Leukemia Market Size (2025-2030)

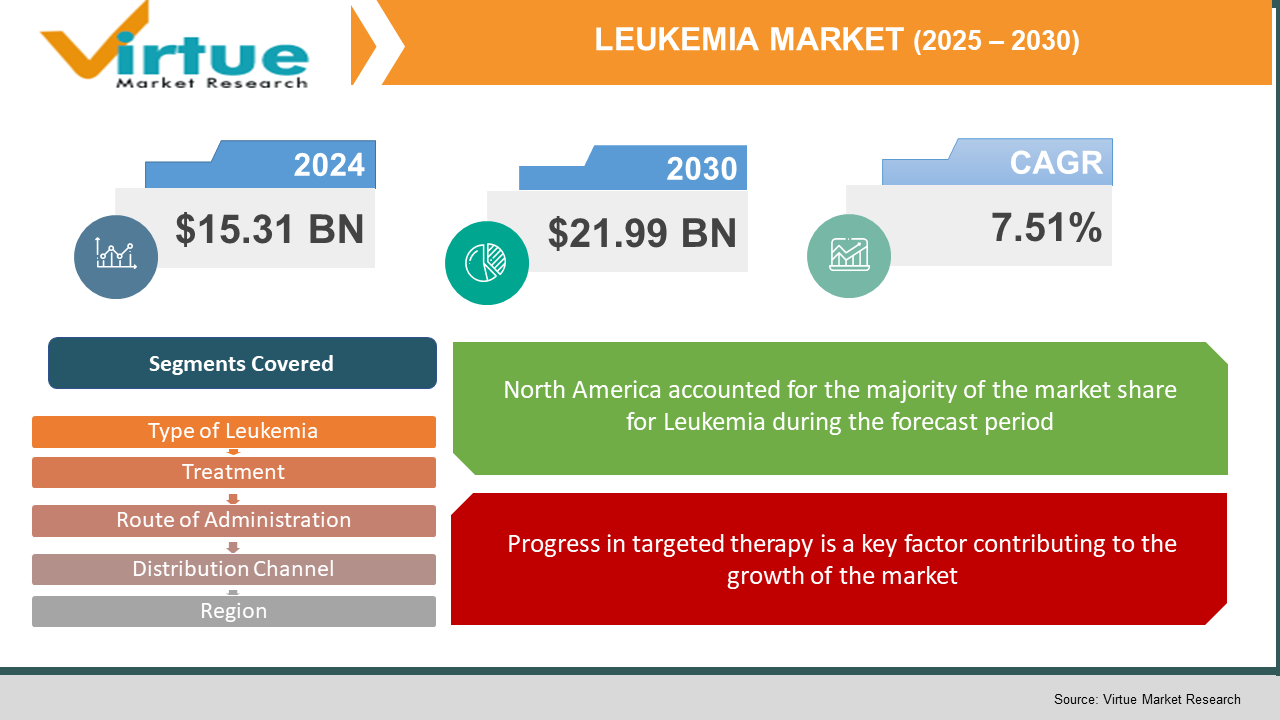

The Leukemia Market was valued at USD 15.31 billion in 2024. Over the forecast period of 2025-2030 it is projected to reach USD 21.99 billion by 2030, growing at a CAGR of 7.51%.

Leukemia represents a form of blood cancer that arises due to genetic mutations affecting the normal development of white blood cells (WBCs). These genetic alterations result in the production of abnormal WBCs within the bone marrow, ultimately leading to the onset of leukemia. Additional risk factors associated with this condition include tobacco use, a family history of leukemia, exposure to certain chemicals or radiation, existing blood disorders, and inherited genetic conditions such as Down syndrome.

Key Market Insights:

Chemotherapy and targeted therapy are among the most commonly utilized treatment approaches for leukemia. Chemotherapeutic agents circulate through the bloodstream, enabling them to reach and destroy cancer cells throughout the body. This systemic approach makes chemotherapy particularly effective for conditions like leukemia, especially in patients diagnosed with acute lymphocytic leukemia. On the other hand, targeted therapy involves the use of drugs that specifically identify and attack cancer cells, thereby inhibiting their growth and contributing to improved treatment outcomes for patients.

Leukemia Market Drivers:

Progress in targeted therapy is a key factor contributing to the growth of the market.

The rapid evolution of targeted therapies, including CAR-T cell therapy and various immunotherapies, is transforming the landscape of leukemia treatment. This method has demonstrated enhanced effectiveness, particularly in cases that do not respond to conventional treatments. By selectively attacking leukemia cells while sparing healthy tissues, CAR-T therapy significantly reduces adverse effects compared to standard chemotherapy.

In addition, checkpoint inhibitors offer an alternative strategy by enhancing immune system activity. These agents remove inhibitory signals that prevent T-cells from attacking cancer cells, thereby amplifying the body’s natural defense mechanisms. As a result, these therapies provide less invasive and more targeted treatment options alongside traditional methods.

Ongoing advancements in targeted therapies contribute to improved clinical outcomes by tailoring treatment to the unique genetic and molecular characteristics of each patient’s disease. This personalized approach has led to increased survival rates, improved quality of life, and supports the growing demand for precision medicine in oncology.

Leukemia Market Restraints and Challenges:

Significant treatment-related side effects act as a limiting factor for market expansion.

Despite notable advancements in leukemia treatment, the presence of severe side effects continues to pose a significant challenge to patient adherence and widespread therapeutic adoption. Conventional treatments such as chemotherapy and radiation remain integral to leukemia management but are associated with substantial toxicity. Common adverse effects—such as fatigue, nausea, hair loss, and immune suppression—arise from the non-selective nature of these therapies, which impact both healthy and malignant cells. These complications are particularly concerning for elderly or late-stage patients, who may be unable to tolerate intensive regimens.

While targeted therapies, including tyrosine kinase inhibitors (TKIs), have enhanced clinical outcomes in specific leukemia types like chronic myeloid leukemia (CML), they are not without risks. Patients undergoing TKI treatment may experience cardiovascular complications, fluid retention, and gastrointestinal disturbances. Prolonged use can also lead to hepatic and renal impairment, necessitating ongoing monitoring and, in some cases, treatment cessation due to concerns over quality of life.

Similarly, CAR-T cell therapy—despite its transformative potential in treating relapsed or refractory leukemia—carries significant risks such as cytokine release syndrome (CRS) and neurotoxic effects. In addition to physical side effects, patients often face emotional and financial burdens related to treatment. The high costs of managing complications, coupled with potential income loss and reduced ability to work, contribute to increased stress levels and can discourage patients from maintaining their prescribed therapy. These factors collectively represent key barriers to treatment compliance and, by extension, market growth.

Leukemia Market Opportunities:

Developments in precision medicine are opening new avenues for growth within the market.

Precision medicine has transformed the treatment paradigm for leukemia by leveraging genetic testing and biomarker profiling to design therapies that are specifically tailored to an individual’s genetic makeup. This personalized strategy significantly improves therapeutic efficacy while minimizing side effects—an essential advancement given the genetic variability that influences treatment responses in leukemia patients.

A prominent example of precision medicine in practice is the use of tyrosine kinase inhibitors (TKIs) for individuals with chronic myeloid leukemia (CML) who carry the Philadelphia chromosome mutation. Imatinib (commercially known as Gleevec), the first TKI developed for this purpose, targets the BCR-ABL fusion protein and has delivered exceptional clinical outcomes. Studies indicate that imatinib has elevated the five-year survival rate for CML patients to over 90%, marking a substantial improvement over earlier therapies. Furthermore, next-generation TKIs such as dasatinib and nilotinib offer additional treatment options with enhanced specificity and a reduced side effect profile.

In the case of acute myeloid leukemia (AML), approximately 30% of patients exhibit FLT3 gene mutations, which are linked to a poorer prognosis. The emergence of FLT3 inhibitors like midostaurin has enabled more precise treatment for this subgroup. Clinical research has demonstrated that combining midostaurin with standard chemotherapy can enhance survival outcomes by up to 23%, representing a significant therapeutic advancement for patients with FLT3-mutated AML.

LEUKEMIA MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2024 - 2030

|

|

Base Year

|

2024

|

|

Forecast Period

|

2025 - 2030

|

|

CAGR

|

7.51%

|

|

Segments Covered

|

By type of lukemia, route of administration, treatment, Distribution Channel and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Pfizer Inc., Lupin Ltd. and Novartis

|

Leukemia Market Segmentation:

Leukemia Market Segmentation By Type of Leukemia:

- Chronic Lymphocytic Leukemia

- Acute Lymphocytic Leukemia

- Acute Myeloid Leukemia

- Chronic Myeloid Leukemia

- Other Types of Leukemia

Chronic Lymphocytic Leukemia (CLL) accounts for the largest share in the leukemia type segment of the global leukemia therapeutics market. This leading position is primarily due to its high prevalence, greater detection rates among older adults, and continuous advancements in available treatments. CLL is recognized as the most common leukemia in adults, particularly across Western regions, and its typically indolent progression allows for the implementation of diverse therapeutic strategies.

According to the American Cancer Society, CLL accounts for roughly one-third of all newly diagnosed leukemia cases in the United States and approximately 1% of all cancer diagnoses. The growing incidence of CLL, especially within aging populations, continues to be a major driver of market growth. The disease is most commonly diagnosed in individuals aged 60 and above, and with global life expectancy on the rise, the prevalence of CLL is expected to increase further in the coming years.

Leukemia Market Segmentation By Treatment:

- Chemotherapy

- Immunotherapy

- Targeted Therapy

- Other Treatments

Targeted therapy has become the leading segment in the leukemia therapeutics market due to its precision and enhanced effectiveness when compared to conventional treatments such as chemotherapy. Unlike chemotherapy—which impacts both malignant and healthy rapidly dividing cells—targeted therapies are designed to act on specific molecular targets or genetic alterations present in leukemia cells. This targeted mechanism reduces the risk of widespread side effects and significantly improves clinical outcomes by interfering with the biological pathways that support leukemia cell proliferation and survival.

The introduction of tyrosine kinase inhibitors (TKIs) for chronic myeloid leukemia (CML) has been particularly transformative. Medications such as Imatinib (Gleevec) and Dasatinib have redefined the treatment landscape for CML, turning a once-fatal disease into a manageable chronic condition. Clinical data shows that TKIs contribute to a five-year survival rate exceeding 90% in CML patients, marking a significant improvement in long-term outcomes.

In the context of acute leukemia, targeted agents are increasingly being integrated with standard therapeutic protocols to improve remission rates and extend survival. Moreover, targeted therapies have become critical in addressing specific genetic mutations, such as the FLT3 mutation in acute myeloid leukemia (AML) and the Philadelphia chromosome in acute lymphoblastic leukemia (ALL), further solidifying their central role in the evolving leukemia treatment paradigm.

Leukemia Market Segmentation By Route of Administration:

- Oral Mode

- Injectable Mode

The injectable route of administration holds the largest share in the global leukemia therapeutics market. This dominance is primarily attributed to the high efficacy and rapid absorption associated with injectable treatments, which enable direct delivery of chemotherapy, immunotherapy, and other advanced therapies into the bloodstream for immediate therapeutic action.

Injectable formulations, including monoclonal antibodies and various biologics, provide greater precision in dosage and scheduling, making them especially suitable for the complex treatment needs of leukemia patients. The expanding use of biologic and targeted therapies has further reinforced the preference for injectable administration, solidifying its leading position within the market.

Meanwhile, the oral route of administration accounts for 33.1% of the market share. This segment has witnessed steady growth, driven by the convenience and patient-friendly nature of oral medications, which allow for at-home administration without the need for clinical visits or injections.

Oral leukemia treatments, including targeted agents and tyrosine kinase inhibitors (TKIs), have gained popularity due to their potential to enhance patient adherence and comfort. Ongoing advancements in drug formulation technologies have improved the efficacy and safety profile of oral therapies, supporting their increasing use in the management of leukemia.

Leukemia Market Segmentation By Distribution Channel:

- Retail Pharmacy

- Hospital Pharmacy

- Online Pharmacy

Hospital pharmacies represented the largest share of the distribution segment within the leukemia therapeutics market. Hospitals play a vital role in delivering comprehensive and advanced leukemia care, as they are equipped to handle the multifaceted nature of treatment. They function as primary referral centers for patients requiring specialized interventions and access to cutting-edge therapies.

Due to their robust infrastructure, hospitals are well-positioned to administer complex treatment protocols. Specialized oncology departments within these institutions provide tailored, patient-centric care, enhancing treatment outcomes. Furthermore, hospitals are equipped with state-of-the-art imaging technologies and diagnostic laboratories that are essential for ongoing monitoring of patients' responses to leukemia therapies. For instance, the Helford Clinical Research Hospital in the United States contributes to approximately 4.8% of initial leukemia diagnoses nationwide, reflecting the central role hospitals play in managing this disease.

Leukemia Market Segmentation- by region

- North America

- Europe

- Asia Pacific

- South America

- Middle East & Africa

North America currently holds the leading position in the global leukemia therapeutics market, driven by a high disease prevalence and significant advancements in treatment modalities. The region’s strong demand for innovative therapies, including immunotherapies and CAR T-cell treatments, is supported by a sizable patient population requiring specialized care.

According to the National Cancer Institute (NCI), the United States reports an incidence rate of 14.1 leukemia cases per 100,000 individuals, amounting to approximately 62,770 new diagnoses annually. As of 2021, over 508,796 people in the U.S. were living with leukemia, emphasizing the urgent need for advanced therapeutic solutions. Chronic myeloid leukemia (CML) alone affects over 9,000 individuals and contributes to roughly 1,000 deaths each year.

Robust investments in clinical research and trials—particularly those supported by NCI-led initiatives—further stimulate the development of combination therapies. These factors, coupled with favorable regulatory environments, firmly establish North America as a dominant force in the leukemia therapeutics landscape.

The Asia-Pacific region is expected to experience the most rapid growth in the leukemia therapeutics market over the forecast period. Key developments include Japan’s 2024 approval of acalabrutinib for first-line use and China’s multi-indication authorization for zanubrutinib, both of which cater to the region’s expanding elderly population. Chinese pharmaceutical companies continue to advance BCL-2 and BTK inhibitor pipelines, exploring competitive pricing strategies that could influence global market dynamics. Additionally, Australia and South Korea have introduced rapid reimbursement pathways for fixed-duration venetoclax-based regimens, while India is scaling flow cytometry testing capacity and pursuing local manufacturing to reduce treatment costs.

COVID-19 Pandemic: Impact Analysis

The COVID-19 pandemic has had both positive and negative effects on the healthcare sector. In response to efforts to curb the virus’s spread, governments around the world imposed strict lockdowns, which disrupted the balance between supply and demand for pharmaceutical products. Many pharmaceutical manufacturers operate production facilities in countries significantly impacted by the pandemic, including the United States, the United Kingdom, and Germany. These disruptions adversely affected revenues for a broad range of healthcare products during the crisis.

Moreover, the decline in non-COVID patient admissions led to a reduction in the number of medical procedures and prescription volumes for various treatments, including those unrelated to COVID-19. However, the pandemic also brought increased attention to the vulnerabilities of immunocompromised individuals. According to findings from the U.K. Coronavirus Cancer Monitoring Project (UKCCMP), patients with blood cancers—particularly leukemia, multiple myeloma, and lymphoma—face a heightened risk of severe COVID-19 complications. This elevated risk is expected to drive greater demand for leukemia therapeutics, as healthcare systems prioritize the treatment of at-risk populations.

Latest Trends/ Developments:

June 2025: Nurix Therapeutics announced its intention to initiate global registration trials for its investigational BTK degrader, NX-5948, following promising results from the Phase 1a/1b clinical study. The trial demonstrated a response rate of 75.5% in patients with relapsed or refractory chronic lymphocytic leukemia (CLL).

February 2025: InnoCare Pharma secured regulatory approval in China to commence a Phase III clinical trial evaluating a combination of the BCL-2 inhibitor ICP-248 and the BTK inhibitor orelabrutinib as a first-line treatment for leukemia. The trial represents a significant step in advancing precision medicine for treatment-naïve patients.

Key Players:

These are top 10 players in the Leukemia Market :-

- Pfizer Inc.

- Lupin Ltd.

- Novartis

- AbbVie

- Amgen Inc.

- Bristol-Myers Squibb

- Johnson & Johnson Services, Inc.

- Takeda Pharmaceutical Co Ltd

- F. Hoffmann-La Roche

- Sanofi/ Genzyme Corporation