Counter-UAS Systems Market

In 2025, the Global Counter-UAS Systems Market was valued at approximately USD 3,214 million and is projected to reach around USD 8,472 million by 2030, expanding at a CAGR of about 21.4% during 2026–2030.

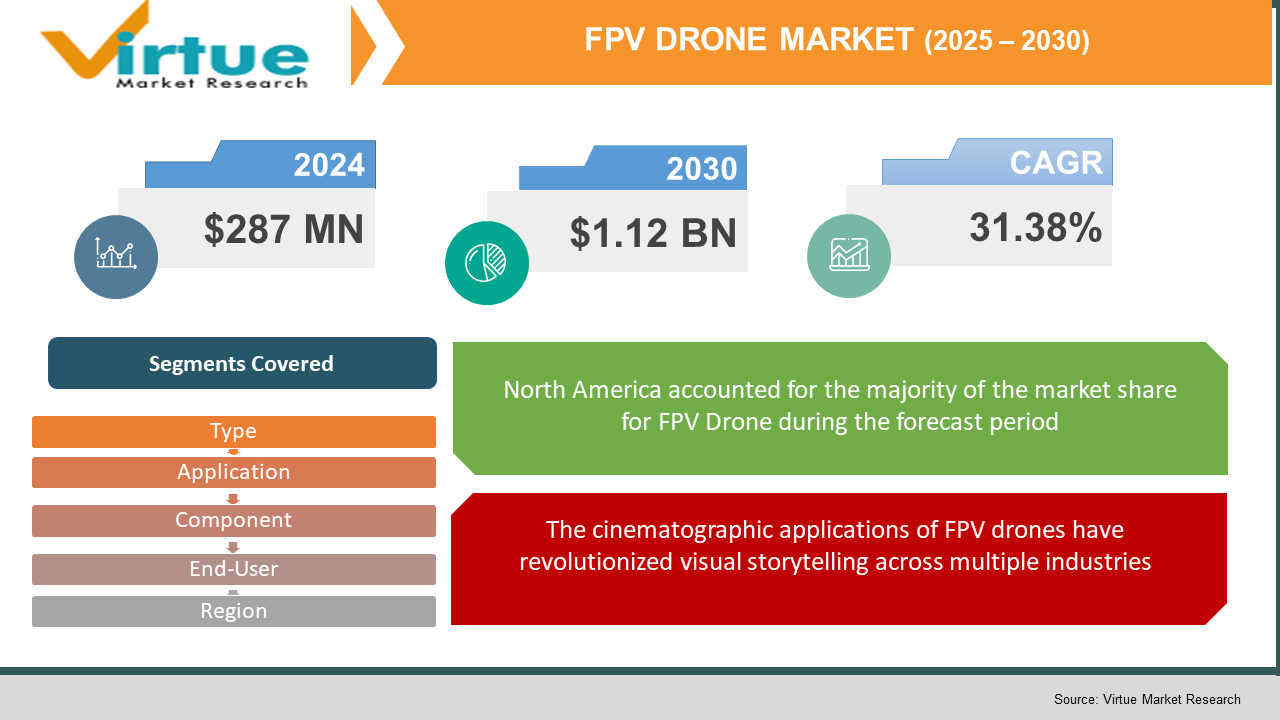

Explore reportThe FPV Drone Market was valued at USD 287 million in 2024 and is projected to reach a market size of USD 1.12 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 31.38%.

The FPV Drone Market represents a revolutionary convergence of cutting-edge aviation technology, immersive virtual reality experiences, and democratized aerial cinematography. Unlike traditional unmanned aerial vehicles, FPV drones create an unprecedented pilot experience by transmitting real-time video feeds directly to specialized goggles or display screens, effectively placing operators in the virtual cockpit of their aircraft. This technological paradigm shift has catalyzed the emergence of entirely new industries, recreational activities, and professional applications that were previously inconceivable. The market's foundation rests upon the seamless integration of multiple sophisticated technologies, including high-definition video transmission systems, ultra-low latency communication protocols, precision flight control algorithms, and miniaturized camera systems capable of delivering broadcast-quality footage. These components work harmoniously to create an immersive flying experience that bridges the gap between remote operation and actual piloting, offering users an adrenaline-fueled perspective that traditional drones simply cannot match. The contemporary FPV drone ecosystem encompasses a diverse spectrum of applications, from high-octane racing competitions that have evolved into internationally recognized sports, to cinematic applications that are revolutionizing the film and television industry. Hollywood productions increasingly rely on FPV drones to capture dynamic sequences that would be impossible or prohibitively expensive to achieve through traditional filming methods. These nimble aircraft can navigate through tight spaces, perform complex maneuvers, and deliver stunning aerial choreography that adds unprecedented visual depth to storytelling. Manufacturing trends within the FPV drone industry reflect a shift toward modular design philosophies that allow users to customize and upgrade their aircraft according to specific requirements. This approach has fostered a vibrant aftermarket ecosystem of specialized components, ranging from high-performance motors and propellers to advanced camera systems and transmission equipment. The modularity also enables rapid repair and maintenance, addressing one of the primary concerns of intensive FPV operations.

The emergence of FPV drone racing as a legitimate competitive sport has fundamentally transformed the market landscape.

Professional racing leagues, including the Drone Racing League (DRL) and MultiGP, have established international circuits with substantial prize pools, television coverage, and corporate sponsorship opportunities that rival traditional motorsports. This competitive ecosystem drives continuous innovation in drone performance, with manufacturers investing heavily in developing faster, more agile aircraft capable of withstanding the rigorous demands of professional racing. The spectator appeal of FPV racing, aided by immersive broadcast technologies that let spectators to experience the pilot's point of view, has sparked mainstream media interest and investment, propelling market expansion.

The cinematographic applications of FPV drones have revolutionized visual storytelling across multiple industries.

These versatile aircraft enable filmmakers to capture dynamic sequences that were previously impossible or prohibitively expensive, including high-speed chases, interior building flights, and complex aerial choreography that adds unprecedented visual depth to productions. The democratization of professional-quality aerial cinematography has empowered independent content creators, real estate professionals, and marketing agencies to produce compelling visual content at a fraction of traditional costs. Major streaming platforms and production companies increasingly recognize FPV technology as an essential tool for creating engaging content that captures audience attention in an increasingly competitive entertainment landscape.

The FPV drone market faces significant obstacles including steep learning curves that require extensive pilot training and practice, regulatory complexities that vary across jurisdictions and create compliance challenges for operators, and safety concerns related to high-speed operations in populated areas. Technical limitations such as short battery life, susceptibility to weather conditions, and the fragility of racing configurations result in frequent crashes and high maintenance costs that can deter potential users from market entry.

The market presents substantial opportunities in emerging applications such as emergency response operations, where FPV drones can navigate confined spaces and provide real-time reconnaissance in hazardous environments. The integration of artificial intelligence and autonomous capabilities offers potential for developing self-piloting systems that could expand market accessibility. Additionally, the growing demand for immersive entertainment experiences and virtual reality integration creates opportunities for developing next-generation FPV systems that blur the lines between reality and simulation.

FPV DRONE MARKET REPORT COVERAGE:

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 - 2030 |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2030 |

|

CAGR |

31.38% |

|

Segments Covered |

By Type, application, component, end user, and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regional Scope |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Key Companies Profiled |

DJI, TBS (Team BlackSheep), ImmersionRC, Walkera, Eachine, HGLRC, iFlight, BetaFPV, GEPRC, Holybro, NewBeeDrone, TMotor, FrSky, Fat Shark, and Caddx, |

FPV Drone Market Segmentation:

Freestyle Drones represent the fastest-growing segment, driven by the creative flexibility they offer pilots and the growing community of content creators who showcase spectacular aerial maneuvers on social media platforms. These versatile aircraft bridge the gap between racing performance and cinematographic capabilities, attracting both recreational users and professional pilots.

Racing Drones maintain dominance as the most established segment, commanding the largest market share due to the organized competitive infrastructure, professional leagues, and dedicated enthusiast communities that drive consistent demand for high-performance aircraft and specialized components.

FPV Drone Market Segmentation by Application:

Cinematography and Photography applications are experiencing the fastest growth, fueled by the increasing demand for dynamic aerial content across entertainment, marketing, and social media platforms. The ability to capture unique perspectives and perform complex camera movements has made FPV drones indispensable tools for modern content creators.

Sports and Recreation remains the most dominant application, encompassing both competitive racing and recreational flying that form the foundation of the FPV community. This segment includes organized competitions, casual flying clubs, and individual enthusiasts who drive the majority of consumer purchases.

Video Transmission Systems are the fastest-growing component segment, driven by demand for higher resolution, lower latency, and more reliable wireless video links that enhance the immersive flying experience. Advances in digital transmission technology and antenna design continue to push the boundaries of real-time video quality.

Motors and Propellers represent the most dominant component segment by replacement frequency and performance impact, as these high-stress components require regular maintenance and upgrades to maintain optimal performance in demanding FPV applications.

Content Creators are the fastest-growing end-user segment, as social media platforms and digital marketing create increasing demand for unique aerial footage that can only be captured through FPV technology. This segment includes individual creators, marketing agencies, and production companies seeking distinctive visual content.

Hobbyist Enthusiasts maintain dominance as the largest end-user group, encompassing recreational pilots who participate in racing, freestyle flying, and casual aerial photography. This segment drives the majority of consumer sales and aftermarket component purchases.

North America commands approximately 40% of the global market share, driven by the presence of major racing leagues, technology companies, and a well-established hobbyist community with high disposable income. The region benefits from relatively permissive regulations and a strong culture of technological innovation.

Asia-Pacific demonstrates the highest growth rate, propelled by increasing disposable income, growing interest in technology hobbies, and the emergence of local manufacturing capabilities that reduce costs and improve accessibility for regional consumers.

The pandemic initially disrupted FPV drone racing events and competitions, leading to reduced equipment sales and delayed product launches. However, the increased focus on outdoor recreational activities and home entertainment created new opportunities for FPV flying as a socially distanced hobby. The shift toward remote work and digital content creation also increased demand for aerial photography and videography services, partially offsetting losses in the competitive racing segment.

Current market trends focus on the integration of artificial intelligence for autonomous flight capabilities, development of longer-lasting battery technologies, and the emergence of standardized racing drone specifications. There's also growing interest in hybrid systems that combine FPV technology with traditional autonomous drones, creating versatile platforms suitable for both recreational and commercial applications. The industry is also witnessing increased collaboration between drone manufacturers and component suppliers to develop optimized systems.

The primary drivers include the explosive growth of competitive drone racing as a legitimate sport with professional leagues and substantial prize pools, the revolutionary impact of FPV technology on cinematography and content creation enabling previously impossible aerial footage, and the increasing accessibility of high-performance components that make FPV flying more approachable for newcomers.

Major concerns center around the steep learning curve required for safe FPV piloting, complex and varying regulatory frameworks across different jurisdictions, safety risks associated with high-speed operations near people and property, short battery life limiting flight duration, and the fragility of racing configurations leading to frequent crashes and high maintenance costs

Key players include DJI, TBS (Team BlackSheep), ImmersionRC, Walkera, Eachine, HGLRC, iFlight, BetaFPV, GEPRC, Holybro, NewBeeDrone, TMotor, FrSky, Fat Shark, and Caddx, each contributing specialized components and complete systems to the FPV ecosystem.

North America holds the largest market share, driven by established racing leagues, technology companies, high disposable income, and a strong hobbyist community with relatively permissive regulatory environments that encourage FPV development and adoption.

Asia-Pacific demonstrates the fastest growth rate, fueled by increasing disposable income, growing interest in technology hobbies, emerging local manufacturing capabilities, and expanding access to FPV technology through improved distribution networks and reduced costs.

Joining thousands of companies around the world committed to making the Excellent Business Solutions.

Specify your preferred Countries, Segments, or timeframes

Unlock Country Level Outlook, Trends, Cross-country Comparability, or supply Chain Variations.

Analyst Support

Every order comes with Analyst Support.

Customization

We offer customization to cater your needs to fullest.

Verified Analysis

We value integrity, quality and authenticity the most.