Carbon Fiber Printing Materials Market Size (2024 – 2030)

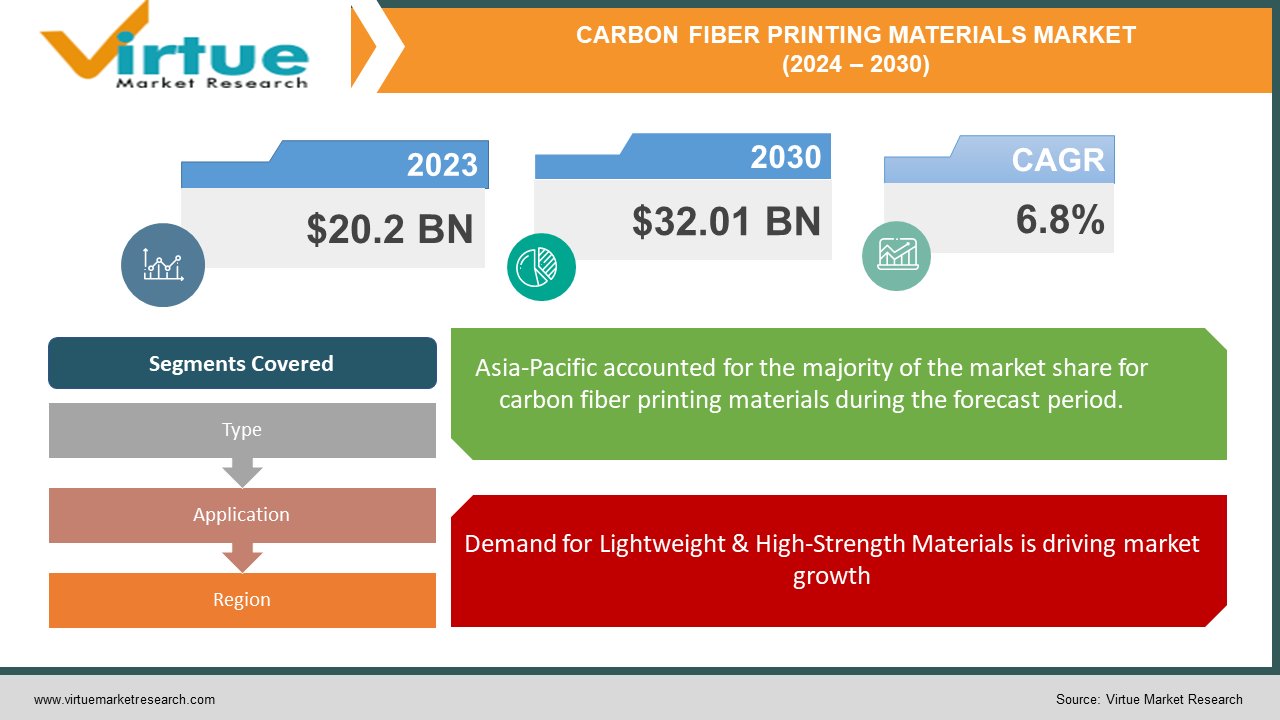

The Global Carbon Fiber Printing Materials Market was valued at USD 20.2 billion in 2023 and will grow at a CAGR of 6.8% from 2024 to 2030. The market is expected to reach USD 32.01 billion by 2030.

The Carbon Fiber Printing Materials Market focuses on materials that combine 3D printing with the superior strength and lightness of carbon fiber. This rapidly growing market offers filaments with carbon fiber inclusions, boosting the strength and stiffness of 3D printed parts. Used in applications like aerospace components and racing parts, this market is expected to surge due to its ability to create high-performance, functional products through additive manufacturing.

Key Market Insights:

Increasing demand for lightweight and high-strength materials in industries like aerospace, automotive, and sporting goods. Advancements in 3D printing technology enable the precise incorporation of carbon fibers for enhanced performance. Growing adoption of additive manufacturing for prototyping and end-use parts.

The Carbon Fiber Printing Materials Market presents a promising opportunity driven by the synergy between advanced materials and 3D printing technology. Overcoming cost and technical hurdles will be crucial for wider adoption and market expansion.

Global Carbon Fiber Printing Materials Market Drivers:

Demand for Lightweight & High-Strength Materials is driving market growth:

The demand for lightweight, high-performance materials is fueling the growth of carbon fiber printing in multiple sectors. Stringent regulations on fuel efficiency in aerospace and defense industries are pushing for lighter aircraft designs. Here, 3D printing with carbon fiber shines, enabling the creation of complex, high-performance parts that shave off weight without sacrificing strength. Similarly, the automotive industry seeks to shed pounds for better fuel economy and performance. Carbon fiber printing allows car manufacturers to create lighter and stronger components for everything from chassis parts to racing components. Even high-end car bodies can benefit from this technology. Beyond transportation, athletes crave equipment that offers both strength and minimal weight. 3D printing with carbon fiber steps up to the challenge, allowing for the creation of custom-fit, high-performance sporting goods like never before. Bicycle frames with optimized stiffness, baseball bats with improved swing weight, and even prosthetics tailored to individual needs are all becoming a reality thanks to this innovative technology.

Advancements in 3D Printing Technology are driving market growth:

Advancements in 3D printing technology are acting as a major catalyst for the growth of the carbon fiber printing materials market. One key driver is the improvement of printing techniques like Continuous Filament Fabrication (FFF). By overcoming the challenge of handling abrasive carbon fibers, FFF opens the door to wider adoption of this material. Additionally, the exciting development of multi-material printing allows for the creation of parts with a gradient of carbon fiber content within a single print. This opens up a world of possibilities for optimizing both strength and weight distribution in a single component. Imagine a lightweight race car part with a high-carbon fiber core for maximum strength and a lighter composite outer layer to reduce overall weight. Finally, advancements in 3D printing software are playing a crucial role. These improved programs allow engineers to design and optimize parts specifically for carbon fiber printing. This translates to better integration of the carbon fibers within the printed object, leading to parts that are not only strong and lightweight but also perform flawlessly under stress. These combined advancements in printing techniques, material handling, and design software are paving the way for a future where carbon fiber 3D printing becomes a mainstream manufacturing tool.

Growing Adoption of Additive Manufacturing is driving market growth:

3D printing with carbon fiber materials unlocks a new level of manufacturing potential compared to traditional techniques. Unlike traditional methods restricted by subtractive processes (removing material to create a shape), 3D printing offers unparalleled design freedom. Complex geometries, intricate lattice structures, and even internal channels can be printed with ease, leading to lighter and more efficient parts. This is a game-changer for industries like aerospace and sporting goods, where weight reduction is paramount. Furthermore, 3D printing excels at rapid prototyping. Gone are the days of lengthy lead times and expensive tooling changes. With carbon fiber filaments, designers can quickly iterate on prototypes, test new ideas, and refine their creations much faster. This translates to shorter development cycles and quicker time-to-market for innovative products. Finally, 3D printing allows for unmatched customization. Parts can be tailored to specific needs and user requirements. Imagine creating a custom-fit prosthetic limb with optimal strength and flexibility, or a lightweight bicycle frame perfectly designed for an athlete's riding style. By combining the inherent advantages of 3D printing with the superior properties of carbon fiber, manufacturers can create high-performance, functional products for a wide range of applications, pushing the boundaries of what's possible.

Global Carbon Fiber Printing Materials Market challenges and restraints:

High Cost is a significant hurdle for Carbon Fiber Printing Materials:

The high cost of carbon fiber printing materials stems from several factors. First, the raw carbon fibers themselves are expensive to produce. Unlike readily available plastics like PLA or ABS, carbon fiber involves complex processes that convert precursor materials like polyacrylonitrile (PAN) into high-performance fibers. This intricate manufacturing process adds significant cost. Secondly, the specialized equipment needed for printing with carbon fiber adds another layer of expense. Traditional FDM printers may not be suitable, as carbon fibers are abrasive and can damage standard nozzles. Upgraded printers with features like wear-resistant nozzles and heated beds are necessary, driving up the initial investment. Finally, the actual printing process with carbon fiber is often more complex. Printing settings require careful optimization to achieve successful results, and this can involve trial and error, leading to wasted materials and increased printing time. These factors, from the raw materials to the specialized printing setup, all contribute to the significantly higher cost of carbon fiber filaments compared to traditional 3D printing materials.

Technical Complexity is throwing a curveball at the Carbon Fiber Printing Materials market:

The complexity starts with the printer itself. Standard FDM printers might not be up to the challenge. Carbon fibers are highly abrasive, and their tiny, sharp edges can quickly wear down regular nozzles. Upgrading to printers with specialized features like wear-resistant nozzles becomes mandatory. Additionally, heated beds play a crucial role. Uneven cooling can cause warping and cracking in carbon fiber prints, so a heated bed that maintains a consistent temperature throughout the printing process is essential. But the challenges extend beyond the hardware. Optimizing print settings for carbon fiber requires a significant amount of experience and meticulous fine-tuning. Factors like printing temperature, retraction settings, and printing speed need to be carefully adjusted to ensure proper adhesion between layers and prevent filament clogging. This can involve trial and error, leading to wasted filament and numerous failed prints before achieving the desired results. In essence, printing with carbon fiber demands a higher level of technical expertise and user experience compared to working with standard filaments.

Limited Availability of Recycled Materials is a growing nightmare for Carbon Fiber Printing Materials:

The environmental footprint of carbon fiber printing materials is a current hurdle. The majority of filaments use virgin carbon fibers, raising sustainability concerns. Manufacturing virgin carbon fibers is an energy-intensive process, and the large amount of material often discarded during production contributes to waste. This clashes with the growing focus on eco-friendly practices. While carbon fiber itself boasts excellent durability, its use in 3D printing doesn't translate to a particularly sustainable solution at this stage. However, researchers are actively exploring ways to incorporate recycled carbon fiber into printing filaments. This would not only reduce reliance on virgin materials and lessen the environmental impact, but it could also potentially bring down production costs. The challenge lies in developing cost-effective methods for recycling carbon fibers while maintaining their structural integrity for use in filaments. Several mechanical recycling techniques are being investigated, but this area is still in its early stages. If successful methods can be developed, recycled carbon fiber filaments could become a viable option, transforming carbon fiber printing into a more sustainable and attractive manufacturing technology.

Market Opportunities:

The Carbon Fiber Printing Materials Market presents a treasure trove of opportunities for innovative applications and market expansion. The ever-increasing demand for lightweight, high-performance materials across industries like aerospace, automotive, and sporting goods creates a fertile ground for carbon fiber printing. This technology allows for the creation of complex, custom-designed parts with exceptional strength-to-weight ratios, a key factor for improving fuel efficiency and overall performance. Advancements in 3D printing technology further fuel this opportunity. Improved printing techniques like Continuous Filament Fabrication (FFF) with better handling of abrasive carbon fibers enable wider adoption. Multi-material printing opens doors for parts with varying carbon fiber content within a single print, optimizing strength and weight distribution. Software advancements allow for superior design and optimization of parts specifically for carbon fiber printing, maximizing material utilization and performance. Beyond these technical advancements, the inherent advantages of 3D printing unlock a new level of design freedom. Imagine intricate lattice structures and internal channels in lightweight aircraft parts, or custom-fit prosthetics with optimal strength and flexibility – these are just a glimpse of the possibilities. Furthermore, the rapid prototyping capabilities of 3D printing accelerate product development cycles, allowing companies to bring innovative products to market faster. While challenges like high material cost, technical complexity, and limited recycled materials exist, ongoing research and development address these issues. As production costs decrease, printing techniques improve, and the availability of recycled materials increases, the market is poised for significant growth. The potential for on-demand, localized manufacturing of high-performance parts with minimal waste further strengthens the appeal of this technology. Overall, the Carbon Fiber Printing Materials Market offers a compelling opportunity to revolutionize manufacturing across various industries, pushing the boundaries of design, performance, and efficiency.

CARBON FIBER PRINTING MATERIALS MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

6.8% |

|

Segments Covered

|

By Type, Application, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Owens Corning, Solvay, BASF, Mitsubishi Chemical Corporation, Toray Industries Inc., SGL Carbon, Extrudair, Stratasys Ltd., Markforged Inc., Desktop Metal Inc.

|

Carbon Fiber Printing Materials Market Segmentation - By Type

-

Carbon Fiber Content

-

Resin Type

In the Carbon Fiber Printing Materials Market, the most prominent sector by resin type is currently Thermoplastic filaments. While thermoset filaments offer superior high-temperature performance, the advantages of thermoplastics in terms of printability, material availability, and printing speed make them the more prominent sector in the current Carbon Fiber Printing Materials Market.

Carbon Fiber Printing Materials Market Segmentation - By Application

-

Aerospace & Defense

-

Automotive

The automotive sector has significant growth potential. As car manufacturers strive for lighter vehicles with improved fuel economy and performance, carbon fiber printing offers a compelling solution. The potential applications in automotive, like lightweight racing components and even future high-end car bodies, are vast. As production costs decrease and printing techniques improve, the automotive sector is expected to catch up and potentially become the dominant user of carbon fiber printing materials in the future.

Carbon Fiber Printing Materials Market Segmentation - Regional Analysis

-

North America

-

Asia-Pacific

-

Europe

-

South America

-

Middle East and Africa

Asia-Pacific is currently expected to be the strongest contender. However, North America and Europe are strong contenders as well, with established aerospace and automotive industries that readily embrace advanced materials. The future dominance will likely depend on factors like the pace of technological advancements, cost reduction strategies, and government policies in each region.

COVID-19 Impact Analysis on the Global Carbon Fiber Printing Materials Market

The COVID-19 pandemic threw a curveball at the Carbon Fiber Printing Materials Market. Disruptions in global supply chains hampered the availability of raw materials and printing equipment, impacting production and temporarily stalling market growth. The crucial end-user industries, particularly Aerospace & Defense and Automotive, experienced significant downturns due to travel restrictions and production slowdowns. This led to a decrease in demand for lightweight, high-performance parts, impacting the adoption of carbon fiber printing materials. However, there were silver linings. The pandemic highlighted the need for agile and adaptable manufacturing processes. 3D printing, with its ability for on-demand production and rapid prototyping, gained traction in certain sectors. Research and development continued, with advancements in material properties and printing techniques. As economies recover and industries adapt to the post-pandemic landscape, the Carbon Fiber Printing Materials Market is expected to rebound. The focus on lightweight and performance optimization in key industries, coupled with ongoing advancements in technology, positions carbon fiber printing materials for a promising future, albeit with a potential reset in the short-term growth trajectory due to the pandemic's impact.

Latest trends/Developments

The Carbon Fiber Printing Materials Market is buzzing with exciting trends and developments. One key area is the exploration of recycled carbon fiber filaments. Sustainability is a growing concern, and incorporating recycled materials could significantly reduce the environmental footprint of this technology. Researchers are developing cost-effective methods for recycling carbon fibers while maintaining their structural integrity for use in filaments. Another trend is the emergence of multi-material printing with carbon fiber. This allows for parts with varying carbon fiber content within a single print. Imagine a lightweight race car part with a high-carbon fiber core for strength and a lighter outer layer, optimizing both weight and performance. Advancements in software are also playing a crucial role. Improved design programs allow engineers to optimize parts specifically for carbon fiber printing, maximizing material utilization and performance. Additionally, there's a growing focus on developing filaments with improved printability. This includes filaments with better adhesion between layers and reduced clogging issues, leading to smoother printing processes and higher success rates. Overall, the Carbon Fiber Printing Materials Market is experiencing a wave of innovation that addresses both technical challenges and sustainability concerns. These advancements pave the way for wider adoption and the creation of high-performance, functional parts across diverse industries...

Key Players:

-

Owens Corning

-

Solvay

-

BASF

-

Mitsubishi Chemical Corporation

-

Toray Industries Inc.

-

SGL Carbon

-

Extrudair

-

Stratasys Ltd.

-

Markforged Inc.

-

Desktop Metal Inc.