Asia Pacific Wet Adhesive Market Size (2024-2030)

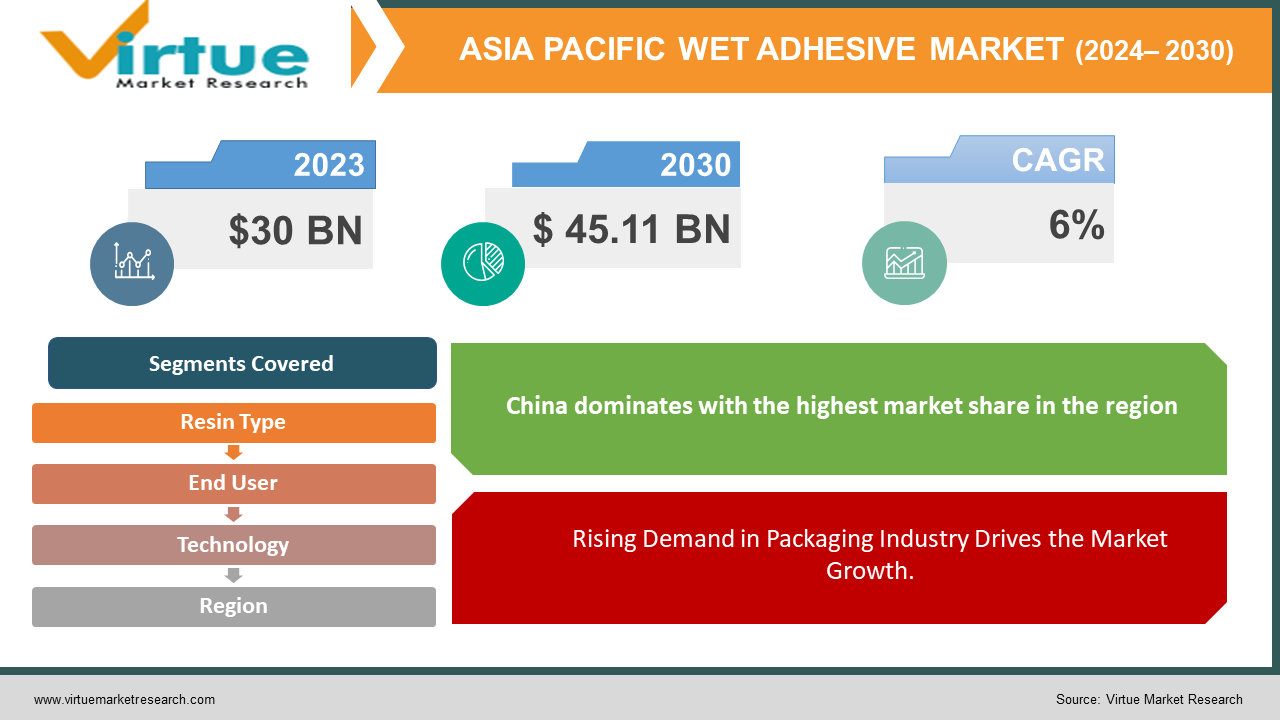

The Asia Pacific Wet Adhesive Market was valued at USD 30 billion in 2023 and is projected to reach a market size of USD 45.11 billion by the end of 2030. The market is anticipated to expand at a compound annual growth rate (CAGR) of 6% between 2024 and 2030.

The Asia Pacific Wet Adhesive Market is experiencing robust growth driven by a diverse range of industrial applications and technological advancements. Wet adhesives, known for their versatility and strong bonding capabilities, are widely used in sectors such as automotive, construction, packaging, and electronics. The region's rapid industrialization and increasing infrastructure development are significant contributors to the rising demand for these adhesives. Additionally, the booming e-commerce sector and evolving consumer packaging needs are further fueling market expansion. Technological innovations in adhesive formulations, which enhance performance attributes like adhesion strength, durability, and environmental resistance, are also shaping market trends. The market is characterized by a dynamic landscape of key players striving to develop sustainable and high-performance adhesive solutions. With regulatory frameworks becoming more stringent and environmental concerns gaining prominence, the industry is witnessing a shift towards eco-friendly and low-VOC adhesives. Overall, the Asia Pacific Wet Adhesive Market is poised for continued growth as it adapts to evolving industrial demands, technological advancements, and sustainability trends, positioning itself as a crucial component of the region’s industrial and commercial infrastructure.

Key Market Insights:

- Over 40% of the wet adhesive demand in the region is driven by the packaging industry.

- The automotive sector accounts for about 25% of the total wet adhesive consumption in Asia Pacific.

- Around 30% of the market is shifting towards environmentally friendly and low-VOC adhesive formulations.

- The construction industry represents roughly 20% of the wet adhesive market.

Asia Pacific Wet Adhesive Market Drivers:

Rising Demand in Packaging Industry Drives the Market Growth.

The Asia Pacific Wet Adhesive Market is significantly driven by the booming packaging industry, which has become a major consumer of wet adhesives. The rapid expansion of the e-commerce sector and changing consumer preferences for convenient and sustainable packaging solutions have spurred this demand. Wet adhesives are essential for ensuring strong bonds and durability in various packaging materials, including cartons, labels, and flexible films. The increasing emphasis on product presentation and tamper-evident packaging also contributes to the high consumption of wet adhesives. Additionally, innovations in packaging design and technology are further fueling the need for advanced adhesive solutions that offer superior performance and environmental benefits. As the region continues to witness high growth in retail and packaged goods, the packaging industry's reliance on wet adhesives is expected to remain a key driver, promoting continued market expansion.

Growth in Automotive and Construction Sectors Revolutionizing the APAC Wet Adhesive Market.

Another significant driver of the Asia Pacific Wet Adhesive Market is the growth in the automotive and construction sectors. In the automotive industry, wet adhesives are crucial for various applications, including assembly, repair, and interior bonding, due to their ability to provide strong, flexible, and durable connections. As the automotive sector in Asia Pacific experiences robust growth, driven by increasing vehicle production and sales, the demand for wet adhesives in this sector is also rising. Similarly, the construction industry relies heavily on wet adhesives for applications such as flooring, tiling, and panel bonding. The rapid urbanization, infrastructure development, and residential construction projects across the region contribute to the heightened need for effective adhesive solutions. Both sectors' expansion drives substantial demand for wet adhesives, making them vital contributors to the market's overall growth.

Asia Pacific Wet Adhesive Market Restraints and Challenges:

The Asia Pacific Wet Adhesive Market faces several restraints and challenges that could impact its growth trajectory. One major challenge is the increasing regulatory pressure regarding environmental sustainability. Governments across the region are implementing stricter regulations on volatile organic compounds (VOCs) and other hazardous substances found in adhesives, pushing manufacturers to develop low-VOC and eco-friendly formulations. This transition can be costly and complex, potentially affecting market dynamics. Additionally, fluctuating raw material prices and supply chain disruptions pose significant risks. The volatility in the costs of key ingredients like resins and solvents can lead to price instability, impacting profit margins for manufacturers. Another restraint is the intense competition within the market, with numerous players vying for market share, which can lead to price wars and reduced profitability. Furthermore, the market's dependence on industrial sectors such as automotive and construction makes it vulnerable to economic downturns and fluctuations in these industries, affecting overall demand. Addressing these challenges requires strategic adjustments, including investment in sustainable technologies and efficient supply chain management, to maintain competitiveness and market stability.

Asia Pacific Wet Adhesive Market Opportunities:

The Asia Pacific Wet Adhesive Market presents several promising opportunities for growth and innovation. One significant opportunity lies in the increasing demand for eco-friendly and sustainable adhesive solutions. As environmental regulations tighten and consumer preferences shift towards greener products, there is a growing market for low-VOC, water-based, and biodegradable adhesives. Companies investing in these sustainable technologies can capture a substantial share of the market and enhance their competitive edge. Additionally, the rapid expansion of the e-commerce sector offers new avenues for wet adhesive applications, particularly in packaging and labeling. Innovations in adhesive formulations that cater to the evolving needs of the packaging industry, such as enhanced adhesion and recyclability, are likely to see high demand. The ongoing urbanization and infrastructure development across the Asia Pacific also create opportunities in the construction sector, where advanced wet adhesives are required for various applications including flooring, tiling, and structural bonding. Moreover, the rise of smart technologies and automation in manufacturing processes presents opportunities for developing specialized adhesives that meet the technical demands of these innovations. By leveraging these trends, companies can position themselves strategically in the growing and evolving market landscape.

ASIA PACIFIC WET ADHESIVE MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

6%

|

|

Segments Covered

|

By resin Type, technology, end user industry, and Region

|

|

Various Analyses Covered

|

Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

china, Japan, India, South Korea, Rest of Asia-Pacific |

|

Key Companies Profiled

|

Henkel AG & Co. KGaA, 3M Company, Sika AG, H.B. Fuller Company, Bostik (a subsidiary of Arkema), Avery Dennison Corporation, Dow Chemical Company, Kraton Corporation, Ashland Global Holdings Inc., Illinois Tool Works Inc.

|

Asia Pacific Wet Adhesive Market Segmentation:

Asia Pacific Wet Adhesive Market segmentaion By Technology:

- Water-borne

- Solvent-borne

- Reactive

- Hot Melt

- Others

The Water-borne segment held the highest market share last year and is poised to maintain its dominance throughout the forecast period. Environmental concerns and regulatory pressures are driving the increasing adoption of water-borne adhesives in the Asia Pacific region. As awareness of environmental issues grows, and regulations on volatile organic compounds (VOCs) become more stringent, water-borne adhesives have gained favor due to their lower environmental impact and compliance with strict safety and health standards. These adhesives offer a cost-effective alternative to solvent-borne options, contributing to their rising popularity. Their versatility allows them to be used across various applications, including packaging, construction, and woodworking, further boosting their demand. Market research reports consistently highlight the trend towards water-borne adhesives, particularly in countries with robust environmental regulations and a focus on sustainability. However, challenges remain, such as performance limitations in specific applications where water-borne adhesives may not match the efficacy of solvent-borne or reactive adhesives. Technological advancements are underway to enhance the performance of water-borne adhesives, addressing these limitations and expanding their applications. Additionally, the dominance of water-borne adhesives can vary across the region due to differing regulatory environments and consumer preferences, which may influence the market dynamics and adoption rates in specific countries.

Asia Pacific Wet Adhesive Market segmentaion By Resin Type:

- Acrylic

- Polyurethane

- Rubber-based

- Epoxy

- Others

Acrylic had the largest market share last year and is poised to maintain its dominance throughout the forecast period. Acrylic adhesives are gaining prominence in the Asia Pacific wet adhesive market due to their versatility, cost-effectiveness, and environmental benefits. Their broad range of properties makes them suitable for various applications across industries, including packaging, construction, and consumer goods. Acrylic adhesives offer a favorable balance between performance and cost, appealing to manufacturers looking for efficient solutions. Many of these adhesives are water-based, aligning with the increasing emphasis on sustainability and reducing environmental impact. Their excellent adhesion to a variety of substrates further enhances their appeal. Market research consistently highlights the dominance of acrylic adhesives, driven by robust demand from multiple end-use sectors. However, the market faces challenges from competing resins, such as polyurethane and rubber-based adhesives, which are gaining traction in certain applications and could impact acrylic adhesives' market share. Technological advancements are underway to improve the performance of acrylic adhesives, addressing specific application requirements and expanding their utility. Additionally, market dominance may vary across different countries in the Asia Pacific region due to diverse industry needs and regulatory environments, influencing the adoption and growth of acrylic adhesives in specific locales.

Asia Pacific Wet Adhesive Market segmentaion By End-Use Industry:

- Packaging

- Construction

- Woodworking

- Automotive

- Paper and Board

- Others

The Packaging segment had majority of the market share last year and is poised to maintain its dominance throughout the forecast period. The dominance of the packaging industry in the Asia Pacific Wet Adhesive Market is primarily driven by the e-commerce boom, growth in consumer goods, and a focus on sustainability. The rapid increase in online shopping has significantly raised the demand for packaging materials, which, in turn, boosts the consumption of wet adhesives used in various packaging applications. The expanding consumer goods sector, encompassing food, beverages, and personal care products, further fuels this demand as extensive and reliable packaging solutions are required. Additionally, the growing emphasis on sustainable packaging solutions has created opportunities for water-based and environmentally friendly adhesives, aligning with consumer and regulatory expectations for greener alternatives. Market research consistently underscores packaging as the leading end-user of wet adhesives in the Asia Pacific region, supported by rising disposable incomes, evolving consumer preferences, and the expansion of organized retail. However, the market faces potential challenges such as fluctuating packaging trends, which might impact the demand for specific adhesive types, and cost pressures due to increasing competition. Furthermore, the trend toward lightweight packaging could influence adhesive choices, necessitating adaptations in adhesive technology to meet new requirements and maintain market relevance.

Asia Pacific Wet Adhesive Market segmentaion By Country:

- China

- India

- Japan

- Australia

- South Korea

China holds the largest market share and is poised to maintain its dominance throughout the forecast period. China's dominance in the Asia Pacific Wet Adhesive Market is underpinned by its massive manufacturing base, large domestic market, cost competitiveness, and strong government support. As a global manufacturing powerhouse, China plays a crucial role in producing various products that require adhesives, benefiting from a robust industrial infrastructure. The country's growing population and expanding economy drive significant demand for adhesives across multiple sectors, including packaging, automotive, construction, and consumer goods. China's cost advantage, stemming from lower labor and production costs, makes it an attractive location for adhesive manufacturing, ensuring its competitiveness on both regional and global scales. Additionally, favorable government policies promoting industrial growth and manufacturing have further strengthened the adhesive industry, providing a conducive environment for expansion and innovation. However, challenges are emerging that could impact China's market dominance. Rising labor costs may gradually erode the country's cost advantage, while stricter environmental regulations could impose additional costs on the adhesive manufacturing process, particularly in the shift towards more sustainable and eco-friendly formulations. These factors may influence China's ability to maintain its leadership in the market, requiring strategic adjustments and innovations to address these evolving challenges and sustain its competitive edge in the Asia Pacific region.

COVID-19 Impact Analysis on the Asia Pacific Wet Adhesive Market.

The COVID-19 pandemic had a notable impact on the Asia Pacific Wet Adhesive Market, causing disruptions across various sectors and altering market dynamics. Initially, the pandemic led to significant supply chain interruptions and a slowdown in manufacturing activities due to lockdowns and restrictions. This resulted in delays in the production and delivery of wet adhesives, affecting industries like automotive, construction, and packaging. However, the crisis also accelerated certain market trends, such as the surge in demand for packaging materials driven by the e-commerce boom, which partially offset the negative impact. The pandemic heightened awareness of hygiene and safety, spurring interest in adhesives for medical and sanitary applications, which became crucial for packaging and sealing health products. Additionally, as construction and infrastructure projects gradually resumed, there was a renewed focus on advanced adhesives for building and renovation purposes. The market's recovery is linked to the pace of economic recovery and industry revival in the post-pandemic period, with a growing emphasis on adopting sustainable and resilient adhesive solutions. Overall, while the pandemic posed challenges, it also presented new opportunities for innovation and adaptation in the wet adhesive sector.

Latest trends / Developments:

The Asia Pacific Wet Adhesive Market is currently experiencing several key trends and developments driven by technological advancements and evolving industry needs. One prominent trend is the increasing shift towards eco-friendly and sustainable adhesive solutions, as both regulatory pressures and consumer demand for low-VOC and biodegradable products intensify. Innovations in adhesive formulations are focusing on enhancing performance attributes such as bonding strength, durability, and temperature resistance, catering to a wide range of applications from packaging to automotive and construction. The growing e-commerce sector has spurred advancements in packaging adhesives, emphasizing the need for efficient, strong, and tamper-evident solutions. Additionally, the market is witnessing a rise in the adoption of smart adhesives integrated with sensors for applications in electronics and smart packaging. The rapid urbanization and infrastructure development across the Asia Pacific are driving demand for advanced adhesives in construction and renovation projects. Furthermore, the emphasis on automation and technological integration in manufacturing processes is leading to the development of adhesives that meet the stringent requirements of modern industrial applications. These trends reflect the market's adaptability and innovation in response to changing industrial and consumer demands.

Key Players:

- Henkel AG & Co. KGaA

- 3M Company

- Sika AG

- H.B. Fuller Company

- Bostik (a subsidiary of Arkema)

- Avery Dennison Corporation

- Dow Chemical Company

- Kraton Corporation

- Ashland Global Holdings Inc.

- Illinois Tool Works Inc.