North America Super Engineering Plastics Market Size (2024-2030)

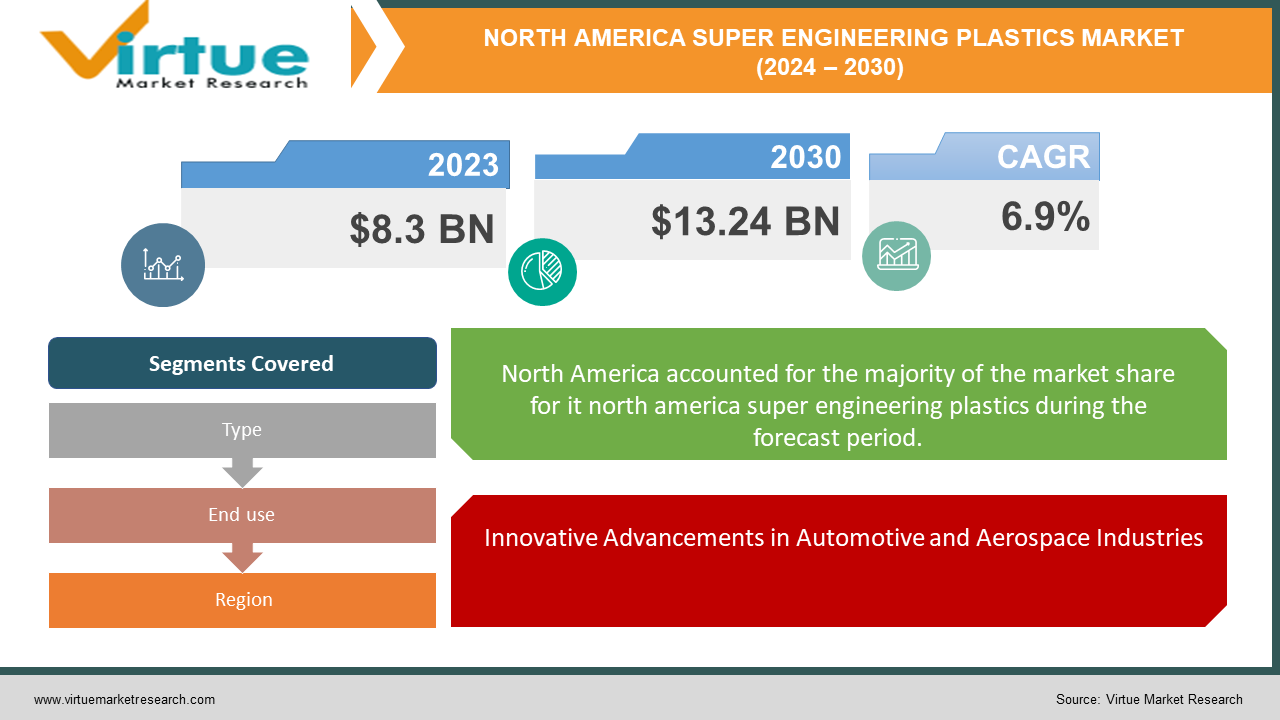

The North America Super Engineering Plastics Market, valued at USD 8.3 billion in 2023, is projected to achieve a market size of USD 13.24 billion by 2030. This growth trajectory anticipates a compound annual growth rate (CAGR) of 6.9% from 2024 to 2030.

The North America Super Engineering Plastics Market is characterized by the request for progressed high-performance materials that display prevalent mechanical properties, warm soundness, and chemical resistance, making them irreplaceable in different high-end applications. These plastics, counting polyphenylene sulfide (PPS), polyetheretherketone (Look), and fluid precious stone polymers (LCP), are looked after in businesses such as car, aviation, hardware, and restorative gadgets due to their capacity to resist cruel conditions and amplify item life expectancies. The region's showcase development is impelled by a strong fabricating segment, progressing mechanical advancements, and an increased center on maintainability and lightweight in item plan. As producers look for materials that offer both tall execution and natural benefits, super building plastics have risen as a key arrangement, tending to the basic requirement for materials that diminish weight without compromising quality or solidness. Besides, North America's well-established foundation and favorable administrative environment back the improvement and selection of these progressed materials. With a drift towards miniaturization in hardware and the expanding complexity of car components, the request for superdesigning plastics is anticipated to witness considerable development. Showcase players are also contributing to inquire about and advancement to upgrade fabric properties and extend application scopes, in this way driving the advertise forward. As businesses proceed to thrust the boundaries of execution and maintainability, the North America Super Designing Plastics Showcase stands balanced for noteworthy development, characterized by development and vital collaborations.

Key Market Insights:

Super engineering plastics like PEEK (Polyether Ether Ketone) and PAEK (Polyaryletherketone) are increasingly used in automotive applications due to their high heat resistance and mechanical strength.

Ongoing advancements in polymer chemistry and manufacturing processes are enhancing the performance characteristics of super engineering plastics.

Within North America, the United States remains a key market for super engineering plastics.

Manufacturers are developing bio-based super engineering plastics to meet growing environmental regulations and consumer demand for sustainable materials.

Canada is experiencing a steady increase in the adoption of super engineering plastics, particularly in industrial machinery and consumer goods sectors.

There's a trend towards miniaturization in various industries, driving the demand for super engineering plastics that can maintain high performance in compact designs.

North America Super Engineering Plastics Market Drivers:

Innovative Advancements in Automotive and Aerospace Industries:

The automotive and aerospace sectors are progressively receiving super designing plastics due to their predominant mechanical properties, lightweight nature, and resistance to tall temperatures. As these businesses endeavor for more prominent fuel productivity and execution, the request for progressed materials like super designing plastics proceeds to rise, driving advertise development.

Developing Request in Electrical and Electronics Applications:

Super engineering plastics are fundamental within the electrical and electronics industry due to their great protection properties and resistance to electrical stretch. With the quick expansion of electronic gadgets, counting smartphones, tablets, and other shopper hardware, the requirement for materials that can withstand high-performance prerequisites and upgrade item life span is moving the showcase forward.

Challenges in the North America Super Engineering Plastics Market:

One of the primary restraints of the North America Super Engineering Plastics Market is the significant production costs associated with these advanced materials.

The complex manufacturing processes, coupled with the need for specialized equipment and high-quality raw materials, drive up expenses. These elevated costs can limit the adoption of super engineering plastics, particularly among smaller companies that might struggle to justify the investment. As a result, market growth may be hampered by the financial barriers to entry and scalability.

The market also faces considerable challenges due to environmental and regulatory pressures.

As global awareness of sustainability and environmental impact increases, stringent regulations governing the use and disposal of plastics are becoming more prevalent. Super engineering plastics, while offering superior performance, often involve chemicals and processes that are subject to rigorous scrutiny. Compliance with these regulations can increase operational costs and complexity for manufacturers. Additionally, the push for greener alternatives and recycling solutions may divert focus and resources away from the development and implementation of super engineering plastics, thereby constraining market expansion.

Opportunities in the North America Super Engineering Plastics Market:

One market opportunity in the North America Super Engineering Plastics Market lies in the burgeoning demand within the electric vehicles (EVs) sector. As the automotive industry pivots towards electrification, the need for lightweight, durable, and high-performance materials has become paramount. Super engineering plastics, with their superior mechanical properties, thermal stability, and resistance to harsh environments, are ideally suited to meet these requirements.

The EV market's rapid growth in North America, driven by increasing consumer awareness, stringent emission regulations, and substantial government incentives, presents a lucrative opportunity for manufacturers of super engineering plastics. By focusing on developing innovative, high-strength plastic components for EV applications, companies can capitalize on this expanding market. This includes parts for battery housings, electric motor components, and charging infrastructure, all of which demand materials that can withstand high temperatures and mechanical stress.

NORTH AMERICA SUPER ENGINEERING PLASTICS MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

6.3%

|

|

Segments Covered

|

By Type, end use, and Region

|

|

Various Analyses Covered

|

Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, USA, Canada, mexico

|

|

Key Companies Profiled

|

DuPont, BASF SE, Solvay S.A., Celanese Corporation, SABIC, Covestro AG, DSM Engineering Plastics, Arkema S.A., Mitsubishi Engineering-Plastics Corporation, Evonik Industries AG, Polyplastics Co., Ltd., Lanxess AG, Toray Industries, Inc., Sumitomo Chemical Co., Ltd., Asahi Kasei Corporation

|

North America Super Engineering Plastics Market Segmentation:

North America Super Engineering Plastics Market Segmentation: By Type

- Polyphenylene Sulfide (PPS)

- Polyether Ether Ketone (PEEK)

- Polyimides (PI)

- Polysulfones (PSU)

- Liquid Crystal Polymers (LCP)

The North America Super Engineering Plastics Market is balanced for vigorous development, with Polyether Ether Ketone (Look) developing as the fastest-growing section, anticipated to grow at a CAGR of 7.5% from 2024 to 2029. This fast development is driven by the expanding request for lightweight, high-performance materials in aviation and restorative applications. On the other hand, Polyphenylene Sulfide (PPS) holds the most noteworthy showcase share, bookkeeping for around 25% in 2023, owing to its remarkable chemical resistance and dimensional steadiness, making it irreplaceable within the car and gadgets divisions. Polyimides (PI) and Polysulfones (PSU) are too noteworthy players, with individual advertise offers of 18% and 15% in 2023, anticipated to develop at CAGRs of 6.0% and 5.8%, fueled by the require for high-temperature and solid materials in different businesses. Fluid Gem Polymers (LCP), with their special combination of mechanical quality and amazing electrical properties, held a 12% showcase share in 2023 and are expected to develop at a CAGR of 6.3%, driven by their application in miniaturized and high-performance electronic components. In general, the showcase exhibits an energetic scene with Look driving in development and PPS in showcase dominance.

North America Super Engineering Plastics Market Segmentation: By End User

- Automotive

- Electrical & Electronics

- Aerospace

- Industrial

- Medical

The North America Super Engineering Plastics Market is seeing critical dynamism, driven by the Restorative segment as the fastest-growing section, bragging a surprising CAGR of 7.2% from 2023 to 2028. This surge is fueled by the heightening request for progressed restorative gadgets and gear that require the special properties of super designing plastics. At the same time, the Car segment holds the biggest advertise share, commanding roughly 30% in 2023, driven by the industry's tireless interest in lightweight, solid, and high-performance materials to upgrade vehicle effectiveness and execution. Other key portions, such as Electrical & Hardware, Aviation, and Mechanical, also contribute considerably to the showcase, developing at CAGRs of 6.8%, 5.9%, and 5.5% individually. These segments use the remarkable capabilities of super designing plastics to meet the exacting prerequisites of their applications, guaranteeing the market's vigorous and supported development in North America.

North America Super Engineering Plastics Market Segmentation: By Region

- United States

- Canada

- Mexico

The highest market share in the North America Super Engineering Plastics market belongs to the United States, where it commands approximately 60% of the regional market. Renowned for its advanced industrial base and substantial investments in research and development, the United States drives the demand for high-performance plastics across diverse sectors such as automotive, aerospace, electronics, and healthcare. Meanwhile, Mexico emerges as the fastest-growing region with a remarkable compound annual growth rate (CAGR) of 7.2% from 2023 to 2028. This rapid expansion is fueled by robust growth in the automotive and electronics industries, bolstered by favorable governmental policies and increasing foreign investments. Canada, while holding a significant market share of 25%, emphasizes sustainable manufacturing practices and benefits from strong trade partnerships with the United States, ensuring steady growth in the adoption of super engineering plastics within its automotive, electronics, and industrial machinery sectors. Collectively, these dynamics underscore a vibrant North American market landscape for super engineering plastics, driven by distinctive growth trajectories across its key regions.

Impact of COVID-19 on the North America Super Engineering Plastics Market:

The COVID-19 pandemic significantly impacted the North America super engineering plastics market, reshaping demand dynamics and supply chains across the region. Initially, as the virus spread and lockdown measures were enforced, industrial activities and manufacturing operations faced unprecedented disruptions, leading to a temporary slowdown in the market. Many end-user industries such as automotive, aerospace, and electronics, which are major consumers of super engineering plastics, experienced a downturn as production facilities shuttered and consumer demand waned. However, amidst these challenges, certain segments like medical devices and packaging materials saw increased demand due to heightened healthcare needs and the surge in online shopping, respectively. As the region gradually navigated through various phases of reopening and recovery, the market witnessed a shift towards resilience and adaptation. Companies accelerated their digital transformation efforts, emphasizing remote work capabilities and digital solutions to maintain operational continuity. Moreover, there was a notable focus on enhancing supply chain robustness and localizing production to mitigate future risks associated with global disruptions. Looking forward, the North America super engineering plastics market is poised for recovery, driven by innovation in product development, sustainable solutions, and renewed investments in critical sectors. The pandemic has underscored the importance of agility and strategic foresight in navigating uncertain market conditions, prompting stakeholders to rethink strategies and embrace resilience as a cornerstone of future growth.

Latest Trends & Developments:

In recent years, the North America Super Engineering Plastics Market has witnessed dynamic shifts driven by technological advancements and evolving consumer demands. A notable trend shaping the market is the growing emphasis on sustainability, with manufacturers increasingly focusing on developing bio-based and recyclable super engineering plastics to meet stringent environmental regulations and cater to eco-conscious consumers. This trend not only addresses environmental concerns but also enhances the marketability of products across industries such as automotive, electronics, and aerospace. Additionally, there has been a significant surge in research and development activities aimed at enhancing the performance characteristics of super engineering plastics, particularly in terms of heat resistance, mechanical strength, and chemical stability. This innovation-driven approach is fostering the introduction of novel materials that can withstand extreme conditions, thereby expanding their application scope in high-performance components and structural parts. Moreover, collaborations and strategic partnerships between key market players and research institutions are accelerating the commercialization of advanced super engineering plastics, ensuring a robust pipeline of new products tailored to meet the evolving needs of end-users. Furthermore, the COVID-19 pandemic has underscored the importance of resilient supply chains, prompting manufacturers to invest in local production capabilities and mitigate disruptions. Looking ahead, the North America Super Engineering Plastics Market is poised for continued growth, driven by ongoing technological innovations, increasing industrial applications, and a renewed focus on sustainability and resilience.

North America Super Engineering Plastics Market Key Players:

- DuPont

- BASF SE

- Solvay S.A.

- Celanese Corporation

- SABIC

- Covestro AG

- DSM Engineering Plastics

- Arkema S.A.

- Mitsubishi Engineering-Plastics Corporation

- Evonik Industries AG

- Polyplastics Co., Ltd.

- Lanxess AG

- Toray Industries, Inc.

- Sumitomo Chemical Co., Ltd.

- Asahi Kasei Corporation