Oncolytic Virus Diagnostics Market Size (2024 – 2030)

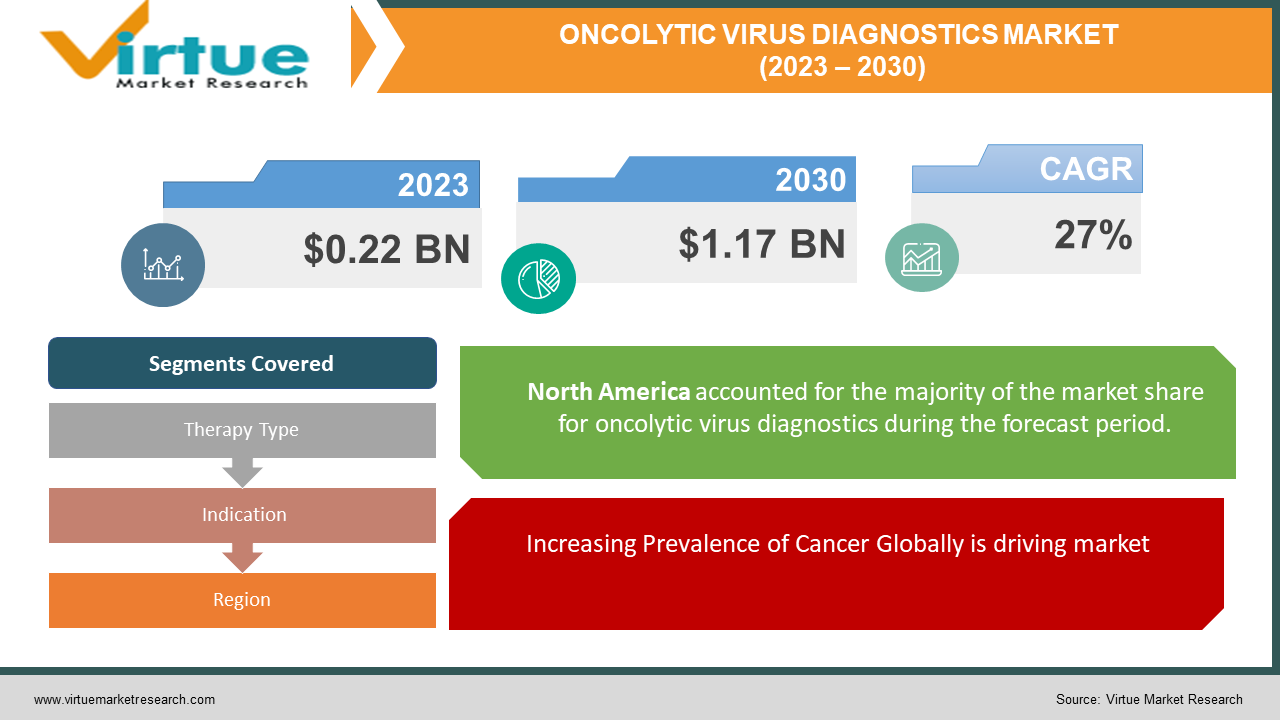

The Global Oncolytic Virus Diagnostics Market was valued at USD 0.22 billion in 2023 and is projected to reach a market size of USD 1.17 billion by the end of 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 27%.

The Global Oncolytic Virus Diagnostics Market is experiencing notable growth driven by advancements in diagnostic technologies and a growing focus on personalized cancer therapies. With increasing research and development activities, the market is witnessing innovations in oncolytic virus diagnostics, enhancing early detection and monitoring of cancer, thus contributing to more effective treatment strategies. Key players in this market, such as Roche, Thermo Fisher Scientific, and Abbott Laboratories, are at the forefront of developing diagnostic solutions that play a crucial role in the evolving landscape of oncolytic virus-based cancer therapies.

Key Market Insights:

The Global Oncolytic Virus Diagnostics Market is being propelled by several key drivers. Firstly, the rising prevalence of cancer globally has generated a heightened demand for advanced diagnostic tools to detect and monitor various types of cancer. With cancer being a leading cause of mortality worldwide, accurate and early detection is imperative for improving patient outcomes. Secondly, ongoing advancements in viral engineering play a pivotal role in propelling the market forward. Genetic engineering technology has evolved, enhancing the capabilities of oncolytic viruses for creating innovative anticancer strategies.

However, the oncolytic virus diagnostics market faces notable restraints and challenges. One major challenge is the potential side effects associated with therapy, including immune responses that can lead to adverse effects. Additionally, limited access to healthcare in low and middle-income countries serves as a restraint, as the advanced nature of oncolytic virus diagnostics requires sophisticated healthcare facilities and skilled professionals. The shortage of healthcare professionals with expertise in administering oncolytic virus therapy, especially through intratumoral injections, poses another challenge. Moreover, regulatory hurdles and safety concerns impact the market's development and adoption, requiring stringent regulatory approvals to ensure safety and efficacy. In terms of segmentation, the oncolytic virus diagnostics market is categorized based on therapy type, virus type, indication, demography, and end-users. The market is dominated by HSV-based therapy types, genetically engineered virus types, indications related to lung cancer, and the adult demography. Hospitals are the predominant end-users, but specialty clinics are witnessing a rise in market share.

Global Oncolytic Virus Diagnostics Market Drivers:

Increasing Prevalence of Cancer Globally is driving market.

The global rise in cancer incidence serves as a primary driver for the oncolytic virus diagnostics market. With cancer being a leading cause of mortality worldwide, there is an escalating demand for advanced diagnostic tools to detect and monitor various types of cancer. The oncolytic virus diagnostics market is poised to benefit from the imperative need for accurate and early cancer detection to improve patient outcomes.

Advancements in Viral Engineering is fueling market growth.

Ongoing advancements in viral engineering play a pivotal role in propelling the oncolytic virus diagnostics market forward. Genetic engineering technology has evolved, enhancing the capabilities of oncolytic viruses for creating innovative anticancer strategies. The development of tumor-selective oncolytic viruses with efficacy against a spectrum of malignancies showcases the potential of these diagnostic tools in contributing to precision medicine and personalized cancer therapies

Rise in Clinical Trials and Approvals is contributing to market growth.

The increasing prevalence of cancer has led to a surge in clinical trials and approvals of new virus therapies for cancer treatment. Oncolytic viruses, a promising class of cancer therapies, are undergoing extensive clinical testing to determine their effectiveness in treating specific types of cancer. The positive outcomes of these trials and subsequent approvals contribute to the market's growth, providing healthcare professionals with additional diagnostic tools for cancer management.

Personalized Treatment Demand is causing the market to expand.

The growing demand for personalized treatment options is a significant driver for the oncolytic virus diagnostics market. Scientific advancements have paved the way for tailoring oncolytic viruses to target specific genetic alterations in individual patients. This customization enhances the therapeutic success of oncolytic virus therapies. The increasing adoption of personalized medicine, as evidenced by the approval of a significant percentage of personalized medicine therapies by regulatory authorities, further emphasizes the market's potential for addressing individual patient needs.

Global Oncolytic Virus Diagnostics Market Restraints and Challenges:

One of the significant challenges faced by the oncolytic virus diagnostics market is the potential side effects associated with therapy. Oncolytic viruses, while designed to target and destroy tumor cells, may occasionally infect healthy cells, triggering an immune response that can lead to adverse effects. Common side effects, including chills, fatigue, flu-like symptoms, injection site pain, nausea, and fever, pose challenges to the widespread adoption of oncolytic virus diagnostics.

Access to healthcare infrastructure in low and middle-income countries serves as a restraint for the oncolytic virus diagnostics market. The advanced nature of oncolytic virus diagnostics requires sophisticated healthcare facilities and skilled professionals for effective implementation. The lack of infrastructure and resources in certain regions hinders the widespread adoption of oncolytic virus diagnostics, limiting its accessibility to a broader patient population.

Administering oncolytic virus therapy, particularly through intratumoral injections, requires specialized skills. The shortage of healthcare professionals with the expertise to perform these intricate procedures poses a challenge. Ordinary nurses may find it challenging to administer intratumoral injections, limiting the scalability of oncolytic virus diagnostics in clinical settings. This lack of trained professionals creates a bottleneck in the seamless delivery of oncolytic virus therapy.

The oncolytic virus diagnostics market faces regulatory hurdles and safety concerns that impact its development and adoption. Ensuring the safety and efficacy of oncolytic viruses is a critical aspect that requires stringent regulatory approvals. Addressing safety concerns related to potential viral contamination of healthy cells and the overall immune response remains a complex challenge. Meeting regulatory requirements and demonstrating the long-term safety profile of oncolytic virus diagnostics are essential hurdles to overcome for market growth.

ONCOLYTIC VIRUS DIAGNOSTICS MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

27% |

|

Segments Covered

|

By Therapy Type, Indication, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Amgen Inc., Shanghai Sunway Biotech Co. Ltd., Oncolys BioPharma Inc., TILT Biotherapeutics Ltd., Oncorus Inc., TAKARA BIO INC., Vyriad, Transgene SA, Lokon Pharma AB, Pfizer Inc.

|

Oncolytic Virus Diagnostics Market Segmentation: By Therapy Type

-

HSV-based

-

Adenovirus-based

-

Reovirus

-

Poxviruses

-

NDV

-

Others

The HSV-based therapy type dominates the majority market share, holding a substantial portion of the oncolytic virus diagnostics market. This can be attributed to the extensive clinical trials related to HSV-based viruses, particularly HSV Type 1 (HSV-1), which has been widely investigated in cancer oncolytic viral therapy. The familiarity with HSV-1, coupled with its genomic manipulation, cytotoxicity, pathogenicity, and the availability of antiviral drugs, has contributed to its significant market share.

The Adenovirus-based therapy type is witnessing a notable rise in market share. Ongoing research and clinical trials related to Adenovirus-based oncolytic viruses are contributing to the increasing adoption of this therapy type. Adenovirus-based therapies are gaining attention for their potential efficacy in treating various cancer types, and advancements in genetic engineering are further propelling the growth of this segment.

Genetically Engineered oncolytic viruses hold the majority market share. The ability to tailor oncolytic viruses to specific genetic alterations, enhancing therapeutic success, has fueled the demand for genetically engineered virus types. The precision offered by these viruses in targeting cancer cells while minimizing damage to healthy cells has contributed significantly to their dominant market share.

The Oncolytic Wild virus type is experiencing a surge in market share. Research and development efforts focused on harnessing the natural oncolytic properties of wild viruses for cancer therapy are gaining traction. The potential of oncolytic wild viruses in providing alternative treatment options with fewer genetic modifications is contributing to the growing interest in this segment.

Oncolytic Virus Diagnostics Market Segmentation: By Indication

-

Head & Neck

-

Lung

-

Kidney

-

Liver

-

Pancreatic

-

Breast

-

Colorectal

-

Sarcoma

-

Melanoma

The market is largely dominated by indications related to Lung cancer, holding a significant share. The rising incidence of lung cancer globally and the continuous advancements in diagnostic technologies for lung cancer contribute to the prominence of this indication in the market.

The Pancreatic indication segment is witnessing a notable increase in market share. Advancements in understanding pancreatic cancer and the demand for effective diagnostic solutions for early detection are driving the growth of this segment. Ongoing research and clinical developments are further boosting the market share of pancreatic indications.

The Adult demography segment commands the majority market share. The higher prevalence of cancer in the adult population, coupled with the increasing awareness and adoption of oncolytic virus diagnostics in adult patients, contributes to the dominance of this demographic segment.

The Pediatric demography segment is showing a rising trend in market share. Ongoing research and the focus on developing oncolytic virus diagnostics specifically tailored for pediatric patients are driving the increased adoption of these diagnostics in pediatric oncology.

Hospitals are the predominant end-users, holding the majority market share. Hospitals serve as primary centers for cancer diagnosis and treatment, making them key stakeholders in the adoption of oncolytic virus diagnostics.

Specialty Clinics are witnessing a rise in market share. The increasing establishment of specialty clinics dedicated to cancer care and the integration of oncolytic virus diagnostics into specialized treatment settings contribute to the growing market share of this segment.

Oncolytic Virus Diagnostics Market Segmentation: Regional Analysis

-

North America

-

Asia-Pacific

-

Europe

-

South America

-

Middle East and Africa

North America leads in market share, holding a substantial portion of the global oncolytic virus diagnostics market. With the market share of 45%, the presence of advanced healthcare infrastructure, ongoing research activities, and high cancer incidence rates contribute to the dominance of this geographical segment.

The Asia-Pacific region is experiencing a notable rise in market share. Increasing investments in healthcare infrastructure, rising awareness about advanced diagnostics, and a growing patient population contribute to the expanding market share in the Asia-Pacific region.

COVID-19 Impact Analysis on the Global Oncolytic Virus Diagnostics Market:

The COVID-19 pandemic has significantly impacted the Global Oncolytic Virus Diagnostics Market, introducing both challenges and opportunities. The outbreak has led to disruptions in the healthcare sector, affecting the dynamics of cancer diagnostics and treatment. During the initial phases of the pandemic, there was a notable decline in routine cancer screenings and diagnostics due to healthcare resource reallocation and patient reluctance to seek medical attention for non-COVID-19-related issues. The oncolytic virus diagnostics market experienced delays in clinical trials, hindering the progress of research and development activities. Additionally, supply chain disruptions and logistical challenges impeded the manufacturing and distribution of diagnostic technologies. The overall uncertainty and economic constraints during the pandemic led to a temporary slowdown in market growth.

However, the pandemic has also underscored the importance of advanced diagnostic technologies, including oncolytic virus diagnostics, in addressing healthcare challenges. The heightened focus on public health and the urgency to enhance diagnostic capabilities for critical illnesses like cancer have accelerated innovations in the oncolytic virus diagnostics market. The increased adoption of telemedicine and remote patient monitoring during the pandemic has further emphasized the need for efficient diagnostic tools that can be integrated into evolving healthcare delivery models. As the global healthcare system adapts to the post-pandemic landscape, the oncolytic virus diagnostics market is poised to recover and exhibit resilience. The heightened awareness of the importance of early cancer detection, coupled with ongoing technological advancements, is expected to drive the market's resurgence. The integration of oncolytic virus diagnostics into comprehensive cancer care strategies will likely play a crucial role in mitigating the long-term impact of the pandemic on cancer diagnostics and treatment.

Latest Trends/ Developments:

The Global Oncolytic Virus Diagnostics Market is witnessing a dynamic landscape marked by several latest trends and developments that are shaping the future of cancer diagnostics and treatment. One prominent trend is the increasing focus on precision medicine, driving the customization of oncolytic viruses to target specific genetic alterations in individual patients. This trend aligns with the broader shift towards personalized treatment strategies, optimizing therapeutic success and minimizing adverse effects. Another noteworthy development is the growing emphasis on immunotherapy, with oncolytic virus diagnostics playing a pivotal role in enhancing the efficacy of immunotherapeutic interventions. The synergy between oncolytic viruses and immunotherapy is opening new avenues for comprehensive cancer treatment approaches. Researchers and pharmaceutical companies are exploring innovative combinations of oncolytic viruses with immunotherapeutic agents to maximize treatment outcomes.

Advancements in viral engineering technologies are fostering the creation of novel oncolytic viruses with enhanced capabilities. Genetic engineering breakthroughs are allowing for the development of more potent and targeted oncolytic viruses, expanding their applicability across a broader spectrum of cancer types. These developments underscore the continual evolution of oncolytic virus diagnostics towards more sophisticated and effective diagnostic and therapeutic solutions. The integration of artificial intelligence (AI) and machine learning (ML) in oncolytic virus diagnostics is a trend gaining momentum. AI and ML algorithms are being employed to analyze complex datasets, facilitating quicker and more accurate interpretation of diagnostic results. This trend not only streamlines the diagnostic process but also contributes to the identification of patterns and correlations that may lead to more informed treatment decisions.

Geographically, there is a rising trend in the adoption of oncolytic virus diagnostics in the Asia-Pacific region. Increasing investments in healthcare infrastructure, a growing awareness of advanced diagnostic technologies, and a rising burden of cancer cases are driving the expansion of the market in this region. The Asia-Pacific region is becoming a focal point for research, development, and market penetration of oncolytic virus diagnostics. Furthermore, collaborative efforts between pharmaceutical companies and research institutions are fostering innovation in the field. Partnerships and strategic collaborations are facilitating the pooling of resources, expertise, and technologies, expediting the development of cutting-edge oncolytic virus diagnostics.

Key Players:

-

Amgen Inc.

-

Shanghai Sunway Biotech Co. Ltd.

-

Oncolys BioPharma Inc.

-

TILT Biotherapeutics Ltd.

-

Oncorus Inc.

-

TAKARA BIO INC.

-

Vyriad

-

Transgene SA

-

Lokon Pharma AB

-

Pfizer Inc.

- In February, 2023, a Phase I/II trial for the first mRNA-based shingles vaccine programme has been initiated by Pfizer Inc. and BioNTech SE.

- In October, 2023, Amgen has acquired Horizon Therapeutics in a deal valued at $27.8bn following approval from the US Federal Trade Commission.