Electronic-Grade Polysilicon Market Size (2024 –2030)

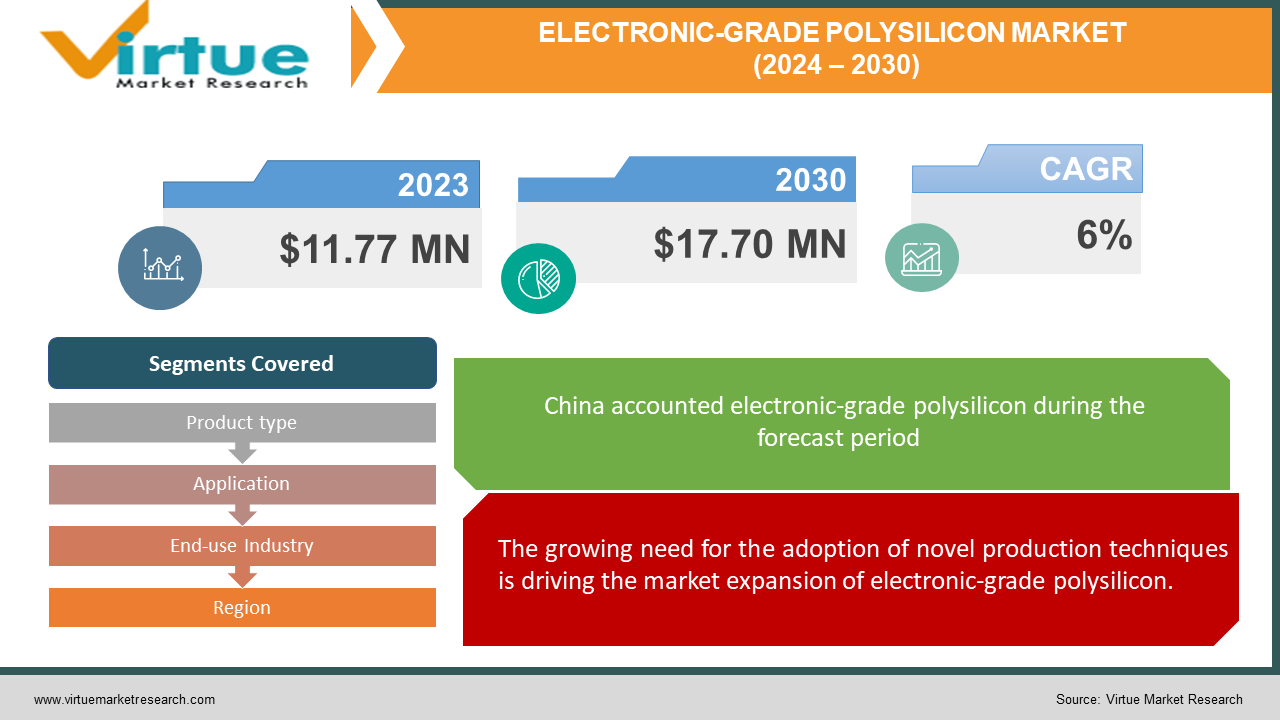

In 2023, The Electronic-Grade Polysilicon Market was valued at USD 11.77 Million and is projected to reach a market size of USD 17.70 Million by 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 6%.

Electronic-grade polysilicon, also known as polycrystalline silicon, is a highly pure variety of silicon that is extensively utilized in semiconductor circuits and devices. It is valued for its semiconductor qualities and is frequently utilized in the electronics and solar energy sectors. The Siemens process, the FBR method, and the enhanced metallurgical grade process are the three primary commercial production methods for polysilicon. Granular polysilicon is produced by the FBR process, whereas rod-shaped polysilicon is produced by the Siemens process. There are two types of silicon: electronic-grade, which is used to make integrated circuits, power devices, optics, and microelectromechanical systems (MEMSs), and solar-grade, which is used to make photovoltaic cells.

Key Market Insights:

The market share of monocrystalline silicon accounts for around 70% of the total electronic-grade polysilicon demand, while multicrystalline silicon accounts for the remaining 30%. The average price of electronic-grade polysilicon ranges from $15 to $25 per kilogram, depending on the purity level and supply-demand dynamics.The global production capacity of electronic-grade polysilicon is estimated to be around 500,000 metric tons per year. The top five producers of electronic-grade polysilicon account for approximately 80% of the total market share.

Global Electronic-Grade Polysilicon Market Drivers:

The growing need for the adoption of novel production techniques is driving the market expansion of electronic-grade polysilicon.

As the capacity for producing polysilicon expands quickly in the upcoming years, there might be an excess of the material. As a result, manufacturers of electronic-grade polysilicon will need to simplify their operations and cut expenses. Businesses employ silane gas as a precursor in the production of polysilicon, resulting in a closed-loop process that lowers costs, improves environmental quality, and saves time. Ultra-high purity hydrogen purifiers are used by polysilicon factories that supply the global electronic-grade market to eliminate common pollutants like methane and nitrogen. Large gas plants are the primary producers of trichlorosilane (TCS) gas, which is used to make semiconductor-grade polysilicon. This gives businesses greater flexibility to compete in the market for electronic-grade polysilicon. Generally, it is anticipated that the market will grow during the forecast period due to the adoption of innovative manufacturing techniques.

A contributing factor to the increase in demand for electronic-grade polysilicon is the growing popularity of electric and hybrid vehicles (HEVs).

High-purity polysilicon is an essential component of many semiconductor devices and sensors found in electric and hybrid electric vehicles (HEVs). Power semiconductors, such as insulated-gate bipolar transistors (IGBTs) and metal-oxide-semiconductor field-effect transistors (MOSFETs), are made of polysilicon and are essential for managing power conversion and distribution in EVs and HEVs. Polysilicon is also used in the production of microelectromechanical systems (MEMS) sensors, which track the performance and safety of vehicles. Examples of these sensors include pressure, gyroscopes, and accelerometers.

Electronic-Grade Polysilicon Market Challenges and Restraints:

The photovoltaic (PV) industry is the main consumer of polysilicon since it uses it to create solar cells and modules. The PV industry is impacted by several factors, including market incentives, government regulations, technological developments, and environmental concerns. Variations in the growth of the PV market in various nations and regions may have an impact on the demand for polysilicon. For instance, global PV demand and polysilicon prices fell sharply in 2018 when China lowered its PV installation targets and subsidies. The amount of polysilicon that is available is determined by the production capacity of polysilicon. There may be an excess of polysilicon if production capacity grows too quickly or isn't used to its full potential, which would reduce prices and benefit producers. The dynamics of the PV sector and the polysilicon industry both affect the balance between supply and demand for polysilicon. Due to trade restrictions, supply issues, and the high demand for photovoltaics, the supply of polysilicon is currently limited. This could alter in the future, though, if more polysilicon plants come online and boost supply.

Electronic-Grade Polysilicon Market Opportunities:

There are numerous prospects for expansion and innovation in the market for electronic-grade polysilicon. A significant prospect is the growing need for polysilicon in the solar energy industry, which is being propelled by worldwide endeavors towards sustainable energy and the growth of solar power infrastructure. Manufacturers of polysilicon can benefit from this trend as governments and businesses place a higher priority on clean energy solutions by increasing production capacity and efficiency to fulfill the rising demand for solar cells and modules. There is also the semiconductor industry, where the production of sophisticated semiconductor devices used in 5G networks, AI applications, IoT devices, and cloud computing systems requires electronic-grade polysilicon. High-grade polysilicon will continue to be in high demand as these technologies develop and grow. Furthermore, polysilicon manufacturers have the chance to increase their market share and become more competitive thanks to advancements in manufacturing processes, such as improved purification methods and lower production costs. All things considered, the market for electronic-grade polysilicon presents encouraging prospects for expansion and innovation, propelled by the growing uptake of renewable energy sources and advances in semiconductor technologies.

ELECTRONIC-GRADE POLYSILICON MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

6% |

|

Segments Covered

|

By Product type, Application, End-use Industry, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Wacker Chemie, Tokuyama Corporation, Hemlock Semiconductor, Mitsubishi, Sinosico, GCL-Poly Energy, OCI, Huanghe Hydropower, Yichang CSG, REC Silicon

|

Global Electronic-Grade Polysilicon Market Segmentation: By Product Type

-

Grade I Polysilicon

-

Grade II Polysilicon

-

Grade III Polysilicon

Using the Siemens method, which achieves extremely high purity levels exceeding 99.999999% (9N) by chemical vapor deposition (CVD) of silane gas on thin silicon rods, grade I polysilicon is made. The primary application of this kind of polysilicon is the production of large, sophisticated 300mm-diameter semiconductor wafers for high-performance electronics like memory chips and microprocessors. The market for electronic-grade polysilicon is anticipated to be dominated by grade I polysilicon because of its remarkable purity and wide application in the semiconductor sector. By employing the fluidized bed reactor (FBR) method, which involves gas-phase deposition of silane gas on silicon grains in a fluidized bed, grade II polysilicon can be produced with purity levels higher than 99.99999% (10N). Smaller and less complicated 200mm wafers, used in gadgets like RFID tags, smart cards, and solar cells, are usually made from grade II polysilicon. Demand for grade II polysilicon is anticipated to rise quickly as a result of reduced production costs, enhanced efficiency, and growing use in the solar energy industry.

Global Electronic-Grade Polysilicon Market Segmentation: By Application

-

300-mm Wafer

-

200-mm Wafer

-

Others

The demand for electronic-grade polysilicon is expected to rise significantly for 200-mm wafers due to increased demand from the solar energy sector, improved efficiency, and lower manufacturing costs. The solar energy sector is growing rapidly because of cost-effectiveness, government regulations, technological advancements, and environmental concerns. On the other hand, due to their high quality, high purity, and widespread application in the semiconductor industry, 300-mm wafers are expected to rule the electronic-grade polysilicon market. The Internet of Things (IoT), cloud computing, 5G, artificial intelligence (AI), and other technological advancements are driving demand for semiconductors.

Global Electronic-Grade Polysilicon Market Segmentation: By End-use Industry

-

Automotive

-

Aerospace

-

Solar Energy

-

Electronics

-

Others

Since solar energy is now more affordable to produce, more efficient, and in greater demand for solar power projects, the global market for electronic-grade polysilicon is predicted to grow rapidly. Environmental concerns, governmental laws, technical developments, and declining solar energy production costs are the main drivers of this growth. Because of its high purity, excellent quality, and widespread application in the production of semiconductor devices, electronics is anticipated to be the most significant market for electronic-grade polysilicon. The Internet of Things (IoT), cloud computing, 5G, artificial intelligence (AI), and other technological advancements are driving demand for semiconductors.

Global Electronic-Grade Polysilicon Market Segmentation: By Region

-

North America

-

Europe

-

Asia-Pacific

-

South America

-

Middle East and Africa

In terms of both production and consumption, China commands the largest share of the Asia Pacific market for electronic-grade polysilicon. The anticipated growth in the Chinese market over the forecast period can be attributed to heightened investments in the semiconductor, electronics, and solar industries. India's market for electronic-grade polysilicon is anticipated to expand at a significant clip due to the country's burgeoning solar energy sector and well-established semiconductor industry. The demand for electronic-grade polysilicon in North America is high due to the need for better semiconductor devices and sensors for use in electric and hybrid vehicles (EVs). North America's aerospace sector is also making significant investments in cutting-edge technologies, necessitating the use of high-performance semiconductor components and devices.

COVID-19 Impact on the Global Electronic-Grade Polysilicon Market:

The COVID-19 pandemic had a major impact on the market for polysilicon of an electronic grade. The disruption of global supply chains resulted in a decrease in the demand for products related to electronic-grade polysilicon. Due to lockdowns and social distancing measures, consumer spending fell during the pandemic, particularly in the first half of 2020 as people gave priority to essential purchases. In addition to upsetting industrial processes and supply chains, the pandemic also resulted in labor shortages and transportation delays, which delayed production and created a shortage of raw materials. These elements further impacted the market by reducing the supply of products made of electronic-grade polysilicon.

Latest Trend/Development:

There are important trends and advancements in the market for polysilicon of electronic grade right now. One noteworthy development in the solar energy industry is the growing need for polysilicon as a result of the increased use of solar power due to environmental concerns and technological advancements. To meet the needs of the solar industry, producers of polysilicon are being compelled by this demand to increase production capacity and efficiency. Another trend in the semiconductor industry is the growing use of electronic-grade polysilicon, which is driven by the development of high-quality semiconductor materials needed for the Internet of Things (IoT), cloud computing, 5G, and artificial intelligence (AI). Furthermore, continuous advancements in manufacturing processes—such as the use of fluidized bed reactor (FBR) techniques—aim to meet the demand for solar and electronic applications while lowering costs and increasing the purity and efficiency of polysilicon production. All things considered, the market is seeing a shift toward renewable energy sources and improvements in semiconductor technology, which is propelling the industry's ongoing expansion and innovation.

Key Players:

-

Wacker Chemie

-

Tokuyama Corporation

-

Hemlock Semiconductor

-

Mitsubishi

-

Sinosico

-

GCL-Poly Energy

-

OCI

-

Huanghe Hydropower

-

Yichang CSG

-

REC Silicon

Market News: