Nuclear Pressure Transmitter Market Size (2024 – 2030)

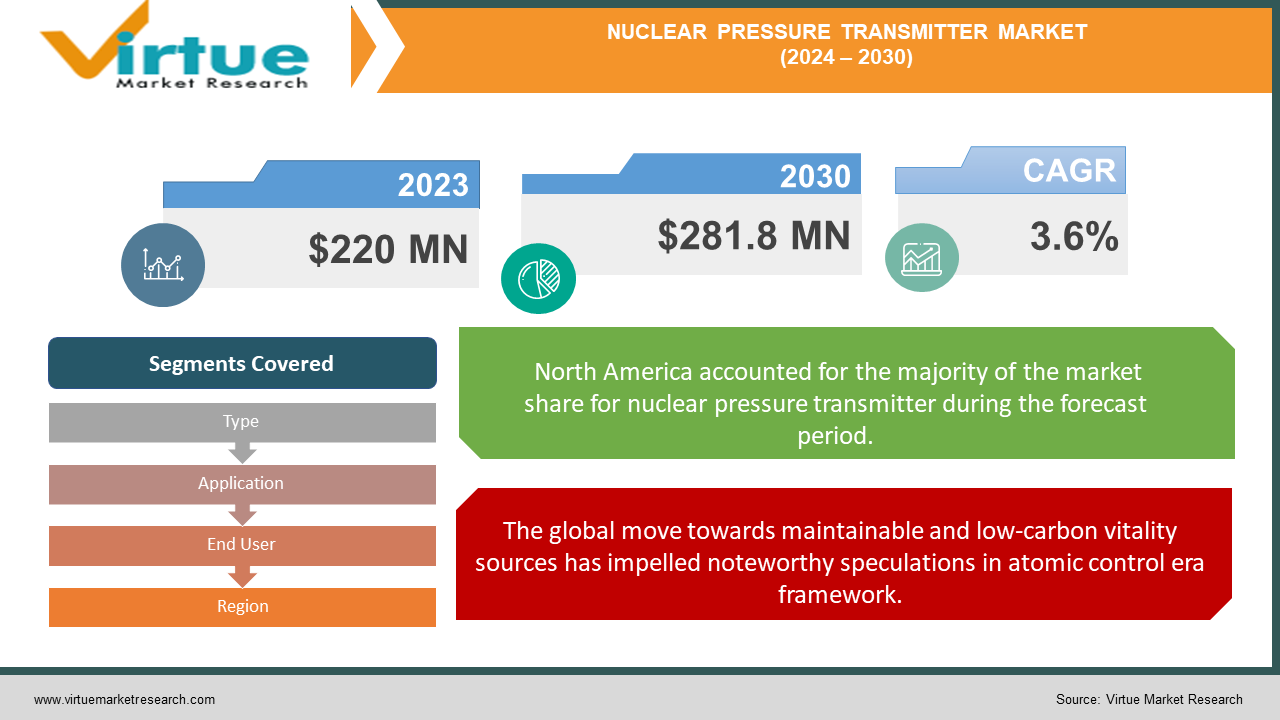

The Global Nuclear Pressure Transmitter Market was valued at USD 220 million and is projected to reach a market size of USD 281.8 million by the end of 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 3.6%.

The global nuclear pressure transmitter market is characterized by its significant part in guaranteeing secure and productive operations inside atomic control plants around the world. These transmitters are outlined to precisely degree and screen weight levels in atomic reactors, basic for keeping up operational security and optimizing execution. As concerns over vitality security and natural supportability develop, atomic control remains a critical component of numerous countries' vitality portfolios, driving the request for solid instrumented like weight transmitters.

Key Market Insights:

Countries in Asia-Pacific, particularly China and India, are seeing a rapid expansion in nuclear power generation capacities, boosting the demand for nuclear pressure transmitters in these regions.

MEMS-based pressure transmitters are gaining traction, accounting for around 30% of the market share in terms of technology adoption.

New technologies such as MEMS (Micro-Electro-Mechanical Systems) are being integrated into nuclear pressure transmitters, enhancing accuracy and reliability.

Stringent regulatory standards regarding safety and operational reliability in nuclear facilities are driving the adoption of high-performance pressure transmitters.

The adoption of SIL (Safety Integrity Level) certified pressure transmitters is increasing, ensuring compliance with stringent safety standards in nuclear operations.

Nuclear Pressure Transmitter Market Drivers:

The global move towards maintainable and low-carbon vitality sources has impelled noteworthy speculations in atomic control era framework.

Nations pointing to decrease their reliance on fossil fills and relieve nursery gas outflows are progressively turning to atomic vitality as a practical elective. This slant is especially articulated in developing economies over Asia-Pacific and Eastern Europe, where quick industrialization and urbanization are driving the require for dependable and persistent control supply. Atomic weight transmitters are necessarily to the proficient operation of atomic reactors, encouraging precise observing and control of weight varieties in basic forms. As governments and private division substances proceed to contribute in growing atomic control capacity, the request for progressed weight transmitter arrangements competent of improving operational proficiency and security will witness vigorous development.

The evolution of sensor technology and digitalization has revolutionized the nuclear instrumentation landscape, offering enhanced capabilities in data accuracy, real-time monitoring, and predictive maintenance.

Modern nuclear pressure transmitters leverage cutting-edge sensor technologies, such as silicon strain gauges and piezoelectric sensors, to deliver precise measurements under extreme operating conditions. Furthermore, the integration of digital communication protocols, such as HART (Highway Addressable Remote Transducer) and Foundation Fieldbus, enables seamless connectivity with control systems and supervisory platforms, facilitating remote monitoring and diagnostics. These technological advancements not only enhance the reliability and performance of nuclear pressure transmitters but also enable proactive maintenance strategies, thereby reducing downtime and operational costs for nuclear power plant operators. As the nuclear industry continues to embrace digital transformation, the demand for smart and interconnected pressure transmitter solutions is poised to expand, driving market growth globally.

The Global Nuclear Pressure Transmitter Market is propelled by stringent safety regulations governing nuclear facilities worldwide.

In the aftermath of historical nuclear incidents, such as Fukushima and Chernobyl, regulatory bodies have enforced rigorous safety standards. Nuclear pressure transmitters play a pivotal role in ensuring the safe operation of nuclear reactors by continuously monitoring and transmitting critical pressure data. These devices are designed to withstand extreme environmental conditions and provide accurate pressure readings, thereby enhancing operational safety and reliability in nuclear power plants. As governments and regulatory authorities prioritize nuclear safety, the demand for advanced pressure transmitter technologies is expected to grow steadily across global nuclear installations.

Nuclear Pressure Transmitter Market Challenges:

The nuclear industry operates under stringent regulatory frameworks globally, imposing rigorous standards and safety requirements.

Nuclear pressure transmitters, essential for monitoring and controlling pressure within nuclear reactors and associated systems, must comply with these stringent regulations. Any deviation or non-compliance can lead to regulatory sanctions, delays in project timelines, and increased costs. Manufacturers and operators in the nuclear pressure transmitter market are compelled to invest heavily in research and development to ensure their products meet or exceed these demanding regulatory standards. This regulatory environment not only increases operational costs but also extends product development cycles, thereby posing a significant challenge to market players aiming for timely product launches and market penetration.

The nuclear industry demands substantial initial investments due to the complexity and high standards of safety required.

Nuclear pressure transmitters, being critical components in ensuring the safe and efficient operation of nuclear plants, are subject to these high capital expenditures. The upfront costs associated with designing, manufacturing, and installing nuclear-grade pressure transmitters are considerable, often deterring potential investors and operators from entering the market. Moreover, the long payback period further complicates financial viability, as returns on investment may take decades to materialize. This financial burden restricts market growth, especially in regions or countries with limited financial resources or political uncertainties regarding nuclear energy.

Nuclear Pressure Transmitter Market Opportunities:

In the domain of nuclear energy, the Global Nuclear Pressure Transmitter Market stands as a vital component, advertising unparalleled exactness and unwavering quality in measuring weights inside atomic control plants. As the world gravitates towards cleaner vitality arrangements, the request for atomic control proceeds to develop, cultivating a burgeoning advertise for specialized instrumented like weight transmitters.

These gadgets play a urgent part in guaranteeing operational security and effectiveness, accurately observing and controlling weight levels basic to the operation of atomic reactors. With rigid administrative prerequisites overseeing atomic offices around the world, the require for progressed weight checking innovations gets to be ever more articulated. Additionally, innovative headways in weight transmitter plan are enhancing their versatility to resist extraordinary conditions predominant in atomic situations. Advancements such as upgraded strength, radiation resistance, and inaccessible checking capabilities are reshaping the scene, advertising administrator’s uncommon control and situational mindfulness.

NUCLEAR PRESSURE TRANSMITTER MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

3.6% |

|

Segments Covered

|

By Type, Application, End User, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Emerson Electric Co., ABB Ltd., Yokogawa Electric Corporation, Siemens AG, Honeywell International Inc., Schneider Electric SE, Endress+Hauser AG, General Electric Company, WIKA Alexander Wiegand SE & Co. KG, Vega Grieshaber KG, Fuji Electric Co., Ltd., KROHNE Messtechnik GmbH, Yokogawa Electric Corporation, Azbil Corporation, Danfoss A/S

|

Nuclear Pressure Transmitter Market Segmentation: By Type

The highest market share within the Global Nuclear Pressure Transmitter Market has a place to Analog Weight Transmitters, eminent for their unwavering quality and vigorous execution in atomic settings. These transmitters have long ruled the advertise due to their demonstrated innovation and compatibility with existing atomic control framework. In any case, the fastest-growing section is Computerized Weight Transmitters, driven by headways in sensor innovation and expanding request for improved precision and real-time observing capabilities in atomic offices around the world. This move underscores a broader industry slant towards digitalization and more brilliant instrumented arrangements, pointed at optimizing operational effectiveness and assembly rigid security benchmarks in atomic control operations. As advanced advances proceed to advance, Computerized Weight Transmitters are anticipated to progressively enter the showcase, complementing and inevitably challenging the built up dominance of Analog Weight Transmitters within the atomic weight detecting segment.

Nuclear Pressure Transmitter Market Segmentation: By Application

-

Steam Generator System

-

Pressurizer System

-

Containment System

-

Others

The highest and fastest-growing segment within the Global Nuclear Pressure Transmitter Market is the Reactor Coolant Framework, basic for keeping up ideal center temperature and operational steadiness in atomic control plants. This section not as it were commands a critical showcase share but too appears steady development driven by expanding requests for dependable atomic vitality arrangements around the world. Nearby, the Steam Generator Framework fragment plays a vital part in proficient steam generation, reflecting its crucial commitment to control era proficiency and security conventions inside atomic offices.

In a broader setting, much like how different showcase portions in atomic innovation back basic operations, businesses nowadays too use different techniques and advances to upgrade their competitive edge. Fair as atomic weight transmitters guarantee steadiness, companies innovate over divisions to preserve their advertise positions and drive development.

Nuclear Pressure Transmitter Market Segmentation: By End User

-

Nuclear Power Plants

-

Research Reactors

The highest segment within the Global Nuclear Pressure Transmitter Market is ruled by Atomic Control Plants, which command a noteworthy share due to rigid security guidelines requiring exact weight checking all through operational stages. This portion holds around 75% of the showcase, reflecting its basic part in guaranteeing the secure and effective operation of atomic offices around the world. Concurrently, Inquire about Reactors rise as the fastest-growing section, driven by growing investigate activities in atomic science and innovation. With an yearly development rate of 8%, this fragment underscores the expanding appropriation of progressed weight transmitter innovations custom fitted to the specialized needs of investigate situations. Together, these fragments outline the urgent part of atomic weight transmitters in keeping up operational judgment and security over differing applications inside the atomic vitality division.

Nuclear Pressure Transmitter Market Segmentation: By Region

The highest market share and fastest-growing segment in the global nuclear pressure transmitter market can be found in North America. Here, stringent safety regulations and extensive nuclear power infrastructure in countries such as the United States and Canada drive substantial demand. This region leads in adopting advanced pressure monitoring solutions, particularly for reactor pressure vessel monitoring and safety systems, reflecting a robust market presence. Meanwhile, Asia-Pacific emerges as another pivotal region, fueled by rapid industrialization and significant energy demands in nations like China, India, and South Korea. The region witnesses accelerated growth in nuclear power capacity additions, particularly in new reactor construction projects and upgrades to existing facilities. Europe follows closely, maintaining a strong position with investments in nuclear energy and stringent safety standards across countries like France, Germany, and the UK. These efforts emphasize the adoption of advanced pressure monitoring technologies to enhance operational efficiency and safety in nuclear facilities.

COVID-19 Impact Analysis on the Global Nuclear Pressure Transmitter Market:

The COVID-19 pandemic significantly impacted the Global Nuclear Pressure Transmitter Market, introducing both challenges and opportunities across the sector. As the pandemic unfolded, stringent lockdowns and travel restrictions disrupted supply chains, leading to delays in production and shipment of nuclear pressure transmitters. The initial phase saw a notable decline in demand as nuclear projects faced postponements and budget constraints amidst economic uncertainties. However, the crisis also spurred innovation in remote monitoring and diagnostics technologies, driving the adoption of advanced digital solutions to ensure operational continuity and safety in nuclear facilities. Moreover, heightened focus on maintaining nuclear plant reliability amidst workforce limitations emphasized the importance of robust, reliable pressure measurement systems, thereby boosting the market for high-precision and durable pressure transmitters. The shift towards renewable energy sources amidst global recovery efforts further underscored the importance of nuclear power as a stable and low-carbon electricity generation option, thereby sustaining long-term investment prospects for nuclear pressure transmitter technologies. Looking ahead, as the industry adapts to the post-pandemic landscape with renewed emphasis on resilience and sustainability, collaborations between key stakeholders and advancements in digitalization are expected to play pivotal roles in shaping the future growth trajectory of the global nuclear pressure transmitter market.

Latest Trends/ Developments:

One of the noticeable patterns forming the showcase is the integration of progressed sensor innovations, upgrading exactness and unwavering quality in atomic control plants. These sensors are progressively being prepared with advanced communication capabilities, encouraging consistent integration into advanced control frameworks and empowering real-time checking and information analytics. Another vital advancement is the accentuation on upgrading the toughness and strength of weight transmitters to resist cruel atomic situations, subsequently dragging out operational life expectancies and decreasing upkeep costs. Additionally, there has been a striking move towards the selection of savvy weight transmitters that offer prescient upkeep highlights, leveraging information analytics and machine learning calculations to expect potential disappointments and optimize plant productivity.

Besides, administrative systems emphasizing atomic security measures proceed to drive advancement in weight transmitter plan, guaranteeing compliance with exacting rules and cultivating believe among stakeholders. The showcase is additionally seeing a developing request for remote weight transmitters, empowering adaptability in establishment and lessening cabling complexities inside atomic offices. Topographically, districts contributing in atomic vitality extension, such as Asia-Pacific and Europe, are developing as key development markets, driven by expanding vitality requests and the modernization of existing atomic framework. In general, the worldwide atomic weight transmitter advertise is balanced for proceeded advancement, impelled by innovative developments and a immovable commitment to upgrading operational effectiveness and security in atomic control era.

Key Players:

-

Emerson Electric Co.

-

ABB Ltd.

-

Yokogawa Electric Corporation

-

Siemens AG

-

Honeywell International Inc.

-

Schneider Electric SE

-

Endress+Hauser AG

-

General Electric Company

-

WIKA Alexander Wiegand SE & Co. KG

-

Vega Grieshaber KG

-

Fuji Electric Co., Ltd.

-

KROHNE Messtechnik GmbH

-

Yokogawa Electric Corporation

-

Azbil Corporation

-

Danfoss A/S