Agriculture Market

In 2025, the global Agriculture Market was valued at approximately USD 12.97 trillion, making it one of the world’s largest and most economically critical industries.

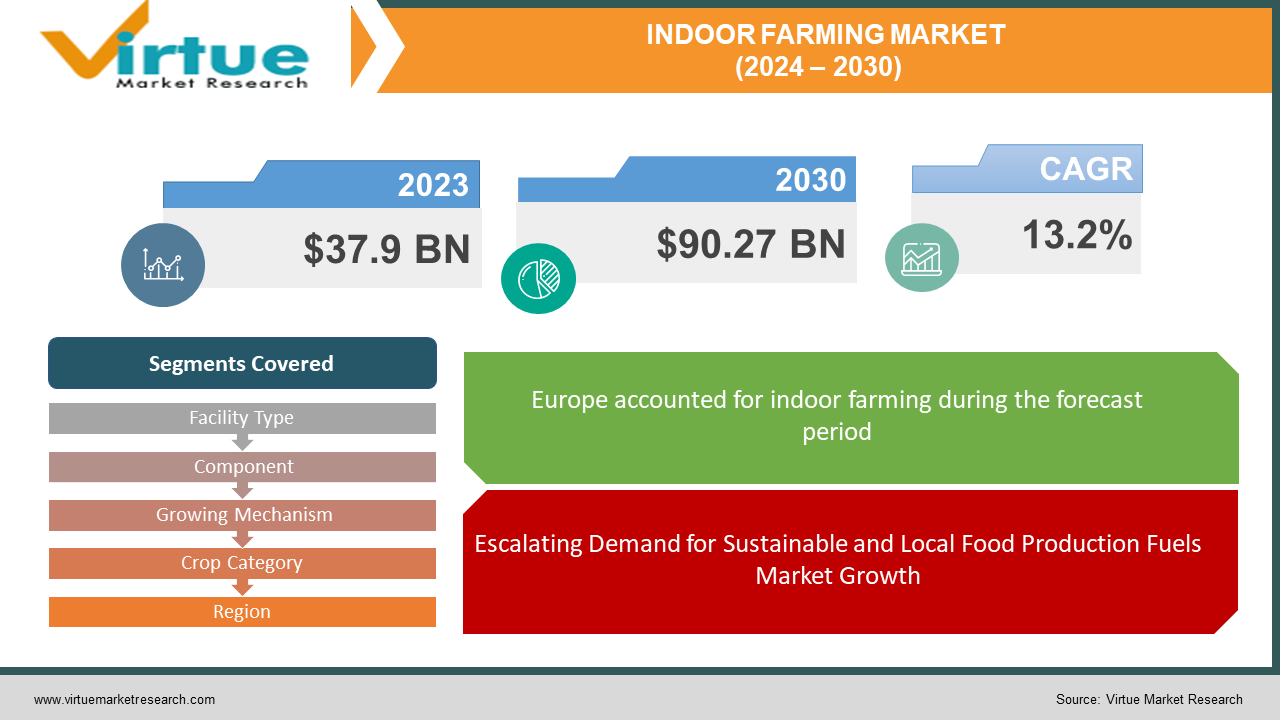

Explore reportThe Global Indoor Farming Market size was exhibited at USD 37.9 billion in 2023 and is projected to hit around USD 90.27 billion by 2030, growing at a CAGR of 13.2% during the forecast period from 2024 to 2030.

Indoor farming serves as a complementary source for the local food supply, providing consumers with fresh and nutritious vegetables. Through the regulation of plant-fertilizing nutrients, this farming method yields highly nutritious food. The versatility of indoor farming extends to the cultivation of various crops, encompassing leafy vegetables, herbs, fruits, microgreens, and flowers. Employing vertical farming techniques indoors ensures the production of organic food, free from agrochemical contamination. The increasing consumer preference for pesticide and herbicide-free produce contributes significantly to the growing demand for indoor vertical farming.

Key Market Insights:

The market is anticipated to witness growth driven by heightened consumer awareness regarding the benefits of consuming fresh and high-quality food. The global population surge, particularly in emerging economies like China and India, has resulted in an increased demand for food, thereby fostering the expansion of the indoor farming market. Nevertheless, the impact of changing climatic conditions, leading to environmental issues such as soil degradation and groundwater depletion, poses challenges to food and agriculture production systems. Governments are actively promoting indoor farming initiatives to address these challenges, anticipating a positive impact on market growth.

Organic foods are increasingly perceived as healthier, safer, and more environmentally friendly. Consumer food purchasing behavior plays a pivotal role in driving the demand for organic produce, necessitating effective marketing strategies for producers, policymakers, and suppliers. Land degradation-induced scarcity of arable land has prompted farmers to seek alternative solutions for fresh food production.

The adoption of vertical farming techniques is expected to empower indoor farm owners to cultivate crops in layers within a multi-story building, on racks, or in a warehouse. This trend is foreseen to gain significance in the market by 2030, providing a solution to the challenge of declining arable land.

Global Indoor Farming Market Drivers:

Escalating Demand for Sustainable and Local Food Production Fuels Market Growth:

The market is witnessing a surge in demand driven by the increasing preferences of individuals for sustainable and locally sourced food alternatives. A key factor contributing to market expansion is the substantial reduction in the environmental footprint associated with indoor farming compared to traditional agriculture. Traditional farming practices often involve prolonged transportation distances, excessive water consumption, and the application of pesticides and herbicides. Concurrently, the growing emphasis on local indoor farms aims to minimize the need for extended transportation routes, thereby reducing carbon emissions related to food distribution. Additionally, indoor farming offers the advantage of year-round crop production, addressing challenges posed by seasonal variations and food shortages. Regions with harsh climates or limited arable land, such as the Middle East, can decrease dependence on food imports through investments in indoor farming. The heightened focus on optimizing growing conditions, including light spectrum and nutrient delivery, allows for the customization of crops to meet specific consumer preferences, such as sweeter tomatoes or spicier peppers.

Impact of Fluctuating Climatic Conditions on Market Growth:

The market is experiencing growth driven by the minute impact of fluctuating climatic conditions. Both agricultural productivity and geographical area are influenced by climate factors. Climate change poses a threat to the integrity of global food supplies and goods. While elevated CO2 levels stimulate plant growth, they come with trade-offs in terms of crop nutrition. Changing temperatures, ozone levels, and water and nutrient constraints can counteract the positive effects of increased CO2. Overheating, inadequate water, and nutrient availability can lead to reduced crop yields. Elevated CO2 levels also contribute to decreased protein and nitrogen content in crops like alfalfa and soybeans. In this context, indoor farming emerges as a mitigating factor against climate change. The controlled environment of indoor farming provides better environmental control compared to traditional farming, resulting in water and nutrient conservation and a smaller ecological footprint. By offering protection against weather and seasonality impacts on crop yield, indoor farming supports year-round agricultural production, thereby driving market demand.

Global Indoor Farming Market Restraints and Challenges:

Substantial Initial Investments:

The pricing dynamics of indoor farming are significantly impacted by the substantial upfront investments required. The energy consumption for crop cultivation and the resultant economic production costs play a crucial role in determining the overall cost of indoor farming. Larger indoor farms allocate up to 25% of their operating budget to energy expenses, while smaller farms spend approximately 12%. The use of LED lights in indoor farming warehouses replaces natural sunlight, and controlled temperature through air conditioners and heaters adds to the initial capital outlay. Small-scale indoor farms and novice farmers often find it financially challenging to invest in essential hardware for controlling lighting, CO2 levels, nutrient reservoirs, and plumbing.

Given the energy-intensive nature of indoor farming, which necessitates artificial light, moisture, and climate control, the electricity consumption for indoor lettuce production is ten times higher per growing area than in heated greenhouses in temperate climates. The economic viability of indoor farming is further influenced by the cost of electricity, with breakeven requiring USD 3-5 per kW/h in the U.S. and even higher in Japan. Elevated electricity costs pose a hindrance to the growth of the indoor farming industry. Additionally, both small and large indoor farms incur substantial personnel costs, with vertical farming demanding significant labor. Although aeroponic farms utilize water recapture systems that reduce water usage by 95%, the installation and maintenance costs of these systems indoors are expensive, contributing to the challenges associated with high initial investments.

Global Indoor Farming Market Opportunities:

Technological Advancements:

Indoor farming presents growth opportunities, particularly with technological advancements that set it apart from conventional agricultural practices. Notably, irradiation, biosolids, and genetically modified organisms are not utilized in indoor farming, enhancing the appeal of indoor-grown crops. Consumers are willing to pay a premium for crops cultivated indoors due to their local origin, durability, safety, enhanced taste, and superior quality compared to crops from greenhouses or conventional farms. Indoor farming products have gained recognition among esteemed chefs globally, further driving the expansion of the sector.

Major companies and investors are increasingly funding indoor farming initiatives, recognizing the numerous benefits it offers. For instance, Plenty, a U.S.-based vertical farming startup, secured over USD 200 million in funding to establish a 100,000-square-foot farm. Social media trends, such as the recent surge in millennials adopting a vegan lifestyle, contribute to market growth. Reports from Rise of Vegan indicate a 33% increase in vegan food delivery options across 15 countries. This trend opens avenues for indoor farms to cater to the growing demand for vegan vegetables, expanding their market presence. Continued technological innovations, ongoing research and development, evolving consumer preferences, and substantial funding from large corporations and investors present promising opportunities for market growth in the forecast period.

INDOOR FARMING MARKET REPORT COVERAGE:

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2023 - 2030 |

|

Base Year |

2023 |

|

Forecast Period |

2024 - 2030 |

|

CAGR |

13.2% |

|

Segments Covered |

By Facility Type, Component, Growing Mechanism, Crop Category, and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regional Scope |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Key Companies Profiled |

Argus Control Systems Ltd., Certhon, Richel Group, Netafim, General Hydroponics, Hydrodynamics International, Illumitex, Lumigrow, Signify Holding, Bowery Farming Inc. |

Greenhouses

Vertical farms

Shipping Container

Building-based

Others

The vertical farm segment is poised to demonstrate the highest Compound Annual Growth Rate (CAGR) from 2024 to 2030, driven by the escalating adoption of eco-friendly production practices for fruits and vegetables. The shift in consumer food preferences, particularly the increasing demand for organic food, is expected to be a key driver for this segment. Indoor farming, employing advanced techniques like Controlled Environment Agriculture (CEA), shields crops from extreme weather conditions through controlled light, artificial environmental monitoring, and fertigation.

Farmers are embracing innovative crop production techniques, including greenhouses and vertical farming, to meet the growing demand for food. In 2023, greenhouses held the dominant market share. A greenhouse, also known as a hothouse, is an enclosed structure made of transparent materials used for cultivating plants, crops, and flowers. Greenhouses offer controlled climatic conditions to enhance the quality and quantity of produce, enabling higher yield compared to traditional farming methods.

Hardware

Climate Control Systems

Lighting Systems

Sensors

Irrigation Systems

Software

Web-Based

Cloud-Based

Services

System Integration & Consulting

Managed Services

Assisted Professional Services

The hardware segment led the indoor farming component market in 2023 and is anticipated to maintain its dominance from 2024 to 2030. Hardware plays a crucial role in maintaining the indoor farming environment, and the segment includes climate control systems, lighting systems, sensors, and irrigation systems. Climate control systems are projected to be the fastest-growing sub-segment due to their role in creating an optimal environment for plant growth.

The software segment is forecasted to exhibit a CAGR exceeding 15.4% between 2024 and 2030, driven by emerging technological trends in farming practices. The software traces the origin of fruits and vegetables, providing valuable information to consumers. This segment includes web-based and cloud-based software, with the latter expected to experience significant growth, leveraging real-time data for analysis with machine learning techniques.

Aeroponics

Hydroponics

Aquaponics

The hydroponics segment dominated the market in 2023 and is expected to continue its dominance from 2024 to 2030. Hydroponics, a cost-effective farming method, replaces soil with a mineral solution for plant root growth. It is promoted as a sustainable method, offering efficient water usage, a controlled microclimate, reduced labor requirements, and high-quality food production. Increased awareness about the impact of pesticides is likely to drive the demand for hydroponics.

The aquaponics segment is expected to experience substantial growth during the forecast period, combining elements of hydroponics and aquaculture. Aquaponics reduces the use of harmful chemicals and minimizes water wastage compared to traditional farming, making it an environmentally friendly choice.

Fruits, vegetables & herbs

Tomato

Lettuce

Bell & Chili Peppers

Strawberry

Cucumber

Leafy Greens

Herbs

Others

Flowers & ornamentals

Perennials

Annuals

Ornamentals

Others

The fruits, vegetables, and herbs segment is expected to dominate the indoor farming market between 2024 and 2030. Increased production of commonly grown items such as tomatoes, lettuce, leafy greens, cucumbers, bell peppers, and chili peppers will drive growth, with tomatoes holding the largest market share in 2023 due to their rapid production rate.

The flowers and ornamentals segment is anticipated to contribute significantly to market growth, driven by the increasing use of these items for decorative and aesthetic purposes. Ornamental Flowers held the largest market share in 2023 due to rising sales.

North America

Asia-Pacific

Europe

South America

Middle East and Africa

Europe held the largest market share in 2023 and is expected to maintain dominance due to the widespread adoption of technologies like Controlled Environment Agriculture (CEA) for indoor farms. Initiatives by regional governments and farm owners investing in technologies to improve yield and reduce labor costs contribute to this growth.

Asia-Pacific is projected to witness the fastest CAGR from 2024 to 2030, particularly in countries like China and Japan. The region's growing population has increased demand for organic food, leading to the construction of greenhouses and vertical farms. Rising awareness about alternative farming methods to address less fertile agricultural land further fuels regional demand.

COVID-19 Impact on the Global Indoor Farming Market:

The COVID-19 pandemic has significantly influenced the market, particularly in terms of sales, with more than 44% of unit sales being hindered. This obstruction is attributed to disruptions in manufacturers' transportation capabilities, stemming from stringent lockdown measures and heightened safety concerns. Additionally, supply chain disruptions, demand contraction, and shifts in customer behavior resulting from widespread lockdowns worldwide have left a lasting impact on the indoor farming market.

The pandemic has fostered a sense of skepticism regarding outside food among consumers. With the COVID-19 outbreak emphasizing health and food safety, there has been a global shift towards home cooking and self-prepared meals. Consequently, the food and hospitality industries are facing increased risks. The adverse effects of the pandemic have prompted a surge in the adoption of urban indoor farming systems worldwide.

The early stages of the pandemic posed challenges for the agriculture industry, marked by severe labor shortages on farms, missed harvesting windows for seasonal crops, declining agricultural product prices, and disruptions in logistics. Recognizing the vulnerabilities associated with excessive reliance on food imports, many countries have redirected their focus towards supporting local and indoor farming initiatives.

Recent Trends and Innovations in the Global Indoor Farming Market:

In January 2023, a strategic partnership was unveiled by Priva, establishing collaboration with Aranet. The primary objective of this partnership is to meet the increasing demand for advanced greenhouse sensors aimed at data generation. This strategic alliance is designed to bridge the gap between wireless sensor platforms and other data sources within greenhouse environments.

In October 2023, Planet Farms disclosed plans for a new facility in the Como region of Italy, set to commence operations in 2024. The brand is strategically expanding its footprint beyond Italy, with targeted countries including Norway, the Middle East, Iceland, and the United States.

In August 2023, Gotham Greens inaugurated a state-of-the-art hydroponic greenhouse in Colorado, United States. This facility, the brand's second in the state, incorporates cutting-edge technology to enhance productivity and efficiency.

In May 2022, Signify Holding made a significant announcement regarding the acquisition of Fluence. This acquisition is poised to strengthen Signify's capabilities in providing advanced indoor farming lighting solutions, reinforcing its position in the North American horticulture lighting market.

Key Players:

Argus Control Systems Ltd.

Certhon

Richel Group

Netafim

General Hydroponics

Hydrodynamics International

Illumitex

Lumigrow

Signify Holding

Bowery Farming Inc.

The Global Indoor Farming Market size is valued at USD 37.9 billion in 2023.

The worldwide Global Indoor Farming Market growth is estimated to be 13.2% from 2024 to 2030.

The Global Indoor Farming Market is segmented By Facility Type (Greenhouses, Vertical farms and Others), By Component (Hardware, Software, and Services), By Growing Mechanism (Aeroponics, Hydroponics, Aquaponics), By Crop Category (Fruits, vegetables & herbs, Flowers & ornamentals, Others).

Future trends in the Global Indoor Farming Market may include increased adoption of smart farming technologies, advanced automation, and sustainable practices. Opportunities lie in addressing food security challenges, expanding into untapped markets, and leveraging innovations to optimize resource efficiency, fostering a resilient and dynamic industry.

The COVID-19 pandemic has significantly impacted the Global Indoor Farming Market, disrupting supply chains, causing sales hindrances, and altering consumer behavior. Increased awareness of food safety and a shift towards home cooking have influenced market dynamics, leading to challenges and opportunities for the industry's future adaptation and growth.

Joining thousands of companies around the world committed to making the Excellent Business Solutions.

Specify your preferred Countries, Segments, or timeframes

Unlock Country Level Outlook, Trends, Cross-country Comparability, or supply Chain Variations.

Analyst Support

Every order comes with Analyst Support.

Customization

We offer customization to cater your needs to fullest.

Verified Analysis

We value integrity, quality and authenticity the most.