HVAC Renewable Materials Market Size (2023 – 2030)

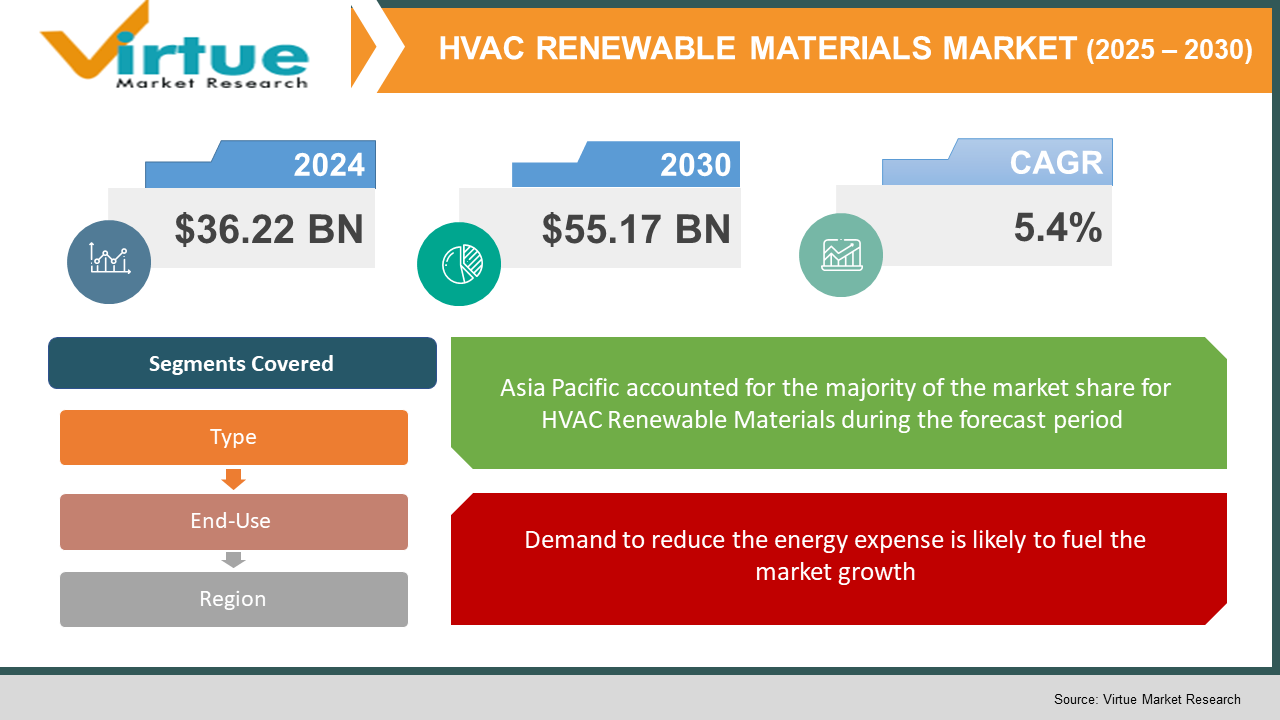

In 2022, the Global HVAC Renewable Materials Market was valued at $36.22 Billion and is projected to reach a market size of $55.17 Billion by 2030. Over the forecast period of 2023-2030 market is projected to grow at a CAGR of 5.4 %. The rise in market revenue is being driven by the rising desire to lower energy costs and enhance energy efficiency. Renewable HVAC systems are becoming more popular as a result of increased emphasis on energy conservation brought on by worries about climate change and rising oil and gas costs.

INDUSTRY OVERVIEW:

To achieve emission-reduction targets, environmental engineers are working with others to create sustainable technology. To protect natural resources and the global ecology, governments are also developing sustainability goals. By developing renewable energy sources, nations are reducing the carbon footprint of their electricity infrastructures. The use of renewable energy is significantly altering how we live our everyday lives and having an effect on several economic sectors. The HVAC sector could be one of those most severely affected, in part because of how much energy HVAC systems use. The HVAC sector and the systems it relies on are changing as a result of renewable energy sources. The way HVAC systems function, the knowledge needed to use them, and the effects they have on our lives and the environment all evolve along with technology. The ability to utilise renewable HVAC equipment efficiently prevents people from irrationally misusing energy when cooling or heating buildings. Energy-efficient heating, ventilation, and air-conditioning (HVAC) systems are those that perform equally well as traditional HVAC systems while utilising fewer energy sources to operate.

COVID-19 IMPACT ON THE HVAC RENEWABLE MATERIALS MARKET

The outbreak of COVID-19 has significantly impacted the economy across the globe. It resulted in workforce & travel restrictions, supply chain disruptions, and a reduction in demand & spending across different sectors. Many device manufacturing companies had to shut down their manufacturing facilities as partial or full lockdown was imposed across regions. A sudden decline was observed in infrastructure development and installation projects. The construction market witnessed an abrupt downturn during the covid-19 crisis. The shortage of materials and electronics components has a significant impact on the global supply chain. Delays in planned projects and reductions in capital budgets have hampered the global economy. The key players in the renewable HVAC system market faced a slight negative impact from the covid-19 crisis as compared to other industries. The decline in business activities has negatively impacted the renewable HVAC system market in the short term. A slow recovery is anticipated in the post-pandemic period.

MARKET DRIVERS:

The growing construction industry is propelling the market growth:

Due to increased infrastructure investment and rising disposable incomes in major nations, the market for Renewable HVAC equipment is fast developing. Climate change is a significant influence on the rising demand for HVAC systems worldwide. Due to the rising temperatures and unpredictability of the weather, many consumers view HVAC equipment as a wise investment. Additionally, a rise in customer comfort preferences has boosted demand for renewable HVAC systems.

Demand to reduce the energy expense is likely to fuel the market growth:

One of the key elements that will positively affect the worldwide market for energy-efficient renewable HVAC systems during the projected period is the need to lower energy usage and operating expenses. A variety of heating, cooling, and climate management systems are used in a large number of residential, commercial, and industrial buildings across the world to provide thermal comfort and acceptable levels of indoor air quality. The excessive energy usage for heating and cooling in buildings drives up operating expenses for the owner or operator. The need for energy-efficient renewable HVAC systems will increase in response to the rising need to lower building energy consumption rates and operational costs.

Growing government initiatives toward building renewable sources of energy are creating lucrative opportunities for the market:

Governments play a major role in supporting initiatives toward energy savings, the construction of smart buildings, and transforming infrastructures. Several regulations and policies have been formulated by the government to improve energy efficiency and reduce a building’s footprint on renewable energy, lighting, and HVAC. Increased investments in the digitalization of the grid by the implementation of advanced communication technologies will propel the home energy management system market growth.

MARKET RESTRAINTS:

The cost for setting up and maintenance of the renewable HVAC system is on the higher side which is hampering the wide adoption of the system:

The high cost for the setup and installation of renewable HVAC systems is acting as a barrier to market development. Renewable HVAC system comprises expensive equipment. There are expenses connected with implementing and maintaining renewable HVAC systems which furthermore increases the cost. Moreover, these systems require regular maintenance and checkup for smooth functioning which further increases the input cost which is not favourable for many consumers.

Lack of awareness among the public and consumers regarding the various benefits and shortage of workforce in the BEMS sector is negatively affecting the market growth.

Many people and industries are not aware of the benefits of the building energy management system and do not implement renewable HVAC systems in their homes. Moreover, a skilled workforce is required for the installation of the system. The engineers analyse the system parameters and configure them to the optimum uses. As there is a shortage of skilled labour in the market it is acting as a major factor decelerating the market growth

HVAC RENEWABLE MATERIALS MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2022 - 2030

|

|

Base Year

|

2022

|

|

Forecast Period

|

2023 - 2030

|

|

CAGR

|

5.4%

|

|

Segments Covered

|

By Type, By End-Use and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Apollo America, Azbil, Belimo, Daikin Industries, Delta Controls, Distech Controls Emerson Electric, Honeywell, ICM Controls Ingersoll-Rand, Jackson Systems, Johnson Controls, KMC Controls, Lennox, LG Electronics, PECO, Sauter, Schneider Electric

|

This research report on the HVAC Renewable Materials Market has been segmented and sub-segmented based on Type, By End-Use and By Region.

HVAC RENEWABLE MATERIALS MARKET – BY TYPE

Based on the end-use, the HVAC renewable market is segmented into Geothermal Heat Pumps, Solar HVAC Systems, Hydronic Heating Technology, Ice-Powered AC Units and Wind Power Heaters. Among these, the most popular renewable HVACAc system was Geothermal Heat Pumps. During this transitional period, green electricity becomes the norm. Utilizing geothermal energy is one ecological heating and cooling technique. Geothermal heat pumps are the go-to sustainable heating option for the majority of house and building owners. To store and transfer heat, these systems rely on the regular subsurface temperatures of the planet. The core of the Earth is considerably warmer than the surface. To generate heat naturally, geothermal heaters circulate a refrigerant through subsurface pipes. The cost of using electricity is reduced by the sustainable heating technology's high-efficiency rate. The carbon footprints of geothermal heat pumps are one issue for the environment. The construction process exposes subterranean climates to the Earth's surface, and these climates emit a limited amount of sulphur dioxide and carbon dioxide into the atmosphere. As a result of their lower carbon footprint, geothermal heat pumps continue to be more environmentally friendly than traditional HVAC systems.

The Solar HVAC system was also among the most popular ones in the year 2021. The inherent feature is that HVAC systems may be directly powered by solar energy, reducing emission pollution is driving the market. Photovoltaic (PV) panels are used in the green heating and cooling system to produce electricity and regulate interior temperatures. PV panels have an efficiency range of 15% to 22%. By producing electricity with no emissions, PV panels improve the sustainability of a structure. The technology is reasonably priced and enables users to reduce their recurring electricity costs. Building owners only need three to six years to recover their original investment in PV panels. Over time, they may sell any extra power back to the grid and generate a passive income.

The United States and other developed nations have high sustainability objectives. Wind energy is being used by America to decarbonize its electricity system, and it may also be used by individuals to meet their needs for HVAC power. Utilizing little windmills, environmental engineers created wind-powered heaters. They attach to a heat source and release heat into a radiator. Wind-powered heaters warm a structure without emitting any pollution.

HVAC RENEWABLE MATERIALS MARKET - BY END-USE

-

Residential

-

Commercial

-

Industrial

Based on the end-use, the HVAC renewable market is segmented into Residential, Commercial and Industrial. Among these, with a revenue share of 40.1 % in 2021, the residential sector dominated the market for renewable HVAC systems. A growing number of multi-family dwellings and single-family homes are opening up opportunities for the residential renewable HVAC market. As a result, the segment's estimated value in 2021 was significantly high. The demand for home HVAC (Heating, ventilation, and air conditioning) is anticipated to remain more or less stable in established regions of the world, while it will be somewhat greater in developing regions. This is mostly attributed to the expanding populations in developing countries and the maturing markets in industrialised countries, as well as to increased public awareness of climate change and rising demand for lower energy prices.

Commercial renewable HVAC space has a tonne of expansion potential. From 2023 - 2030, the category is anticipated to see a CAGR of over 6.0 % in the renewable HVAC systems market. The future of the commercial renewable HVAC industry is anticipated to be significantly shaped by several trends, from automated systems to green and smart technologies. The need for renewable HVAC systems in business settings is predicted to rise as the COVID-19 pandemic turns endemic and permanent WFH models gradually switch to a hybrid operating paradigm.

HVAC RENEWABLE MATERIALS MARKET - BY REGION

-

North America

-

Europe

-

The Asia Pacific

-

Latin America

-

The Middle East

-

Africa

By region, the HVAC Renewable Materials Market is grouped into North America, Europe, Asia Pacific, Latin America, The Middle East and Africa. Asia Pacific dominated the market for renewable HVAC systems in 2021, with a revenue share of more than 40.0 %. The region has experienced enormous growth throughout the years due in large part to expanding urbanisation, population expansion, and rising consumer disposable income. The commercial sector has recently grown, creating opportunities for possible regional expansion in the future. In 2021, North America was the second-largest customer of releasable HVAC systems, closely followed by Europe. The market for HVAC systems as a whole has matured, but replacement sales prompted by ageing infrastructure or retrofit projects are generating new sources of income for OEMs in addition to their growth in the services and maintenance sector. Over the projection period, the area is estimated to see a CAGR of more than 5.5 %.

HVAC RENEWABLE MATERIALS MARKET - BY COMPANIES

Some of the major players operating in the HVAC Renewable Materials Market include:

- Apollo America

- Azbil

- Belimo

- Daikin Industries

- Delta Controls

- Distech Controls

- Emerson Electric

- Honeywell

- ICM Controls

- Ingersoll-Rand

- Jackson Systems

- Johnson Controls

- KMC Controls

- Lennox

- LG Electronics

- PECO

- Sauter

- Schneider Electric

NOTABLE HAPPENING IN THE HVAC RENEWABLE MATERIALS MARKET

- PRODUCT LAUNCH- Johnson Controls introduced wrap-around heat exchangers (WAHX) to its YORK Solution Indoor and Outdoor air-handling systems in February 2020. These exchangers are completely integrated, factory-built, and installed. This newly created item will assist the business in satisfying the rising need for small-footprint, energy-efficient dehumidification techniques.

- PRODUCT LAUNCH- Grande Heavy-Duty Air Conditioner was introduced in February 2020 by Havells India Ltd. The air quality is improved with the AC's catechine-coated dust filter, Green Bio air filter, and antibacterial Eva Coils.

- MERGER- March 2020 - 2020, Gardner Denver finalized the merger with the Industrial division of Ingersoll Rand. The newly combined business, now known as Ingersoll Rand Inc. With a wider range of products, the newly combined business will significantly dominate the market for industrial technology and mission-critical flow management.