Asia Pacific Smoothies Market

The Asia Pacific smoothies’ market is expected to grow from approximately USD 4.5 billion in 2025 to around USD 8.5 billion in 2030, at a compound annual growth rate of around 12.8% during 2025-2030.

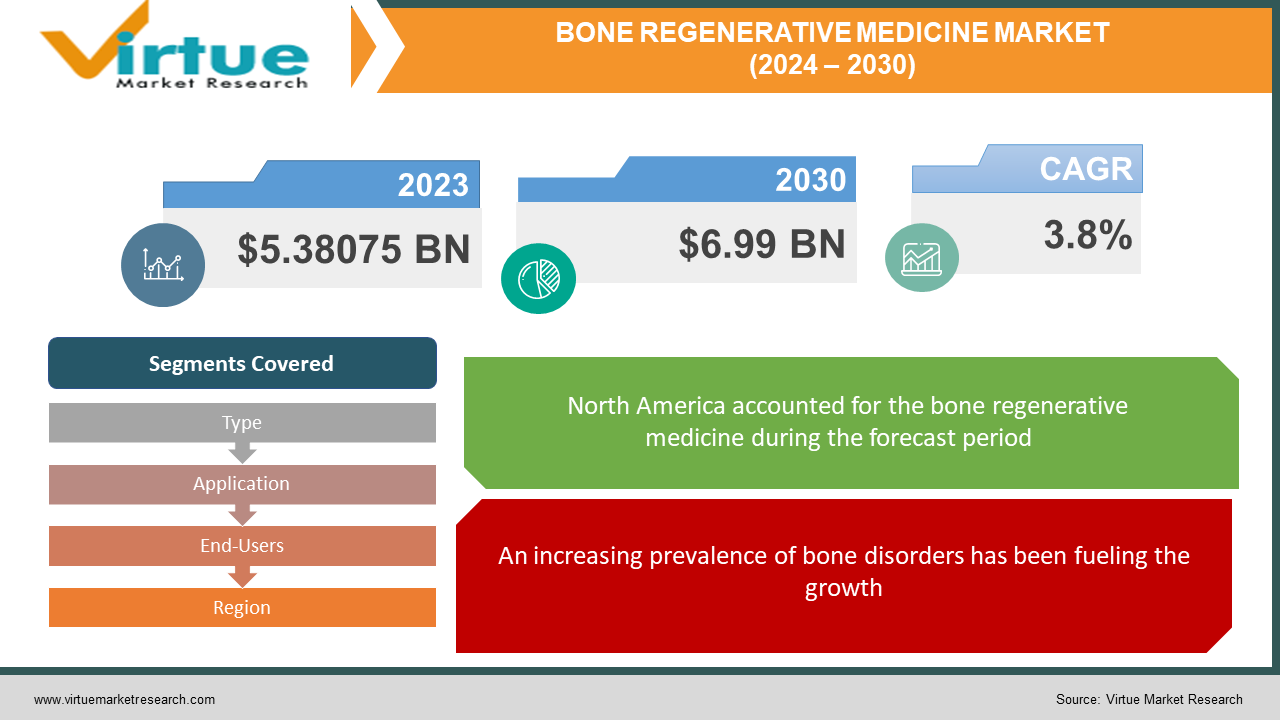

Explore reportThe global bone regenerative medicine market was valued at USD 5.38075 billion and is projected to reach a market size of USD 6.99 billion by the end of 2030. Over the forecast period of 2024–2030, the market is projected to grow at a CAGR of 3.8%.

A therapeutic procedure known as bone regenerative medicine replaces missing tissue without the need for autologous tissue transplants by employing biological signals or cellular constituents. Tissue engineering and bone grafting are two aspects of bone regenerative medicine. This market has had a significant presence in the past. Earlier, bone grafting was one of the main procedures that was used. Presently, due to an increasing number of clinical trials and advanced technologies, the market has witnessed a notable expansion. During the forecast period, with a focus on personalized medicine and drug delivery systems, immense growth is anticipated.

Key Market Insights:

More than 70% of patients with Stage 3 Avascular Necrosis and more than 80% of those with Stage 2 Avascular Necrosis respond well to bone cell therapy. The worldwide market for bone replacements and grafts is expected to reach around 4.86 billion U.S. dollars by 2030. An estimated 2.2 million bone-grafting orthopedic surgeries are performed globally each year, and the incidence rate is expected to rise by 13% annually. Allografts have a 90.9% survival rate, compared to 99.6% for composite bone transplants. The cost of extracting and preparing a patient's stem cells for implantation in autologous stem cell treatment for bone repair can range from $10,000 to $20,000 or more per surgery. To address this, governmental initiatives in the form of schemes and funds are being taken. Additionally, insurance coverage is being emphasized to cover the cost.

Bone Regenerative Medicine Market Drivers:

An increasing prevalence of bone disorders has been fueling the growth.

Life expectancy has increased over the years, with the range being 63–73. As people age, their bones lose mass and strength, leading to various types of diseases. The incidence of bone-related conditions, including osteoporosis, osteoarthritis, and bone fractures, is rising as a result. Besides, bone problems are becoming more common among the younger generation due to lifestyle factors. This includes the consumption of a poor diet that includes junk food and fried items. Additionally, sedentary behavior and an increase in sports-related accidents have also contributed to the elevation. Osteoporosis in the hip, spine, or both affects 12.6% of people over 50, according to the CDC, with osteoporosis affecting 19.6% of women and 4.4% of men. The need for bone regenerative medicine solutions is driven by the increasing recognition of the significance of bone health and the need for efficient therapies to enhance the quality of life.

Advancements in regenerative medicine have been boosting the market.

Innovation in bone regeneration is being propelled by ongoing developments in regenerative medicine technologies, such as stem cell treatment, tissue engineering, and biomaterials. The goal of tissue engineering is to create alive, breathing tissues rather than merely inert scaffolds. Biopolymers, bioactive fillers, and a biodegradable matrix structure make up bone regeneration biomaterials. These fillers readily resorb and are nanoscale in size. Synovial cells, chondrocytes, and mesenchymal stem cells (MSCs) may all be cultured in temperature-responsive culture plates. To harvest the cell sheets, the plates can be left at room temperature (20 °C) for a few days or weeks. Furthermore, new technologies, including 3D bioprinting, make it possible to precisely create intricate bone structures, which makes it easier to create specialized implants and scaffolds for bone healing. Apart from this, the potential uses of regenerative medicine in bone repair and regeneration are further expanded by research into new growth factors, gene treatments, and immunomodulatory techniques. The market is growing and becoming more widely used as a result of these technical developments that improve bone regenerative medicine therapies' accessibility, safety, and effectiveness.

Bone Regenerative Medicine Market Restraints and Challenges:

Associated costs, side effects, implant rejection, and mechanical rigidity are the main issues that the market is currently facing.

The expenses for bone regeneration therapies like stem cell therapy, tissue engineering, and bone transplants are very high. Complexities are developed in the human body because people are unable to afford healthcare. Tackling this price and making it accessible to the public is a significant barrier. Secondly, a lot of individuals have reported side effects after the procedure. Low white blood cell counts, low red blood cell counts (anemia), low platelet counts, mouth sores, appetite loss, taste changes, exhaustion, hair loss, nausea, diarrhea, and weight loss are all possible problems after bone marrow transplants. Thirdly, there is a chance of rejection of the implant by the body. In this process, stem cells are transplanted. The body might decline, causing an immune rejection. This can be acute, mild, or severe. This leads to improper functioning and the failure of other organs. Furthermore, tissue engineering can create technical challenges. It can lead to abrupt mass and mechanical strength loss throughout the degradation process, as well as acidic byproducts of the hydrolysis reaction that cause the material to break down.

Bone Regenerative Medicine Market Opportunities:

Numerous opportunities have been presented to the market by personalized medicine. The development of medications is dependent on the genetic makeup of the patient. Environmental influences, as well as other aspects of lifestyle, are taken into account. Biomarkers are used in this process. Biomarkers provide real-time information on the processes occurring within human cells. Based on variables including genetics, tissue compatibility, and disease pathology, opportunities exist to create customized regenerative treatments that may enhance therapy results and patient satisfaction. Secondly, gene therapy is another emerging field. Genes can be safely delivered with sustained protein expression using cationic polymers and osteogenic growth factor-encoding DNA. Gene therapy may be used to treat congenital skeletal defects, infections, fractures, and trauma-related bone loss. Gene therapy can be used to regulate the kind and quantity of bone that regenerates, as well as to replicate natural bone formation processes. In addition to treating osteogenesis imperfecta and other bone abnormalities, gene therapy has demonstrated the potential of viral vectors to aid in the mending of bones. Thirdly, multipotent bone marrow-derived cells called mesenchymal stem cells (MSCs) are gaining prominence. Mesenchymal stem cells can proliferate, move to areas of damage, develop into osteoblasts, alter the local immune system, and stimulate bone rebuilding. They have the ability to repair damaged tissue, have autocrine and paracrine functions, and transport therapeutic chemicals or genes to cure bone diseases. Furthermore, research studies are being conducted to study the relationship & action between bones and nerves. Cartilage repair is another interesting area of study. By understanding the anatomy, better and more effective treatment options can be available.

BONE REGENERATIVE MEDICINE MARKET REPORT COVERAGE:

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2023 - 2030 |

|

Base Year |

2023 |

|

Forecast Period |

2024 - 2030 |

|

CAGR |

3.8% |

|

Segments Covered |

By Type, Application, End-Users, and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regional Scope |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Key Companies Profiled |

Medtronic plc, Johnson & Johnson, Zimmer Biomet Holdings, Inc., Stryker Corporation, Smith & Nephew plc, ACell, Inc., Integra LifeSciences Holdings Corporation, NuVasive, Inc., Baxter International, Inc., Wright Medical Group N.V. |

Bone Grafts Substitutes

Allografts

Demineralized Bone Matrix (DBM)

Others

Xenograft

Autografts

Synthetic Bone Graft

Bone Morphogenetic Protein (BMP)

Bone Growth Stimulators

Non-Invasive Electrical Bone Growth Stimulators

Invasive Electrical Bone Growth Stimulators

Bone graft substitutes are both the largest and fastest-growing type. BMP and synthetic bone grafts are the most commonly used techniques. BMPs induce the growth of new bone tissue and are frequently utilized in bone regeneration. They have strong osteogenic (bone-forming) qualities and are hence used therapeutically in orthopedic surgery and bone regeneration. In spinal fusion operations, non-union fractures, and orthopedic reconstructions, recombinant human BMPs (rhBMPs) are utilized therapeutically to encourage bone fusion and healing. They are produced using biotechnology techniques. The use of synthetic bone transplant alternatives is expanding quickly as a result of developments in tissue engineering and biomaterials. Compared to conventional grafting materials, these synthetic alternatives provide several benefits, such as uniform quality, adjustable qualities, and a lower chance of disease transmission.

Osteoarthritis (OA)

Osteoporosis

Rheumatoid Arthritis (RA)

Spinal Disorders

Dentistry

Craniomaxillofacial (CMF)

Trauma Cases

Spinal disorders are the largest application. For spine disorders like spondylosis, regenerative medicine has become a viable, long-term, less invasive therapeutic option. By facilitating the body's inherent healing process, regenerative techniques may be able to address problems affecting the spine. The process creates new, healthy cells in injured areas by using the patient's stem cells. The cells are taken from the patient's fat or bone marrow and subsequently injected into the facet joints and discs. After three to seven weeks of therapy, the majority of patients start to see improvements in their condition. The need for bone-regenerating treatments in the treatment of spinal problems has increased due to developments in spinal fusion techniques and the uptake of less invasive procedures. Osteoarthritis (OA) is the fastest-growing application. The most common kind of chronic joint illness is osteoarthritis (OA). This is the main cause of joint discomfort, loss of function, and disability. Since it mostly affects the knee joint, pathology is most commonly found there. Platelet-rich plasma (PRP) and mesenchymal stem cell (MSC) injections are two intriguing therapy approaches for knee osteoarthritis (KOA) that may be made possible by regenerative medicine. These injections could aid in tissue healing, pain alleviation, and the restoration of functional ability.

Hospitals

Research Institutions

Orthopedic Clinics

Ambulatory Surgical Centers

Others

Hospitals are both the largest and fastest-growing end-users. This is a result of their highly qualified medical staff and state-of-the-art diagnostic tools. Hospitals provide comprehensive healthcare services, including treating and evaluating bone health, to a diverse patient population. They also often lead the way in this regard. The aging population, the increase in bone-related diseases, and the acceptance of the public are driving up demand.

North America

Asia-Pacific

Europe

South America

Middle East and Africa

North America has the largest market, with the leading nations being the United States and Canada. This area has a very advanced healthcare system. There are several notable hospitals located here. In addition, a large number of businesses manufacture tools and other essential supplies. Additionally, the economy makes investments simpler. Several Ivy League colleges and companies are researching this condition. This is leading to an increase in revenue. The market with the fastest growth is Asia-Pacific. China, India, and Japan are the notable countries. The standard of living has changed as a result of urbanization. As a result, there is a growing middle class and discretionary money. Governmental initiatives in the form of grants and plans have resulted in a massive development of the healthcare business. Well-known expertise is contributing to the success. Besides, an increase in the number of hospitals and orthopedic clinics has been enabling better profits.

COVID-19 Impact Analysis on the Global Bone Regenerative Medicine Market:

The market was harmed by the viral epidemic. Lockdowns, movement limitations, and social isolation were among the new standards. To avoid any kind of contamination, people postponed their hospital visits and stayed at home. Delays in diagnosis and treatment resulted from this. In addition, the majority of hospitals were overflowing with coronavirus-affected patients. As a result, there was a decline in bone grafts, stem cell transplants, and other methods in many hospitals & clinics. Besides, economic uncertainty prevailed, due to which people lost their jobs. The costs of these procedures were very high, and many people were unable to afford them. While telemedicine services gained popularity quickly, in-person visits were still necessary for bone regeneration techniques. All joint ventures and product introductions in this market were suspended and delayed. Studies on the virus and its potential effects on various individuals were given priority in research and development operations. Few R&D studies were conducted to analyze the effect on bones in patients who were infected with the coronavirus. Researchers at Indiana University School of Medicine's Department of Orthopaedic Surgery found that after two weeks of infection, mice models infected with the new coronavirus lost around 25% of their bone density. However, this led to no growth in consultation services. Following the epidemic, the market expanded quickly as a result of the relaxation of laws and regulations. Individuals began coming in for regular examinations and discussions.

Latest Trends/ Developments:

Therapeutic medicines, including growth factors, cytokines, and small molecules, can be delivered directly to the site of bone damage or defect using nanoparticle-based drug delivery systems. By extending release kinetics, improving local concentration, and shielding the payload from degradation, these nanoparticles aid in tissue repair and regeneration.

Key Players:

Medtronic plc

Johnson & Johnson

Zimmer Biomet Holdings, Inc.

Stryker Corporation

Smith & Nephew plc

ACell, Inc.

Integra LifeSciences Holdings Corporation

NuVasive, Inc.

Baxter International, Inc.

Wright Medical Group N.V.

In June 2023, launched in partnership with NLC, a health tech venture builder, TherageniX is a University of Nottingham spin-out company focused on developing technology that employs gene therapy to deliver biological cues to enhance the body's reaction to rebuilding skin, bone, muscle, and cartilage. TherageniX's first focus will be on orthopedic applications to enhance patient outcomes for individuals suffering from illness, infection, and bone loss. A gene therapy system that can regenerate and repair human tissue is being developed for use in orthopedic surgery.

In April 2023, without implanting bone tissue or biomaterials, the University of Pittsburgh researchers created a novel method that encourages bone regeneration in adult mice. By carefully stretching the skull along its sutures, the method activates the skeletal stem cells that are present in these joints.

In November 2022, with the use of a unique hydrogel, a novel technique was created to allow bone regeneration to repair significant bone defects. Because hydrogels include pro-angiogenic cells, they can stimulate bone regeneration by forming a biphasic system with MSCs that speeds up the healing of bone defects. Experts from TAU's Maurice and Gabriela Goldschleger School of Dental Medicine, under the direction of Professor Lihi Adler-Abramovich and Dr. Michal Halperin-Sternfeld, carried out the ground-breaking study in cooperation with researchers from the University of Michigan in Ann Arbor, as well as Professor Itzhak Binderman, Drs. Rachel Sarig, and Moran Aviv.

The global bone regenerative medicine market was valued at USD 5.38075 billion and is projected to reach a market size of USD 6.99 billion by the end of 2030. Over the forecast period of 2024–2030, the market is projected to grow at a CAGR of 3.8%.

An increasing prevalence of bone disorders and advancements in regenerative medicine are the main factors propelling the global bone regenerative medicine market.

Based on type, the global bone regenerative medicine market is segmented into bone graft substitutes and bone growth stimulators.

North America is the most dominant region for the global bone regenerative medicine market.

Medtronic plc, Johnson & Johnson, and Zimmer Biomet Holdings, Inc. are the key players operating in the global bone regenerative medicine market.

Joining thousands of companies around the world committed to making the Excellent Business Solutions.

Specify your preferred Countries, Segments, or timeframes

Unlock Country Level Outlook, Trends, Cross-country Comparability, or supply Chain Variations.

Analyst Support

Every order comes with Analyst Support.

Customization

We offer customization to cater your needs to fullest.

Verified Analysis

We value integrity, quality and authenticity the most.