Mucopolysaccharidosis Type II Treatment Market Size (2024 – 2030)

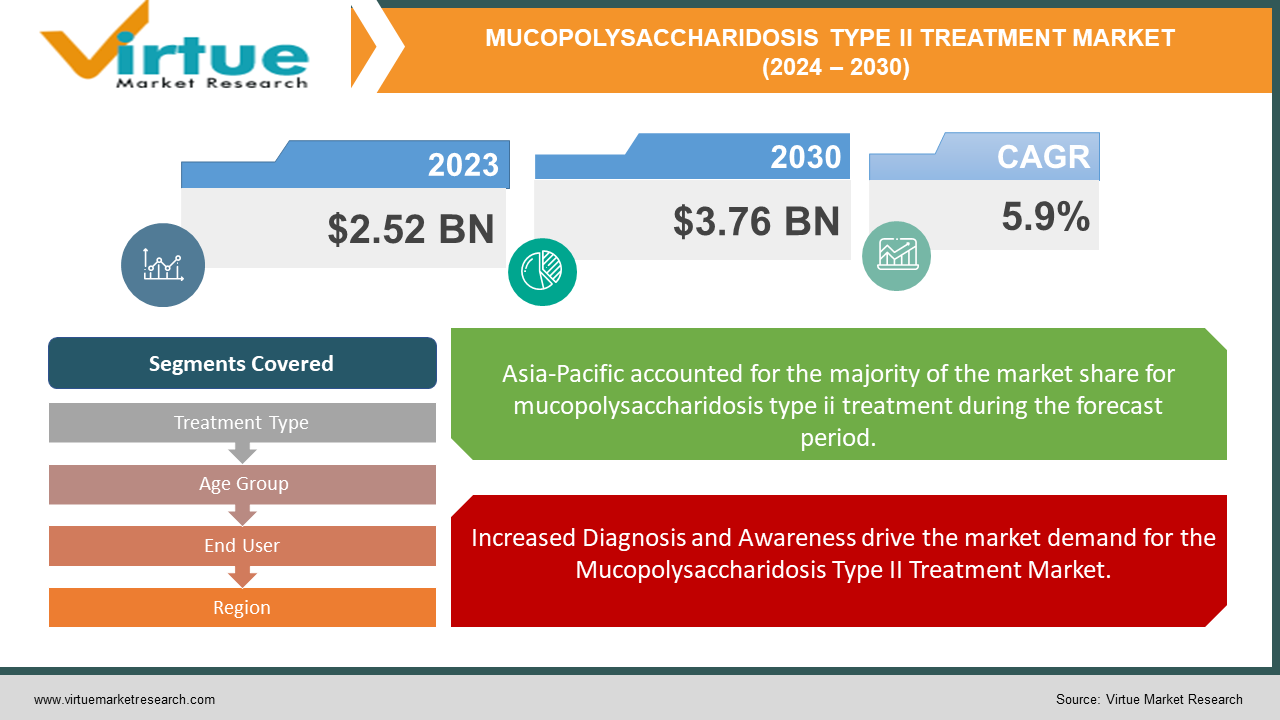

The Global Mucopolysaccharidosis Type II Treatment Market is valued at USD 2.52 Billion and is projected to reach a market size of USD 3.76 Billion by the end of 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 5.9%.

One significant long-term driver in the Mucopolysaccharidosis Type II (MPS II) treatment market is the increasing awareness and diagnosis of the condition. MPS II, also known as Hunter syndrome, is a rare genetic disorder that affects many organs and tissues. Historically, the rarity and complexity of the disease have made it difficult to diagnose and treat. However, advancements in genetic testing and increased efforts to raise awareness about rare diseases have led to more diagnoses. This surge in diagnoses has created a growing demand for effective treatments. As more patients are identified, the market for MPS II treatments expands, providing a robust and sustained growth trajectory. An exciting opportunity in the MPS II treatment market lies in gene therapy. Gene therapy aims to address the root cause of the disease by correcting the genetic defect responsible for MPS II. Several gene therapy candidates are currently in clinical trials, showing promising results.

One notable trend in the MPS II treatment industry is the increasing focus on patient-centric care. Healthcare providers and pharmaceutical companies are working closely with patients and advocacy groups to better understand the needs and challenges faced by those living with MPS II.

Key Market Insights:

The Mucopolysaccharidosis Type II Treatment Market is projected to expand at a compound annual growth rate of over 5.9% in the coming seven years, propelled by increasing urbanization and population growth in major cities worldwide.

Optum, Inc. (USA), Virgin Pulse (USA), ComPsych Corporation (USA) are some example of Mucopolysaccharidosis Type II Treatment Market.

North America & Asia-Pacific accounts for approximately 65-70 % of the Mucopolysaccharidosis Type II Treatment Market, driven by Increased Diagnosis and Awareness, Advancements in Enzyme Replacement Therapies, Emergence of Gene Therapy & Government and Regulatory Support.

Mucopolysaccharidosis Type II Treatment Market Drivers:

Increased Diagnosis and Awareness drive the market demand for the Mucopolysaccharidosis Type II Treatment Market.

One of the primary drivers of the Mucopolysaccharidosis Type II (MPS II) treatment market is the increased diagnosis and awareness of the condition. Over the past few years, advancements in genetic testing and a broader understanding of rare diseases have led to earlier and more accurate diagnoses of MPS II. Healthcare professionals are now better equipped to recognize the symptoms and genetic markers of the disease, which has resulted in a higher rate of identification. Additionally, advocacy groups and educational campaigns have played a pivotal role in raising awareness about MPS II among both medical professionals and the general public. This heightened awareness not only helps in early diagnosis but also drives demand for effective treatments, as more patients and families seek medical intervention to manage the condition.

Advancements in Enzyme Replacement Therapies drive the market demand for Mucopolysaccharidosis Type II Treatment Market.

Advancements in enzyme replacement therapies (ERT) are a significant driver in the MPS II treatment market. ERTs have become the cornerstone of MPS II management, as they help to replace the deficient or missing enzymes in patients. Recent developments in biotechnology have led to the creation of more effective and safer ERTs. These new therapies are designed to be more efficient in delivering the necessary enzymes to affected tissues and organs, thereby improving the patient's quality of life and slowing the progression of the disease. The approval and commercialization of these advanced ERTs provide a substantial boost to the market, as they offer a lifeline to patients who previously had limited treatment options.

The emergence of Gene Therapy drives the market demand for Mucopolysaccharidosis Type II Treatment Market.

Gene therapy represents a groundbreaking advancement and a significant driver for the MPS II treatment market. Unlike traditional therapies that manage symptoms, gene therapy aims to correct the underlying genetic defect causing the disease. This approach has the potential to provide a long-term solution or even a cure for MPS II. Several gene therapy candidates are currently in clinical trials, showing promising preliminary results. The possibility of a one-time treatment that can provide lasting benefits is a powerful motivator for investment and research in this area. As gene therapy continues to advance, it holds the promise of transforming the treatment landscape for MPS II, attracting considerable interest from both the medical community and pharmaceutical companies.

Government and Regulatory Support drive the market demand for Mucopolysaccharidosis Type II Treatment Market.

Government and regulatory support play a crucial role in driving the MPS II treatment market. Rare diseases like MPS II often receive special attention from regulatory bodies, which may offer incentives such as orphan drug status, grants, and expedited review processes to encourage the development of new treatments. These incentives reduce the financial and administrative burden on pharmaceutical companies, making it more feasible for them to invest in research and development for rare disease treatments. Additionally, government funding and support for rare disease research help to accelerate the discovery and development of new therapies. This supportive regulatory environment fosters innovation and ensures that new and effective treatments reach the market more quickly, benefiting patients with MPS II.

Mucopolysaccharidosis Type II Treatment Market Restraints and Challenges:

One of the most significant restraints in the Mucopolysaccharidosis Type II (MPS II) treatment market is the high cost of treatment. Enzyme replacement therapies (ERT), which are the current standard treatment for MPS II, are extremely expensive. The development, production, and distribution of these therapies involve sophisticated biotechnological processes, contributing to their high prices. For instance, the annual cost of ERT for a single patient can run into hundreds of thousands of dollars. This financial burden can be prohibitive for many patients and their families, even with insurance coverage. Moreover, healthcare systems and insurance companies often struggle with the reimbursement of such high-cost treatments, which can limit patients' access to necessary therapies. This economic barrier is a significant challenge that impacts the overall market growth and the ability of patients to receive consistent and effective care.

Mucopolysaccharidosis Type II Treatment Market Opportunities:

One of the most promising opportunities in the Mucopolysaccharidosis Type II (MPS II) treatment market lies in the expansion of personalized medicine. Personalized medicine involves tailoring treatments to the individual genetic makeup and specific needs of each patient. As our understanding of MPS II and its genetic variations deepens, there is a growing potential to develop treatments that are specifically designed for different subtypes of the disease. This approach can enhance the effectiveness of therapies and reduce adverse effects, providing better outcomes for patients.

Advancements in genetic sequencing and molecular diagnostics are key enablers of personalized medicine. By identifying the unique genetic mutations present in each patient, healthcare providers can select the most appropriate treatment regimen. For example, certain enzyme replacement therapies (ERT) might be more effective for some genetic variants of MPS II than others. Additionally, personalized medicine can help in the development of new therapeutic strategies that target the disease at a molecular level, potentially leading to more innovative and effective treatments. As personalized medicine continues to evolve, it offers a significant opportunity to improve the quality of life for MPS II patients and drive growth in the treatment market.

MUCOPOLYSACCHARIDOSIS TYPE II TREATMENT MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

5.9% |

|

Segments Covered

|

By Treatment Type, Age Group, End User, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Optum, Inc. (USA), Virgin Pulse (USA), ComPsych Corporation (USA), Wellness Corporate Solutions LLC (USA), Provant Health Solutions, LLC (USA), EXOS (USA), Interactive Health, Inc. (USA), LifeDojo Inc. (USA), Central Corporate Wellness (Australia), Fitbit, Inc. (USA)

|

Mucopolysaccharidosis Type II Treatment Market Segmentation: By Treatment Type

-

Enzyme Replacement Therapy

-

Hematopoietic Stem Cell Transplant

-

Gene Therapy

-

Substrate Reduction Therapy

-

Supportive Care

Enzyme Replacement Therapy (ERT) stands as the largest segment in the Mucopolysaccharidosis Type II (MPS II) treatment market. ERT is a well-established treatment method that addresses the root cause of MPS II by providing patients with the enzyme they lack. The therapy involves regular infusions of the synthetic enzyme idursulfase, which helps break down the glycosaminoglycans (GAGs) that accumulate in the cells of individuals with MPS II. The effectiveness of ERT in managing symptoms and improving the quality of life for patients has led to its widespread adoption. Many patients have shown significant improvements in their physical abilities, respiratory functions, and overall well-being, making ERT the cornerstone of MPS II treatment.

Gene therapy represents the fastest-growing segment in the MPS II treatment market, driven by its potential to offer a more definitive and long-term solution to the disease. Unlike traditional therapies that manage symptoms, gene therapy aims to correct the underlying genetic defect responsible for MPS II. This innovative approach involves delivering a functional copy of the defective gene to the patient’s cells, potentially providing a permanent cure. Early clinical trials have shown promising results, with some patients experiencing sustained improvements in enzyme levels and a reduction in disease symptoms.

Mucopolysaccharidosis Type II Treatment Market Segmentation: By Age Group

The pediatric segment is the largest in the Mucopolysaccharidosis Type II (MPS II) treatment market. MPS II, also known as Hunter syndrome, typically presents symptoms in early childhood, often between the ages of two and four. Given the early onset of the disease, the majority of diagnosed cases fall within the pediatric age group. Parents and healthcare providers prioritize early intervention to manage symptoms and improve the quality of life for these young patients. Treatments such as enzyme replacement therapy (ERT) are most effective when started early, as they can slow disease progression and mitigate severe complications. The focus on early diagnosis and treatment in children drives the demand for therapies tailored to the pediatric population, making it the largest segment.

While the pediatric segment remains the largest, the adult segment is the fastest-growing in the MPS II treatment market. Advances in medical care and early intervention strategies have significantly improved the life expectancy of individuals with MPS II, allowing more patients to transition into adulthood. As these patients age, there is an increasing need for continued treatment and management of the disease's chronic aspects. The growing population of adult patients has led to a surge in demand for therapies that address the long-term effects of MPS II and improve the quality of life for adults living with the condition.

Mucopolysaccharidosis Type II Treatment Market Segmentation: By End User

-

Hospitals

-

Specialty Clinics

-

Home Care Settings

-

Research Institutes

Hospitals represent the largest segment in the Mucopolysaccharidosis Type II (MPS II) treatment market. This is primarily due to the complex and specialized nature of the treatments required for managing MPS II. Hospitals are equipped with the necessary facilities and healthcare professionals to administer enzyme replacement therapy (ERT), perform hematopoietic stem cell transplants (HSCT), and conduct gene therapy procedures. These medical institutions also have the capabilities to handle the intensive monitoring and follow-up care needed for MPS II patients. Additionally, hospitals often serve as the primary centers for diagnosing rare diseases like MPS II, thus becoming the initial point of contact for patients seeking treatment. The concentration of specialized care and resources in hospitals ensures that they remain the dominant end user in the MPS II treatment market. Moreover, hospitals frequently collaborate with pharmaceutical companies and research institutions to conduct clinical trials and research studies aimed at developing new treatments for MPS II. This collaboration fosters an environment of innovation and progress within hospital settings, further enhancing their role in the treatment landscape. The ability of hospitals to provide comprehensive care, from diagnosis to advanced therapeutic interventions, solidifies their position as the largest segment in the MPS II treatment market.

Specialty clinics are emerging as the fastest-growing segment in the MPS II treatment market. These clinics are dedicated to the treatment of rare diseases and genetic disorders, offering a more focused and personalized approach to patient care. The rise of specialty clinics is driven by the increasing demand for specialized and convenient care options for MPS II patients. Unlike hospitals, which serve a broad range of medical needs, specialty clinics concentrate their resources and expertise on specific conditions, enabling them to provide more tailored and efficient treatment regimens. Specialty clinics are often at the forefront of adopting new treatment modalities and innovative care strategies. They are more agile in incorporating the latest advancements in gene therapy and other cutting-edge treatments, providing patients with access to the most up-to-date therapies. Additionally, these clinics frequently offer multidisciplinary care, bringing together specialists from various fields to address the comprehensive needs of MPS II patients. The growing recognition of the benefits of specialized and patient-centered care is driving the rapid expansion of specialty clinics, making them the fastest-growing segment in the MPS II treatment market.

Mucopolysaccharidosis Type II Treatment Market Segmentation: Regional Analysis

-

North America

-

Europe

-

Asia-Pacific

-

Latin America

-

Middle East and Africa

North America stands as the largest segment in the Mucopolysaccharidosis Type II (MPS II) treatment market. This dominance is primarily driven by the region's advanced healthcare infrastructure and significant investments in medical research and development. The United States, in particular, has numerous specialized healthcare facilities and research institutions dedicated to the diagnosis and treatment of rare diseases like MPS II. These institutions are well-equipped to conduct comprehensive genetic testing, provide cutting-edge enzyme replacement therapies (ERT), and engage in pioneering gene therapy research. Moreover, North America benefits from substantial government and private funding for rare disease research, which supports the development and availability of innovative treatments.

The Asia-Pacific region is emerging as the fastest-growing segment in the MPS II treatment market. This growth is fueled by the region's rapidly improving healthcare infrastructure and increasing awareness of rare diseases. Countries such as China, Japan, and South Korea are making significant investments in healthcare modernization, which includes the development of specialized facilities for the treatment of genetic disorders like MPS II. These investments are enhancing the region's capacity to diagnose and treat rare diseases, leading to a higher demand for advanced therapies. Moreover, the Asia-Pacific region is experiencing a surge in medical research and biotechnological advancements. Governments and private organizations in the region are funding research initiatives aimed at developing new treatments for rare diseases. This has led to the establishment of numerous clinical trials and research collaborations with international institutions.

COVID-19 Impact Analysis on Mucopolysaccharidosis Type II Treatment Market:

The COVID-19 pandemic significantly impacted the Mucopolysaccharidosis Type II (MPS II) treatment market by causing disruptions in both patient care and clinical trials. During the height of the pandemic, healthcare systems worldwide were overwhelmed by the surge in COVID-19 cases, leading to a reallocation of resources and a focus on urgent pandemic response efforts. As a result, many routine medical appointments, including those for MPS II patients, were postponed or canceled. This disruption affected the timely administration of enzyme replacement therapies (ERT) and other essential treatments, potentially leading to delays in patient care and worsening of symptoms for those with MPS II. Additionally, many ongoing clinical trials for new MPS II therapies were paused or faced delays, hindering the progress of innovative treatments and extending the timeline for new therapies to reach the market.

Latest Trends/ Developments:

One of the most exciting trends in the Mucopolysaccharidosis Type II (MPS II) treatment market is the rapid advancement of gene therapy and the development of new enzyme replacement therapies (ERT). Gene therapy represents a groundbreaking approach to treating MPS II by aiming to correct the genetic mutation that causes the disease. Recent developments in this field include promising clinical trials that focus on delivering a functional copy of the defective gene into patients’ cells. This innovative method has the potential to provide long-lasting or even permanent solutions for MPS II, moving beyond the symptom-management approach of traditional therapies. Companies and research institutions are making significant strides in this area, working to refine techniques, improve delivery mechanisms, and ensure the safety and efficacy of gene therapy treatments. As these therapies progress through clinical trials and approach regulatory approval, they offer the exciting prospect of a transformative leap forward in the treatment of MPS II.

Key Players:

-

Optum, Inc. (USA)

-

Virgin Pulse (USA)

-

ComPsych Corporation (USA)

-

Wellness Corporate Solutions LLC (USA)

-

Provant Health Solutions, LLC (USA)

-

EXOS (USA)

-

Interactive Health, Inc. (USA)

-

LifeDojo Inc. (USA)

-

Central Corporate Wellness (Australia)

-

Fitbit, Inc. (USA)