Dry Steam Power Plant Market Size (2024 – 2030)

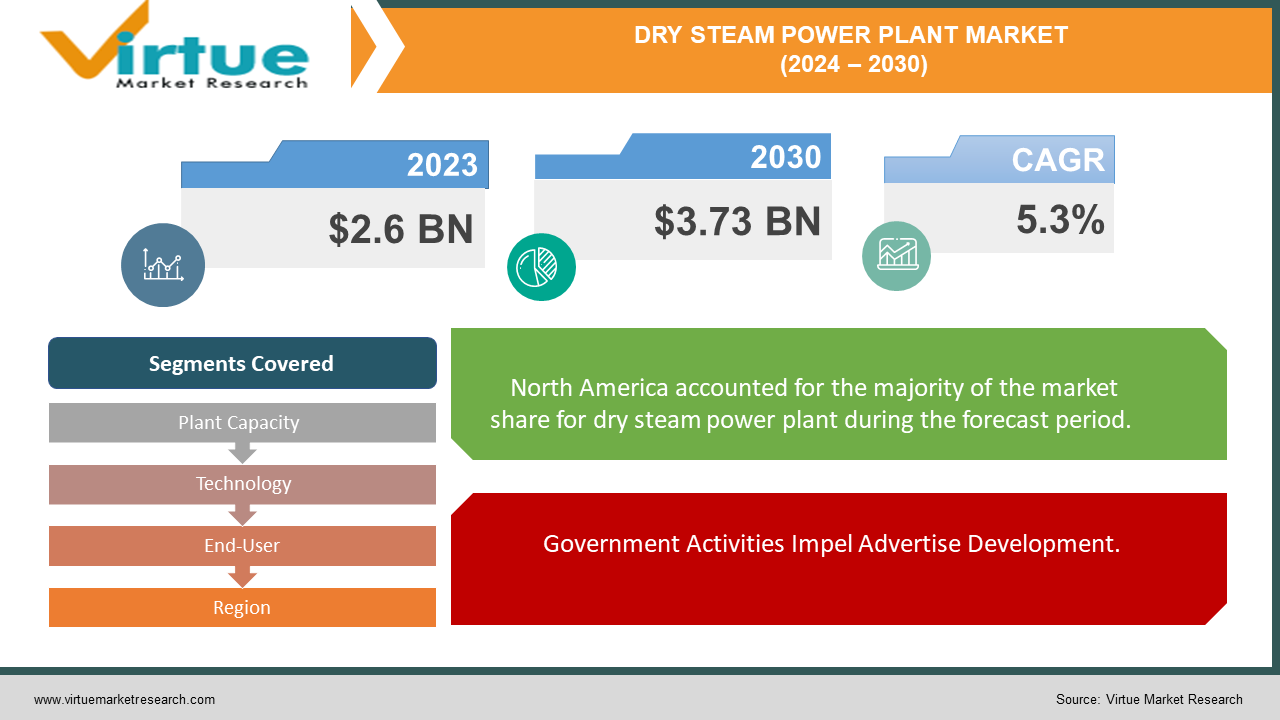

The market for Dry steam power plant market was estimated to be worth 2.6 USD billion in 2023 and is expected to increase to 3.73 USD billion by 2030, with a projected compound annual growth rate (CAGR) of 5.3% from 2024 to 2030.

The dry steam control plant advertises may be an energetic division inside the renewable vitality scene, balanced for unfaltering development and development. Fueled by the Earth's normal geothermal assets, these control plants saddle steam from underground stores to produce power, advertising an economical elective to the conventional fossil fuel-based vitality era. With expanding worldwide awareness of climate alteration and the squeezing to decrease nursery gas emanations, dry steam control plants play a crucial part in the move towards cleaner vitality sources. Showcase flow is driven by variables such as mechanical headways, favorable government approaches advancing renewable vitality appropriation and developing speculations in geothermal vitality foundations. As a result, the showcase has seen considerable extension in later a long time, with critical openings developing over topographical districts, differing end-user fragments, and changing plant capacities. Looking ahead, the advertisement is balanced for proceeded development, fueled by a vigorous compound yearly development rate (CAGR), showing a promising future for partners committed to maintainable vitality arrangements.

Key Insights:

Geothermal power capacity has been steadily rising, with installed capacity reaching 15.4 GW in 2020, marking a significant increase from 12.8 GW in 2015, demonstrating the growing adoption of geothermal energy worldwide.

Governments around the globe are actively promoting the development of geothermal energy through supportive policies and incentives.

For instance, the United States offers Production Tax Credits (PTCs) and Investment Tax Credits (ITCs) for geothermal energy projects, stimulating market growth.

Despite its potential, the dry steam power plant market faces challenges in resource exploration, with only 10% of the world's geothermal potential being tapped.

Improved exploration techniques and investment in resource assessment are crucial to unlocking untapped geothermal reserves.

Global Dry Steam Power Plant Market Drivers:

Government Activities Impel Advertise Development.

Government activities and steady arrangements have risen as significant drivers in impelling the development of the worldwide dry steam control plant showcase. Over different districts, governments are progressively prioritizing renewable vitality sources to moderate climate alteration and diminish reliance on fossil powers. Significant speculations in investigation and advancement, coupled with monetary motivating forces and administrative systems, are incentivizing the sending of dry steam control plants. For occurrence, assess credits and feed-in duties advertised by governments energize private division cooperation and goad speculation in the geothermal vitality framework, driving advertise extension.

Rising Natural Concerns Fuel Appropriation of Clean Vitality Arrangements.

Developing natural concerns, especially related to contamination and carbon emanations, are fueling the appropriation of clean vitality arrangements such as dry steam control plants. With mounting weight to check nursery gas outflows and move towards maintainable vitality sources, there's an increased center on the part of geothermal vitality within the worldwide vitality blend. Dry steam control plants, known for their negligible natural impression and reliable control era, are progressively favored as a dependable and ecologically inviting elective to ordinary fossil fuel-based control era innovations. This drift is anticipated to drive advertising development as businesses and governments look to meet driven climate targets.

Innovative Developments Improve Proficiency and Cost-Competitiveness.

Innovative developments play a significant part in improving the productivity and cost-competitiveness of dry steam control plants, subsequently driving advertise development. Progresses in penetrating procedures, store building, and control plant plans have altogether made strides in the execution and practicality of geothermal vitality ventures. Developments such as double-cycle innovation and improved geothermal frameworks (EGS) have extended the topographical reach of dry steam control plants by tapping into already blocked-off assets and expanding vitality transformation productivity. In addition, progressing inquiries about improvement endeavors pointed at diminishing forthright capital costs and operational costs are assisting in reinforcing the competitiveness of dry steam control plants within the worldwide vitality showcase.

Global Dry Steam Power Plant Market Restraints and Challenges:

Constrained Geothermal Asset Accessibility Postures Imperatives.

The worldwide dry steam control plant showcase faces imperatives due to restricted geothermal asset accessibility, especially in locales with moo geographical action. Despite the noteworthy potential of geothermal vitality, reasonable locales for dry steam control plants are moderately rare, obliging advertise development. Distinguishing reasonable geothermal stores and surveying asset quality stay key challenges, driving geographic restrictions and competition for prime areas. Tending to this imperative requires imaginative investigation procedures and key asset administration to open undiscovered geothermal potential and support advertise development.

Tall Starting Capital Venture Hampers Showcase Entrance.

Tall beginning capital speculation speaks to a noteworthy obstruction to advertise infiltration for dry steam control plants, ruining the far-reaching appropriation of geothermal vitality arrangements. The forthright costs related to boring, plant development, and foundation advancement pose budgetary challenges for financial specialists and extended designers, especially in comparison to routine fossil fuel-based control era innovations. Additionally, the long payback periods and speculation dangers discourage potential partners, constraining advertising development. Overcoming this challenge requires imaginative financing components, government motivating forces, and fetched lessening procedures to upgrade the financial practicality of dry steam control plant ventures and draw-in ventures.

Administrative and Allowing Obstacles Delay Venture Improvement.

Administrative and allowing obstacles pose challenges for venture advancement within the worldwide dry steam control plant advertise, leading to delays and expanded costs. The complex administrative scene, changing allowing prerequisites, and long endorsement forms posture deterrents for engineers, obstructing the convenient execution of geothermal ventures. Moreover, natural affect evaluations and compliance with arrive utilize directions assist contribute to venture delays and vulnerabilities. Streamlining administrative strategies, improving partner engagement, and building up clear allowing systems are fundamental to moderate these challenges and encourage the assisted arrangement of dry steam control plants, in this manner quickening advertise development.

Global Dry Steam Power Plant Market Opportunities:

Constrained Geothermal Asset Accessibility Postures Imperatives.

The worldwide dry steam control plant showcase faces imperatives due to restricted geothermal asset accessibility, especially in locales with moo geographical action. Despite the noteworthy potential of geothermal vitality, reasonable locales for dry steam control plants are moderately rare, obliging advertise development. Distinguishing reasonable geothermal stores and surveying asset quality stay key challenges, driving geographic restrictions and competition for prime areas. Tending to this imperative requires imaginative investigation procedures and key asset administration to open undiscovered geothermal potential and support advertise development.

Tall Starting Capital Venture Hampers Showcase Entrance.

Tall beginning capital speculation speaks to a noteworthy obstruction to advertise infiltration for dry steam control plants, ruining the far-reaching appropriation of geothermal vitality arrangements. The forthright costs related to boring, plant development, and foundation advancement pose budgetary challenges for financial specialists and extended designers, especially in comparison to routine fossil fuel-based control era innovations. Additionally, the long payback periods and speculation dangers discourage potential partners, constraining advertising development. Overcoming this challenge requires imaginative financing components, government motivating forces, and fetched lessening procedures to upgrade the financial practicality of dry steam control plant ventures and draw-in ventures.

Administrative and Allowing Obstacles Delay Venture Improvement.

Administrative and allowing obstacles pose challenges for venture advancement within the worldwide dry steam control plant advertise, leading to delays and expanded costs. The complex administrative scene, changing allowing prerequisites, and long endorsement forms posture deterrents for engineers, obstructing the convenient execution of geothermal ventures. Moreover, natural affect evaluations and compliance with arrive utilize directions assist contribute to venture delays and vulnerabilities. Streamlining administrative strategies, improving partner engagement, and building up clear allowing systems are fundamental to moderate these challenges and encourage the assisted arrangement of dry steam control plants, in this manner quickening advertise development.

DRY STEAM POWER PLANT MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

5.3% |

|

Segments Covered

|

By Plant Capacity, Technology, End-User, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Ormat Technologies, Inc., Mitsubishi Power, Ltd., Toshiba Energy Systems & Solutions Corporation, Enel Green Power, Calpine Corporation, Chevron Corporation, Innergex Renewable Energy Inc., KenGen (Kenya Electricity Generating Company PLC), Terra-Gen, LLC, Energy Development Corporation (EDC), Reykjavik Geothermal, Contact Energy Limited

|

Dry Steam Power Plant Market Segmentation: By Plant Capacity

Within the domain of dry steam control plants, both small-scale and large-scale establishments offer unmistakable focal points, catering to distinctive showcase sections and vitality needs. Be that as it may, when considering adequacy, the large-scale section stands out as especially impactful. Large-scale dry steam control plants ordinarily gloat higher capacity and effectiveness, permitting for considerable power era to meet the requests of utility-scale applications. These establishments advantage of economies of scale, empowering fetched efficiencies in both development and operation stages. Besides, large-scale ventures frequently pull in noteworthy ventures and earn consideration from policymakers due to their potential to contribute altogether to the vitality move and decarbonization endeavors. Also, their sizable yield makes them important resources for lattice soundness and unwavering quality, particularly in locales with tall vitality requests. Whereas small-scale establishments have their merits, the sheer greatness and effect of large-scale dry steam control plants position them as the foremost successful choice for driving considerable renewable vitality selection and making noteworthy strides towards a maintainable vitality future.

Dry Steam Power Plant Market Segmentation: By Technology

-

Traditional Flash steam

-

Newer Binary Cycle

Within the division of dry steam control plants by innovation, the more current parallel cycle stands out as the foremost compelling choice in numerous respects. Not at all like conventional streak steam innovation, which straightforwardly employments high-pressure steam to drive turbines, the twofold cycle innovation works by utilizing lower-temperature geothermal assets to vaporize an auxiliary liquid, ordinarily a natural compound with a lower bubbling point. This liquid vaporizes at lower temperatures, permitting the effective era of power indeed from lower-grade geothermal assets. This innovation offers a few preferences, counting higher vitality transformation efficiencies, expanded operational adaptability, and improved natural supportability due to minimized outflows and potential for reinjection of the auxiliary liquid. Also, double-cycle frameworks are less inclined to erosion and scaling, coming about in diminished support prerequisites and drawn-out hardware life expectancy. As renewable vitality markets proceed to advance and requests for feasible control era arrangements develop, the inventive highlights and predominant performance of double-cycle innovation position it as the foremost viable choice for progressing the capabilities and practicality of geothermal vitality utilization on a worldwide scale.

Dry Steam Power Plant Market Segmentation: By End-User

-

Residential Consumers

-

Utility Companies

When fragmenting the dry steam control plant showcase by end-users, utility companies develop as the foremost viable section due to their critical impact and capacity to drive showcase development. Utility companies ordinarily work on a bigger scale, serving tremendous populations and businesses with their power needs. Dry steam control plants adjusted with utility companies' operations can give a solid and reliable source of baseload control, contributing to framework solidness and assembly of the tall vitality requests of urban and mechanical centers. Moreover, utility companies frequently have the assets and foundation to contribute to and create large-scale geothermal ventures, leveraging economies of scale to optimize costs and maximize proficiency. Moreover, the integration of dry steam control plants into utility company portfolios adjusts with broader vitality move activities, encouraging the move towards a more feasible and strong vitality framework. By focusing on utility companies as key partners, dry steam control plant designers can open noteworthy advertising openings and play a significant part in driving the selection of renewable vitality on a mass scale, eventually quickening the move towards a cleaner and more economical vitality future.

Dry Steam Power Plant Market Segmentation: Regional Analysis

-

North America

-

Europe

-

Asia-Pacific

-

South America

-

Middle East & Africa

Within the worldwide dry steam control plant advertise, territorial dissemination of advertising share outlines a shifted scene of geothermal vitality utilization. North America leads the pack, claiming 40% of the showcase share, driven by its progressed geothermal investigation methods, steady administrative systems, and significant speculation in renewable vitality foundation. Taking closely behind is Europe, capturing 25% of the showcase share, where nations like Iceland and Italy have long grasped geothermal vitality for the heating and power era. Within the energetic Asia-Pacific locale, bookkeeping for 23% of the showcase share, nations such as Indonesia and the Philippines display noteworthy potential for geothermal improvement, fueled by inexhaustible geothermal assets and expanding vitality requests. South America holds an unassuming 7% of the advertising share, with nations like Chile and Peru investigating geothermal openings amid their renewable vitality desire. In conclusion, the Center East and Africa locale contribute 5% of the showcase share, with nations like Kenya and Ethiopia driving the geothermal charge in Africa, whereas the Center East investigates geothermal alternatives to differentiate its vitality blend. In general, these territorial advertising offers highlight the worldwide conveyance of geothermal vitality utilization and imply the differing openings and challenges shown in each locale.

COVID-19 Impact Analysis on the Global Dry Steam Power Plant Market:

The COVID-19 widespread has had a striking effect on the worldwide dry steam control plant showcase, influencing different viewpoints of its supply chain, request flow, and venture timelines. Amid the starting stages of the widespread, broad lockdowns and travel confinements disturbed extended advancement exercises, driving delays in development, allowing, and financing for geothermal ventures. Furthermore, financial instabilities and decreased speculation craving prevented financing for modern ventures, especially in locales intensely affected by the widespread. Be that as it may, as nations continuously recuperate and economies revive, there's a reestablished center on feasible recuperation measures and ventures in a clean vitality framework, counting dry steam control plants. Additionally, the widespread has underscored the significance of flexible and decentralized vitality frameworks, driving intrigue in geothermal vitality as a solid and locally accessible asset. Moving forward, partners within the dry steam control plant showcase are likely to explore advancing showcase elements, leveraging innovative developments, and strong approaches to bounce back from the pandemic's effect and drive maintainable development within the post-COVID period.

Latest Trends/ Developments:

Within the ever-evolving scene of the worldwide dry steam control plant advertise, a few outstanding patterns and advancements are forming the industry's direction. One conspicuous slant is the expanding center on improved geothermal frameworks (EGS) and geothermal asset development. EGS innovations, which include making built stores to extricate warm from hot rocks profound underground, are opening already blocked-off geothermal assets and growing the topographical reach of dry steam control plants. Furthermore, headways in boring strategies, such as directional penetrating and slimhole penetrating, are progressing in investigation effectiveness and decreasing costs, encouraging geothermal asset improvement. Another noteworthy slant is the developing integration of digitalization and shrewd innovations in dry steam control plant operations. Computerized checking and control frameworks, coupled with prescient analytics and machine learning calculations, are optimizing plant execution, upgrading operational effectiveness, and reducing maintenance costs. Moreover, there's an eminent slant towards half-breed geothermal frameworks, combining geothermal vitality with other renewable energy sources like sun-powered and wind to make coordinates and versatile control era arrangements. These patterns emphasize the industry's continuous advancement towards more noteworthy proficiency, supportability, and development, situating dry steam control plants as pivotal donors to the worldwide move towards a low-carbon vitality future.

Key Players:

-

Ormat Technologies, Inc.

-

Mitsubishi Power, Ltd.

-

Toshiba Energy Systems & Solutions Corporation

-

Enel Green Power

-

Calpine Corporation

-

Chevron Corporation

-

Innergex Renewable Energy Inc.

-

KenGen (Kenya Electricity Generating Company PLC)

-

Terra-Gen, LLC

-

Energy Development Corporation (EDC)

-

Reykjavik Geothermal

-

Contact Energy Limited