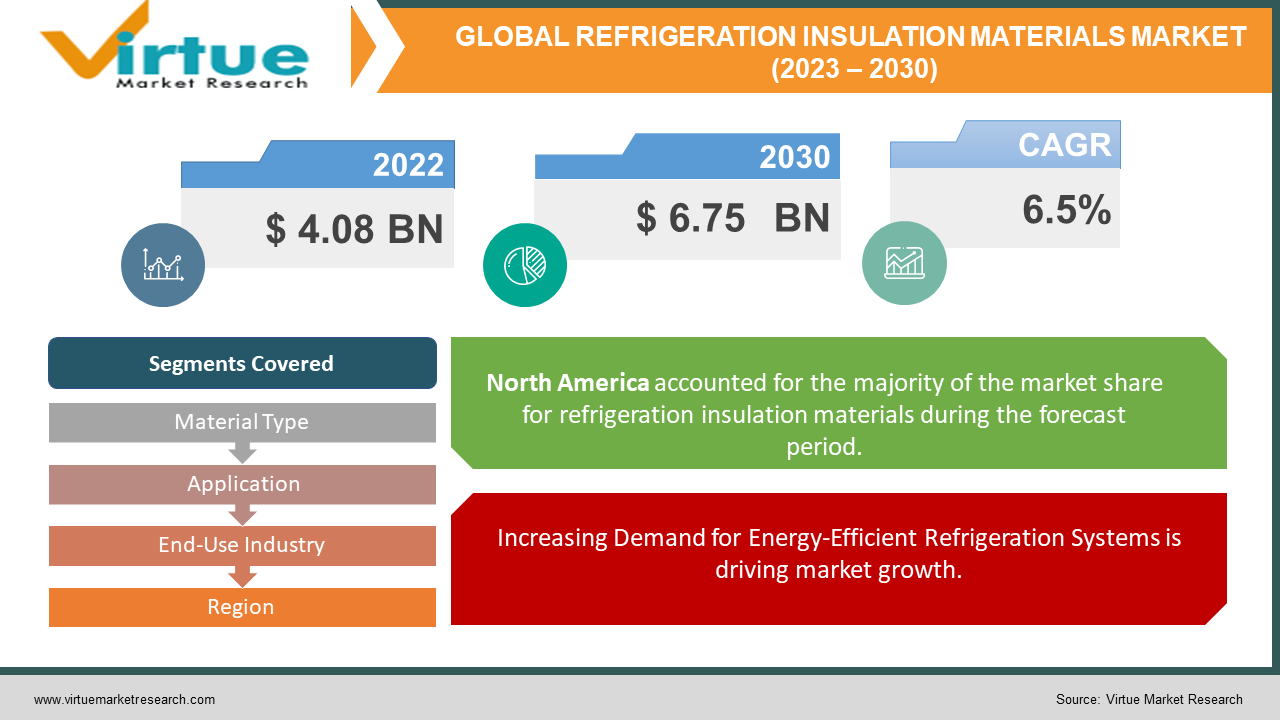

Refrigeration Insulation Materials Market Size (2023 – 2030)

Global Refrigeration Insulation Materials Market is estimated to be worth USD 4.08 Billion in 2022 and is projected to reach a value of USD 6.75 Billion by 2030, growing at a CAGR of 6.5% during the forecast period 2023-2030.

The refrigeration insulating materials market is critical to preserving refrigeration systems’ energy efficiency and performance. These materials are used to keep refrigerators and freezers at low temperatures by preventing heat transmission. They are critical components that contribute to the overall efficiency and longevity of refrigeration units. As a result of factors such as increased demand for energy-efficient refrigeration systems, arising environmental concerns, and stringent energy consumption legislation, the global refrigeration insulating materials market has grown quickly in recent years. These factors have driven manufacturers to create insulating materials that provide better thermal performance while using less energy and emitting fewer greenhouse gases. The refrigeration insulating materials market is progressively developing as a consequence of increased demand for energy-efficient refrigeration systems, environmental limitations, and the escalation of several sectors. The most prevalent insulating materials used in refrigeration applications are polyurethane foam and polystyrene foam, however natural and ecological alternatives are gaining popularity. With a propelling focus on sustainability and energy efficiency, the market is projected to see more breakthroughs in insulation materials that fit the changing needs of the refrigeration sector.

Global Refrigeration Insulation Materials Market Drivers:

Increasing Demand for Energy-Efficient Refrigeration Systems is driving market growth

The rising demand for energy-efficient refrigeration systems is driving the global refrigeration insulation materials market. As energy consumption remains a major concern, enterprises are looking for solutions to reduce their carbon footprint and optimize energy utilization. Energy-efficient refrigeration systems contribute to these objectives by reducing energy usage and operational expenses. Insulation materials are essential in improving the energy efficiency of refrigeration systems. Polyurethane foam and polystyrene foam, for example, have excellent thermal insulation capabilities, limiting heat transfer and maintaining low temperatures within refrigerators and freezers. Manufacturers can increase the total energy efficiency of refrigeration systems by employing high-performance insulating materials, resulting in lower energy consumption and lower greenhouse gas emissions. Furthermore, governments and regulatory agencies around the world are enforcing strict energy efficiency norms and restrictions for refrigeration systems. Compliance with these standards mandates the use of efficient insulation materials, which drives market demand for refrigeration insulation materials.

The Growing Importance of Sustainable and Environmentally Friendly Solutions is boosting demand and expanding the market

The arising relevance of ecologically friendly and sustainable solutions is a primary driver for the refrigeration insulating materials industry. With growing environmental concerns and the need to minimize carbon emissions, companies are actively looking for insulation materials that provide outstanding performance while having the least environmental impact. In the refrigeration business, natural and renewable insulating materials such as aerogel, cellulose, and cork are gaining appeal. These materials have high thermal insulation capabilities and are biodegradable and renewable, making them a sustainable alternative to standard insulation materials. The usage of these materials reduces reliance on non-renewable resources while also reducing waste output. Furthermore, consumer and industry demand for ecologically friendly refrigeration systems is increasing. Retailers, supermarkets, and food service providers are increasingly emphasizing sustainability programs and environmentally friendly operations. Using insulating materials that match these goals helps businesses fulfill their sustainability goals while also improving their brand image. Furthermore, government rules and programs promoting environmentally friendly practices in a variety of industries, including refrigeration, are boosting the adoption of environmentally friendly insulation materials. Manufacturers are investing in R&D to develop sustainable insulating solutions to meet the rising market demand for eco-friendly refrigeration systems.

Global Refrigeration Insulation Materials Market Challenges:

Pricing and availability of alternative insulating materials are significant concerns in the global refrigeration insulation materials business. While natural and sustainable insulating materials like aerogel, cellulose, and cork are environmentally friendly, they can be more expensive than standard materials such as polyurethane foam and polystyrene foam. These alternative materials production techniques may be more complex and necessitate the use of specialist equipment, resulting in higher costs. Alternative insulation materials may also be scarce, particularly in some areas. The infrastructure and supply chains required for mass manufacturing and distribution of these materials may be insufficient, limiting their availability and price. To encourage the widespread adoption of sustainable technologies, pricing, and availability barriers must be overcome.

Global Refrigeration Insulation Materials Market Opportunities:

In the worldwide refrigeration insulating materials market, technological advancements present a substantial opportunity. Continuous research and development activities result in the introduction of new insulation materials with improved thermal properties, lower environmental effects, and improved manufacturing methods. Nanotechnology-based insulation, for example, has the potential to revolutionize the market by improving insulation performance and durability. Technological advancements enable manufacturers to differentiate themselves and meet the arising need for high-performance, long-term insulating solutions in the refrigeration industry.

COVID-19 Impact on Global Refrigeration Insulation Materials Market:

The COVID-19 pandemic has raised public awareness of the importance of cleanliness and food safety, fuelling demand for refrigeration equipment in the healthcare and food industries. This increase in demand has helped the refrigeration insulation materials market indirectly, as insulation materials are critical components of refrigeration systems. The industry has the potential to provide insulation materials for new installations and modifications due to the requirement for reliable and effective cold storage for vaccinations, pharmaceuticals, and perishable food items. The pandemic has also presented difficulties for the refrigerator insulating materials business. The availability and timely delivery of insulating materials have been disrupted by supply chain interruptions, reduced industrial operations, and logistical difficulties. Furthermore, the economic crisis and decreased investment in numerous industries have impacted the overall demand for refrigeration systems and, as a result, the demand for insulation materials. Market uncertainty and end-user financial constraints have hindered new installations and projects, limiting the market's growth potential.

Global Refrigeration Insulation Materials Market Recent Developments:

In January 2020, Cabot China Limited, a subsidiary of Cabot Corporation, agreed to pay about $115 million for Shenzhen Sanshun Nano New Materials Co., Ltd (SUSN). In China, SUSN is a major manufacturer of carbon nanotubes. This strategic initiative will strengthen Cabot's market presence and formulation skills in the rapidly increasing battery sector, particularly in China's booming electric car market, which is the world's largest.

REFRIGERATION INSULATION MATERIALS MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2022 - 2030

|

|

Base Year

|

2022

|

|

Forecast Period

|

2023 - 2030

|

|

CAGR

|

6.5%

|

|

Segments Covered

|

By Material Type, Application, End-Use Industry, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Armacell, Owens Corning, Kingspan Group PLC, Morgan Advanced Materials, Etex, Isover, BASF SE, Kflex, Aspen Aerogel

|

Global Refrigeration Insulation Materials Market Segmentation: By Material Type

-

Elastomeric Foam

-

PU & PIR

-

Polystyrene Foam

-

Phenolic Foam

-

Fiberglass

-

Others

The global refrigeration insulation materials market may be divided into elastomeric foam, PU & PIR, polystyrene foam, phenolic foam, fiberglass, and others depending on material type. Elastomeric foam is a flexible and lightweight material that is appropriate for refrigeration applications due to its outstanding thermal insulation capabilities and resistance to moisture and condensation. Polyurethane and polyisocyanurate (PU and PIR) are common insulation materials with good thermal efficiency and mechanical strength. Polystyrene foam is a lightweight and stiff material that provides excellent thermal insulation and structural support. Phenolic foam has high fire resistance and low thermal conductivity. Fiberglass insulation is well-known for its thermal insulation and durability. Natural and sustainable insulating materials may also be used. Market insights and market share differ depending on the material type, with PU & PIR and polystyrene foam often holding considerable market shares due to their extensive use and advantageous features. However, elastomeric foam, phenolic foam, fiberglass, and other materials' market shares may vary depending on regional preferences and unique industrial requirements.

Global Refrigeration Insulation Materials Market Segmentation: By Application

The global refrigeration insulating materials market can be segmented into commercial, industrial, cryogenic, and refrigerated transportation applications. Applications in refrigeration systems used in retail stores, supermarkets, restaurants, and commercial buildings consist of the commercial section. Refrigeration systems utilized in businesses such as food processing, pharmaceuticals, chemicals, and cold storage facilities are included in the industrial category. Insulation materials used in severe low-temperature applications, such as the liquefied natural gas (LNG) sector, are included in the cryogenic section. Insulation materials for refrigerated vehicles, containers, and trailers used in the transportation of perishable commodities are included in the refrigerated transportation industry. Market insights and market share differ across different categories, with the industrial and commercial segments accounting for the majority of market contributions due to the significant demand for refrigeration systems in the food and beverage industries and cold chain logistics. Because of the increased need for LNG and other cryogenic uses, the cryogenic market has great potential. As the demand for efficient cold storage during transit grows, the refrigerated transportation market also presents potential.

Global Refrigeration Insulation Materials Market Segmentation: By End-Use Industry

Based on the end-use industry, the worldwide refrigeration insulation materials market can be divided into food and beverage, chemicals and pharmaceuticals, oil and gas, and petrochemicals. Due to the necessity to preserve perishable items along the supply chain, the food and beverage industry is a big consumer of refrigeration systems and insulating materials. Because of the strong need for insulation materials in refrigerators, freezers, and cold storage facilities, this category commands a sizable market share. The chemicals and pharmaceutical industries also make major contributions to the market, as refrigeration systems are required for the storage of temperature-sensitive chemicals and medications. Refrigeration insulating materials are required by the oil and gas industry for applications such as LNG storage and transportation. Refrigeration systems are used in the petrochemical industry to preserve various petrochemicals. The food and beverage business often holds the highest proportion due to its substantial usage of refrigeration systems, followed by the chemicals and pharmaceutical industries. The oil and gas and petrochemical sectors' market shares may fluctuate depending on regional demand and unique project requirements.

Global Refrigeration Insulation Materials Market Segmentation: By Region

-

North America

-

Europe

-

Asia Pacific

-

South America

-

Middle East & Africa

North America, Europe, Asia Pacific, South America, the Middle East, and Africa account for the majority of the worldwide refrigeration insulating materials market. Because of well-established businesses and strong energy efficiency requirements, North America and Europe maintain considerable market shares. The Asia Pacific region dominates the market, owing to the fast-propelling food and beverage industry, the arising retail infrastructure, and cold chain logistics. Because of expanding urbanization, changing lifestyles, and increased disposable incomes, the region provides significant growth potential. South America, the Middle East, and Africa also contribute to the market, which is driven by arising industrial sectors and the demand for refrigeration systems. The market share varies by region, with North America and Europe holding large shares, while the Asia Pacific region is expected to grow significantly in the next years.

Global Refrigeration Insulation Materials Market Key Players:

-

Armacell

-

Owens Corning

-

Kingspan Group PLC

-

Morgan Advanced Materials

-

Etex

-

Isover

-

BASF SE

-

Kflex

-

Aspen Aerogel