Industrial Dust Collector Market Size (2024-2030)

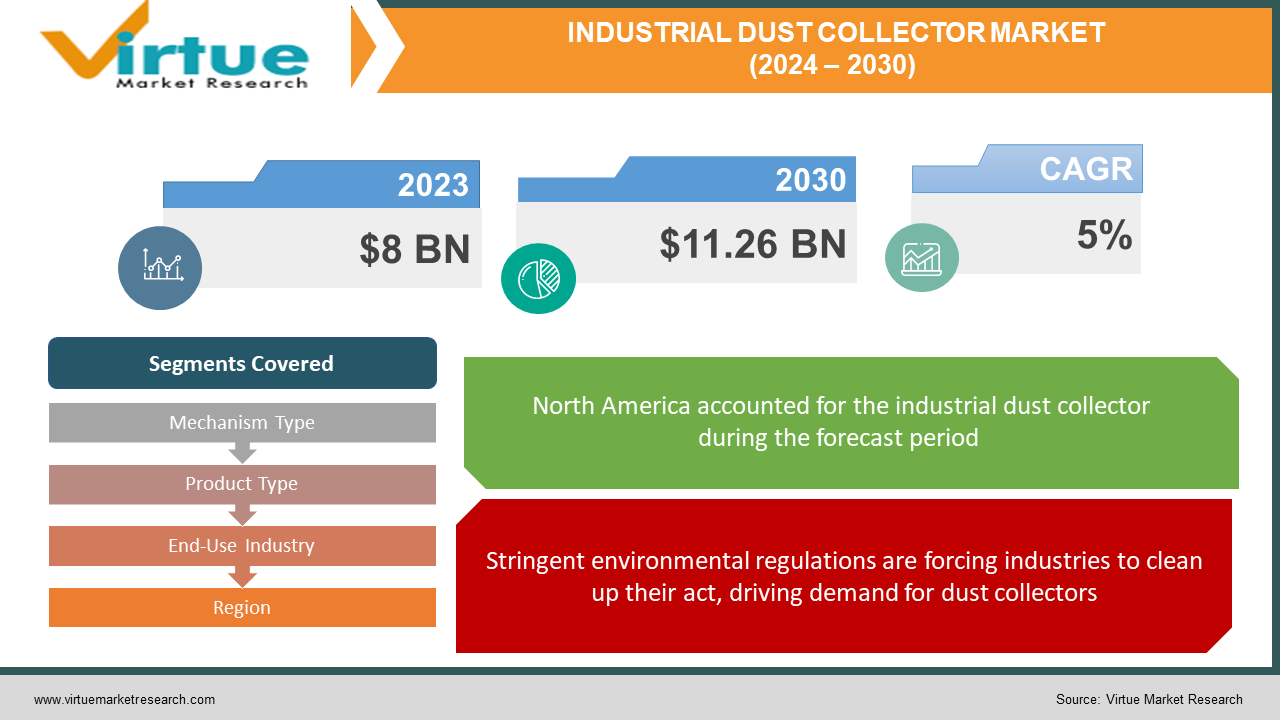

The Industrial Dust Collector Market was valued at USD 8 billion in 2023 and is projected to reach a market size of USD 11.26 billion by the end of 2030. Over the cast period of 2024 – 2030, the figure for requests is projected to grow at a CAGR of 5%.

The industrial dust collector market is on an upward trajectory, fueled by a growing focus on environmental responsibility and healthy workplaces. Stricter regulations and rising awareness of clean air are driving demand for these air pollution control systems across various industries. From metalworking to food processing, dust collectors play a crucial role in capturing harmful airborne particles, safeguarding worker health and product quality. As manufacturing activities expand, particularly in developing economies, the need for efficient dust collection solutions will continue to rise. Manufacturers are innovating to create energy-saving and user-friendly dust collectors, further propelling market growth.

Key Market Insights:

The industrial dust collector market is experiencing a surge, fueled by a growing commitment to clean air and healthy work environments. Environmental regulations are becoming stricter worldwide, and worker safety is taking center stage. This is leading to a rise in demand for dust collection systems across various industries. From metalworking to food processing, these systems play a crucial role in capturing harmful airborne particles. As a result, dust collectors are becoming essential for businesses to ensure worker health, product quality, and compliance with environmental regulations. This is particularly true in developing economies where rapid industrialization is creating a significant increase in dust generation.

This growing demand is pushing manufacturers to innovate. They are developing energy-efficient dust collectors with features like remote monitoring for easier maintenance. Additionally, they are creating industry-specific solutions. For instance, cost-effective baghouse collectors are ideal for cement production, while easily cleaned cartridge collectors cater well to the food processing industry. This customization ensures optimal dust control solutions for various applications.

Looking ahead, the industrial dust collector market shows a promising future. With a focus on clean air, worker safety, and sustainable practices, manufacturers are constantly seeking ways to reduce the environmental footprint of these systems. This commitment to a cleaner future position the industrial dust collector market for continued growth.

The Industrial Dust Collector Market Drivers:

Stringent environmental regulations are forcing industries to clean up their act, driving demand for dust collectors.

Stringent environmental regulations are a major driver. Governments worldwide are enacting stricter air quality standards, mandating businesses to invest in dust collection systems to comply. This regulatory push creates a robust market for dust collectors across numerous industries.

Growing awareness of worker health risks is prompting companies to invest in dust collection for a safer work environment.

With growing awareness of the health risks associated with dust exposure, worker safety is becoming a top priority. Companies are actively seeking solutions to capture harmful airborne particles, fostering a safer and healthier work environment for employees. This increased focus on worker well-being directly translates to a rise in demand for industrial dust collectors.

The surge of industrial activity, particularly in developing economies, creates a dust problem that dust collectors can solve.

Rapid industrialization, particularly in developing economies, is causing a surge in dust generation. Industries such as metalworking, cement production, and power generation are major dust producers. To minimize environmental impact and ensure healthy working conditions, these industries require efficient dust collection solutions, driving market growth.

Manufacturers are innovating with energy-efficient and user-friendly dust collectors, making them more attractive to businesses.

Manufacturers are constantly innovating dust collector technology. The focus is on developing energy-efficient systems with features like Internet of Things (IoT) integration for remote monitoring and easier maintenance. These advancements make dust collectors more attractive for businesses seeking cost-effective and user-friendly solutions, further propelling market growth.

The focus on sustainability is leading to the development of eco-friendly dust collectors, ensuring a greener future for the market.

There's a growing emphasis on sustainable practices within the dust collector market itself. Manufacturers are exploring ways to reduce the environmental footprint of these systems, such as using recycled materials in construction and developing energy-efficient operation mechanisms. This focus on sustainability positions the market for continued growth as industries strive for cleaner operations.

The Industrial Dust Collector Market Restraints and Challenges:

The industrial dust collector market, while promising, faces hurdles that can impede its growth. A significant barrier is the high initial investment required to purchase and install these systems. This upfront cost can be a burden for smaller businesses, limiting their adoption. Additionally, ongoing maintenance costs, such as filter replacements, add to operational expenses. Choosing the right dust collector further complicates things. Businesses unfamiliar with the technology might struggle to select the most suitable system for their specific dust type, volume, and airflow needs. Furthermore, limited awareness, particularly in developing economies, can hinder market penetration. Businesses may not fully understand the benefits of dust collectors, leading them to overlook these solutions. Finally, economic fluctuations pose a challenge. During downturns, businesses may tighten spending and view dust collectors as non-essential, potentially curbing market demand. These restraints necessitate innovative solutions from manufacturers, such as offering financing options or developing more cost-effective systems. Educational outreach can also play a role in raising awareness about the long-term benefits of dust collectors for worker health, product quality, and environmental compliance. By addressing these challenges, the industrial dust collector market can navigate these hurdles and continue its upward trajectory.

The Industrial Dust Collector Market Opportunities:

The industrial dust collector market's potential extends far beyond addressing current needs. Emerging economies with booming industrial activity represent a vast untapped market. As environmental regulations and worker safety concerns rise in these regions, the demand for efficient dust collection solutions will surge. Manufacturers can seize this opportunity by tailoring their products and educational efforts to these specific markets. Furthermore, advancements in technology hold immense promise. Imagine dust collectors with remote monitoring, predictive maintenance, and real-time data analysis for optimal performance – all powered by the Internet of Things. These innovations will not only improve efficiency but also make dust collectors more appealing to businesses seeking intelligent solutions. Sustainability is another key area. Manufacturers who develop eco-friendly dust collectors built from recycled materials and designed for energy-efficient operation will be well-positioned for success. Additionally, customization is crucial. Developing dust collectors specifically tailored to the unique needs of various industries, like those designed for specific dust types, particle sizes, or airflow requirements in pharmaceuticals or woodworking, will cater more effectively to diverse clientele. Finally, the aftermarket for dust collector parts and maintenance services presents a lucrative opportunity. By providing readily available replacement filters, efficient maintenance programs, and accessible technical support, manufacturers can build stronger customer loyalty and generate recurring revenue streams. By capitalizing on these opportunities, the industrial dust collector market can ensure a bright and clean future, fostering cleaner air, healthier workplaces, and a more sustainable industrial landscape.

INDUSTRIAL DUST COLLECTOR MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

5% |

|

Segments Covered

|

By Mechanism Type, Product Type, End-Use Industry, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Donaldson Company, Camfil Group, Nederman Holding AB, Parker Hannifin Corporation, 3M Company, Babcock & Wilcox Enterprises, Inc., FLSmidth, AAF International, CECO Environmental Corp.

|

Industrial Dust Collector Market Segmentation: By Mechanism Type

-

Dry Dust Collectors

-

Wet Dust Collectors

Dry dust collectors dominate the industrial dust collector market due to their affordability and ease of maintenance. They use filters like fabric bags or cartridges to capture dust without water. Conversely, wet dust collectors, while effective for hazardous materials and fine dust particles, are expected to be the fastest-growing segment. Their ability to handle these challenging dust types makes them increasingly attractive in various industries.

Industrial Dust Collector Market Segmentation: By Product Type

The most dominant segment in the industrial dust collector market by product type is Baghouse Dust Collectors. These are popular for their high capacity and cost-effectiveness, making them ideal for heavy dust loads in industries like cement and metalworking. However, the fastest-growing segment is Cartridge Dust Collectors. Their ability to capture finer dust particles makes them attractive for applications in pharmaceuticals, food processing, and other industries with stricter air quality requirements.

Industrial Dust Collector Market Segmentation: By End-Use Industry

-

Metalworking

-

Chemicals

-

Food and Beverage

-

Pharmaceuticals

-

Woodworking

-

Power Generation

-

Cement

The cement industry is currently the dominant segment in the industrial dust collector market by end-use industry, due to the large amount of dust generated during material handling and processing. Regulations and a focus on environmental impact are driving growth in this sector. The fastest-growing segment is expected to be developing economies, as rapid industrialization leads to a surge in dust generation across various industries. This will require them to implement dust collection systems to comply with stricter environmental regulations and ensure worker safety.

Industrial Dust Collector Market Segmentation: Regional Analysis

-

North America

-

Europe

-

Asia-Pacific

-

South America

-

Middle East and Africa

North America: This established market boasts robust regulations and a high level of awareness regarding the benefits of dust collection systems. Growth here is primarily driven by stricter environmental regulations and a continued emphasis on worker safety within existing industries. Manufacturers in North America are likely to focus on developing even more efficient and innovative dust collectors to comply with evolving regulations.

Europe: Much like North America, Europe presents a well-developed market with stringent regulations in place. However, the European market differentiates itself through a strong focus on technological advancements and energy efficiency in dust collector design. Manufacturers here are likely to prioritize features like remote monitoring and Internet of Things (IoT) integration for improved performance and user experience.

Asia-Pacific: This region is experiencing the fastest growth in the dust collector market, fueled by rapid industrialization. While regulations are currently less stringent compared to developed regions, they are gradually becoming more robust. China and India are major players in this market, generating significant amounts of dust and driving a surge in demand for effective dust collection solutions. Manufacturers can capitalize on this growth by offering cost-effective, yet efficient dust collectors tailored to the specific needs of these booming economies.

South America: This developing market showcases a growing awareness of environmental concerns and worker safety. As environmental regulations become stricter, the demand for dust collectors is expected to rise significantly. Manufacturers here have an opportunity to cater to this growing need by offering educational outreach programs alongside their products, helping businesses understand the long-term benefits of dust collection systems.

Middle East and Africa: This region holds immense potential for future market growth due to increasing industrial activity and expanding economies. However, limited awareness about dust collection benefits and underdeveloped infrastructure poses challenges. Manufacturers can play a crucial role in overcoming these hurdles by investing in educational initiatives and collaborating with local partners to establish a strong market presence. By addressing these challenges, the Middle East and Africa can unlock their full potential in the industrial dust collector market.

COVID-19 Impact Analysis on the Industrial Dust Collector Market:

The COVID-19 pandemic undoubtedly threw a curveball at the industrial dust collector market. Lockdowns and economic slowdowns forced temporary closures or reduced activity in industries like construction, automotive, and manufacturing. This naturally led to a drop in demand for dust collectors as production processes slowed down. However, the impact wasn't uniform across all sectors. While some industries saw a decline, others like pharmaceuticals and healthcare experienced a rise in demand. The need for sterile environments in these sectors pushed the need for dust collectors to ensure product quality and worker safety. Interestingly, the pandemic also triggered a renewed focus on clean air and worker well-being. This has led to stricter environmental regulations and a renewed emphasis on worker safety in some regions. This bodes well for the long-term growth of the dust collector market as businesses prioritize dust control solutions. The pandemic did disrupt global supply chains, causing shortages of raw materials and delays in equipment deliveries, posing challenges for manufacturers, and impacting project timelines. However, as economies recover and industrial activity picks up again, the demand for dust collectors is expected to rebound. The growing focus on clean air, worker safety, and stricter environmental regulations will continue to propel market growth. Manufacturers who can adapt to this evolving landscape and offer innovative solutions that address post-pandemic concerns will be well-positioned to succeed in the future.

Latest Trends/ Developments:

The industrial dust collector market is embracing innovation and sustainability. One exciting trend is the integration of Internet of Things (IoT) technology. This allows for remote monitoring, real-time data analysis, and even predictive maintenance through sensors and connectivity features. This translates to better operational efficiency, reduced downtime, and dust collectors that perform optimally. Artificial intelligence (AI) is also making its way into the mix, with potential applications in analyzing performance data and predicting maintenance needs. This proactive approach can prevent equipment failures before they happen. Sustainability is another key area of development. Manufacturers are focusing on energy-efficient designs, like variable speed drives, to lower energy consumption and operating costs. They're also exploring the use of recycled materials in construction and biodegradable filter materials to minimize environmental impact. Additionally, customization is on the rise. Dust collector manufacturers are developing solutions tailored to specific industries, addressing needs like dust explosion protection or capturing specific dust particle types. Finally, the importance of aftermarket services is growing. By providing readily available replacement parts, efficient maintenance programs, and accessible technical support, manufacturers can not only generate recurring revenue but also build stronger customer loyalty. These trends highlight a shift towards intelligent, sustainable, and industry-specific dust collection solutions, ensuring a future of clean air and a thriving industrial dust collector market.

Key Players:

-

Donaldson Company

-

Camfil Group

-

Nederman Holding AB

-

Parker Hannifin Corporation

-

3M Company

-

Babcock & Wilcox Enterprises, Inc.

-

FLSmidth

-

AAF International

-

CECO Environmental Corp.