Asia Pacific Smoothies Market

The Asia Pacific smoothies’ market is expected to grow from approximately USD 4.5 billion in 2025 to around USD 8.5 billion in 2030, at a compound annual growth rate of around 12.8% during 2025-2030.

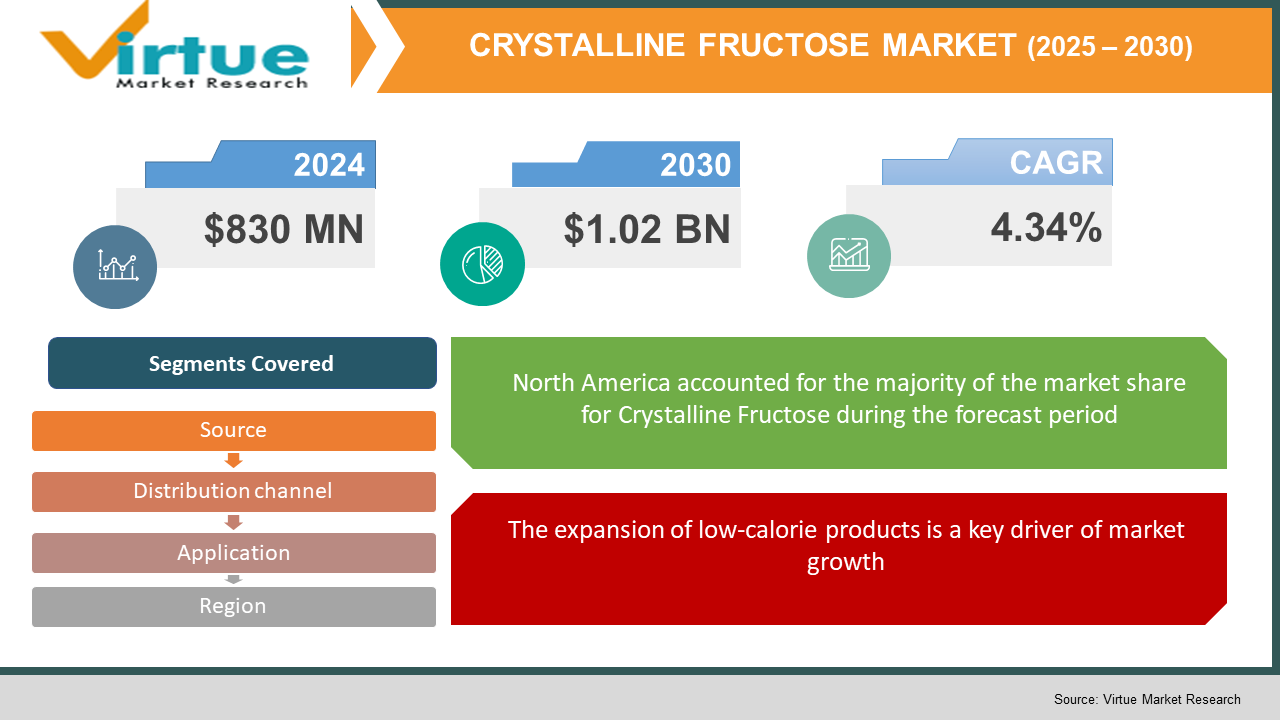

Explore reportThe Crystalline Fructose Market was valued at USD 830 million in 2024. Over the forecast period of 2025-2030, it is projected to reach USD 1.02 billion by 2030, growing at a CAGR of 4.34%.

Crystalline fructose is a naturally occurring sugar derived from fructose, present in fruits and honey. It is created through the fermentation process of glucose and has a white, crystalline granular form. Being sweeter than sucrose, it is commonly utilized as a sweetener in various food and beverage products. It provides advantages such as a lower glycemic index, moisture retention, and enhanced flavor and texture.

Crystalline Fructose Market Drivers:

Initiatives focused on sugar reduction are significantly driving the growth of the market.

Sugar reduction initiatives are accelerating as food and beverage companies adapt to regulatory pressures and the increasing consumer demand for healthier alternatives. With the rise in obesity and related health concerns, manufacturers are reformulating their products to reduce sugar content.

Crystalline fructose has gained popularity as an effective sugar substitute, offering enhanced sweetness that allows for the use of smaller quantities while preserving flavor. This shift not only enables companies to meet regulatory requirements but also aligns with consumer preferences for lower-calorie and healthier products.

The expansion of low-calorie products is a key driver of market growth.

The retail market for low-calorie and reduced-sugar products is expanding rapidly as more health-conscious consumers seek healthier alternatives. Crystalline fructose, a natural sweetener, is becoming increasingly popular in a variety of applications, including beverages, snacks, and desserts, to meet this growing demand. Its higher sweetness level allows manufacturers to use smaller amounts, effectively reducing overall sugar content while preserving flavor. For example, Coca-Cola's "Coca-Cola Life," which is sweetened with a combination of cane sugar and stevia, often includes crystalline fructose in similar formulations to lower the calorie count while maintaining the desired sweetness.

Crystalline Fructose Market Restraints and Challenges:

Health concerns related to the excessive consumption of sugar and artificial sweeteners are restraining market growth.

Studies linking high fructose intake to a range of health issues, including obesity, diabetes, and metabolic disorders, have heightened consumer concerns. These apprehensions have prompted increased scrutiny from health organizations and regulatory bodies. Consequently, some food and beverage manufacturers are exercising caution when incorporating fructose into their products, which may hinder market growth. This growing caution is driving the search for alternative sweeteners that offer similar benefits without the associated health risks.

Crystalline Fructose Market Opportunities:

The shift toward organic and clean-label products is creating significant opportunities in the market.

The rising consumer preference for organic and clean-label products presents a substantial opportunity for the crystalline fructose market. As consumers become more health-conscious and environmentally aware, there is a growing demand for natural, organic sweeteners. Manufacturers can leverage this trend by creating organic crystalline fructose products and highlighting their natural origins. This shift aligns with the clean-label movement, offering opportunities for market expansion within premium product categories and appealing to health-conscious consumers who prioritize transparent ingredient lists.

Regulatory support for sugar reduction is creating significant opportunities in the market.

As governments and health organizations recognize the health risks linked to excessive sugar consumption, such as obesity and diabetes, initiatives aimed at reducing sugar intake are gaining momentum. These efforts encourage food and beverage companies to reformulate their products to lower sugar content.

This supportive regulatory environment fosters the adoption of alternatives like crystalline fructose, which provides a sweeter taste with fewer calories. As companies respond to these guidelines, crystalline fructose is becoming an appealing option for creating healthier products that align with public health objectives and meet consumer demand for better-for-you choices.

CRYSTALLINE FRUCTOSE MARKET REPORT COVERAGE:

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 - 2030 |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2030 |

|

CAGR |

4.34% |

|

Segments Covered |

By Source, application, Distribution Channel and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regional Scope |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Key Companies Profiled |

Tate & Lyle, Now Foods and Shijiazhuang Huaxu Pharmaceutical Co. Ltd. |

Crystalline Fructose Market Segmentation:

Corn is the dominant source in the crystalline fructose industry due to its high availability and cost-effectiveness. The widespread cultivation of corn ensures a reliable supply of raw materials, essential for large-scale production. Its high starch content is effectively converted into fructose through enzymatic hydrolysis, making it an ideal source. The well-established infrastructure for corn processing, including advanced technologies and robust supply chains, further strengthens its market position. Moreover, corn-based fructose benefits from economies of scale, which help reduce production costs and enable competitive pricing. These economic advantages and extensive use make corn the leading source in the crystalline fructose market.

The food and beverage sector dominates the crystalline fructose market due to its strong demand for low-calorie, high-intensity sweeteners. Crystalline fructose's superior sweetness and low glycemic index make it an ideal ingredient for enhancing the flavor of various products, including soft drinks, baked goods, and processed foods. Its ability to deliver a sweeter taste with fewer calories aligns perfectly with consumer preferences for healthier options. The sector's substantial growth, driven by increasing health awareness and the push for reduced sugar content, further strengthens crystalline fructose's key role in product formulations and supports market expansion.

The dominance of the offline distribution channel in the crystalline fructose industry can be attributed to its strong presence in traditional retail environments. Supermarkets, hypermarkets, and specialty stores offer direct access to a wide consumer base, making them essential channels for distributing crystalline fructose products. These outlets enable in-store promotions and provide consumers with the opportunity to make immediate purchasing decisions. Furthermore, well-established relationships between manufacturers and distributors ensure consistent product availability and support. While online shopping continues to grow, the offline channel remains crucial due to its extensive reach and ability to cater to consumers who prefer shopping in physical stores.

North America leads the crystalline fructose market, driven by its well-established food and beverage industry, which generates significant demand for low-calorie sweeteners. The region’s high consumer awareness and growing preference for healthier alternatives to traditional sugars contribute to this demand. Advanced technological infrastructure enables efficient production and continuous innovation in crystalline fructose manufacturing. Additionally, North America's strong regulatory framework ensures product safety and quality, enhancing consumer confidence. Major industry players in the region benefit from robust distribution networks and substantial investments in research and development, further cementing North America's dominance in the market.

The Asia Pacific region holds the second-largest market share for crystalline fructose, primarily due to its increasing use in pharmaceuticals and the food and beverage industry. China leads the market due to the presence of key industry players and the country's large population, while India is the fastest-growing market, driven by innovative production techniques and rising income levels. The growth of the food and beverage sector in the region, along with a rising demand for low-calorie and nutritional supplements, has significantly boosted the demand for crystalline fructose, with expectations for continued market expansion in the region.

The global COVID-19 pandemic, which began in early 2020, significantly disrupted the global economy and had a negative impact on the growth of the food and beverage industry. Food manufacturers scaled back the production of many major food products, while the sales of food service restaurants plummeted as consumer demand for outside food diminished. The production of crystalline fructose, primarily derived from corn, was also adversely affected as trade activities and the processing of agricultural products were halted to curb the spread of the virus. As a result, the COVID-19 outbreak led to a moderate disruption in the movement of food-grade crystalline fructose.

Latest Trends/ Developments:

In January 2023, Universal Biosensors, Inc. launched the fourth test on its Sentia wine testing platform, the fructose biosensor test. This test measures the amount of sugar available to yeast for conversion into ethanol, with glucose and fructose levels serving as key indicators of grape quality.

In September 2022, Cargill opened a corn wet mill in Pandaan, Pasuruan, Surabaya, Indonesia, with an investment of USD 100 million (IDR 1.3 trillion). This facility is designed to meet the increasing demand for starches, sweeteners, and feed products in the Asian and Indonesian markets. The mill is also expected to provide a significant economic boost to the local community by creating up to 4,000 new jobs and employment opportunities.

These are top 10 players in the Crystalline Fructose Market :-

The demand for crystalline fructose is predominantly fueled by its widespread use in the food and beverage sector, where it serves as a key sweetener and functional ingredient.

The top players operating in the Crystalline Fructose Market are - Tate & Lyle, Now Foods and Shijiazhuang Huaxu Pharmaceutical Co. Ltd.

The global COVID-19 pandemic, which began in early 2020, significantly disrupted the global economy and had a negative impact on the growth of the food and beverage industry.

The shift toward organic and clean-label products is creating significant opportunities in the market.

The Asia Pacific is the fastest-growing region in the Crystalline Fructose Market.

Joining thousands of companies around the world committed to making the Excellent Business Solutions.

Specify your preferred Countries, Segments, or timeframes

Unlock Country Level Outlook, Trends, Cross-country Comparability, or supply Chain Variations.

Analyst Support

Every order comes with Analyst Support.

Customization

We offer customization to cater your needs to fullest.

Verified Analysis

We value integrity, quality and authenticity the most.