Asia Pacific Smoothies Market

The Asia Pacific smoothies’ market is expected to grow from approximately USD 4.5 billion in 2025 to around USD 8.5 billion in 2030, at a compound annual growth rate of around 12.8% during 2025-2030.

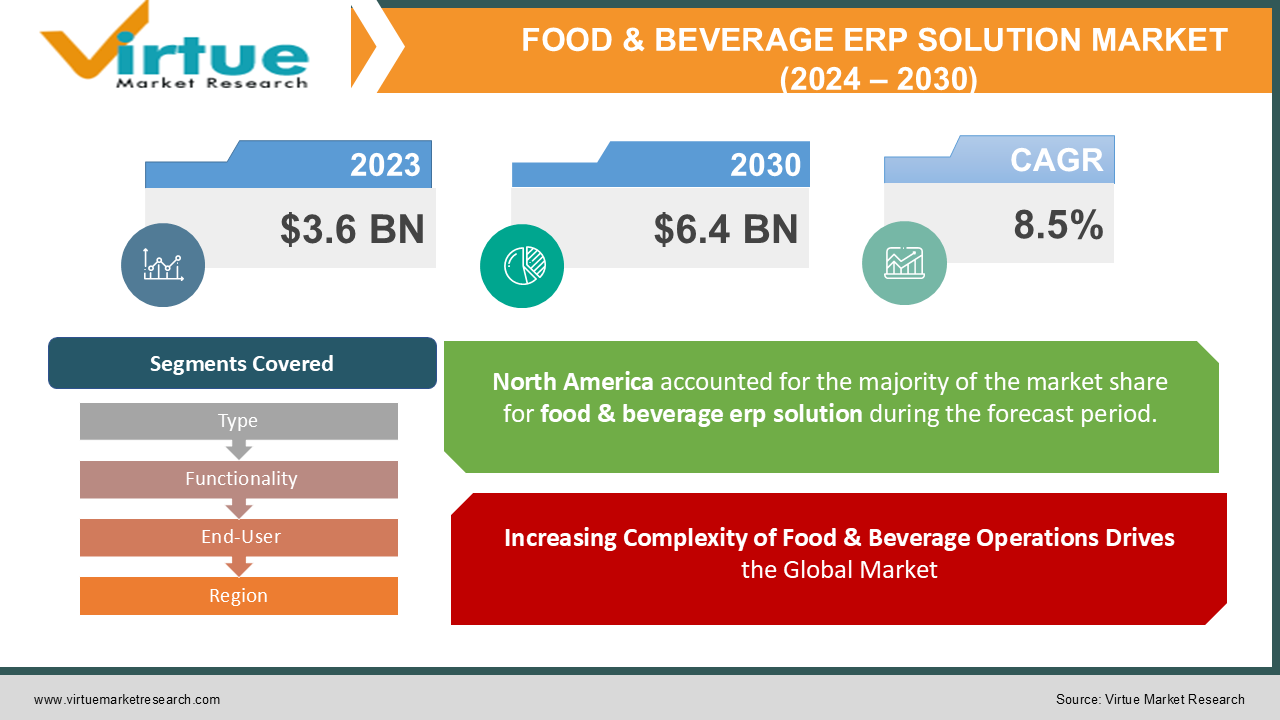

Explore reportAs of 2023, the Global Food & Beverage ERP Solution Market is valued at approximately USD 3.6 billion and is projected to reach USD 6.4 billion by 2030, growing at a compound annual growth rate (CAGR) of 8.5% during the forecast period.

ERP (Enterprise Resource Planning) solutions tailored for the food and beverage industry help businesses streamline processes, manage resources more effectively, and make data-driven decisions. Key functionalities include inventory management, supply chain optimization, production planning, quality control, and compliance management.

The market's growth is fueled by the increasing complexity of food and beverage operations, rising consumer demand for transparency, and the need to maintain high standards of food safety and traceability. The ongoing shift towards cloud-based ERP solutions and the integration of advanced technologies such as AI, IoT, and analytics are expected to further drive the market expansion.

The growing complexity of operations in the food and beverage industry is a primary driver of the ERP solution market. Companies are facing challenges such as managing diverse product lines, ensuring compliance with stringent food safety regulations, and navigating complex supply chains.

ERP solutions provide a centralized platform to manage these complexities, offering real-time visibility into operations, streamlining workflows, and enabling better resource management. The ability to integrate various business processes, from procurement to production and distribution, helps food and beverage companies improve efficiency, reduce costs, and maintain high-quality standards.

Consumer demand for transparency regarding the origins, ingredients, and safety of food products is increasing. This trend is driving the adoption of ERP solutions that offer robust traceability features, enabling companies to track products throughout the supply chain. Traceability is not only crucial for meeting regulatory requirements but also for building consumer trust and managing risks associated with food recalls.

ERP solutions equipped with advanced tracking and reporting capabilities allow food and beverage companies to ensure product quality, comply with industry standards, and respond quickly to safety issues, thus enhancing their market competitiveness.

The shift towards cloud-based ERP solutions is another key driver of the Food & Beverage ERP Solution Market. Cloud-based systems offer several advantages, including lower upfront costs, scalability, and ease of access to data from anywhere, which are particularly beneficial for food and beverage companies operating across multiple locations.

The flexibility and cost-effectiveness of cloud-based ERP solutions make them attractive to small and medium-sized enterprises (SMEs) that may not have the resources to invest in traditional on-premises systems. Additionally, cloud-based ERP solutions are easier to update and integrate with other digital tools, such as IoT devices and analytics platforms, enhancing their functionality and value proposition.

Unlock Market Insights: Get A FREE Sample Report Today!

Despite the numerous benefits of ERP solutions, the high implementation costs and complexity associated with their deployment can be significant barriers, particularly for SMEs. The process of selecting, customizing, and integrating an ERP system can be time-consuming and costly, requiring significant investment in terms of both money and resources.

Additionally, the need for ongoing maintenance, updates, and training can add to the total cost of ownership. The complexity of implementation can also lead to operational disruptions if not managed carefully, posing challenges for companies that are already operating on thin margins and tight schedules.

As food and beverage companies increasingly adopt cloud-based ERP solutions, data security and privacy concerns are becoming more pronounced. The sensitive nature of business data, including proprietary recipes, supplier information, and customer details, makes it a prime target for cyberattacks.

Ensuring the security of cloud-based systems and maintaining compliance with data protection regulations, such as GDPR and CCPA, is a critical challenge for companies adopting ERP solutions. The need to protect data from unauthorized access and breaches adds a layer of complexity and cost, which can deter some companies from fully embracing cloud-based ERP solutions.

The Food & Beverage ERP Solution Market presents several opportunities for growth and innovation. The increasing focus on sustainability and reducing food waste is driving interest in ERP solutions that offer advanced inventory management and demand forecasting capabilities. These features help companies optimize stock levels, minimize waste, and reduce their environmental footprint.

The expansion of ERP solutions into emerging markets, where the food and beverage industry is experiencing rapid growth, also presents significant opportunities. As companies in these regions modernize their operations and seek to improve efficiency, the demand for ERP solutions is expected to rise.

Additionally, the integration of AI, machine learning, and IoT into ERP systems is creating new opportunities for innovation, enabling predictive analytics, real-time monitoring, and automated decision-making. Companies that invest in these advanced technologies and offer flexible, scalable solutions are well-positioned to capitalize on the growing demand for ERP solutions in the food and beverage industry.

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2023 - 2030 |

|

Base Year |

2023 |

|

Forecast Period |

2024 - 2030 |

|

CAGR |

8.5% |

|

Segments Covered |

By Type, Functionality, End-User, and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regional Scope |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Key Companies Profiled |

SAP SE, Oracle Corporation, Microsoft Corporation, Infor,Epicor Software Corporation, Aptean, SYSPRO, JustFood ERP, Plex Systems, IFS AB |

CUSTOMIZE THIS FULL REPORT AS PER YOUR NEEDS

On-Premises

Cloud-Based

Hybrid

Cloud-based ERP solutions are the most dominant, capturing over 50% of global revenue. The popularity of cloud-based systems is driven by their scalability, lower initial costs, and the ability to access data from any location. These systems are particularly appealing to SMEs, which may lack the resources to invest in traditional on-premises solutions.

On-premises ERP solutions, while offering greater control and customization, are gradually losing market share due to their higher costs and maintenance requirements.

Hybrid solutions, which combine on-premises and cloud functionalities, are also gaining traction as they offer a balanced approach, allowing companies to leverage the benefits of both deployment models.

Inventory Management

Supply Chain Management

Production Planning

Quality Control

Others

Inventory management is a critical functionality within ERP solutions, accounting for over 35% of the market. Effective inventory management helps food and beverage companies reduce waste, optimize stock levels, and ensure the timely availability of raw materials and finished products.

Supply chain management is another key area, providing tools to enhance visibility, streamline logistics, and improve supplier collaboration. Production planning and quality control functionalities are also essential, helping companies optimize production schedules, maintain product quality, and comply with industry standards.

As companies continue to face challenges related to food safety, compliance, and operational efficiency, the demand for comprehensive ERP functionalities is expected to grow.

Small & Medium Enterprises

Large Enterprises

Large enterprises are the primary users of ERP solutions in the food and beverage industry, contributing significantly to market revenue. These companies require sophisticated systems to manage complex operations, comply with stringent regulations, and maintain high standards of quality and efficiency.

Small and medium-sized enterprises (SMEs) are also increasingly adopting ERP solutions as they seek to modernize their operations and compete more effectively in the market. The availability of affordable, scalable cloud-based solutions has made ERP systems more accessible to SMEs, driving their adoption. As SMEs continue to recognize the benefits of ERP solutions in improving efficiency and reducing costs, their share of the market is expected to increase.

North America

Europe

Asia-Pacific

Latin America

Middle East and Africa

What's Next for Your Market? Get a Snapshot with FREE Sample Report

North America leads the Global Food & Beverage ERP Solution Market, contributing to 40% of global revenue. The region's dominance is driven by the presence of major food and beverage companies, high adoption rates of digital solutions, and stringent regulatory requirements. The U.S. market, in particular, is characterized by advanced technological infrastructure, a focus on innovation, and a strong emphasis on food safety and quality.

Europe follows closely, with a mature market supported by strong regulatory frameworks and a high level of digitalization in the food and beverage industry.

The Asia-Pacific region is expected to witness the highest growth rate, driven by rapid industrialization, expanding food and beverage sectors, and increasing investment in technology.

Latin America the Middle East and Africa are emerging markets with significant potential, driven by economic growth, rising consumer demand, and the need for improved operational efficiency in the food and beverage industry.

The COVID-19 pandemic had a profound impact on the Global Food & Beverage ERP Solution Market. The pandemic disrupted supply chains, caused fluctuations in demand, and highlighted the need for greater agility and resilience in food and beverage operations. As a result, many companies accelerated their digital transformation efforts, increasing investments in ERP solutions to improve visibility, manage disruptions, and adapt to changing market conditions.

The shift to remote work and the need for real-time data access further drove the adoption of cloud-based ERP systems, which offer flexibility and support remote operations. While the pandemic posed challenges, such as supply chain disruptions and economic uncertainties, it also underscored the importance of digital solutions in maintaining business continuity and optimizing operations.

As the global economy recovers, the demand for ERP solutions in the food and beverage industry is expected to continue growing, supported by ongoing digitalization efforts and the need for greater operational efficiency.

Several trends and developments are shaping the Food & Beverage ERP Solution Market. One significant trend is the increasing adoption of AI and machine learning in ERP systems, enhancing predictive analytics, demand forecasting, and real-time decision-making capabilities. The integration of IoT devices is also gaining traction, enabling real-time monitoring of production processes, inventory levels, and supply chain activities.

The growing focus on sustainability is driving demand for ERP solutions that offer advanced features for waste reduction, energy efficiency, and sustainable sourcing. The rise of e-commerce and direct-to-consumer sales channels is prompting food and beverage companies to adopt ERP solutions that support multi-channel order management and fulfillment.

Additionally, the increasing importance of cybersecurity is driving investments in secure, cloud-based ERP systems that protect sensitive business data and comply with data protection regulations. These trends are expected to drive further innovation and growth in the Food & Beverage ERP Solution Market as companies seek to stay competitive and meet evolving consumer and regulatory demands.

SAP SE

Oracle Corporation

Microsoft Corporation

Infor

Epicor Software Corporation

Aptean

SYSPRO

JustFood ERP

Plex Systems

IFS AB

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

As of 2023, the Global Food & Beverage ERP Solution Market is valued at approximately USD 3.6 billion and is projected to reach USD 6.4 billion by 2030, growing at a CAGR of 8.5% during the forecast period.

The key drivers include the increasing complexity of food and beverage operations, rising demand for transparency and traceability, and the shift towards cloud-based ERP solutions.

The Food & Beverage ERP Solution Market is segmented by type (On-Premises, Cloud-Based, Hybrid), functionality (Inventory Management, Supply Chain Management, Production Planning, Quality Control, Others), and end-user (Small & Medium Enterprises, Large Enterprises).

North America is the most dominant region, contributing 40% of global revenue, driven by the presence of major food and beverage companies, high adoption of digital solutions, and stringent regulatory requirements.

The leading players in the market include SAP SE, Oracle Corporation, Microsoft Corporation, Infor, Epicor Software Corporation, Aptean, SYSPRO, JustFood ERP, Plex Systems, and IFS AB.

Joining thousands of companies around the world committed to making the Excellent Business Solutions.

Specify your preferred Countries, Segments, or timeframes

Unlock Country Level Outlook, Trends, Cross-country Comparability, or supply Chain Variations.

Analyst Support

Every order comes with Analyst Support.

Customization

We offer customization to cater your needs to fullest.

Verified Analysis

We value integrity, quality and authenticity the most.