Asia Pacific Smoothies Market

The Asia Pacific smoothies’ market is expected to grow from approximately USD 4.5 billion in 2025 to around USD 8.5 billion in 2030, at a compound annual growth rate of around 12.8% during 2025-2030.

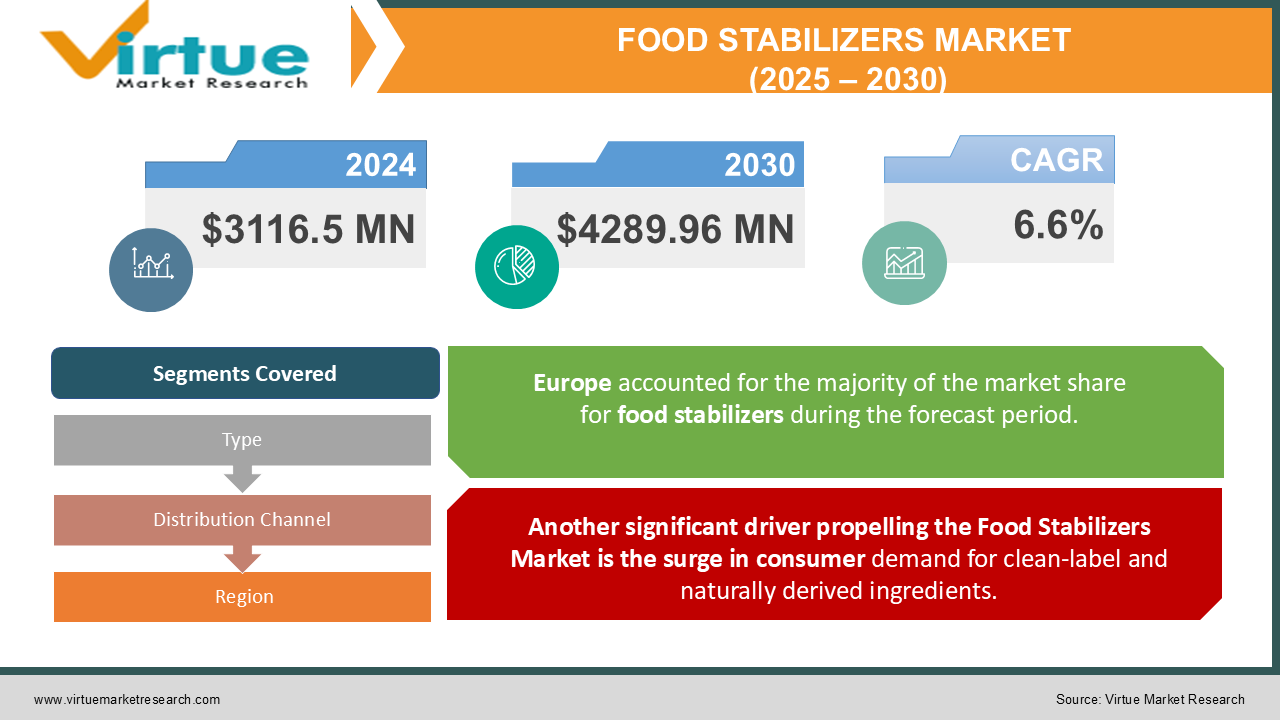

Explore reportThe Food Stabilizers Market was valued at USD 3116.5 million in 2024 and is projected to reach a market size of USD 4289.96 million by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 6.6%.

The Food Stabilizers Market has evolved into an essential sector within the global food ingredients industry, emerging as a pivotal element in ensuring product consistency, texture, and shelf-life in an increasingly competitive market landscape. This market encompasses a wide range of additives that help maintain the structural integrity and appearance of food products, even when subjected to fluctuations in temperature, humidity, and mechanical handling. In today’s fast-paced consumer world, where convenience and quality are paramount, food stabilizers have garnered significant attention as manufacturers strive to meet the dual demands of taste and longevity. Manufacturers have been investing in research and development to create innovative stabilizer formulations that not only extend the shelf-life but also enhance the sensory attributes of food products. This pursuit of excellence has opened avenues for incorporating natural, plant-based alternatives alongside traditional chemical additives, thereby catering to an increasingly health-conscious consumer base.

Key Market Insights:

The market witnessed a 1.2 million metric ton consumption of various stabilizers in 2024.

2024 records indicate a 10% overall increase in market volume for innovative stabilizer applications.

A significant 78% of processors noted a marked improvement in product stability during transportation.

Market Drivers:

One of the most powerful market drivers in the Food Stabilizers Market is the escalating demand for enhanced product quality and consistency across the food industry.

In an era where consumer expectations are rapidly evolving, manufacturers have become increasingly focused on delivering products that not only taste great but also maintain their quality from production to consumption. This drive for consistency has led to an amplified reliance on stabilizers, as these additives ensure that every batch of food products retains a uniform texture, colour, and structural integrity regardless of external variables during storage or transport. The influence of this driver is evident in how manufacturers are investing in advanced stabilization techniques to address issues related to phase separation, syneresis, and deterioration over time. With the proliferation of ready-to-eat and convenience foods, where extended shelf-life without compromising on sensory attributes is crucial, food stabilizers have become indispensable. The market is responding by developing multifunctional additives that not only serve as stabilizers but also enhance nutritional profiles and taste, thereby offering a dual advantage. These innovations enable food producers to experiment with new formulations and reduce dependency on synthetic chemicals, meeting the growing demand for natural ingredients.

Another significant driver propelling the Food Stabilizers Market is the surge in consumer demand for clean-label and naturally derived ingredients.

Over the past few years, there has been a profound shift in consumer behaviour, with more shoppers scrutinizing ingredient lists and actively seeking products that contain fewer artificial additives. This transformation in purchasing habits has spurred food manufacturers to reformulate products by incorporating stabilizers that are both effective and derived from natural sources. The growing preference for transparency and sustainability in food production is steering manufacturers toward plant-based and naturally sourced stabilizers, which are perceived as safer and healthier alternatives to their synthetic counterparts. Furthermore, regulatory authorities in many parts of the world are tightening the guidelines around artificial additives, which in turn has accelerated the shift toward natural alternatives. Food manufacturers are now compelled to reassess their product formulations, favouring ingredients that support clean-label claims and sustainable practices. This regulatory impetus, coupled with a strong consumer-driven demand for authenticity, is driving innovation and competitive differentiation among suppliers. Manufacturers who successfully adapt to these changes not only secure a competitive advantage but also contribute to broader industry trends that emphasize health, sustainability, and transparency. The synergy between consumer demand for natural products and the regulatory push towards transparency has created a robust environment for innovation in natural stabilizers. This dynamic market scenario is compelling manufacturers to invest heavily in research and development, leading to breakthrough technologies that are reshaping the traditional paradigms of food stabilization.

Market Restraints and Challenges:

Despite the promising opportunities, the Food Stabilizers Market is confronted by a series of restraints and challenges that hinder its unfettered growth. One of the primary challenges is the stringent regulatory landscape governing the use of food additives. Global and local food safety authorities impose rigorous standards to ensure that stabilizers used in food products are safe for consumption. This results in prolonged approval processes and the necessity for extensive documentation and testing, thereby increasing time-to-market and operational costs. Manufacturers often struggle to balance innovation with compliance, as rapid advancements in technology must be aligned with slowly evolving regulatory frameworks, leading to a potential bottleneck in product rollout. Consumer skepticism towards new additives further compounds the challenge. In an era where food safety and ingredient transparency are paramount, any misstep or controversy related to the efficacy or safety of a stabilizer can lead to widespread consumer distrust. Negative perceptions, even if unfounded, can have a lasting impact on market dynamics, forcing companies to invest heavily in marketing and public relations campaigns to restore confidence. Additionally, global supply chain complexities, particularly in emerging markets, introduce logistical challenges that can result in delays, quality inconsistencies, and increased transportation costs.

Market Opportunities:

The Food Stabilizers Market is ripe with opportunities that can propel the industry into new frontiers of innovation and profitability. One of the most compelling opportunities lies in the burgeoning demand for clean-label and natural food ingredients. As consumers become more educated about their dietary choices, there is a marked preference for products that boast transparency in ingredient sourcing and production methods. This trend creates an opening for companies to innovate and develop natural stabilizers that meet both performance criteria and consumer expectations. The shift towards natural ingredients not only enhances brand reputation but also opens doors to premium pricing and access to niche market segments that are willing to pay more for products with proven health benefits. The integration of digital technologies and advanced analytics into the production and distribution processes is yet another opportunity. Digital transformation can enhance quality control, streamline supply chain management, and enable real-time monitoring of production parameters. Such technological advancements help in ensuring consistent product quality and reducing waste, thereby improving operational efficiencies and profitability. Additionally, strategic collaborations and partnerships between ingredient suppliers, food manufacturers, and technology firms can drive research initiatives that lead to the development of novel stabilizers with multifunctional properties.

FOOD STABILIZERS MARKET REPORT COVERAGE:

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 - 2030 |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2030 |

|

CAGR |

6.6% |

|

Segments Covered |

By Type, Distribution Channel and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regional Scope |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Key Companies Profiled |

Ingredion, CP Kelco, DuPont, Cargill, Kerry Group, Tate & Lyle, DSM, Roquette, BASF, Corbion |

Hydrocolloid Stabilizers

Protein-Based Stabilizers

Starch-Based Stabilizers

Synthetic Stabilizers

Enzyme-Modified Stabilizers

Among these types, the fastest-growing segment is the hydrocolloid stabilizers, which are gaining traction due to their versatility in providing texture enhancement and moisture retention while being perceived as more natural. Conversely, the most dominant type in terms of market share remains the protein-based stabilizers, largely due to their widespread application in dairy and bakery products where they deliver consistent performance and product quality.

Direct Sales

Online Distribution

Distributors and Wholesalers

Retail Outlets

Contract Manufacturing

Within the distribution channel segment, online distribution is emerging as the fastest-growing channel, driven by advancements in e-commerce and digital marketing strategies that make it easier for manufacturers to reach a global customer base. Meanwhile, the most dominant channel remains direct sales, which continues to be favoured by larger food manufacturers due to its ability to facilitate customized solutions and foster closer relationships with key customers.

North America

Europe

Asia Pacific

South America

Middle East and Africa

In 2024, Europe holds the largest market share due to its mature food processing industry and high regulatory standards, which drive the need for consistent and high-quality food stabilization solutions. However, the Asia-Pacific region is emerging as the fastest-growing region, fueled by rapid urbanization, increased consumer spending, and a surge in processed food demand. The robust industrial growth in Asia-Pacific, coupled with evolving consumer tastes and modernization of food production technologies, is reshaping the regional landscape and creating new opportunities for market players.

COVID-19 Impact Analysis on the Market:

The COVID-19 pandemic exerted a profound influence on the Food Stabilizers Market, altering supply chain dynamics, production priorities, and consumer behaviour in ways that continue to reverberate in 2024. In the wake of the pandemic, food manufacturers were compelled to reexamine their operational strategies, particularly as disruptions in global logistics and raw material availability forced companies to adopt more resilient and agile supply chains. The pandemic underscored the need for longer shelf-life and enhanced product stability, as panic buying and shifts in consumption patterns resulted in increased demand for packaged and non-perishable foods. In response, manufacturers ramped up their usage of food stabilizers to ensure that products remained safe and consistent over extended storage periods, thereby mitigating the risk of spoilage and waste. Consumer behaviour during the pandemic also played a critical role in shaping the market dynamics. With heightened concerns over food safety and product authenticity, consumers began scrutinizing ingredient labels more closely, demanding transparency and quality assurance. This shift in mindset led to a greater acceptance of stabilizers that not only enhanced product durability but also complied with stringent quality standards. As a result, manufacturers focused on improving the traceability of stabilizer production processes and reinforcing consumer confidence through rigorous testing and certification measures.

Latest Trends and Developments:

In 2024, the Food Stabilizers Market is witnessing a wave of transformative trends and technological advancements that are reshaping product development and market strategies. One of the most notable trends is the accelerated adoption of green chemistry in the production of food stabilizers. Companies are increasingly investing in eco-friendly technologies that reduce environmental impact by utilizing renewable resources and minimizing waste during production. This focus on sustainability is driven not only by regulatory requirements but also by the growing consumer demand for clean-label products that support health and environmental well-being. As a result, manufacturers are actively exploring innovative extraction methods and biotechnological processes that deliver high-performance stabilizers while ensuring minimal ecological footprints. The emergence of multifunctional stabilizers that can serve dual or even triple roles—such as emulsification, thickening, and gelling—is another development capturing the industry's attention. These multifunctional additives offer a significant advantage by streamlining formulations and reducing the number of ingredients required in a product. This not only simplifies the production process but also contributes to cleaner and more recognizable ingredient lists, which are highly valued in the current market scenario. Furthermore, continuous research into natural and bio-based alternatives has led to a broader acceptance of plant-derived stabilizers, a trend that aligns with the growing consumer focus on health and sustainability.

Key Players in the Market:

Ingredion

CP Kelco

DuPont

Cargill

Kerry Group

Tate & Lyle

DSM

Roquette

BASF

Corbion

Key factors driving growth include increasing consumer demand for clean-label, natural ingredients, rapid technological advancements in food processing, sustainability initiatives, rising focus on product shelf-life extension, and enhanced regulatory standards that collectively promote innovation and market expansion globally, competitively, effectively.

Key concerns in the Food Stabilizers Market include escalating raw material costs, divergent regulatory standards, supply chain disruptions, consumer skepticism towards synthetic additives, maintaining product efficacy while transitioning to natural ingredients, and highly intense competitive pressures that challenge smaller companies.

Ingredion, CP Kelco, DuPont, Cargill, Kerry Group, Tate & Lyle, DSM

North America currently holds the largest market share, estimated around 35%.

Asia Pacific has shown significant room for growth in specific segments.

Joining thousands of companies around the world committed to making the Excellent Business Solutions.

Specify your preferred Countries, Segments, or timeframes

Unlock Country Level Outlook, Trends, Cross-country Comparability, or supply Chain Variations.

Analyst Support

Every order comes with Analyst Support.

Customization

We offer customization to cater your needs to fullest.

Verified Analysis

We value integrity, quality and authenticity the most.