Intraocular Lens Market Size (2025 – 2030)

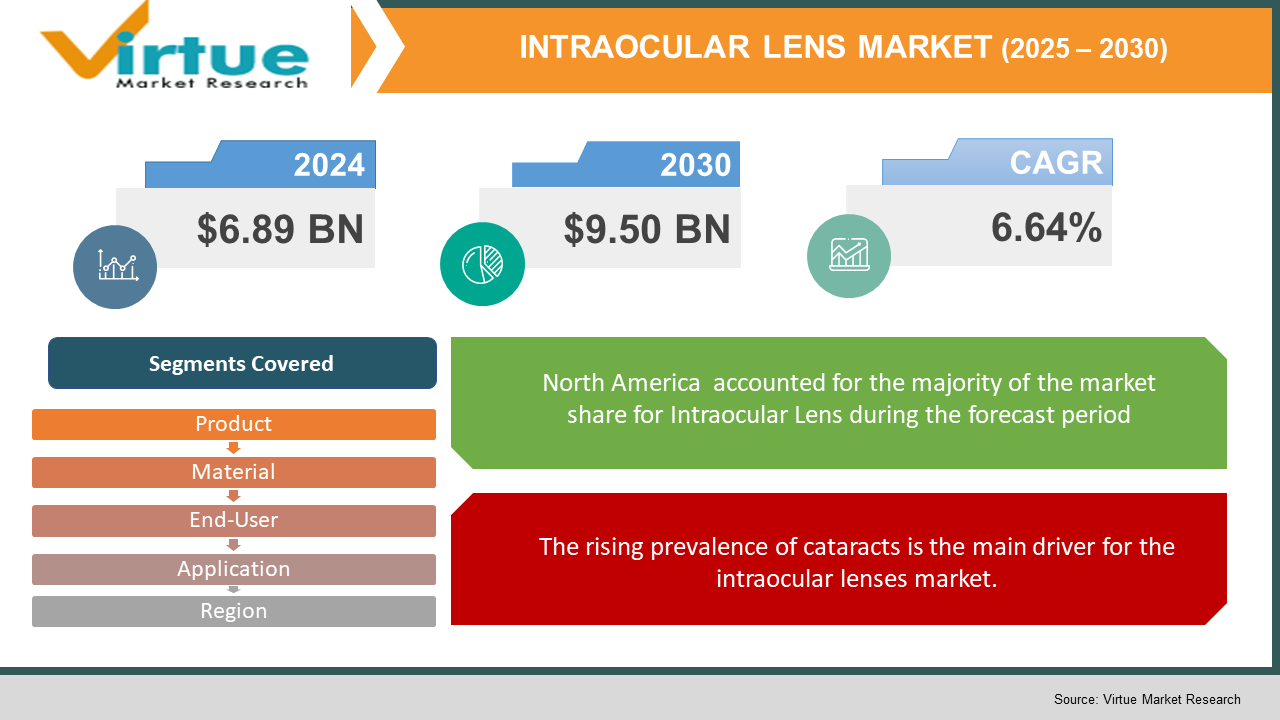

The Global Intraocular Lens Market was valued at USD 6.89 billion and is projected to reach a market size of USD 9.50 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 6.64%.

Rising cataract numbers and improvements in lens technology will drive substantial growth in the worldwide intraocular lens (IOL) industry from 2025 to 2030. During cataract surgery or to fix refractive errors, intraocular lenses are artificial lenses planted to restore the eyes' natural lens. The increasing aged populace together with a boom in ocular problems brought about by diabetes has raised the requirement for IOLs.

Key Market Insights:

- Trifocal and extended depth-of-focus (EDOF) lenses among other inventions are improving vision results and lowering reliance on optical aids. These developments are enlarging the market by means of which premium IOLs are becoming more accepted.

- Increasing cataract frequency caused by an aging world population and rising diabetes rates are driving the demand for IOLs, therefore appealing to customers. Often correlated with aging and diabetes, the rising prevalence of eye diseases like cataracts and diabetic retinopathy calls for more IOLs. Expected market development in the next years is driven by this trend.

- Rising demand for minimally invasive cataract procedures is fueling the growth of the intraocular lens (IOL) industry. Patients and surgeons alike are increasingly using methods like phacoemulsification, which create minor cuts and provides fast recovery time. This tendency improves results for patients and helps the IOL industry develop.

Intraocular Lenses Market Drivers:

The rising prevalence of cataracts is the main driver for the intraocular lenses market.

Leading everywhere in the world for vision loss is cataracts. Since these lenses are necessary to restore vision after cataract surgery, the rising number of cataract cases has resulted in a greater need for intraocular lens (IOL) implants. Cataract operations' increase exactly drives IOL industry expansion.

Technological advancements in the ILO are a major reason behind the growth of the intraocular lens market.

Continuous innovations have spurred the creation of sophisticated IOLs including accommodating, multifocal, and toric lenses. Improved visual results provided by these lenses help to fix astigmatism and presbyopia. Their superior performance and increased patient satisfaction are driving their use among both patients and ophthalmologists.

The increase in the portion of the aging population is leading to a high demand for intraocular lenses and hence leading to the growth of the market.

An increased prevalence of age-related eye issues, including cataracts, has resulted from the worldwide demographic change toward an older society. Growing numbers of older people will increase the need for cataract operations and therefore IOLs, hence driving market expansion.

Government initiatives and reimbursement policies are pushing the growth of the market.

Many governments are running initiatives to alleviate the load on visually impaired individuals. More patients are starting these operations thanks in part to projects meant to make eye care affordable and accessible in concert with good reimbursement rules for cataract surgery. This support greatly raises the market for IOLs.

Intraocular Lenses Market Restraints and Challenges:

The high cost of premium IOLs is a big market challenge for the intraocular lenses market.

High-cost advanced IOLs like toric and multifocal lenses provide better vision results but come at a premium cost. Especially in areas with limited health funding or insufficient insurance coverage, this cost factor can be prohibitive for patients, hence driving a preference for more affordable, conventional IOL alternatives.

There is a shortage of highly skilled ophthalmic surgeons which is restricting the market growth.

Successfully implanted IOLs need particular surgical knowledge. A sharp shortage of qualified ophthalmologists in many developing nations limits the number of operations done and slows down market expansion. Patients may have to wait longer and access to essential eye care might be limited as a result of this deficit.

Strict and complex rules and regulations are a hindrance to market growth.

Stringent government guidelines are imposed on the intraocular lens sector to guarantee patient safety and product performance. For manufacturers, negotiating difficult approval procedures can be time-consuming and expensive, possibly slowing down the launch of fresh goods to the consumer. Furthermore complicating worldwide market entry plans are different laws across nations.

Limited awareness and availability of ILOs in emerging markets is a major challenge for market growth.

The level of knowledge in many less developed areas about cataract-related vision loss and the possibility of corrective operations is still modest. This lack of knowledge restricts the use of intraocular lenses among the limited medical facilities. Essential for surpassing this obstacle and increasing market reach are initiatives in population education and higher accessibility of healthcare.

Intraocular Lenses Market Opportunities:

An increase in technological advancements poses a great opportunity for the market to grow.

Constant ophthalmologic research and development have resulted in the creation of sophisticated IOLs, including accommodating and self-adjusting lenses. These advances seek to mimic the eye's natural focusing capacity, therefore resulting in better visual outcomes for patients. As patients and medical experts look for better vision correction options, the ongoing development of IOL technology offers many chances for market expansion.

The rising awareness and demand for better eye treatment facilities are contributing to market growth.

Developing nations are growing economically, which increases disposable income and enhances hospital infrastructure with time and ability. Greater numbers of people can have cataract operations and IOL implants thanks in large part to this economic development. Rising awareness of eye health and increasing accessibility of medical institutions will together substantially increase IOL demand in these areas, therefore offering a great chance for market development.

Supportive Government policies are a major market opportunity for the intraocular lens market to grow.

Several governments are running initiatives to lower the incidence of vision impairments including cataracts. Cataract procedures should be more readily available and inexpensive through programs like public information campaigns, discounts on eye care services, and cooperation with private healthcare providers. These supportive policies are expected to help the number of operations performed rise, therefore driving IOLs' demand.

The rise in the global aging population presents a great market opportunity for the intraocular lens market to grow worldwide.

The general rise in the elderly population corresponds with a greater frequency of age-related eye disorders, especially cataracts. Rising life expectancy also calls for good vision correction technologies. As more people look for surgical solutions to keep their quality of life, this demographic trend is predicted to propel the need for IOLs.

INTRAOCULAR LENS MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2024 - 2030

|

|

Base Year

|

2024

|

|

Forecast Period

|

2025 - 2030

|

|

CAGR

|

6.64%

|

|

Segments Covered

|

By Product, material, end user, application, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Johnson and Johnson Vision Care, Carl Zeiss Meditec, HOYA Corporation, Rayner Intraocular Lenses, Alcon, Bausch + Lomb, and STAAR Surgical Company

|

Intraocular Lenses Market Segmentation:

Intraocular Lens Market Segmentation: By Product

- Monofocal

- Multifocal

- Toric

- Accommodative

Monofocal lenses are the dominant segment and multifocal and toric lenses are the fast-growing segment.

Most commonly employed in regular cataract operations, monofocal intraocular lenses are meant for sight at one distance.

By imitating the eye's natural adjustment, an accommodative intraocular lens lets one focus at various distances.

Multifocal Intraocular Lens: Offers many focal points to minimize the need for spectacles for long and near sight.

Toric Intraocular Lenses specifically fix astigmatism by offsetting corneal anomalies.

Intraocular Lens Market Segmentation: By Material

- Hydrophobic Acrylic

- Hydrophilic Acrylic

- Polymethylmethacrylate

Hydrophobic Acrylic is the dominant segment and the Hydrophilic Acrylic is the fast-growing segment.

Hydrophobic Acrylic are widely used due to their foldable nature that allows them insertion through smaller incisions which helps in faster recovery.

Hydrophilic Acrylic are known for their flexibility and high water content that can help in enhancing biocompatibility.

Polymethylmethacrylate was the first ever material that was used in IOL manufacturing and is characterized by its rigidity.

Intraocular Lens Market Segmentation: By End-User

- Hospitals

- Ambulatory Surgery Centers

- Ophthalmic Clinics

Hospitals and Ambulatory Surgery Centers are the dominant segment whereas, Ophthalmic Clinics are the fast-growing segment.

Primary centers for surgical procedures and postoperative treatment are hospitals.

Ambulatory Surgery Centers offer surgical procedures that have shorter recovery times.

Research institutions and sophisticated eye centers are among other end users.

Intraocular Lens Market Segmentation: Application

- Cataract

- Presbyopia

- Corneal Disorders

- Other Applications

The dominant segment is the Cataract and the fast-growing segment is the Presbyopia.

Clear vision is restored by the replacement of the clouded natural lens in cataracts.

Age-related near vision decline, corrected with particular IOL models, is referred to as presbyopia.

Corneal illnesses include keratoconus fixed by special lenses.

Other refractive disorders include myopia, hyperopia, and other refractive errors.

Intraocular Lens Market Segmentation: By Region

- North America

- Asia-Pacific

- Europe

- South America

- Middle East and Africa

Advanced healthcare infrastructure and great use of premium IOLs in North America are the reasons why it has the largest market share.

Europe is seeing a major expansion resulting from more cataract surgeries and good reimbursement policies.

Asia-Pacific is a faster-growing area propelled by a big aging population and increasing consciousness of ocular health.

The Middle East and Africa are seeing a long market expansion with advancements in medical infrastructure.

South America is an emerging market with growing ophthalmic treatment investments.

COVID-19 Impact Analysis on the Global Intraocular Lens Market:

The worldwide intraocular lens (IOL) business was greatly thrown off by the COVID-19 epidemic. To give COVID-19 cases priority and reduce virus spread, elective surgeries including cataract procedures were postponed or canceled, therefore causing a marked drop in IOL need during the height of the epidemic. Resource limitations for healthcare institutions meant that patients delayed non-urgent medical appointments, therefore affecting market expansion. But as vaccination rates rose and healthcare systems adjusted to the new normal, surgical numbers have rebounded, and the IOL market is on track for growth. The epidemic also sped up the use of telemedicine, which allowed preoperative appointments and postoperative follow-up remotely, therefore improving patient access to eye care.

Latest Trends/ Developments:

The IOL market is seeing developments including trifocal lenses and extended-depth-of-focus (EDOF) lenses aiming to give patients better vision across several distances and therefore lower dependence on corrective eyewear.

Patient demand for improved vision quality and the need to fix astigmatism and presbyopia during cataract operation is driving an increasing preference for premium IOLs such as toric and multifocal lenses.

Key players are growing their international presence to match the rising demand. For example, Rayner grew their presence in Australia and France in 2022, therefore increasing product availability in those areas. AffaMed Technologies, for example, acquired exclusive rights from SIFI in October 2023 to develop and sell extended mono-focal IIL EVOLUX in Greater China. By preserving distance vision and enhancing intermediate vision for patients, this collaboration seeks to increase daily activities. Becoming a major trend, these partnerships let businesses build upon each other’s strengths and speed up the use of sophisticated IOL technologies in many locations.

Key Players:

- Alcon (Novartis AG)

- Bausch + Lomb (Bausch Health Companies Inc.)

- Johnson and Johnson Vision Care, Inc.

- Carl Zeiss Meditec AG

- HOYA Corporation

- Rayner Intraocular Lenses Limited

- STAAR Surgical Company