Fiberglass-based Wind Turbine Market Size (2024 – 2030)

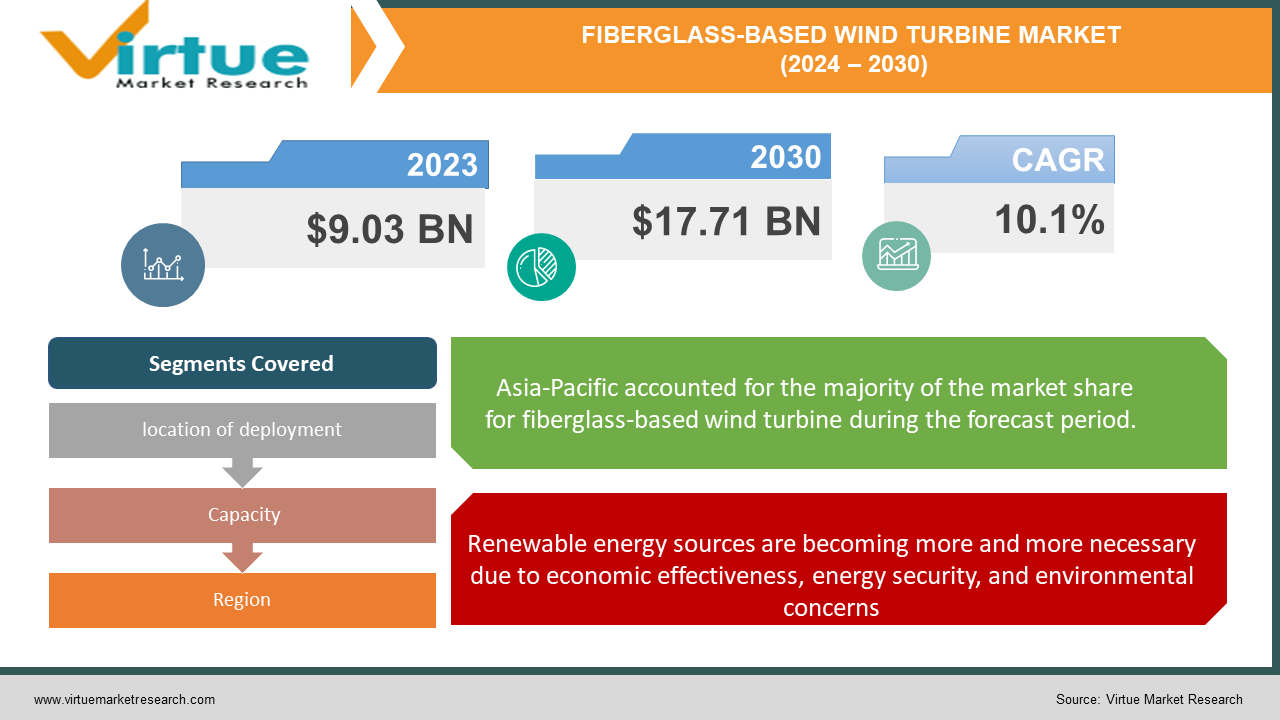

The Global Fiberglass-based Wind Turbine Market was valued at USD 9.03 billion in 2023 and is projected to reach a market size of USD 17.71 billion by 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 10.1%.

Fibreglass composites are used to make the rotor blades of a particular type of wind turbine called a fibreglass-based wind turbine, which is intended to capture wind energy and produce electricity. Fibreglass composites combine glass fibres with a resin matrix to provide blade strength and stiffness. Fiberglass-based wind turbines are widely used for onshore and offshore wind power production due to their many advantages, including a long shelf life, low maintenance requirements, resistance to corrosion, and a high strength-to-weight ratio. Fiberglass-based wind turbines are widely used for both onshore and offshore applications because of their resilience to severe weather and their capacity to reduce the bulk and loads of the turbine system. Fiberglass-based wind turbines may be designed with a variety of shapes, sizes, and configurations to improve their aerodynamic performance and energy collection. Fiberglass-based wind turbines are among the most widely available variants, alongside carbon fibre-based wind turbines, which are more expensive but also possess superior stiffness and strength.

Key Market Insights:

As fibreglass is so inexpensive, it is the material of choice for producing wind turbine blades. Manufacturers find fibreglass to be an appealing option because of its substantial cost advantage over alternatives such as steel. Statistics show that fibreglass composites are used to produce the great majority of wind turbine blades worldwide. Fibreglass provides an advantageous blend of remarkable strength and low weight. Longer turbine blades that can harness more wind energy will result from this, increasing electricity production in the long run. The average size of wind turbine blades has been rising continuously, and the characteristics of fibreglass are ideal for this development. The market for fiberglass-based wind turbines offers a profitable opportunity in the offshore wind energy segment. Because offshore winds are usually stronger and more consistent, more power may be produced. These are tougher settings that require blades that are both strong and light. Because of its superior performance in these circumstances, fibreglass is a material of choice for offshore wind turbine blades.

Global Fiberglass-based Wind Turbine Market Drivers:

Renewable energy sources are becoming more and more necessary due to economic effectiveness, energy security, and environmental concerns:

Renewable energy sources including wind, solar, hydro, bioenergy, and geothermal energy may be used to generate safe, affordable, and clean electricity for a range of sectors and regions. The usage of fossil fuels to create energy results in the production of greenhouse gas emissions and air pollution. Both health problems and climate change are exacerbated by these pollutants. Renewable energy sources can contribute to greater energy security and energy source diversification since they are less dependent on foreign oil and more robust to supply disruptions. Renewable energy sources may benefit social welfare and sustainable economic growth by creating jobs, reducing energy poverty, and making modern energy services more accessible. Wind power is one of the most advanced and cost-effective renewable energy sources, with more than 700 GW of installed capacity globally. Wind power has several uses in energy generation, including dispersed, hybrid, off-grid, and grid-connected systems.

Technological developments and cost reductions enhance wind power's performance, reliability, and competitiveness:

Innovations in wind turbine design have led to increases in the rotor blades' size, efficiency, and reliability as well as in the gearbox, generator, and nacelle. Additionally, new concepts including modular design, direct drive, and hybrid drive have been created. Technological breakthroughs in the wind turbine manufacturing business include improvements in materials, manufacturing procedures, and component quality assurance. Additionally, supply chain and logistics optimisation are highlighted. Innovations in wind turbine installation technology include new boats, cranes, and methods for assembling and moving the pieces, especially for offshore wind farms. Technological developments in wind turbine operation include improving the systems' condition monitoring, control, and maintenance as well as linking them to the grid and energy markets. Wind turbine design, fabrication, installation, and operating costs are minimised via the use of economies of scale, learning effects, competition, and standardisation. Savings can lower the levelized cost of energy (LCOE) of wind generation and increase its competitiveness with other energy sources.

Global Fiberglass-based Wind Turbine Market Restraints and Challenges:

To fully understand and optimise wind resources, atmospheric research, and airflow at wind farms, precise measurement, modelling, and simulation of the intricate multiscale interactions between the turbulent atmospheric boundary layer (ABL) and the wind turbines and wind farms are required. The diurnal cycle, temperature stratification, synoptic forcing, and topographical complexity all affect the temporal and geographical variability of wind shear, turbulence, speed, and direction. Atmospheric science includes the study of the physical and chemical processes that govern the thermodynamics and dynamics of the ABL as well as the turbulent fluxes of heat, moisture, and contaminants. Airflow in wind farms is impacted by the wake effects of wind turbines, which reduce wind speed and increase turbulence downstream of the rotors, as well as the collective effects of several turbines and rows, which have an impact on the power generation and fatigue loads of wind farms. Understanding and optimising these elements may enhance wind farm design, operation, control, and grid integration, as well as their consequences on society and the environment.

Global Fiberglass-based Wind Turbine Market Opportunities:

The market for wind turbines made of fibreglass is expanding due to a few causes. First off, as we work to reduce our reliance on fossil fuels and combat climate change, demand for renewable energy sources like wind power is growing worldwide. Additionally, fibreglass is less expensive than steel and other rival materials, which attracts wind turbine blade makers. Lastly, fibreglass provides the ideal combination of strength to withstand demanding operational conditions and a lightweight design for longer blades that catch more wind energy. In this market, these elements come together to produce interesting prospects.

FIBERGLASS-BASED WIND TURBINE MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

10.1% |

|

Segments Covered

|

By location of deployment, Capacity, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

China Ming Yang Smart Energy Group Limited, Dongfang Electric Corporation Limited, Envision Energy, General Electric Company, Nordex SE, Shanghai Electric Wind Power Equipment Co., Ltd., Siemens Gamesa Renewable Energy, S.A., Suzlon Energy Limited, Vestas Wind Systems A/S, Xinjiang Goldwind Science & Technology Co., Ltd

|

Global Fiberglass-based Wind Turbine Market Segmentation: By location of deployment

-

Onshore wind turbines

-

Offshore wind turbines

Globally, the onshore sector leads the market for fiberglass-based wind turbines with a higher share. Onshore wind resources are easier to develop and manage, less expensive, more broadly scattered geographically, and more easily available. Onshore wind turbine installations on land. The offshore segment of the worldwide fibreglass-based wind turbine market is growing at the fastest rate. Some of the factors propelling the offshore industry are higher wind speeds, less visual and acoustic interference, fewer land use limitations, and a rise in technological improvements and cost reductions in the design, manufacture, installation, and operation of offshore wind turbines. On the other hand, offshore wind farms are in lakes, oceans, or other bodies of water.

Global Fiberglass-based Wind Turbine Market Segmentation: By Capacity

-

Small wind turbines

-

Medium wind turbines

-

Large wind turbines

Large wind turbines dominate the global market for fiberglass-based wind turbines. The growth of large wind turbines is being driven by a few factors, including growing utility-scale wind power output demand, technological breakthroughs, and cost reductions in large wind turbine design, construction, installation, and operation, as well as offshore wind development. The market for tiny wind turbines is growing at the fastest rate for fibreglass-based wind turbines. Distributed power is growing in popularity as the demand for off-grid applications such as telecommunications, water pumping, and rural energy increases. Encouraging laws and incentives also help small wind turbines.

Global Fiberglass-based Wind Turbine Market Segmentation: By Region

-

North America

-

Asia-Pacific

-

Europe

-

South America

-

Middle East and Africa

The Asia-Pacific region is home to the biggest market for fibreglass wind turbines. Some of the reasons driving the Asia-Pacific market include the requirement for renewable energy sources, notably wind power, to be included in the mix of power generation; measures to minimise reliance on fossil fuel-based power generation; and legislation about energy efficiency and the reduction of carbon emissions. Europe is seeing the fastest growth in the fibreglass wind turbine industry. A few factors, including a developed and competitive wind power industry, supportive laws and incentives, cost- and technology-cutting measures, and the expansion of offshore wind, are driving the European market. Germany, Spain, France, and the United Kingdom are among the leading countries in the region with significant installed capacity and expanding wind power potential.

COVID-19 Impact Analysis on the Global Fiberglass-based Wind Turbine Market:

The COVID-19 pandemic has had a significant impact on the global wind turbine market, affecting the manufacturing, installation, maintenance, and operation of wind turbines. Supply chains and logistics were interrupted by lockdowns, travel bans, and trade restrictions, which affected the availability and delivery of parts and supplies for wind turbines from other countries, especially China. The social distancing policies, labour shortages, health and safety concerns, legal barriers, and financial constraints all contributed to the postponement or cancellation of the planning, construction, and commissioning of wind farms. Reduction in energy consumption because of a decline in economic and industrial output, which affected wind power producers' and operators' earnings. Operation and maintenance services had to continue since wind energy is essential to providing safe and dependable power to a range of sectors and places. This made certain authorizations, protocols, and safety measures necessary to safeguard the health and safety of the workforce.

Recent Trends and Developments in the Global Fiberglass-based Wind Turbine Market:

The world market for wind turbines made of fibreglass is now going through a phase of innovation and adaptation. Although fibreglass is still the preferred material, important advancements are influencing its future. To meet the needs of ever larger and more powerful turbines, research is focused on enhancing fibreglass composites by pushing for increased strength, durability, and fatigue resistance. The increasing popularity of offshore wind farms, where robust yet lightweight fibreglass blades are essential for withstanding tougher operational circumstances, aligns with this focus on material science. To reduce their negative effects on the environment, eco-friendly fibreglass recycling methods are being developed, yet, due to sustainability concerns. Competition is also growing, with several segments investigating the use of carbon fibre and other substitute materials for high-performance blades. Lastly, for companies that make wind turbine blades, changes in the pricing of raw materials provide even another level of complication. In summary, the market for fiberglass-based wind turbines is changing because of material advancements, adaptability to new uses, and environmental concerns, all while navigating a highly competitive environment.

Key Players:

-

China Ming Yang Smart Energy Group Limited,

-

Dongfang Electric Corporation Limited

-

Envision Energy

-

General Electric Company

-

Nordex SE

-

Shanghai Electric Wind Power Equipment Co., Ltd.

-

Siemens Gamesa Renewable Energy, S.A.

-

Suzlon Energy Limited

-

Vestas Wind Systems A/S

-

Xinjiang Goldwind Science & Technology Co., Ltd