GLOBAL HIGH-ENTROPY ALLOY MARKET (2024 - 2030)

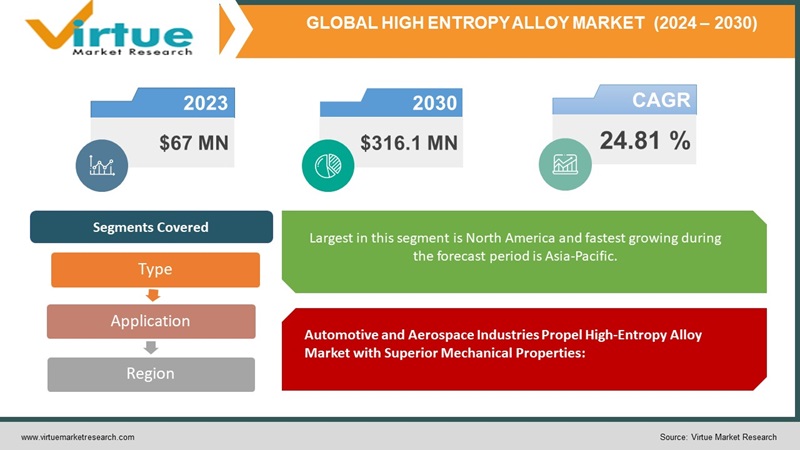

The High-Entropy Alloy Market was valued at USD 67 million in 2023 and is projected to reach a market size of USD 316.1 million by the end of 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 24.81%.

The High-Entropy Alloys (HEA) market has witnessed significant evolution over the years. In its initial stages, HEAs were primarily explored for their unique composition featuring multiple elements in roughly equal proportions, offering enhanced mechanical and thermal properties. Research primarily focused on understanding the fundamental science behind these alloys. There's a notable shift towards practical applications, with HEAs gaining traction in industries such as aerospace, automotive, and energy due to their exceptional strength and corrosion resistance. The HEA market is poised for sustained growth as ongoing research seeks to optimize compositions for specific applications, and industries increasingly recognize the transformative potential of these alloys in pushing the boundaries of material science and engineering. The evolution of the High-Entropy Alloys market reflects a trajectory from exploration and understanding to practical utilization, with a promising outlook for continued advancements and widespread industrial adoption.

Key Market Insights:

High-Entropy Alloys (HEAs) are gaining attention for potential use in core cladding in nuclear reactors due to their resistance to neutron radiation. This unique resistance arises from the composition of HEAs, combining multiple elements in roughly equal proportions to disrupt the movement of dislocations within the crystal lattice, enhancing their durability in nuclear reactor environments.

In terms of market share, North America leads the High-Entropy Alloy market, holding 37.07% in 2022. This dominance is supported by a robust nuclear energy infrastructure, extensive R&D initiatives, and a strong presence of industry players, reflecting a growing demand for HEAs in advancing nuclear technologies.

Sandvik, a major industry player specializing in mining, rock excavation, and material technology, holds a substantial 29.57% market share in 2022. Their expertise in producing high-quality HEAs tailored for demanding applications, coupled with a commitment to innovation, positions Sandvik as a key contributor to the High-Entropy Alloy market.

Projections indicate a strong growth trajectory for the High-Entropy Alloy market, with an anticipated 24.81% CAGR over the next seven years, reaching a valuation of USD 0.31 billion by 2030. This optimistic outlook is driven by the increasing adoption of HEAs in various industrial sectors, ongoing R&D efforts to enhance alloy properties, and rising demand for materials with exceptional mechanical and thermal performance.

High-Entropy Alloy Market Drivers:

Automotive and Aerospace Industries Propel High-Entropy Alloy Market with Superior Mechanical Properties:

The high-entropy alloy market is experiencing a substantial boost propelled by heightened demand from the automotive and aerospace industries, a surge attributed to the extraordinary mechanical properties inherent in high-entropy alloys. These alloys, renowned for their exceptional strength, hardness, and wear resistance, have become indispensable materials in the production of high-performance vehicles and aircraft. Their ability to withstand extreme conditions and provide superior mechanical performance positions high-entropy alloys at the forefront of material innovation, contributing significantly to advancements in automotive engineering and aerospace technology.

Biomedical Revolution - High-Entropy Alloys Excel with Biocompatibility and Corrosion Resistance:

A revolutionary transformation is underway in the high-entropy alloy market as these advanced materials gain substantial traction in biomedical applications. This surge in adoption is attributable to the remarkable biocompatibility and resistance to corrosion exhibited by high-entropy alloys. With the healthcare industry increasingly seeking materials compatible with the human body and capable of withstanding physiological conditions, high-entropy alloys have emerged as game-changers. Their deployment in medical device manufacturing and implant technologies signifies a paradigm shift in the biomedical sector, promising enhanced longevity and performance of healthcare products.

Lightweight Solutions - High-Entropy Alloys Meet Growing Demand in Construction and Engineering:

As the demand for lightweight yet high-strength materials escalates in the construction and engineering sectors, high-entropy alloys have emerged as pivotal contributors to this evolving landscape. These alloys, distinguished by their low density and exceptional mechanical strength, offer an innovative solution to the industry's quest for efficiency and sustainability. Architects and engineers are increasingly turning to high-entropy alloys in the design and construction of structures and components, recognizing their potential to redefine the standards for structural materials in the pursuit of durable, lightweight, and environmentally conscious solutions.

Research and Development Drive Innovation, Unleashing the Potential of High-Entropy Alloys:

The high-entropy alloy market is witnessing a transformative era fueled by a relentless focus on research and development initiatives. This concerted effort aims to unlock the full potential of high-entropy alloys by creating new variants with enhanced properties, including improved thermal stability and corrosion resistance. This wave of innovation is not only pushing the boundaries of material science but also shaping the future of technological breakthroughs. High-entropy alloys are poised to play a central role in pioneering advancements, reflecting a commitment to continuous improvement and excellence in materials innovation.

High-Entropy Alloy Market Restraints and Challenges:

Uncharted Territory - Navigating Restraints and Challenges in the High-Entropy Alloy Market:

The High-Entropy Alloy (HEA) market, while promising, faces a set of distinctive challenges that underscore the complexities inherent in harnessing the full potential of these advanced materials. One primary restraint revolves around the intricate nature of alloy compositions, with the requirement for a specific balance among multiple elements. Achieving this balance poses a significant technical challenge and can impede the scalability of production. Moreover, the relative novelty of HEAs in practical applications necessitates extensive testing and validation, contributing to a slower adoption rate. Another critical challenge is the cost dynamics associated with raw materials. The dependence on diverse elements, coupled with fluctuations in metal prices, makes the manufacturing cost of HEAs susceptible to market volatility. Additionally, environmental regulations impacting metal extraction processes introduce uncertainties in the raw material supply chain, further influencing the overall cost structure. Furthermore, while HEAs exhibit resistance to neutron radiation, their long-term performance and behavior in nuclear environments require rigorous evaluation. As the industry strives to overcome these hurdles, addressing alloy optimization, production scalability, and cost considerations will be pivotal in realizing the transformative potential of High-Entropy Alloys across diverse applications.

High-Entropy Alloy Market Opportunities:

The High-Entropy Alloy (HEA) market is poised for dynamic growth with a spectrum of opportunities emerging on the horizon. The unique properties of HEAs, such as exceptional strength, corrosion resistance, and thermal stability, present avenues for applications in diverse industries. The burgeoning demand for lightweight yet high-strength materials in aerospace, automotive, and construction sectors positions HEAs as a key player in meeting evolving industry needs. Furthermore, the increasing focus on sustainable technologies propels the use of HEAs in renewable energy and eco-friendly applications. Ongoing research and development activities to optimize alloy compositions and enhance performance further open doors to novel applications. As industries increasingly recognize the versatile attributes of HEAs, the market is primed for expansion and innovation, paving the way for transformative advancements in materials science and engineering.

GLOBAL HIGH-ENTROPY MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2022 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

24.81%

|

|

Segments Covered

|

By Type, Application and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Heeger Materials, Sandvik AB, QuesTek Innovations LLC, Carpenter Technology Corporation, Alcoa Corporation, Norsk Titanium AS, Allegheny Technologies Incorporated (ATI), POLEMA, Oerlikon, Metalysis

|

High-Entropy Alloy Market Segmentation:

Market Segmentation: By Type:

- 5 Base Metals

- Above 5 Base Metals

Largest in this segment is 5 Base Metals and fastest growing during the forecast period is Above 5 Base Metals. The appeal of this segment lies in its relatively simpler composition, which allows for more straightforward manufacturing processes and potentially lower production costs. This simplicity makes it attractive to industries seeking the unique properties of HEAs without the complexities associated with higher base metal compositions. The HEA within Above 5 base offers a spectrum of enhanced properties, making it particularly appealing for advanced applications in aerospace, defense, and high-tech industries. The increased demand for intricate alloys with superior mechanical and thermal characteristics is expected to drive the rapid growth of this segment as industries seek cutting-edge materials for their evolving needs.

Market Segmentation: By Application:

- Mechanical

- Electrical

- Magnetic

- Aerospace

- Automotive

- Energy

- Biomedical

Largest in this segment is Mechanical Application and fastest growing during the forecast period is Electrical. The Mechanical segment is driven by the robust demand for HEAs in industries such as aerospace and automotive. The unique mechanical properties of HEAs, including exceptional strength and wear resistance, position them as ideal materials for manufacturing components subjected to mechanical stress. The increasing adoption of HEAs in electrical components, such as conductors and connectors, is fueled by their favorable electrical conductivity and corrosion resistance. The magnetic applications segment is also poised for growth, benefiting from the magnetic properties of certain HEAs, making them suitable for applications in electronics and magnetic devices. The diverse applications of HEAs across mechanical, electrical, and magnetic domains underscore their versatility and contribute to the market's sustained growth.

Market Segmentation: Regional Analysis:

- North America

- Asia-Pacific

- Europe

- Latin America

- Middle East and Africa

Largest in this segment is North America and fastest growing during the forecast period is Asia-Pacific. The well-established research and development infrastructure in North America, particularly in the United States, contributes to its dominance, fostering innovation and early adoption of HEAs across diverse industries. Asia-Pacific region is propelled by rapid industrialization and increasing investments in aerospace, automotive, and energy sectors in countries like China and Japan. The burgeoning demand for lightweight yet high-strength materials in these regions, coupled with a growing emphasis on sustainable technologies, positions HEAs as integral to technological advancements. Europe follows closely, benefiting from a robust aerospace and automotive sector, while Latin America and the Middle East and Africa exhibit steady growth, driven by infrastructure development and a rising focus on advanced materials. The unique properties of HEAs, coupled with regional economic dynamics, contribute to a varied but promising landscape for High-Entropy Alloys across the globe.

COVID-19 Impact Analysis on the High-Entropy Alloy Market:

The High-Entropy Alloy (HEA) market experienced notable impacts due to the COVID-19 pandemic. The global disruption in supply chains, coupled with temporary shutdowns in manufacturing facilities, led to a slowdown in the production and adoption of HEAs. The automotive and aerospace industries, major consumers of HEAs, faced challenges amidst decreased demand and operational constraints. However, the pandemic also underscored the significance of lightweight and resilient materials, potentially driving renewed interest in HEAs for their unique properties. As the world gradually recovers and industries regain momentum, the High-Entropy Alloy market is poised for a resurgence, with the lessons learned from the pandemic highlighting the importance of advanced materials in ensuring resilience and adaptability in various sectors.

Latest Trends/ Developments:

Recent trends in the global high-entropy alloy market underscore a growing adoption across industries driven by the alloys' exceptional mechanical and physical properties. There is an increasing demand for lightweight, strong, and durable materials, particularly in the aerospace, automotive, and energy sectors. The market is witnessing a surge in research and development efforts, focusing on exploring novel alloy compositions and manufacturing techniques to further enhance the capabilities of high-entropy alloys. The integration of advanced technologies such as additive manufacturing is gaining prominence, offering increased design flexibility and customization options. These trends collectively reflect a dynamic landscape where high-entropy alloys continue to evolve and find diverse applications across cutting-edge industries.

Key Players:

- Heeger Materials

- Sandvik AB

- QuesTek Innovations LLC

- Carpenter Technology Corporation

- Alcoa Corporation

- Norsk Titanium AS

- Allegheny Technologies Incorporated (ATI)

- POLEMA

- Oerlikon

- Metalysis

- July 2022: Sandvik, a leading participant in the High-Entropy Alloy sector, possessed a notable market share of 29.57%. With expertise in mining, rock excavation, and material technology, Sandvik's considerable presence highlights its impact and meaningful contribution to the broader industry.

Sep 2022: Scientists have identified a novel mechanism for enhancing both the strength and ductility of high-entropy alloys. These discoveries offer crucial insights for shaping the future development of robust yet flexible high-entropy alloys and high-entropy ceramics.