Global Lung Cancer Market Research Report – Segmentation By Route of Administration (Oral, Intravenous, Intramuscular, Subcutaneous, Parenteral, Topical, Others); By Type (Small Cell Lung Cancer, Non-Small Cell Lung Cancer, Lung Carcinoid Tumour); By Treatment Type (Chemotherapy, Immunotherapy, Radiology, Targeted Therapy, Surgery, Laser Surgery); By End-User (Hospitals, Clinics, Pharmacies); Region – Size, Share, Growth Analysis | Forecast (2024 – 2030)

GLOBAL LUNGS CANCER MARKET (2024 - 2030)

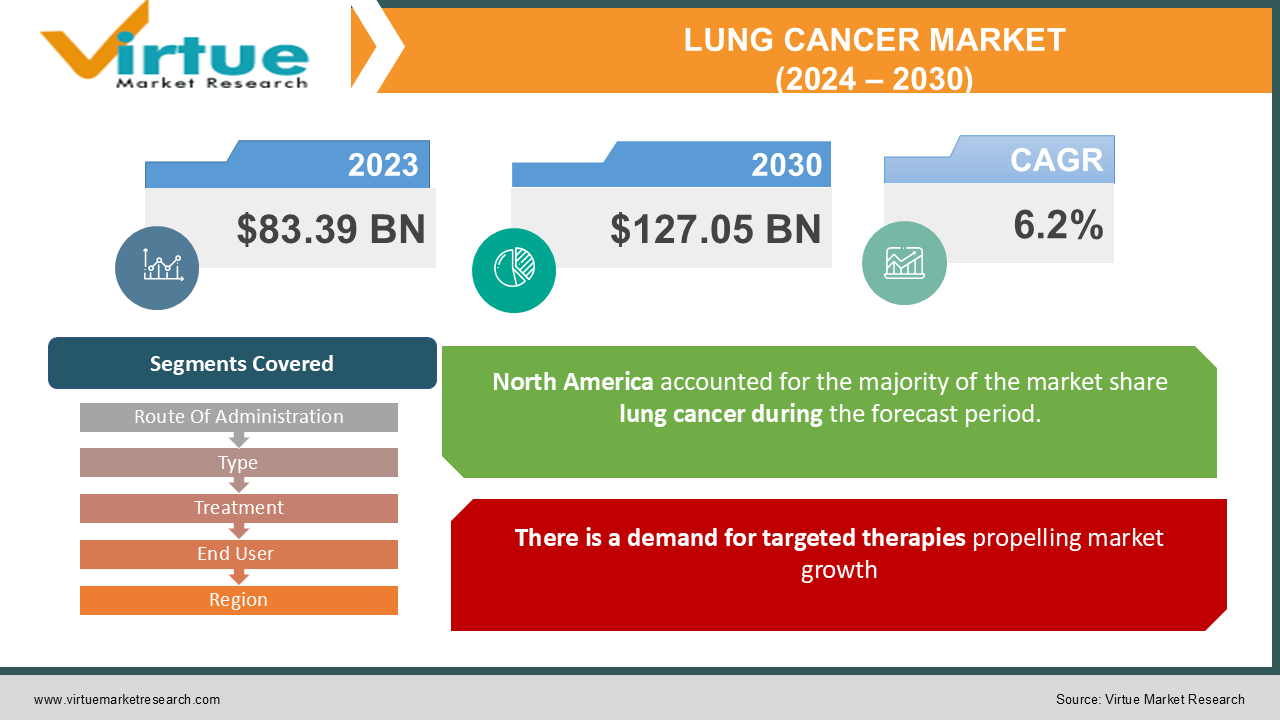

The Lungs Cancer Market was valued at USD 83.39 billion in 2023 and is projected to reach a market size of USD 127.05 billion by the end of 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 6.2%

Key Market Insights:

- The lung cancer market is booming due to early diagnosis efforts, rising demand for minimally-invasive procedures, and personalized treatment options. Targeted therapies and immunotherapy drugs are revolutionizing treatment with remarkable efficacy. Affordability and access are important concerns in R&D. The market is poised for continued growth, fueled by innovation and a focus on improving patient outcomes.

- Public health campaigns and improved screening methods are driving demand for minimally-invasive diagnostic tools. The revolution in precision medicine is offering improved treatment outcomes and reduced side effects compared to traditional chemotherapy. The cornerstone of lung cancer treatment is immunotherapy drugs, which are demonstrating remarkable efficacy.

- New drug delivery systems and innovative pricing models are being developed due to the advancement of artificial intelligence and big data, as well as affordability and access concerns. The future of the lung cancer market looks promising as innovation continues and a focus remains on improving patient outcomes.

- According to the American Cancer Society, there will be 236,740 new cases of lung cancer in the US in the year 2022.

Lungs Cancer Market Drivers:

Unhealthy lifestyles are increasing the incidence of various diseases augmenting market growth:

The increase in the adoption of unhealthy lifestyles, such as smoking, is one of the key factors propelling the overall growth rate of the lung cancer therapeutic market. Lung cancer is caused by cigarette smoking. According to the Global Burden of Disease Study, tobacco use, smoking, and second-hand smoke account for nearly 18 million deaths every year.

Lung cancer is the most lethal cancer in the US and is the second most frequent cancer. According to the American Cancer Society, lung cancer is the most common cause of cancer death. The increasing burden of diseases among the population, especially the geriatric population, along with the introduction of advanced medical technologies for the treatment of various chronic health disorders is driving the demand for medical tourism, worldwide. The support and assistance extended by the government and the tourism department of the source and the host destinations are predicted to significantly augment the market growth. People look for medical tourism due to the expensive treatment or the long waiting time in their home country or the non-availability of any treatment. Therefore, to accomplish fast and affordable medical treatment people tend to opt for medical tourism outside their home country. Moreover, the surging awareness regarding medical tourism and the increasing affordability of advanced medical treatments is a primary factor behind the escalating demand for medical tourism.

There is a demand for targeted therapies propelling market growth:

The demand for targeted therapies to treat and cure lung cancer propels the industry's growth. Targeted therapy is becoming more and more popular as a cancer treatment option. Chemo has a success rate of 30%, but targeted therapy has an 80% success rate. Treatments for lung cancer used to include surgery, chemotherapy, and radiation. Recent clinical studies have shown improvement in patients treated with immunotherapy. The market for highly efficient drugs is growing. The increasing incidence of diseases is fueling the Lungs Cancer market.

The increasing governmental investment in medical infrastructure and maintenance is fuelling the Lungs Cancer market growth.

The surging level of governmental investments to build robust, strong, and advanced healthcare facilities is propelling the medical tourism market. The favourable government policies, growing investments for the improvement of air connectivity and other transport mediums, and several initiatives to promote medical tourism are the main factors that contribute hugely to the development of the global market. Moreover, the easily available information regarding facilities and treatments of various diseases, cost, and best destinations for the treatment plays a chief role in spreading awareness regarding medical tourism among the population. Furthermore, the obvious lack of an adequate number of specialized health professionals’ results in increased medical tourism. Various health professionals undertake tourism activities to perform certain surgeries that require specialization or special knowledge to be conducted.

Medical Tourism Market Restraints and Challenges:

There are regional differences in treatment:

Lung cancer is the most common cause of cancer death in the world, and it's a burden that is felt a lot in lower- and middle-income countries. Less than 30% of cancer patients in low-income nations have access to therapy, according to the findings of the WHO. Almost two-thirds of the global population over the age of 60 will live in low- and middle-income countries by the year 2050. Chemotherapy can have unpleasant side effects, but most can be avoided and the majority will go away once the treatment is over.

Lung Cancer Market Opportunities:

The demand for new and effective lung cancer treatments is expected to increase as the prevalence of lung cancer increases. The number of lung cancer cases is likely to increase due to the aging population and the prevalence of risk factors. Lung cancer is the most common cancer in some countries, accounting for 30% of all cancer cases, according to the International Association for the Study of Lung Cancer. There were over two million new cases of lung cancer and over one million deaths in 2020. The prevalence of lung cancer is expected to increase in foreseen future.

According to researchers, the effectiveness of nanotechnology-based inhalation chemotherapy is much higher than that of conventional chemotherapy. Liposomes, micelles, polymeric NPs, inorganic NPs and solid lipid NPs have been investigated for inhalation treatment of lung cancer. An effective and promising approach for lung cancer treatment has just been published.

The golden age of cancer treatment is the result of the development and approval of new cancer therapies over the past decade. More than 95 drugs for Lung Cancer have been approved by the FDA. The last decade has seen the highest approvals in the last eight decades.

Rates of new cancers are declining due to investments in research by the National Cancer Institute.

The National Cancer Institute is the oldest and has the largest budget and research program.

According to the National Cancer Institute's Budget Fact Book 2020, the annual funds available to the NCI totalled $6, indicating increase of 3% as compared to the previous year.

GLOBAL LUNG CANCER MARKET REPORT COVERAGE:

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2022 - 2030 |

|

Base Year |

2023 |

|

Forecast Period |

2024 - 2030 |

|

CAGR |

6.2% |

|

Segments Covered |

By Route Of Administration, Type, Treatment , End User and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regional Scope |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Key Companies Profiled |

Pfizer, AstraZeneca, Merck (MSD), Bristol-Myers Squibb, Eli Lilly and Company, Boehringer Ingelheim, Novartis, Merck KGaA (EMD Serono), AbbVie, Takeda, Astellas Pharma F. Hoffmann-La Roche, GlaxoSmithKline Johnson & Johnson, Sanofi, Amgen |

Lungs Cancer Market Segmentation:

Market Segmentation: By Route of Administration:

- Oral

- Intravenous

- Intertumoral

- Intramuscular

- Subcutaneous

- Parenteral

- Topical

- Others

In the lung cancer market, intravenous (IV) administration has established itself as the predominant method of delivering treatments. This dominance can be attributed to several key factors, including high efficacy, precise dosing, and compatibility with various treatment modalities. The versatility of IV therapy allows it to seamlessly integrate with minimally-invasive procedures, further solidifying its position as the leading segment in the market. The high efficacy of IV administration is crucial in the context of lung cancer, as it ensures that the therapeutic agents reach the bloodstream directly. This direct delivery enhances the effectiveness of the treatment, allowing for a rapid and targeted response against cancer cells. Additionally, IV administration facilitates precise dosing, enabling healthcare professionals to carefully control the amount of medication administered to patients, thereby minimizing the risk of under or over-dosing.

Fastest Growing segment is Oral Route in lungs cancer segment. Compared to other routes, oral medications offer greater convenience and comfort. It is beneficial for those patients with limited mobility. Drug formulations have been improved. Advancements in drug formulation technology have led to the development of oral medications with enhanced bioavailability and stability, enabling the effective delivery of potent drugs previously limited to other routes. The global landscape is impacted by this growing adoption. The emergence of new oral drugs and innovative delivery systems is a result of the growing adoption of oral medications. The development of patient support programs and educational initiatives to enhance patient understanding and adherence to oral therapies is being driven by this trend. As the oral medication segment continues to evolve, it is expected to play an increasingly significant role in the global lung cancer market.

Market Segmentation: By Type:

- Small Cell Lung Cancer

- Non-Small Cell Lung Cancer

- Lung Carcinoid Tumour.

The global lungs cancer market is dominated by Non- Small Cell Lung Cancer, which has an 80% share. Its dominance is due to its higher prevalence compared to other types, which leads to a larger market size and significant demand for treatment options tailored specifically to non-small cell lung cancer. Targeted therapies, immunotherapy, and traditional chemotherapy are some of the treatment options available to patients with non-small cell lung cancer. Significant investments in research and development for new and more effective NSCLC therapies can be found in this diverse treatment landscape. Increased awareness campaigns and improved diagnostic tools fuel the market for non-small cell lung cancer, enabling more successful treatment interventions and driving demand for specialized treatment options. Drug development, medical device manufacturing, and healthcare services are all affected by this focus on early diagnosis. As the leading segment in the lungs cancer market, NSCLC plays a crucial role in shaping the market landscape, influencing research priorities, driving innovation, and impacting the development of new diagnostic tools and treatment options.

Small Cell Lung Cancer is the fastest growing segment. Small Cell Lung Cancer (SCLC), which is overshadowed by its larger counterpart, Non- Small Cell Lung Cancer, holds a significant presence in the global lungs cancer market. Although accounting for 15% of all lung cancer cases, SCLC's unique characteristics and aggressive nature demand specialized treatment approaches, creating a dedicated market segment with its own growth drivers. SCLC treatment relies heavily on chemotherapy and radiation therapy, with limited options for targeted therapies or immunotherapy due to its specific genetic profile. There is a market segment focused on maximizing the effectiveness of existing treatment protocols for SCLC patients.

Market Segmentation: By Treatment:

- Chemotherapy

- Immunotherapy

- Radiology

- Targeted Therapy

- Surgery

- Laser Surgery

The global market for Chemotherapy continues to hold a significant position. While newer therapies like immunotherapy are challenging its dominance, factors like established treatment protocols, cost-effectiveness, and efficacy against certain types of lung cancer ensure its continued relevance. Side effects and resistance are some of the limitations addressed in ongoing research. Chemo is a vital tool in the fight against lung cancer, and this dedicated focus places it in a position to contribute to overall market growth and influence research and development efforts in the field. Chemotherapy is the leading segment.

Immunotherapy is the fastest growing segment. The lung cancer market has seen significant market growth due to the emergence of immunotherapy. It has demonstrated the ability to achieve remarkable survival rates for non-small cell lung cancer, and this has led to its rapid ascent. As the scientific understanding of the immune system deepens, the range of immunotherapy applications expands, making it applicable to a wider range of patients and fueling market growth. With the growing emphasis on precision medicine, the personalized nature of immunotherapy, targeting specific genetic mutations and cancer pathways, align perfectly with this, further solidifying its position in the market. With ongoing research and development, this segment is expected to maintain its dominance and play a pivotal role in shaping.

Market Segmentation: By End User:

- Hospitals

- Clinics

- Pharmacies

Hospitals are the leading segment. The Hospitals segment is a crucial pillar in the global lung cancer market, playing a variety of roles in treatment delivery and impacting the market landscape in several ways. Hospitals are experiencing increased demand due to rising cancer prevalence and improved early detection efforts, as the primary setting for diagnosis, treatment, and follow-up care for lung cancer patients. Expansion of hospital capacity, investment in advanced technology, and specialized training for healthcare professionals are required because of the surge in demand. Hospitals have to adapt their infrastructure and protocols to accommodate the growing adoption of minimally-invasive procedures and personalized treatment plans. Increasing emphasis on value-based care and cost-effectiveness is prompting hospitals to deliver high-quality care at affordable costs.

The primary point of care for lung cancer patients is provided by the clinic segment. Increased patient referrals to clinics and improved diagnostic tools lead to increased demand for lung cancer services and specialized expertise. The increasing complexity of lung cancer treatment protocols requires close patient monitoring and management by qualified healthcare professionals. Clinics are adapting to this evolving landscape by investing in advanced diagnostic equipment, expanding their team with specialized medical professionals, and implementing innovative treatment delivery models. The focus on providing comprehensive and accessible care within a clinic setting contributes a lot in the growth of lungs cancer.

Market Segmentation: Regional Analysis:

- North America

- Asia-Pacific

- Europe

- South America

- Middle East and Africa

The global lung cancer market is driven by several factors. Its mature healthcare system has advanced diagnostic capabilities and access to cutting-edge treatment options, including novel immunotherapy drugs and targeted therapies. Patients from other regions are attracted to higher patient survival rates. Leading the way in innovative drug discovery and clinical trials are major pharmaceutical companies and research institutions in North America. North America's dominant position is further solidified by this constant stream of innovation. The high cost of healthcare and limited access to treatment for underserved populations pose challenges.

However, the Asia-Pacific region is anticipated to grow at the fastest during the forecast period. Asian countries are seen as the top choice for medical tourism and travel owing to the low cost of treatments. India is considered to be most popular tourist place for medical tourism, as per the Medical Tourism Index. As a result, it is boosting the growth of the market in the Asia-Pacific region. The Asia-Pacific region has become a dynamic force in the global lung cancer market. The unfortunate reality of a high smoking prevalence in many Asian countries leads to a large and increasing patient population, driving demand for effective treatment options. This demand is further amplified by rising healthcare awareness and growing disposable incomes.

COVID-19 Impact Analysis on the Lungs Cancer Market:

Screening and cancer care services were considered to be relatively low priority in many countries because of the COVID-19 outbreak. Cancer patients were at a higher risk of contracting the coronaviruses, which raised more health concerns. Due to restrictions on the movement of people and goods enacted by public and commercial agencies, the supply chain for pharmaceutical products and ingredients was disrupted. The industry has regained its pre-COVID momentum as a result of the declining cases.

The global market for lung cancer treatment has been impacted by the COVID-19 Pandemic, with several positive developments regarding new and innovative treatments. Digital health solutions have driven the global lung cancer treatment industry. Telemedicine, which allows remote consultation and monitoring of lung cancer patients, is one of the digital health solutions that has increased in adoption. This has prompted an expansion in the lungs therapy market interest for computerized wellbeing arrangements, as additional patients can get clinical consideration from a distance, and specialists more closely.

Latest Trends/ Developments:

According to a report by the Lung Cancer Foundation of America, biomarker testing is important in today's world of personalized medicine. Lung cancer testing looks for the genes in the cells of a tumor. The best course of treatment for lung cancer can be determined with the help of these biomarkers. According to a report released by the United States Department of Health and Human Services in January, a new study has identified a potential biomarker for lung cancer Non-Small Cell Lung cancer (NSCLC). There is a potential new biomarker called "SGLT2" that is used to transport glucose into some cells. Precancerous lung growths and early-stage lung cancer can be diagnosed with the help of the biomarker.

The lung cancer market is experiencing a dynamic transformation fueled by growing awareness and early diagnosis, precision medicine, the dominance of immunotherapy, and a focus on affordability and access. Public health initiatives are leading to earlier diagnosis and demand for minimally-invasive diagnostics. Targeted therapies and immunotherapy drugs are showing remarkable efficacy. Affordability and access are key concerns, while artificial intelligence and big data are aiding research and development. A promising future for lung cancer treatment is being shaped by this shift.

Key Players:

- Pfizer

- AstraZeneca

- Merck (MSD)

- Bristol-Myers Squibb

- Eli Lilly and Company

- Boehringer Ingelheim

- Novartis

- Merck KGaA (EMD Serono)

- AbbVie

- Takeda

- Astellas Pharma

- F. Hoffmann-La Roche

- GlaxoSmithKline

- Johnson & Johnson

- Sanofi

- Amgen

- In May 2022, Cizzle Biotechnology, a diagnostics company based in the United Kingdom, signed a deal with CorePath Laboratories, a full-service cancer reference laboratory. There are no simple blood tests for early detection of lung cancer that could be used to enhance access to cancer care and save lives. Over 8 million Americans are at high risk for lung cancer and should be checked annually with low-dose CT scans. Over 24,000 lung cancer deaths can be avoided with a proper examination.

- In April 2022, The European Medicines Agency approved Marketing Authorization Applications (MAAs) for tislelizumab in several non-small cell lung cancer and oesophagal squamous cell carcinoma indications. Tislelizumab is a humanized anti-PD-1 monoclonal antibody that can be used as a single therapy or in combination with other treatments. The data from the RATIONALE 302, 302, 304, and 304 Phase III trials showed significant clinical improvements over chemotherapy in a variety of cancer types and treatment lines.

Chapter 1. GLOBAL LUNGS CANCER MARKET – Scope & Methodology

1.1. Market Segmentation

1.2. Scope, Assumptions & Limitations

1.3. Research Methodology

1.4. Primary Sources

1.5. Secondary Sources

Chapter 2. GLOBAL LUNGS CANCER MARKET– Executive Summary

2.1. Market Size & Forecast – (2023 – 2030) ($M/$Bn)

2.2. Key Trends & Insights

2.2.1. Demand Side

2.2.2. Supply Side

2.4. Attractive Investment Propositions

2.5. COVID-19 Impact Analysis

Chapter 3. GLOBAL LUNGS CANCER MARKET– Competition Scenario

3.1. Market Share Analysis & Company Benchmarking

3.2. Competitive Strategy & Development Scenario

3.3. Competitive Pricing Analysis

3.4. Supplier-Distributor Analysis

Chapter 4. GLOBAL LUNGS CANCER MARKET - Entry Scenario

4.1. Regulatory Scenario

4.2. Case Studies – Key Start-ups

4.3. Customer Analysis

4.5. PESTLE Analysis

4.4. Porters Five Force Model

4.4.1. Bargaining Power of Suppliers

4.4.2. Bargaining Powers of Customers

4.4.3. Threat of New Entrants

4.4.4. Rivalry among Existing Players

4.4.5. Threat of Substitutes

Chapter 5. GLOBAL LUNGS CANCER MARKET- Landscape

5.1. Value Chain Analysis – Key Stakeholders Impact Analysis

5.2. Market Drivers

5.3. Market Restraints/Challenges

5.4. Market Opportunities

Chapter 6. GLOBAL LUNGS CANCER MARKET– By Route Of Administration

-

- Oral

- Intravenous

- Intertumoral

- Intramuscular

- Subcutaneous

- Parenteral

- Topical

- Others

Chapter 7. GLOBAL LUNGS CANCER MARKET– By Type

-

- Small Cell Lung Cancer

- Non-Small Cell Lung Cancer

- Lung Carcinoid Tumour.

Chapter 8. GLOBAL LUNGS CANCER MARKET– By Treatment

-

- Chemotherapy

- Immunotherapy

- Radiology

- Targeted Therapy

- Surgery

- Laser Surgery

Chapter 9. GLOBAL LUNGS CANCER MARKET – By End User

9.1. Hospitals

9.2. Clinics

9.3. Pharmacies

Chapter 10. GLOBAL LUNGS CANCER MARKET, By Geography – Market Size, Forecast, Trends & Insights

10.1. North America

10.1.1. By Country

10.1.1.1. U.S.A.

10.1.1.2. Canada

10.1.1.3. Mexico

10.1.2. By Type

10.1.3. By Treatment Type

10.1.4. By Route Of Administration

10.1.5. End User

10.1.6. Countries & Segments - Market Attractiveness Analysis

10.2. Europe

10.2.1. By Country

10.2.1.1. U.K.

10.2.1.2. Germany

10.2.1.3. France

10.2.1.4. Italy

10.2.1.5. Spain

10.2.1.6. Rest of Europe

10.2.2. By Product Type

10.2.3. By Treatment Type

10.2.4. By Route Of Adminsitration

10.2.5. End User

10.2.6. Countries & Segments - Market Attractiveness Analysis

10.3. Asia Pacific

10.3.2. By Country

10.3.2.2. China

10.3.2.2. Japan

10.3.2.3. South Korea

10.3.2.4. India

10.3.2.5. Australia & New Zealand

10.3.2.6. Rest of Asia-Pacific

10.3.2. By Product Type

10.3.3. By Treatment Type

10.3.4. By Route Of Administration

10.3.5. Molecule Type

10.3.6. Countries & Segments - Market Attractiveness Analysis

10.4. South America

10.4.3. By Country

10.4.3.3. Brazil

10.4.3.2. Argentina

10.4.3.3. Colombia

10.4.3.4. Chile

10.4.3.5. Rest of South America

10.4.2. By Product Type

10.4.3. By Treatment Type

10.4.4. By Route Of Administration

10.4.5. Molecule Type

10.4.6. Countries & Segments - Market Attractiveness Analysis

10.5. Middle East & Africa

10.5.4. By Country

10.5.4.4. United Arab Emirates (UAE)

10.5.4.2. Saudi Arabia

10.5.4.3. Qatar

10.5.4.4. Israel

10.5.4.5. South Africa

10.5.4.6. Nigeria

10.5.4.7. Kenya

10.5.4.10. Egypt

10.5.4.10. Rest of MEA

10.5.2. By Product Type

10.5.3. By Treatment Type

10.5.4. By Route Of Administration

10.6.5. Molecule Type

10.5.6. Countries & Segments - Market Attractiveness Analysis

Chapter 11. GLOBAL LUNGS CANCER MARKET – Company Profiles – (Overview, Product Portfolio, Financials, Strategies & Developments)

11.1. Pfizer

11.2. AstraZeneca

11.3. Merck (MSD)

11.4. Bristol-Myers Squibb

11.5. Eli Lilly and Company

11.6. Boehringer Ingelheim

11.7. Novartis

11.8. Merck KGaA (EMD Serono)

11.9. AbbVie

11.10. Takeda

11.11. Astellas Pharma

11.12. F. Hoffmann-La RocheGlaxoSmithKline

11.13. Johnson & Joson

11.14. Sanofi

11.15 Amgen

Download Sample

Choose License Type

2500

4250

5250

6900

Frequently Asked Questions

The Lungs Cancer Market was valued at USD 83.39 billion and is projected to reach a market size of USD 127.05 billion by the end of 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 6.20%.

High Incidence rate of Lungs Cancer, Highly effective presence of drugs are the key drivers for lung cancer market.

Based on Treatment, the Lungs Cancer Market is segmented into Chemotherapy, Immunotherapy, Targeted therapy and radiology, Surgery, laser Surgery.

North America is the most dominant region for the Lungs Cancer Market.

Hoffmann-La Roche Ltd, Novartis AG, Pfizer, Bristol-Myers Squibb Co, Eli Lilly and Company and Sanofi are the key players operating in the Lungs Cancer Market.