Global Competitive Intelligence Software Market Size (2023 – 2030)

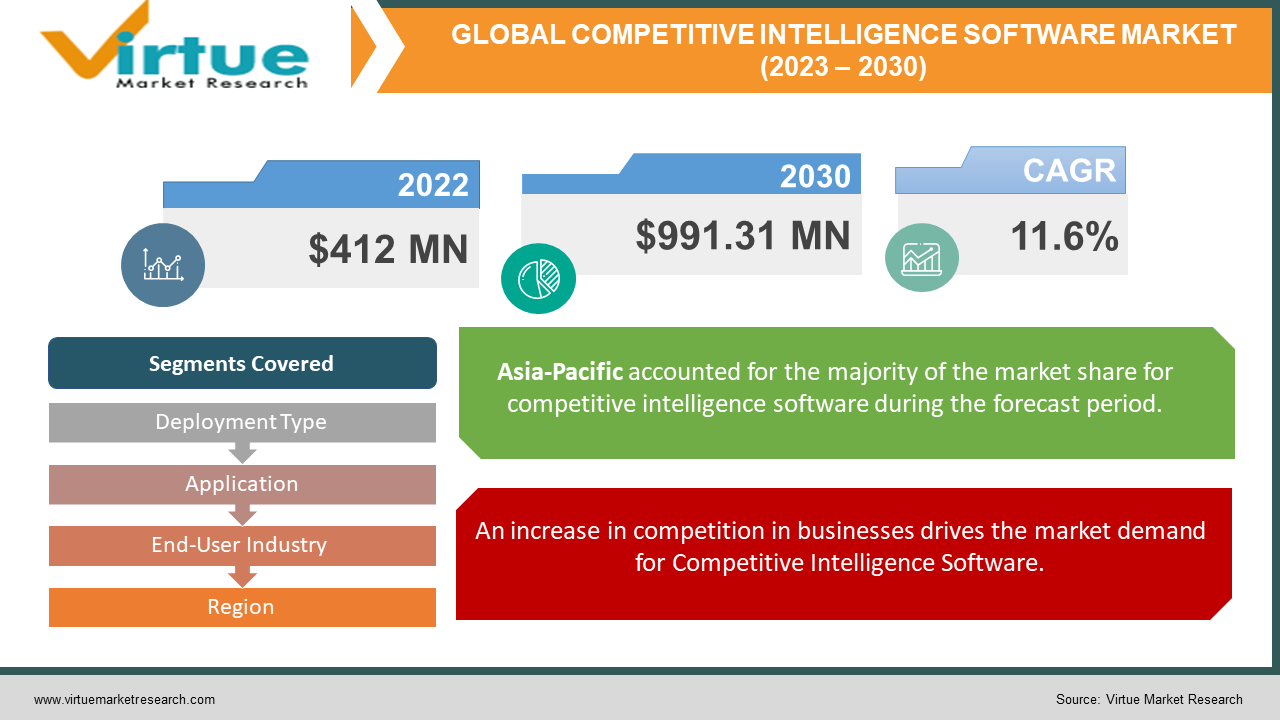

The Global Competitive Intelligence Software Market was valued at USD 459.79 Million and is projected to reach a market size of USD 991.31 Million by the end of 2030. Over the forecast period of 2024-2030, the market is projected to grow at a CAGR of 11.6%.

Earlier, in businesses, there was a great need to gather and analyze large amounts of data and this led to competitive intelligence software solutions. Competitive intelligence software plays an important role in the decision-making of businesses with valuable insights. Technological advancements in competitive intelligence software make it easier to gather, analyze, or interpret data using the latest software. Artificial intelligence and machine learning in competitive intelligence software enhance the analysis faster and help to increase business profit. In the future, with AI predictive analytics, it will be easier to predict market trends with greater accuracy. Key players in this market are Crayon, Klue, Cipher, Contify, and Kompyte

Key Market Insights:

According to a study, there is a 68% increase in business profitability with competitive intelligence Software. With the integration of the latest technologies, competitive intelligence software helps in 82% faster decision-making among industry leaders. Also, 95% of businesses report gaining a competitive edge using CI Software. In 2022, based on market segmentation by deployment type, Cloud-based CI software occupies the highest share of the market. In 2022, based on market segmentation by application, Market Intelligence occupied the highest share of the market at around 47%. In 2022, based on the end-user industry, the "IT and Telecom" segment occupies the highest market share about 30% of the market and the fastest-growing segment in terms of revenue is expected to be the healthcare industry. In 2022, North America occupies the highest share of about 40% of the market and Asia-Pacific is the fastest-growing segment during the forecast period due to growing digitalization and adoption of technology.

Competitive Intelligence Software Market Drivers:

An increase in competition in businesses drives the market demand for Competitive Intelligence Software.

The business landscape is becoming more complex and competitive. With changing consumer behavior, market trends are also changing. There is greater competition in the market as more and more businesses are emerging. This creates a demand for competitive intelligence software. It helps businesses to understand the latest market trends and helps them to make more profit-gaining decisions. Also, the latest competitive intelligence software tools help to gather, analyze, and interpret data on their competitors. In this way, they can stay ahead in this competitive environment.

Technological Advancements and Integration of AI have boosted the market for Competitive Intelligence Software

Recent technological innovations have transformed the Competitive Intelligence Software market. Technological integration with AI led to advanced predictive analytics with greater accuracy. This helps the business to make more profit-gaining decisions with these valuable insights. With AI, it is easier to gather large amounts of data and analyze them more efficiently and quickly. Continuous development and research can lead to more advanced competitive intelligence software. With the advent of technologies, the market is anticipated to witness significant growth in the coming years.

Competitive Intelligence Software Market Restraints and Challenges

The major challenge faced by the Competitive Intelligence Software market is the data privacy and compliance concerns. Competitive Intelligence involves gathering data from external sources and should follow data regulation rules. Data protection regulations like GDPR, CCPA, and others can be complex and time-consuming for companies. Managing large amounts of data available is challenging. Companies may face legal issues if data extraction and data protection are not regulated. Another challenge is the high cost of competitive intelligence software which affects small businesses.

Competitive Intelligence Software Market Opportunities:

The Competitive Intelligence Software market has various opportunities in the market. With the advent of technologies and integration with AI, the market is anticipated to witness significant growth in the coming years. Advanced predictive analytics with greater accuracy helps the business to make more profit-gaining decisions with valuable insights. With AI, it is easier to gather large amounts of data and analyze them more efficiently and quickly. Also, data visualization tools in competitive intelligence software are becoming popular with interactive dashboards. This provides clear, enhanced, and customized report analysis that helps the business make more profit-making decisions and further leads to the demand for Competitive Intelligence Software.

GLOBAL COMPETITIVE INTELLIGENCE SOFTWARE MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2022 - 2030

|

|

Base Year

|

2022

|

|

Forecast Period

|

2023 - 2030

|

|

CAGR

|

11.6%

|

|

Segments Covered

|

By Deployment Type, Application, End-User Industry and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Crayon, Klue, Cipher, Contify, Kompyte, Prisync, Crayon Intel Center, Sentione, IntelliTicks, Klue for Slack

|

Competitive Intelligence Software Market Segmentation: By Deployment Type:

In 2022, based on market segmentation by deployment type, Cloud-based CI software occupies the highest share of the market. It is due to many factors. Cloud-based CI software offers easy scalability, accessibility, and flexibility and enables the business to adapt the changing market conditions. It is easier to use in work-from-home conditions. Many organizations are using cloud-based CI software because of its cost-effectiveness and efficiency in technology.

On-premises CI software is the fastest-growing segment and is growing at a fast CAGR of 20% during the forecast period. Organizations that need strict data privacy and security requirements use On-premises CI software.

Competitive Intelligence Software Market Segmentation: By Application:

-

Market Intelligence

-

Product Intelligence

-

Competitive Benchmarking

-

Sales Intelligence

In 2022, based on market segmentation by application, Market Intelligence occupied the highest share of the market at around 47%. It gives the latest market trends, individual customer behaviors, industrial dynamics, etc. Many organizations require this kind of information so that they can make decisions that help them to get success. It helps in competitive strategy and is essential for businesses to make informed decisions regarding product development, marketing strategies, and overall market positioning.

Sales Intelligence is the fastest-growing segment during the forecast period and is growing at a CAGR of more than 20%. Competitive Intelligence Software involves tools and solutions that provide insights and information to sales teams to help them identify and close deals more effectively.

Competitive Intelligence Software Market Segmentation: By End-User Industry:

-

Healthcare

-

IT and Telecom

-

Manufacturing

-

Financial Services

-

Retail

-

Energy

-

Others

In 2022, the "IT and Telecom" segment occupies the highest market share about 30% of the market. The IT and Telecom industry is highly dynamic and competitive, with constant technological advancements and evolving market trends, and organizations in this sector depend on competitive intelligence software to stay ahead in innovation, pricing strategies, and market trends. Therefore, the demand for competitive intelligence software is crucial in this industry, making it one of the largest segments.

The fastest-growing segment in terms of revenue is expected to be healthcare. The healthcare industry witnessed a digital transformation in electronic health records, telemedicine, and healthcare analytics. Healthcare organizations need data analytics to make informed decisions for patients' treatment and services. Thus, competitive intelligence software plays a vital role in the healthcare industry.

Competitive Intelligence Software Market Segmentation: Regional Analysis:

-

North America

-

Asia-Pacific

-

Europe

-

South America

-

Middle East and Africa

In 2022, North America occupies the highest share of about 40% of the market. North America is a technologically advanced region with nations like the U.S. and Canada. The competition among businesses is pretty high demanding the need for competitive intelligence software. In this region, there are numerous large businesses in technology, healthcare, and finance. Also, the number of startups is increasing rapidly fueling the need for advanced competitive intelligence software.

Asia-Pacific is the fastest-growing segment during the forecast period due to rapid urbanization and industrialization. Growing digitalization and adoption of technology in developing countries like India and Southeast Asian nations drive the demand for competitive intelligence software. Businesses in countries like China strive for market leadership and global expansion creating a huge demand for competitive intelligence software in coming years.

COVID-19 Impact Analysis on the Global Competitive Intelligence Software Market:

The pandemic had a significant impact on the Competitive Intelligence Software market. Businesses had to deal with disruptions, in supply chains changes in customer behavior, and increased competition in the space. This led to a demand for competitive intelligence solutions. Organizations wanted tools that could help them quickly adapt to changing market dynamics keep an eye on competitor strategies and spot opportunities. Additionally, the pandemic accelerated the adoption of cloud-based solutions allowing for work and collaboration. While some industries faced downturns others experienced growth highlighting how important competitive intelligence is, during uncertain times. The Competitive Intelligence Software Market was significantly affected by the COVID-19 pandemic.

Latest Trends/ Developments:

One of the developments, in the Competitive Intelligence Software Market is the rise in the integration of artificial intelligence (AI) and machine learning (ML) capabilities. This advancement empowers businesses to automate the collection of data and improve analytics. Obtain deeper insights from large amounts of information. AI-powered competitive intelligence software enables organizations not to react to market changes but to proactively anticipate competitor actions providing a significant strategic advantage in today's fast-paced and highly competitive business environment. Furthermore, there is an increasing focus on real-time monitoring and alerts enabling companies to remain agile and responsive to shifts in their landscapes. It is important to note that for up-to-date trends and developments, it is recommended to refer to industry reports or specialized sources.

Key Players:

-

Crayon

-

Klue

-

Cipher

-

Contify

-

Kompyte

-

Prisync

-

Crayon Intel Center

-

Sentione

-

IntelliTicks

-

Klue for Slack