Nuclear Fuel Recycling Market Size (2024 – 2030)

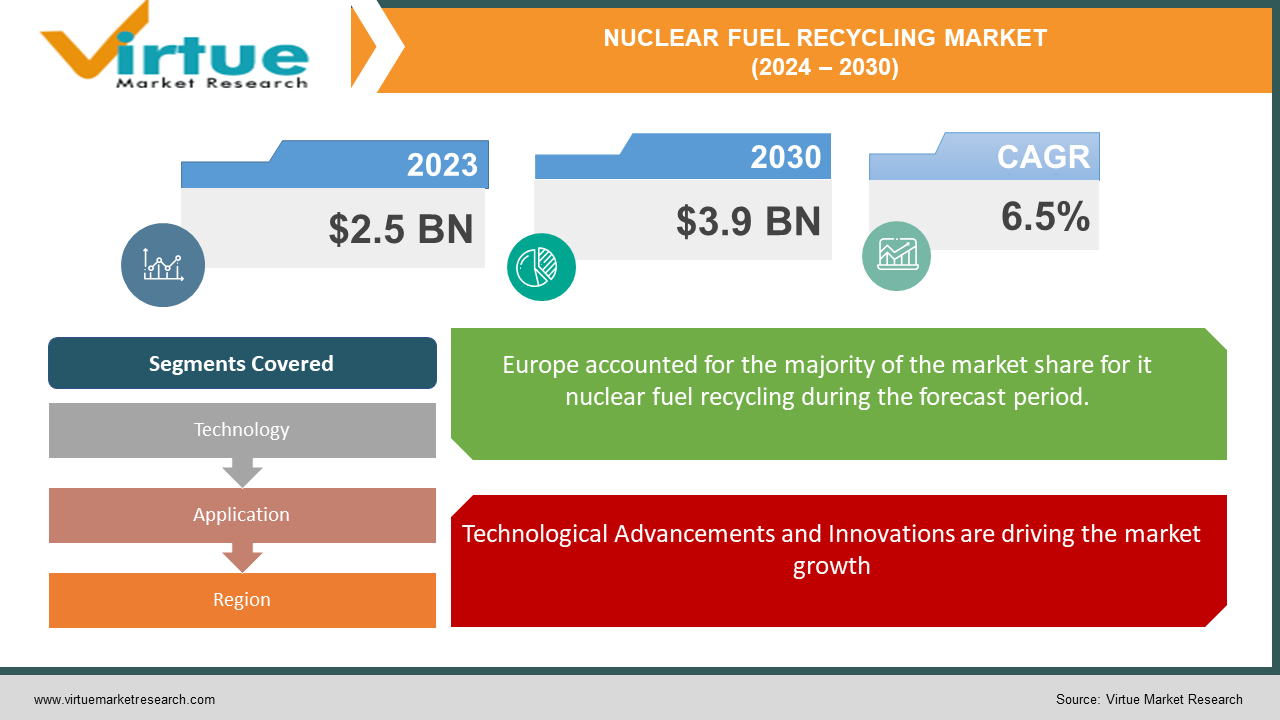

The Global Nuclear Fuel Recycling Market was valued at USD 2.5 billion in 2023 and is projected to grow at a CAGR of 6.5% from 2024 to 2030. The market is expected to reach USD 3.9 billion by 2030.

Nuclear fuel recycling involves the reprocessing of spent nuclear fuel to extract valuable materials such as uranium and plutonium, which can be reused in reactors. This process reduces the volume of high-level radioactive waste and enhances the sustainability of nuclear energy by optimizing the use of nuclear fuel resources.

Key Market Insights:

The increasing demand for sustainable and low-carbon energy sources is driving the growth of the nuclear fuel recycling market.

Technological advancements and innovations in reprocessing techniques are boosting the adoption of nuclear fuel recycling.

Rising concerns about nuclear waste management and the need for efficient disposal solutions are propelling the demand for nuclear fuel recycling.

The growth of nuclear energy programs, especially in emerging economies, is fueling the market for nuclear fuel recycling.

Government initiatives and policies supporting nuclear fuel recycling and waste management are creating opportunities for market expansion.

Global Nuclear Fuel Recycling Market Drivers:

Increasing Demand for Sustainable and Low-Carbon Energy Sources is driving the market growth

The growing global demand for sustainable and low-carbon energy sources is a significant driver for the nuclear fuel recycling market. Nuclear energy is considered a viable option to meet the increasing energy needs while reducing greenhouse gas emissions. Unlike fossil fuels, nuclear power generates electricity with minimal carbon emissions, making it a crucial component of the clean energy transition. According to the International Energy Agency (IEA), nuclear power accounted for approximately 10% of the world's electricity production in 2023. However, the challenge of managing spent nuclear fuel and high-level radioactive waste has been a major concern for the nuclear industry. Nuclear fuel recycling addresses this issue by recovering valuable materials from spent fuel, which can be reused in reactors, thereby reducing the volume of radioactive waste. This not only enhances the sustainability of nuclear energy but also optimizes the use of nuclear fuel resources. As countries strive to achieve their climate goals and reduce reliance on fossil fuels, the demand for nuclear fuel recycling is expected to increase, driving market growth.

Technological Advancements and Innovations are driving the market growth

Technological advancements and innovations in reprocessing techniques are key drivers of the nuclear fuel recycling market. The development of advanced reprocessing technologies, such as the PUREX (Plutonium Uranium Redox Extraction) process and the UREX (Uranium Extraction) process, has significantly improved the efficiency and safety of nuclear fuel recycling. These technologies enable the separation of valuable fissile materials from spent nuclear fuel, which can be reused in new fuel assemblies. Additionally, research and development efforts are focused on developing next-generation reprocessing technologies that minimize waste generation and enhance resource utilization. For instance, pyroprocessing, a high-temperature electrochemical process, is being explored as an alternative to conventional aqueous reprocessing methods. Pyroprocessing offers several advantages, including the ability to handle a wide range of fuel types, reduced waste volume, and improved proliferation resistance. Moreover, advancements in materials science and nuclear engineering are contributing to the development of more efficient and cost-effective reprocessing equipment and facilities. These technological innovations are expected to drive the adoption of nuclear fuel recycling, enhancing the sustainability and economics of nuclear energy.

Rising Concerns About Nuclear Waste Management are driving market growth

Rising concerns about nuclear waste management and the need for efficient disposal solutions are driving the demand for nuclear fuel recycling. The disposal of high-level radioactive waste, which includes spent nuclear fuel, poses significant environmental, safety, and security challenges. Traditional disposal methods, such as geological repositories, require long-term containment and isolation of radioactive waste, which can be costly and technically complex. Nuclear fuel recycling offers an alternative approach by reducing the volume and radiotoxicity of high-level waste through the recovery of reusable materials. This not only mitigates the environmental impact of nuclear waste but also reduces the burden on disposal facilities. Furthermore, nuclear fuel recycling can contribute to non-proliferation efforts by reducing the stockpile of separated plutonium and minimizing the risk of nuclear proliferation. As countries seek sustainable and secure solutions for nuclear waste management, the demand for nuclear fuel recycling is expected to grow. Governments and regulatory bodies are also supporting the development and deployment of recycling technologies through policies and funding initiatives, further driving market growth.

Global Nuclear Fuel Recycling Market Challenges and Restraints:

High Costs and Economic Viability are restricting the market growth

One of the significant challenges faced by the nuclear fuel recycling market is the high costs associated with reprocessing and recycling spent nuclear fuel. The construction, operation, and maintenance of reprocessing facilities require substantial capital investments. Additionally, the complexity of the reprocessing process, which involves handling highly radioactive materials and maintaining stringent safety standards, adds to the operational costs. The economic viability of nuclear fuel recycling is further impacted by fluctuating prices of natural uranium, which can affect the competitiveness of recycled fuel. While technological advancements and economies of scale have the potential to reduce costs, the initial investment and ongoing expenses remain significant barriers for many countries and nuclear operators. To address this challenge, governments and industry stakeholders are exploring innovative financing models, public-private partnerships, and international collaborations to share the financial burden and enhance the economic feasibility of nuclear fuel recycling. Additionally, continued research and development efforts aimed at improving process efficiency and reducing costs are essential to overcome this challenge and drive market growth.

Regulatory and Policy Challenges are restricting the market growth

Regulatory and policy challenges pose significant restraints to the nuclear fuel recycling market. The reprocessing and recycling of spent nuclear fuel are subject to stringent regulatory frameworks and oversight to ensure safety, security, and environmental protection. Compliance with these regulations requires extensive documentation, licensing, and inspections, which can be time-consuming and costly. Additionally, variations in regulatory standards and policies across different countries can create complexities and uncertainties for market participants. For instance, while some countries have established comprehensive frameworks for nuclear fuel recycling, others may have restrictive policies or lack clear guidelines, limiting market opportunities. Moreover, public perception and acceptance of nuclear energy and recycling technologies can influence regulatory decisions and policy development. Addressing these regulatory and policy challenges requires proactive engagement with regulators, policymakers, and stakeholders to promote a clear and consistent regulatory environment. International cooperation and harmonization of standards can also facilitate the adoption of nuclear fuel recycling technologies and support market growth.

Market Opportunities:

The Nuclear Fuel Recycling Market presents numerous opportunities for growth and innovation. One significant opportunity lies in the development of advanced recycling technologies that enhance efficiency, safety, and sustainability. Companies can leverage advancements in materials science, nuclear engineering, and process automation to create innovative reprocessing methods that minimize waste generation, reduce costs, and improve resource utilization. For instance, the development of pyroprocessing and other advanced reprocessing techniques can offer more efficient and flexible solutions for recycling a wide range of nuclear fuels. Additionally, the growing focus on environmental sustainability and circular economy principles presents opportunities for recycling initiatives that align with global climate goals. Governments and regulatory bodies are increasingly supporting sustainable nuclear fuel cycles through funding, policies, and incentives, creating a favorable environment for market growth. Moreover, the expansion of nuclear energy programs in emerging economies, driven by the need for reliable and low-carbon energy sources, offers significant growth potential for the nuclear fuel recycling market. By focusing on technological innovation, sustainability, and market expansion, companies can capitalize on these opportunities and contribute to the advancement of the nuclear fuel recycling industry.

NUCLEAR FUEL RECYCLING MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

6.5% |

|

Segments Covered

|

By Technology, Application, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Areva SA, CAMECO Corporation, Hitachi Zosen Corporation, Japan Nuclear Fuel Limited, Mitsubishi Heavy Industries Ltd., Orano, Rosatom State Atomic Energy Corporation, Toshiba Energy Systems & Solutions Corporation, Urenco Group, Westinghouse Electric Company LLC

|

Nuclear Fuel Recycling Market Segmentation: by Technology

PUREX (Plutonium Uranium Redox Extraction) is currently the most dominant segment in the nuclear fuel reprocessing market. Developed specifically for separating plutonium and uranium from spent nuclear fuel, PUREX has been the industry standard for decades. Its established technology, proven track record, and ability to recover valuable fissile materials contribute to its dominance

Nuclear Fuel Recycling Market Segmentation: by Application

-

Commercial Reactors

-

Research Reactors

-

Naval Reactors

-

Others

Commercial Reactors are the most dominant segment in the nuclear reactor landscape. These reactors are the workhorses of the industry, responsible for generating electricity for millions of homes and businesses around the world. They typically operate at high power outputs for extended periods, producing a significant portion of a country's electrical needs. Research reactors and naval reactors, while crucial for specific purposes, play much smaller roles. Research reactors are used for scientific experiments and medical isotope production, often operating at lower power levels. Naval reactors power warships, requiring unique designs for compactness, maneuverability, and long lifespans between refuelings.

Nuclear Fuel Recycling Market Segmentation: Regional Analysis

-

North America

-

Asia-Pacific

-

Europe

-

South America

-

Middle East and Africa

Europe is the most dominant region in the Nuclear Fuel Recycling Market due to its advanced nuclear infrastructure, strong regulatory framework, and significant investments in nuclear fuel reprocessing and recycling facilities, particularly in countries like France and the United Kingdom. However, factors like stricter regulations and public resistance to nuclear energy are hindering growth

COVID-19 Impact Analysis on the Nuclear Fuel Recycling Market:

The COVID-19 pandemic had a notable impact on the Nuclear Fuel Recycling Market, causing disruptions and challenges across the nuclear energy sector. The pandemic led to temporary shutdowns and reduced operations at nuclear facilities, including reprocessing plants, due to lockdown measures, workforce shortages, and supply chain disruptions. These operational challenges resulted in delays in reprocessing activities and impacted the availability of recycled nuclear fuel. Additionally, the economic uncertainties and budget constraints caused by the pandemic affected funding for nuclear projects and investments in recycling technologies. However, the pandemic also highlighted the importance of energy security and the resilience of nuclear energy as a reliable power source. As countries focused on post-pandemic recovery and infrastructure development, the demand for low-carbon energy sources, including nuclear power, remained strong. The recovery of the nuclear fuel recycling market is expected to be driven by the resumption of nuclear projects, increased government support for sustainable energy solutions, and ongoing investments in advanced recycling technologies. Furthermore, the pandemic underscored the need for efficient and resilient nuclear fuel cycles, creating opportunities for innovation and development in the recycling sector.

Latest Trends/Developments:

The Nuclear Fuel Recycling Market is witnessing several key trends and developments that are shaping its growth and evolution. One notable trend is the increasing focus on advanced reprocessing technologies that enhance efficiency and sustainability. Innovations such as pyroprocessing, which uses high-temperature electrochemical processes, are gaining traction due to their ability to handle a wide range of nuclear fuels and reduce waste volumes. Additionally, there is a growing emphasis on the development of closed nuclear fuel cycles, which aim to maximize the use of nuclear materials and minimize waste generation. Another significant trend is the integration of digital technologies and automation in reprocessing facilities. The use of data analytics, artificial intelligence, and robotics is improving process control, safety, and operational efficiency in recycling plants. Furthermore, there is a rising demand for customized and flexible recycling solutions that can address the specific needs of different reactor types and fuel compositions. The trend towards international collaborations and partnerships is also gaining momentum, with countries and companies working together to share expertise, technology, and resources for nuclear fuel recycling. These trends and developments are expected to drive innovation, enhance the sustainability of nuclear energy, and create new opportunities for growth in the Nuclear Fuel Recycling Market.

Key Players:

-

Areva SA

-

CAMECO Corporation

-

Hitachi Zosen Corporation

-

Japan Nuclear Fuel Limited

-

Mitsubishi Heavy Industries Ltd.

-

Orano

-

Rosatom State Atomic Energy Corporation

-

Toshiba Energy Systems & Solutions Corporation

-

Urenco Group

-

Westinghouse Electric Company LLC