Blood Bags Market Size (2024 – 2030)

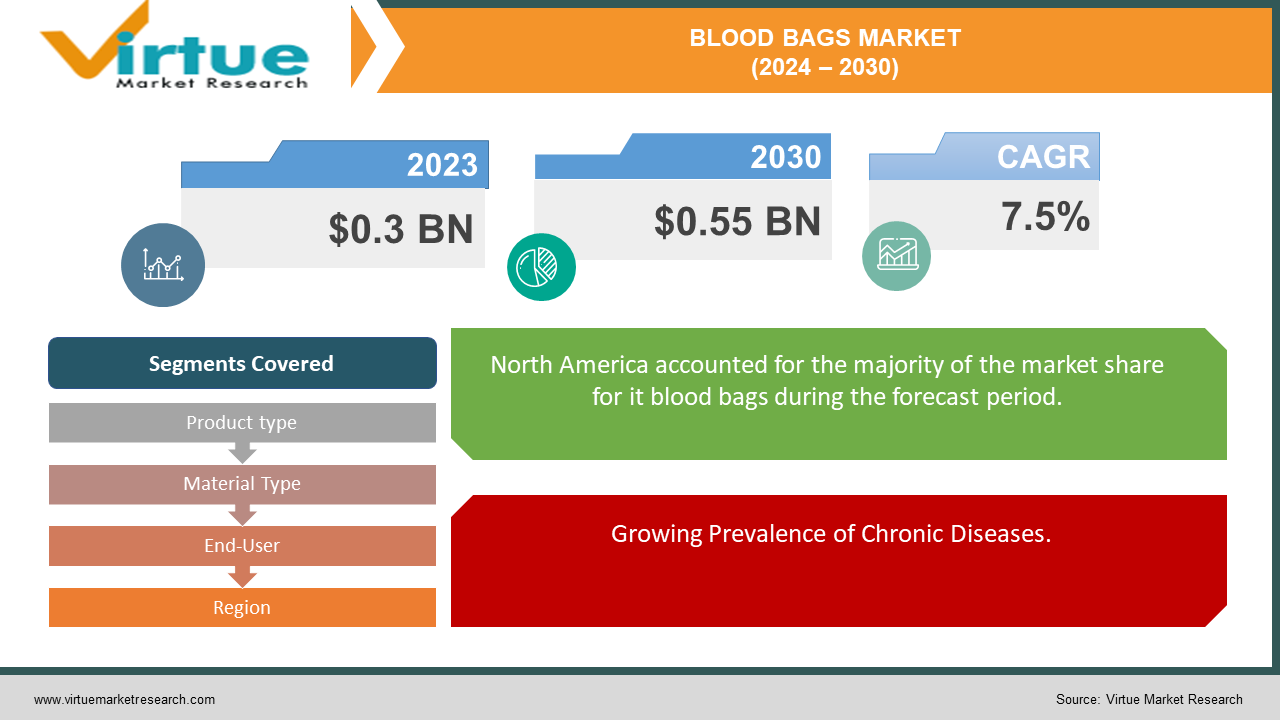

The global blood bags market is projected to grow from an estimated USD 0.3 billion in 2023 to USD 0.55 billion by 2030, reflecting a compound annual growth rate (CAGR) of approximately 7.5% over the forecast period of 2024-2030.

Key factors contributing to this expansion include the rising prevalence of blood disorders, growing incidences of surgeries and trauma cases, and concerted efforts by governments and NGOs to promote blood donation. North America and Europe remain significant markets due to their advanced healthcare infrastructures, while the Asia Pacific region emerges as the fastest-growing market owing to its large population base and escalating healthcare investments.

Key Insights:

By 2025, the number of blood transfusions performed annually is expected to increase by 30%, driven by rising surgical procedures and trauma cases.

The adoption of automated blood collection systems is anticipated to grow by 40% over the next five years, enhancing the efficiency and safety of blood collection processes.

The Asia Pacific region is expected to witness a market growth rate of 10% annually, attributed to improved healthcare infrastructure and growing awareness about blood donation.

Approximately 20% of blood bags currently in use may face compliance issues due to evolving regulatory standards. To address this, manufacturers should invest in R&D to ensure all products meet the latest safety and regulatory requirements.

Global Blood Bags Market Drivers:

Growing Prevalence of Chronic Diseases.

The increasing prevalence of chronic diseases such as cancer, anemia, and kidney disorders is a significant driver of the blood bags market. These conditions often necessitate regular blood transfusions, which in turn boosts the demand for blood collection and storage solutions. As healthcare providers strive to manage and treat these long-term illnesses, the need for reliable and efficient blood bags continues to rise, fueling market growth.

Advances in Blood Collection Technology.

Technological advancements in blood collection and storage are propelling the blood bags market forward. Innovations such as automated blood collection systems and improved materials for blood bags enhance the safety, efficiency, and ease of blood donation and transfusion processes. These advancements reduce the risk of contamination and improve the overall quality of stored blood, making modern blood bags an essential component in healthcare facilities worldwide.

Increasing Government and NGO Initiatives.

Government and non-governmental organizations (NGOs) are playing a crucial role in promoting blood donation and ensuring a stable supply of blood. Various awareness campaigns, blood donation drives, and funding initiatives aimed at improving blood bank infrastructure have significantly increased the availability and accessibility of blood. These efforts not only boost the overall blood supply but also drive the demand for blood bags, as more collected blood requires proper storage and handling solutions.

Global Blood Bags Market Restraints and Challenges:

Stringent Regulatory Requirements.

The blood bags market is heavily regulated to ensure the safety and efficacy of blood collection and storage. Compliance with stringent regulatory standards, such as those set by the FDA and European Medicines Agency, can be challenging for manufacturers. These regulations necessitate continuous updates and rigorous testing of products, which can increase costs and delay market entry for new products.

Risk of Blood Contamination and Infections.

Despite advancements in technology, the risk of contamination and infections during blood collection and transfusion remains a significant challenge. Issues such as bacterial contamination, viral infections, and improper handling can lead to serious health complications. Ensuring the sterility and safety of blood bags is critical, requiring ongoing vigilance and the adoption of advanced safety protocols.

High Costs of Advanced Blood Collection Systems.

While automated and advanced blood collection systems offer numerous benefits, their high costs can be a barrier for many healthcare facilities, particularly in low-income regions. The initial investment in these technologies, along with maintenance and operational costs, can be prohibitive. This financial burden limits the adoption of advanced systems, thereby affecting the overall efficiency and safety of blood collection and storage processes in these areas.

Global Blood Bags Market Opportunities:

Expansion in Emerging Markets.

Emerging markets, particularly in regions like Asia-Pacific, Latin America, and Africa, present significant growth opportunities for the blood bags market. As healthcare infrastructure in these regions continues to improve and awareness about the importance of blood donation increases, the demand for blood bags is expected to rise. Companies that can establish a strong presence in these markets, adapt to local needs, and provide cost-effective solutions will likely experience substantial growth.

Technological Innovations.

There is a considerable opportunity for growth through technological innovations in blood collection and storage systems. Advancements such as RFID-enabled blood bags for better tracking, biodegradable materials to reduce environmental impact, and smart blood bags that monitor blood quality in real-time can revolutionize the market. Investing in research and development to create these advanced products can help companies gain a competitive edge and meet the evolving needs of the healthcare sector.

Strategic Collaborations and Partnerships.

Collaborations and partnerships between blood bag manufacturers, healthcare providers, and governmental and non-governmental organizations can create new growth avenues. Joint ventures and strategic alliances can lead to the development of innovative products, improve distribution networks, and enhance market penetration. By working together, stakeholders can address common challenges, share resources, and expand their reach, ultimately benefiting the global blood bags market.

BLOOD BAGS MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

7.5% |

|

Segments Covered

|

By Product type, Material Type, End-User, and Region

|

|

Various Analyses Covered

|

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

North America, Europe, APAC, Latin America, Middle East & Africa

|

|

Key Companies Profiled

|

Terumo Corporation, Fresenius SE & Co. KGaA, Macopharma, Grifols, Haemonetics Corporation, Abbott Laboratories, Kawasumi Laboratories, Inc., Shanghai Transfusion Technology Co., Ltd., Neomedic Limited, SURU International Pvt. Ltd., Advacare Pharma, Polycine GmbH

|

Blood Bags Market Segmentation: By Product Type

-

Single Blood Bags

-

Double Blood Bags

-

Triple Blood Bags

-

Quadruple Blood Bags

Among the various product types in the blood bags market, triple blood bags have proven to be particularly effective and versatile. Triple blood bags are designed to collect and separate whole blood into three different components: red blood cells, plasma, and platelets. This capability is crucial in modern medical treatments, as it allows healthcare providers to maximize the utility of each blood donation, addressing the specific needs of different patients more efficiently. The ability to separate and store multiple blood components in a single collection process not only enhances the efficiency of blood banks and hospitals but also improves patient outcomes by ensuring that the right component is available for transfusion when needed. This multifunctionality and efficiency make triple blood bags a preferred choice in many medical facilities, driving their demand and effectiveness in the global blood bags market.

Blood Bags Market Segmentation: By Material Type

PVC (Polyvinyl Chloride) blood bags are widely regarded as the most effective material type in the blood bags market due to their superior durability, flexibility, and cost-effectiveness. PVC blood bags offer excellent storage capabilities, maintaining the integrity and safety of stored blood and its components over extended periods. Their robust nature ensures minimal risk of rupture or leakage, which is critical for maintaining the sterility and safety of blood supplies. Additionally, PVC's flexibility allows for easy handling and manipulation during blood collection and transfusion processes. The cost-effectiveness of PVC blood bags also makes them a preferred choice for many healthcare facilities, particularly in regions with budget constraints. These advantages collectively position PVC blood bags as the most effective material type, contributing significantly to their widespread adoption in the global blood bags market.

Blood Bags Market Segmentation: By End-User

-

Hospitals

-

Blood Banks

-

Clinics

-

Home Healthcare

Among the diverse end-users in the global blood bags market, hospitals emerge as the most significant and effective segment. Hospitals consistently account for the largest share due to their high demand for blood bags to support various medical procedures, surgeries, and emergency treatments. Their extensive usage is driven by the need for safe blood storage, transfusion capabilities, and stringent regulatory standards. Moreover, hospitals often serve as central hubs for blood collection drives and donation centers, further bolstering their reliance on blood bags. The increasing prevalence of chronic diseases, surgeries, and trauma cases worldwide continues to amplify the demand within hospital settings, solidifying their pivotal role in driving the growth of the global blood bags market.

Blood Bags Market Segmentation: Regional Analysis

-

North America

-

Europe

-

Asia-Pacific

-

South America

-

Middle East & Africa

The global market for blood bags is geographically diverse, with North America leading at 38%, driven by advanced healthcare infrastructure and stringent safety regulations. Europe follows with 25%, benefiting from robust healthcare systems and a focus on technological advancements. The Asia-Pacific region holds 22%, propelled by increasing healthcare investments and a large patient population. South America accounts for 8%, supported by improving healthcare infrastructure, while the Middle East and Africa contribute 7%, with growing healthcare facilities and initiatives to enhance blood transfusion services. These regional shares highlight varied factors influencing market dynamics, including healthcare development, regulatory frameworks, and population demographics across different continents.

COVID-19 Impact Analysis on the Global Blood Bags Market:

The COVID-19 pandemic has had a profound impact on the global blood bags market, initially disrupting blood donation drives and collection efforts due to lockdowns and safety concerns. This led to temporary shortages in blood supply, particularly affecting elective surgeries and routine medical procedures. However, the crisis also prompted advancements in blood storage and management practices to ensure the safety and availability of blood products. Moving forward, the market is poised to recover as blood donation activities normalize, with ongoing innovations expected to enhance the resilience and efficiency of blood transfusion services worldwide.

Latest Trends/ Developments:

Recent trends and developments in the global blood bags market highlight ongoing advancements aimed at enhancing safety, efficiency, and sustainability. Innovations in blood bag materials, such as the adoption of eco-friendly and biocompatible plastics, are gaining traction to reduce environmental impact and improve blood storage capabilities. Additionally, there is a growing focus on digitalization and automation within blood management systems, including barcoding and RFID technologies, to enhance traceability and reduce errors in blood transfusion processes. Moreover, collaborations between healthcare providers and technology firms are driving the integration of artificial intelligence and machine learning algorithms to optimize blood inventory management and predict demand more accurately. These trends underscore a dynamic shift towards more sophisticated and integrated solutions that are poised to shape the future of blood transfusion practices globally.

Key Players:

-

Terumo Corporation

-

Fresenius SE & Co. KGaA

-

Macopharma

-

Grifols

-

Haemonetics Corporation

-

Abbott Laboratories

-

Kawasumi Laboratories, Inc.

-

Shanghai Transfusion Technology Co., Ltd.

-

Neomedic Limited

-

SURU International Pvt. Ltd.

-

Advacare Pharma

-

Polycine GmbH