Hydrogen Aircraft Market Size (2025-2030)

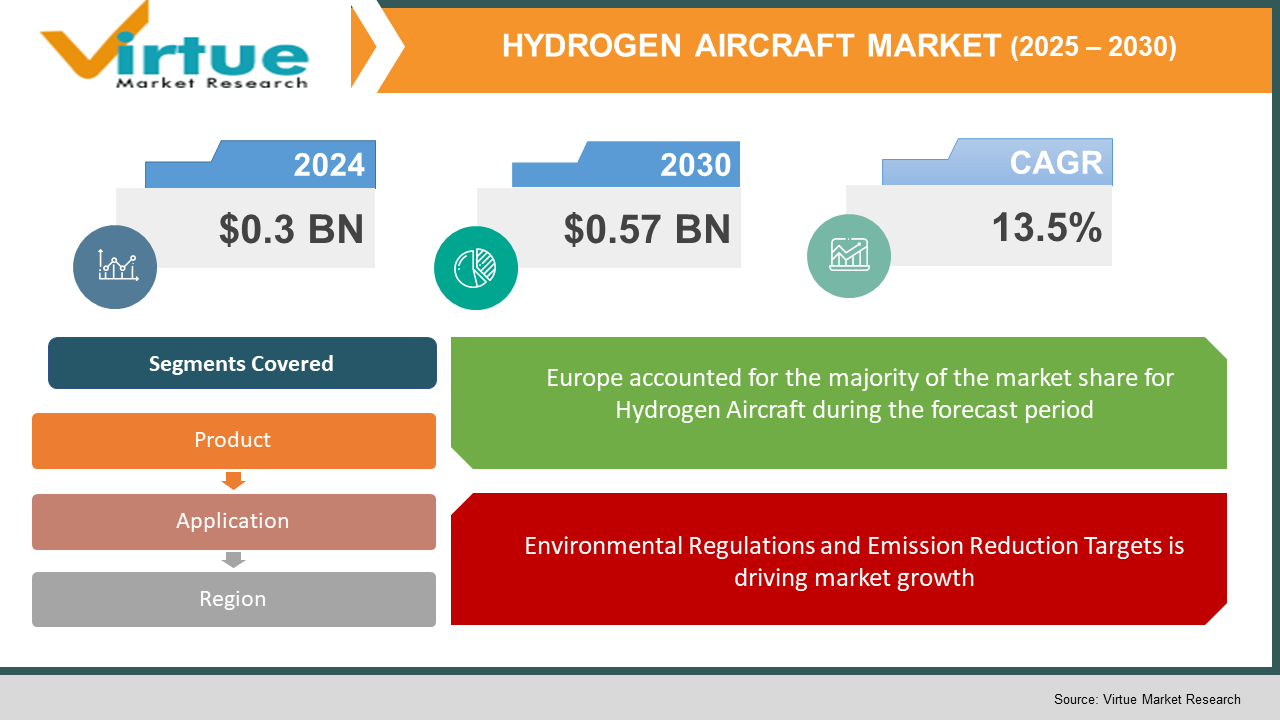

The Global Hydrogen Aircraft Market was valued at USD 0.3 billion in 2024 and is expected to grow at a CAGR of 13.5% from 2025 to 2030. The market is projected to reach USD 0.57 billion by 2030.

The Hydrogen Aircraft Market focuses on the development of aircraft powered by hydrogen as a clean fuel alternative to traditional aviation fuels. This growing market is driven by increasing concerns over the environmental impact of aviation and the need for sustainable energy solutions. Hydrogen-powered aircraft offer zero emissions during flight, making them a potential solution to reduce carbon emissions in the aviation industry, which has faced significant pressure to adopt greener technologies. With technological advancements and investments in hydrogen infrastructure, the hydrogen aircraft sector is poised to make substantial strides in the coming years.

Key Market Insights:

- Governments worldwide are making significant investments in research and development for hydrogen-powered aviation technologies, with both public and private partnerships playing a crucial role.

- Leading aircraft manufacturers are testing hydrogen propulsion systems for both commercial and military aircraft, with expected launches within the next decade.

- Hydrogen-powered aircraft could reduce greenhouse gas emissions by up to 80%, significantly contributing to the aviation sector’s environmental goals.

- The market is witnessing strong interest from both developed and developing countries, driven by the rising awareness of climate change and the need for sustainable transport solutions.

- The commercial aviation segment is anticipated to be the largest contributor to the market growth, with hydrogen aircraft offering new routes for sustainable air travel.

- The technology for hydrogen fuel cells and cryogenic storage systems is rapidly evolving, with breakthroughs expected to further enhance the feasibility of hydrogen-powered aviation.

Global Hydrogen Aircraft Market Drivers:

Environmental Regulations and Emission Reduction Targets is driving market growth:

Governments worldwide have set stringent emission reduction targets, particularly in the aviation sector, which is a major contributor to global greenhouse gas emissions. In line with the Paris Agreement and other international climate accords, there has been increasing pressure on the aviation industry to adopt cleaner technologies. Hydrogen, being a zero-emission fuel, has emerged as one of the most promising solutions to address the sector's carbon footprint. This regulatory push is a primary driver for the development and adoption of hydrogen-powered aircraft. Hydrogen aircraft have the potential to reduce carbon emissions by up to 80%, providing a significant step toward achieving carbon-neutral air travel. As global aviation regulations become stricter, the market for hydrogen aircraft is expected to grow rapidly, attracting investments from governments and private entities.

Technological Advancements in Hydrogen Fuel and Aircraft Design is driving market growth:

Advancements in hydrogen fuel production, fuel cells, and cryogenic storage technologies have created new opportunities for the aviation industry to explore hydrogen as a viable alternative to conventional fuels. These technological improvements have enhanced the efficiency of hydrogen engines and made it more feasible to incorporate hydrogen fuel into aircraft. Additionally, the development of new lightweight materials and improvements in aircraft design are making hydrogen-powered aircraft more practical for commercial use. Aircraft manufacturers, both large and small, are investing heavily in research and development to create hydrogen aircraft with longer ranges, faster refueling times, and increased passenger capacity. As technological innovations continue to reduce the cost and complexity of hydrogen-powered flight, these advancements will drive market growth, making hydrogen aircraft a more attractive option for commercial and military aviation.

Growing Demand for Sustainable Aviation Solutions is driving market growth:

The aviation industry has come under increasing scrutiny over its environmental impact, with consumers, stakeholders, and regulatory bodies demanding more sustainable solutions. With the growing focus on sustainability, the demand for green aviation technologies has surged. Hydrogen aircraft are seen as a key part of the solution to address the growing need for sustainable transportation options. Hydrogen fuel offers a cleaner alternative to traditional aviation fuels, emitting only water vapor during combustion. This offers the aviation sector a potential pathway to decarbonize and meet the rising consumer and corporate demand for sustainable travel options. Moreover, the use of hydrogen in aircraft could reduce reliance on fossil fuels and provide a renewable energy source, making it a key driver for long-term market growth.

Global Hydrogen Aircraft Market Challenges and Restraints:

High Cost of Hydrogen Production and Infrastructure Development is restricting market growth:

One of the primary challenges for the hydrogen aircraft market is the high cost associated with hydrogen production, storage, and distribution. Hydrogen is currently produced using either natural gas or electrolysis, both of which are expensive and require significant energy inputs. While the cost of hydrogen production is expected to decrease with advancements in technology and economies of scale, it remains a significant hurdle for the widespread adoption of hydrogen-powered aircraft. Additionally, developing the necessary infrastructure for hydrogen fueling stations and storage systems at airports is a massive investment that may delay the rollout of hydrogen aircraft. The cost of retrofitting existing aircraft to accommodate hydrogen fuel systems also poses a challenge, as it could require substantial financial commitments from aviation companies.

Technological Challenges in Hydrogen Storage and Safety is restricting market growth:

Hydrogen fuel requires specialized storage systems to maintain its cryogenic state at extremely low temperatures. The storage of liquid hydrogen at such low temperatures necessitates the use of advanced insulation materials and cryogenic tanks, which increase the complexity and cost of aircraft systems. Furthermore, hydrogen’s flammability and its low density make it challenging to ensure the safe storage and handling of hydrogen in aircraft. Safety concerns related to hydrogen fuel tanks, particularly in the event of accidents, must be addressed through rigorous testing, regulations, and innovations in design. While significant progress has been made in these areas, the technical challenges associated with hydrogen storage and safety remain key barriers to the widespread adoption of hydrogen-powered aircraft.

Market Opportunities:

The Hydrogen Aircraft Market is positioned to benefit from multiple opportunities over the coming years. As global pressure to reduce carbon emissions intensifies, hydrogen-powered aircraft provide a promising pathway for decarbonizing the aviation industry. Hydrogen is a clean, renewable energy source that can significantly reduce greenhouse gas emissions, a key requirement for meeting the aviation industry's sustainability goals. Moreover, hydrogen aircraft offer the possibility of significantly reducing operational costs by eliminating the need for conventional jet fuel, whose prices are subject to volatility. With advancements in hydrogen production technology and fuel cell systems, the cost of hydrogen fuel is expected to decrease, further increasing the viability of hydrogen-powered aircraft. Additionally, there is a growing interest in hybrid aircraft that combine hydrogen with traditional fuel systems, which could offer a bridge toward full hydrogen-powered flight. Strategic investments from both public and private sectors are driving technological advancements in hydrogen aircraft, with major aviation companies collaborating with energy and technology firms to develop the necessary infrastructure and systems for widespread adoption. As infrastructure development accelerates, hydrogen-powered aircraft will likely see increased adoption across both commercial and military aviation sectors. The market also offers new opportunities in the areas of hydrogen storage solutions and fuel cell technology, presenting potential growth avenues for specialized suppliers.

HYDROGEN AIRCRAFT MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2024 - 2030

|

|

Base Year

|

2024

|

|

Forecast Period

|

2025 - 2030

|

|

CAGR

|

13.5%

|

|

Segments Covered

|

By Product, application, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Airbus, Boeing, ZeroAvia, H2Fly, Rolls-Royce, and Lockheed Martin.

|

Hydrogen Aircraft Market Segmentation:

Hydrogen Aircraft Market Segmentation By Product:

- Hydrogen Fuel Cell Aircraft

- Hydrogen Combustion Aircraft

- Hybrid Hydrogen Aircraft

The hydrogen fuel cell aircraft segment is expected to dominate the market due to the significant advancements in fuel cell technology, offering a clean and efficient power source for aircraft. Hydrogen fuel cells are an ideal fit for smaller aircraft and regional flights, where their compact size and efficiency can provide substantial benefits. Furthermore, fuel cells have a proven track record in other transportation sectors, enhancing their potential for use in aviation. As hydrogen fuel cell technology matures and becomes more cost-competitive, it is anticipated to lead the hydrogen aircraft market in the coming years.

Hydrogen Aircraft Market Segmentation By Application:

- Commercial Aviation

- Military Aviation

- Cargo Aircraft

The commercial aviation segment is anticipated to be the most dominant in the hydrogen aircraft market. The high volume of air travel and the industry's growing commitment to sustainability make commercial aviation the most promising application for hydrogen-powered aircraft. Airlines are increasingly investing in green technologies to meet emission reduction targets, and hydrogen aircraft offer a viable solution. The need for long-range, high-capacity aircraft for commercial use also positions the commercial aviation sector to be the major driver of hydrogen aircraft adoption, as manufacturers develop larger and more efficient hydrogen-powered aircraft for passenger travel.

Hydrogen Aircraft Market Regional Segmentation:

- North America

- Asia-Pacific

- Europe

- South America

- Middle East and Africa

Europe is currently the dominant region in the hydrogen aircraft market. This can be attributed to the region’s strong commitment to reducing carbon emissions and its supportive regulatory environment for green technologies. European Union policies, such as the European Green Deal, have set ambitious targets to achieve net-zero emissions by 2050, and the aviation sector is a significant part of these efforts. European aircraft manufacturers, such as Airbus, are leading the development of hydrogen-powered aircraft, further strengthening the region's position in the market. Moreover, countries like Germany, France, and the UK are heavily investing in hydrogen infrastructure, making the region a hub for innovation and adoption in the hydrogen aircraft industry.

COVID-19 Impact Analysis on the Hydrogen Aircraft Market:

The COVID-19 pandemic has significantly impacted the global aviation industry, with widespread travel restrictions, reduced demand for air travel, and financial instability. As a result, the hydrogen aircraft market faced delays in development and deployment plans, as companies focused on recovering from the pandemic's financial fallout. However, the crisis has also accelerated the need for more sustainable aviation solutions, as environmental concerns remain a priority in the post-pandemic recovery phase. Governments are increasingly looking toward green recovery programs, and the hydrogen aircraft market is seen as an opportunity to promote innovation while reducing environmental impact. Although the pandemic disrupted supply chains and delayed some projects, it has also prompted renewed interest in sustainable aviation technologies, and hydrogen aircraft are expected to play a crucial role in the future of air travel.

Latest Trends/Developments:

Several recent developments in the hydrogen aircraft market highlight the industry's progress. Major aircraft manufacturers, including Airbus and Boeing, have announced plans to develop hydrogen-powered aircraft, with test flights expected within the next decade. Additionally, new collaborations between aviation companies, energy firms, and governments are advancing the development of hydrogen infrastructure, including hydrogen refueling stations at airports. The use of hydrogen in hybrid aircraft is another key trend, with several companies working on designs that integrate both hydrogen fuel cells and traditional propulsion systems to extend range and improve operational efficiency. Furthermore, technological advancements in hydrogen storage systems, such as cryogenic tanks and lightweight composites, are expected to increase the feasibility of hydrogen-powered flight. The ongoing research and development in hydrogen propulsion and fuel technology will continue to shape the future of the hydrogen aircraft market.

Key Players:

- Airbus

- Boeing

- ZeroAvia

- H2Fly

- Universal Hydrogen

- Rolls-Royce

- Safran

- Hyundai Motor Group

- Lockheed Martin