverse applications and protective properties. These coatings offer exceptional resistance to weather, UV radiation, chemicals, and high temperatures, making them ideal for protecting surfaces and enhancing durability. Additionally, silicone coatings can provide aesthetically pleasing, glossy finishes that improve the appearance of products. However, the dominance of silicone coatings in the organosilicon polymers market is influenced by several factors. Competition from other applications such as elastomers, adhesives, and sealants represents significant and growing market segments that could impact the coatings market share. Economic conditions play a crucial role, as the construction and automotive industries, which are major consumers of silicone coatings, are sensitive to economic cycles. Technological advancements in other applications could also shift the market dynamics, potentially leading to increased competition for coatings. While silicone coatings currently hold a substantial portion of the organosilicon polymers market, it is essential to monitor the evolving dynamics of other application segments and potential market shifts to maintain their market position and adapt to changing industry needs and innovations.

Organosilicon Polymers Market Segmentation: By Region

-

North America

-

Europe

-

Asia-Pacific

-

South America

-

Middle East and Africa

The Global Organosilicon Polymers Market by Region, Asia-Pacific market share last year and is poised to maintain its dominance throughout the forecast period. Asia Pacific's dominance in the organosilicon polymers market is driven by rapid industrialization in countries like China, India, and South Korea, leading to increased demand across various industries. The region benefits from cost-competitive manufacturing due to lower labor costs and abundant raw material resources, establishing it as a global manufacturing hub for organosilicon polymers. The growing automotive and construction sectors, major consumers of these polymers, further propel market growth. Additionally, Asia Pacific's focus on renewable energy projects creates new opportunities for organosilicon polymers, essential for high-performance applications. However, the region faces challenges that must be addressed to sustain its leadership. Ensuring a stable supply of high-quality raw materials is crucial for maintaining competitiveness. Compliance with stringent environmental regulations is essential for sustainable growth, necessitating the development of eco-friendly products and practices. Furthermore, continuous innovation and investment in research and development are necessary to stay ahead of global competition and meet evolving market demands. In conclusion, Asia Pacific's strong economic growth, favorable manufacturing environment, and increasing demand from key industries cement its leading position in the organosilicon polymers market. However, addressing challenges related to raw materials, environmental sustainability, and technological advancement will be crucial for sustaining this leadership.

COVID-19 Impact Analysis on the Global Organosilicon Polymers Market.

The COVID-19 pandemic had a profound impact on the Global Organosilicon Polymers Market, disrupting supply chains and causing fluctuations in demand across various industries. During the initial stages of the pandemic, manufacturing slowdowns and restrictions led to a temporary decline in production and supply of organosilicon polymers. The Automotive and construction sectors, key consumers of these polymers, experienced significant downturns due to halted projects and reduced consumer spending. However, the market demonstrated resilience as the healthcare and electronics industries ramped up demand for organosilicon polymers. The healthcare sector required these materials for medical devices, protective equipment, and biocompatible applications, while the surge in remote work and digitalization spurred demand in electronics for reliable and high-performance components. As industries adapted to the new normal, investments in research and innovation also increased, exploring new uses for organosilicon polymers in emerging technologies and sustainable applications. Despite initial challenges, the market rebounded with a stronger focus on resilience and adaptability, paving the way for future growth. The pandemic underscored the importance of diversifying supply chains and enhancing production capabilities, ensuring that the organosilicon polymers market remains robust and responsive to global disruptions.

Latest trends / Developments:

The Global Organosilicon Polymers Market is witnessing several notable trends and developments driven by technological advancements and evolving industry demands. A key trend is the increasing focus on sustainability and eco-friendly materials, with manufacturers developing bio-based organosilicon polymers to reduce environmental impact. Innovations in nanotechnology are enhancing the performance characteristics of these polymers, making them more versatile for high-tech applications. The automotive industry continues to drive demand, with organosilicon polymers being crucial in developing lightweight, durable, and energy-efficient components, particularly for electric vehicles. In the electronics sector, the push for miniaturization and enhanced performance in devices is boosting the use of organosilicon polymers for their superior dielectric properties and thermal stability. The healthcare industry is also a significant driver, with ongoing research into biocompatible and flexible materials for medical devices and implants. Additionally, smart materials and coatings are emerging, incorporating organosilicon polymers to provide self-healing, anti-corrosive, and anti-fouling properties. Increased investments in R&D are leading to the discovery of new applications and the improvement of existing formulations, ensuring the market's continuous evolution. Overall, these trends indicate a robust growth trajectory for the organosilicon polymers market, marked by innovation and a strong focus on sustainability.

Key Players:

-

Dow Corning Corporation

-

Wacker Chemie AG

-

Shin-Etsu Chemical Co., Ltd.

-

Momentive Performance Materials Inc.

-

Elkem ASA

-

Evonik Industries AG

-

KCC Corporation

-

Gelest, Inc.

-

Innospec Inc.

-

Silchem Inc.