Digital EMR/Practice Management Market Size (2025 – 2030)

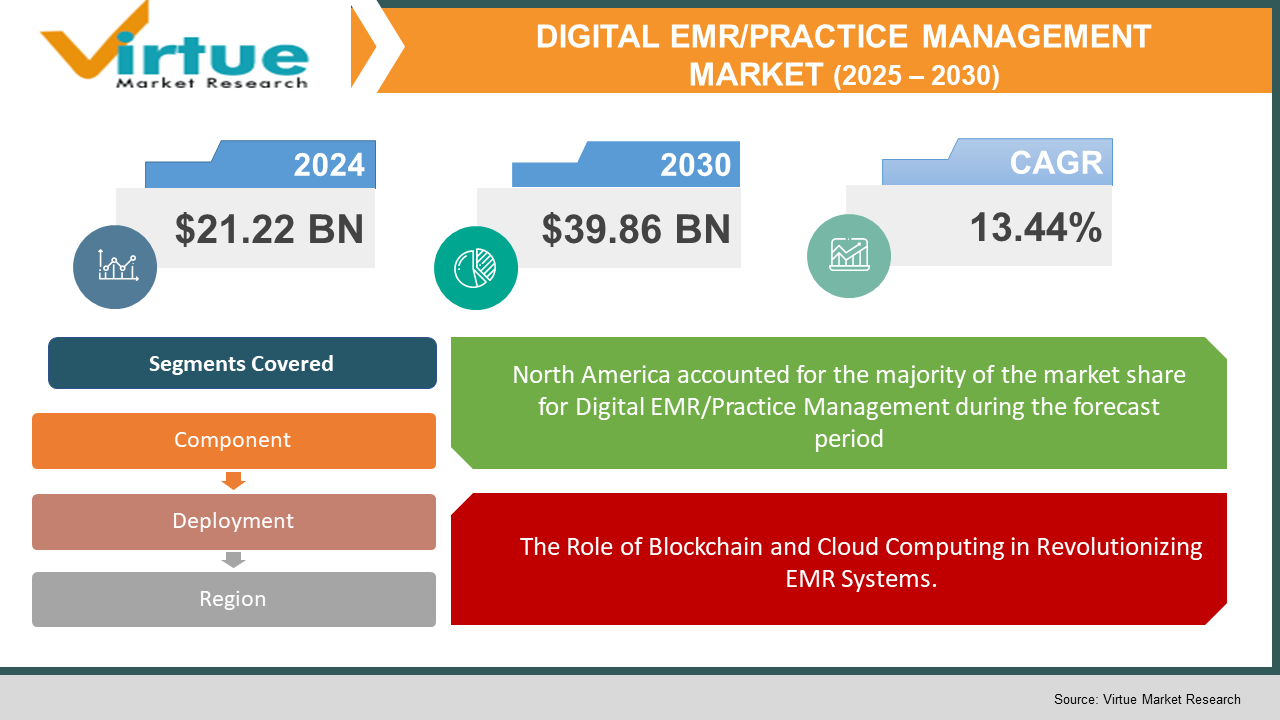

The Digital EMR/Practice Management Market was valued at USD 21.22 billion and is projected to reach a market size of USD 39.86 billion by the end of 2030. Over the forecast period of 2025-2030, the market is projected to grow at a CAGR of 13.44%.

Digital Electronic Medical Records (EMR) and Practice Management (PM) systems have revolutionized healthcare administration, offering streamlined workflow management, enhanced patient care, and improved data accessibility. With increasing digitization in healthcare, providers are investing in automated solutions that reduce administrative burdens while ensuring regulatory compliance. The rising adoption of cloud-based EMR solutions is fuelling market expansion, driven by the need for remote access, data security, and interoperability across healthcare networks. Additionally, government mandates for digital record-keeping and the transition to value-based care are pushing healthcare institutions toward advanced practice management software.

Key Market Insights:

- As per a 2022 report by the Healthcare Information and Management Systems Society (HIMSS), over 85% of hospitals in developed countries have adopted EMR systems, with cloud-based solutions gaining traction due to their scalability and cost-effectiveness. The shift from traditional paper-based records to fully digital workflows is expected to drive continued growth in the market.

- The demand for AI-powered EMR solutions is increasing, with healthcare providers leveraging machine learning and predictive analytics to enhance diagnosis accuracy, treatment planning, and patient monitoring. AI-enabled automation of coding, billing, and documentation is significantly improving practice efficiency.

- In the Asia-Pacific region, the market is witnessing rapid expansion, fueled by government investments in healthcare digitization and a growing number of private healthcare providers implementing digital practice management solutions. Countries such as India, China, and Japan are at the forefront of this digital transformation.

- Interoperability remains a key focus area, with vendors developing cloud-based EMR platforms that seamlessly integrate with insurance databases, telehealth services, and remote patient monitoring systems. Enhanced data-sharing capabilities are expected to improve collaborative healthcare delivery worldwide.

Digital EMR/Practice Management Market Drivers:

The Role of Blockchain and Cloud Computing in Revolutionizing EMR Systems.

Government policies and regulations are playing a crucial role in accelerating the adoption of Digital EMR and Practice Management solutions. Many governments worldwide have mandated the use of electronic health records (EHRs) to improve healthcare accessibility, reduce medical errors, and ensure compliance with data privacy laws such as HIPAA (U.S.), GDPR (Europe), and NDHM (India). Incentive programs such as the U.S. Meaningful Use Program and funding initiatives in Canada, the U.K., and Australia have encouraged hospitals and private practices to transition from paper-based records to digital systems. The growing focus on value-based care is also driving demand for automated patient management solutions that optimize billing, scheduling, and clinical workflows. With the rise of telemedicine, integrated EMR systems now include remote patient monitoring features, ensuring continuity of care. Additionally, the adoption of blockchain technology for enhanced data security and cloud computing for scalable EMR storage is transforming how healthcare providers manage patient records. The ongoing push toward standardized healthcare data exchange protocols, such as FHIR (Fast Healthcare Interoperability Resources), is further improving data interoperability and boosting market growth.

With the advent of AI, there are growing studies and practical research which have pointed out the benefits of integrating AI into Practice Management.

Artificial intelligence is revolutionizing practice management and EMR solutions, enhancing clinical decision support, revenue cycle management, and predictive analytics. AI-driven natural language processing (NLP) is improving clinical documentation automation, reducing the workload on physicians and administrative staff. Moreover, AI-powered chatbots and virtual assistants are being integrated into EMR systems to streamline patient communication, appointment scheduling, and medication reminders. Predictive analytics is enabling proactive patient care by identifying high-risk patients and recommending personalized treatment plans. The expansion of machine learning algorithms in EMR software is also helping in fraud detection, insurance claims management, and real-time data insights, making healthcare more efficient and data-driven.

Digital EMR/Practice Management Market Restraints and Challenges:

The initial implementation costs are high for these systems, and they can be exposed to hacks and other problems, which can result in massive data breaches.

Despite rapid advancements, the Digital EMR and Practice Management Market faces several challenges, including high implementation costs, data security concerns, and system interoperability issues. The initial investment required for software deployment, staff training, and IT infrastructure upgrades can be prohibitive for small and mid-sized healthcare providers. Additionally, cybersecurity threats and data breaches pose significant risks as EMR systems store sensitive patient information. Compliance with stringent data protection laws requires continuous updates and security enhancements, adding to operational costs. Interoperability challenges also persist, as different EMR vendors use proprietary systems, making it difficult for healthcare facilities to share patient records seamlessly. Overcoming these challenges requires industry-wide collaboration, regulatory support, and advancements in standardization protocols to ensure secure and efficient digital healthcare ecosystems.

Digital EMR/Practice Management Market Opportunities:

The growing adoption of cloud-based EMR and practice management software presents a major opportunity for market expansion. Cloud solutions offer scalability, cost efficiency, and real-time data access, making them an attractive option for small and mid-sized healthcare providers that previously struggled with high implementation costs. Additionally, AI-driven automation in practice management is improving clinical documentation, medical billing, and decision support, allowing healthcare providers to focus more on patient care rather than administrative tasks. The demand for AI-powered chatbots, virtual assistants, and predictive analytics in EMR platforms is increasing, further driving innovation in the industry. The push for interoperability in healthcare IT is creating opportunities for vendors that can develop standardized, secure, and compliant EMR solutions. Government-backed initiatives such as FHIR (Fast Healthcare Interoperability Resources) and HL7 standards are paving the way for seamless health data exchange between hospitals, clinics, and insurers.

DIGITAL EMR/PRACTICE MANAGEMENT MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2024 - 2030

|

|

Base Year

|

2024

|

|

Forecast Period

|

2025 - 2030

|

|

CAGR

|

13.44%

|

|

Segments Covered

|

By component, deployment, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Epic Systems Corporation , Cerner Corporation , Allscripts Healthcare Solutions, Inc. , Athenahealth, Inc. , NextGen Healthcare, Inc. , eClinicalWorks , Meditech , GE Healthcare , Philips Healthcare , McKesson Corporation

|

Digital EMR/Practice Management Market Segmentation:

Digital EMR/Practice Management Market Segmentation: By Component

The market is segmented into software and services, with software solutions accounting for the largest share due to the increasing adoption of electronic medical records (EMRs) and practice management software. These solutions enable healthcare providers to digitize patient records, streamline administrative tasks, and improve billing efficiency. Advanced software platforms now incorporate AI-driven analytics, clinical decision support systems (CDSS), and interoperability features, enhancing the overall efficiency of healthcare operations. Services, including installation, training, maintenance, and cloud hosting, are also witnessing growing demand as healthcare providers seek customized solutions, data migration support, and continuous software upgrades to comply with evolving regulatory requirements.

Digital EMR/Practice Management Market Segmentation: By Deployment

The cloud-based segment is experiencing rapid growth due to its cost-effectiveness, scalability, and remote accessibility. Cloud-based EMR solutions allow healthcare providers to access patient data securely from any location, making them ideal for telehealth and multi-location healthcare facilities. Additionally, cloud solutions reduce the need for expensive on-site infrastructure, making them attractive to small and mid-sized clinics.

On the other hand, on-premises solutions remain a preferred choice for large hospitals and healthcare networks that require full control over data security, customization, and compliance with strict data privacy regulations. However, with advancements in cloud security and AI-driven cybersecurity measures, cloud-based solutions are expected to dominate the market in the coming years.

Digital EMR/Practice Management Market Segmentation: Regional Analysis:

- North America

- Asia-Pacific

- Europe

- South America

- Middle East and Africa

North America holds the largest market share in the Digital EMR/Practice Management industry, driven by high adoption rates of healthcare IT solutions, strong regulatory frameworks, and government-backed digitization initiatives. The United States and Canada lead the region, with widespread implementation of electronic health records (EHRs) and AI-integrated practice management software. Government initiatives such as the HITECH Act and Meaningful Use Program have accelerated EMR adoption, while ongoing investments in interoperability and AI-driven analytics continue to drive growth. Similarly, Europe is a mature market, with countries like Germany, the UK, and France advancing healthcare digitization through cloud-based EMR solutions, AI-driven automation, and cross-border health data exchange initiatives. Strict GDPR regulations ensure that data security and privacy remain a top priority in the region.

The Asia-Pacific region is expected to grow at the fastest CAGR, fuelled by government-led healthcare reforms, increased investment in digital infrastructure, and rising demand for AI-powered practice management solutions. Countries like India, China, and Japan are witnessing rapid adoption of cloud-based EMR systems, driven by the need to enhance healthcare accessibility in rural and underserved areas. South America is also emerging as a potential growth market, with countries such as Brazil and Mexico investing in digital health records and telemedicine platforms. In the Middle East & Africa, digital transformation is gaining traction, particularly in the United Arab Emirates and Saudi Arabia

COVID-19 Impact Analysis on the Digital EMR/Practice Management Market

The COVID-19 pandemic significantly accelerated the adoption of Digital EMR and Practice Management solutions as healthcare providers faced an urgent need for remote patient monitoring and telehealth integration. Cloud-based EMR adoption surged, enabling hospitals and clinics to manage virtual consultations and remote diagnostics efficiently. Governments worldwide introduced funding initiatives to support digital transformation in healthcare, further boosting market growth. However, the pandemic also exposed cybersecurity vulnerabilities in digital healthcare systems, leading to increased investments in data protection measures. The demand for AI-powered predictive analytics in EMRs grew, allowing healthcare providers to track and manage COVID-19 cases, vaccine distribution, and patient outcomes more effectively. Post-pandemic, the reliance on cloud-based, AI-integrated practice management systems continues to grow, ensuring long-term market expansion.

Trends/Developments:

With the rise of telemedicine and home-based healthcare, EMR providers are increasingly integrating remote patient monitoring (RPM) and virtual consultation features into their platforms. The adoption of IoT-enabled biometric devices, such as wearable ECG monitors and smart glucose sensors, is further driving demand for real-time data integration within EMR systems. Healthcare providers can now track patient vitals remotely, improving chronic disease management and reducing hospital visits.

With the rise of telemedicine and home-based healthcare, EMR providers are increasingly integrating remote patient monitoring (RPM) and virtual consultation features into their platforms. The adoption of IoT-enabled biometric devices, such as wearable ECG monitors and smart glucose sensors, is further driving demand for real-time data integration within EMR systems.

Oracle’s acquisition of Cerner aims to drive AI-based automation and advanced analytics in digital healthcare management. Athenahealth and NextGen Healthcare are expanding their cloud-based EMR offerings, targeting small and mid-sized healthcare providers.

Key Players:

- Epic Systems Corporation

- Cerner Corporation

- Allscripts Healthcare Solutions, Inc.

- Athenahealth, Inc.

- NextGen Healthcare, Inc.

- eClinicalWorks

- Meditech

- GE Healthcare

- Philips Healthcare

- McKesson Corporation