Asia-Pacific Metallocene Market size (2024-2030)

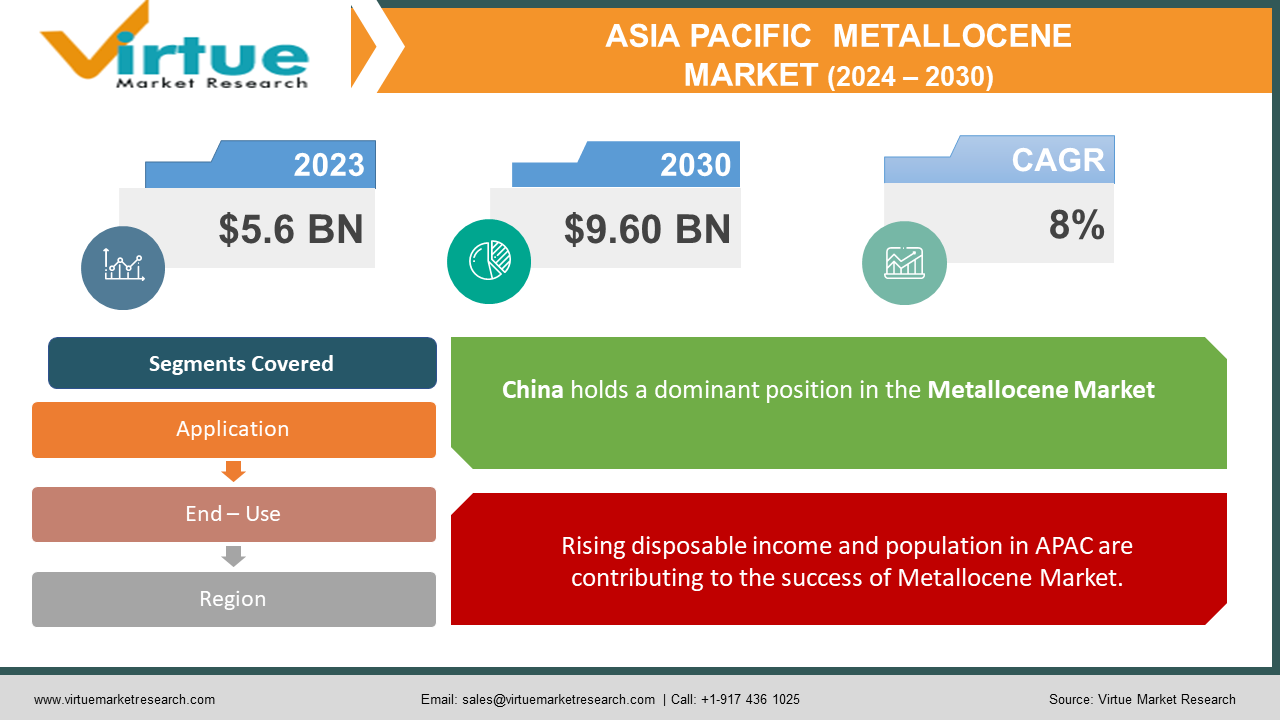

The Asia-Pacific metallocene market was valued at USD 5.6 billion in 2023 and is projected to grow to USD 9.60 billion by 2030, exhibiting a compound annual growth rate (CAGR) of 8% during 2024–2030.

Metallocene refers to tiny structures resembling sandwiches where a metal ion is nestled between two rings of five carbon atoms. Primarily used as catalysts, they act like microscopic matchmakers, enabling the creation of specific plastic structures. This opens doors to plastics with tailored properties like superior clarity, strength, and heat resistance. While not directly used in plastics themselves, metallocene catalysts are revolutionizing the Asia-Pacific market, especially for films in packaging, due to their eco-friendly nature and abundance in the region.

Key Market Insights:

The Asia-Pacific metallocene market reigns supreme, boasting the largest share. This growth is fueled by a booming packaging film industry, particularly in China, India, and Japan. Films dominate the market, valued for their superior toughness and moisture resistance in automotive, construction, and food & beverage applications. Eco-friendly packaging trends and readily available raw materials in developing economies further propel this market. Key players include ExxonMobil, Dow Chemical, and Borealis, but regional competitors are emerging. While North America holds the second-largest share, Asia-Pacific's rapid expansion and focus on innovation solidify its leadership position in the metallocene market.

Asia-Pacific Metallocene Market Drivers:

Rising disposable income and population in APAC are contributing to the success of Metallocene Market.

China and India are the two major countries in this region that have made significant progress in their economies. This has created better incomes. This newfound spending power translates into a larger consumer base, fueling demand for diverse applications utilizing metallocene's unique properties. High-performance packaging for everything from food to electronics benefits from metallocene's strength and clarity, while the automotive industry finds its lightweight yet robust nature ideal for car parts, contributing to both fuel efficiency and performance. This economic boom, coupled with a growing population, creates a vast and fertile ground for the Asia-Pacific Metallocene Market to flourish, shaping the landscape of various industries for years to come.

Growing demand for high-performance plastics is accelerating the growth rate.

Packaging needs to be robust enough to survive journeys across continents, yet crystal clear for consumer appeal. Cars require lightweight components that don't compromise on strength and safety. Food and beverage containers demand superior barrier properties to preserve freshness and flavor. That's where metallocene steps in, offering distinct advantages over conventional polyethylene. Its precisely controlled molecular structure translates to improved strength, clarity, and barrier performance. Food containers that are fresher and lighter car parts without sacrificing structural integrity and packaging that protects the most delicate products are achieved by this. Metallocene isn't just meeting these demands; it's exceeding them, making it the go-to material for industries seeking innovation and performance excellence.

The focus on lightweight materials is propelling the market.

The relentless pursuit of fuel efficiency has led the automotive industry on a global quest for lighter materials. Metallocene emerges as a popular choice, offering a unique advantage: the ability to be tailored for reduced weight while preserving crucial performance properties. Car parts crafted from metallocene shed unnecessary pounds without compromising strength, heat resistance, or durability. This translates to lighter vehicles gliding effortlessly through the gears, sipping less fuel, and emitting fewer emissions. The benefits extend beyond environmental concerns. Lighter cars boast sharper handling, quicker acceleration, and a more dynamic driving experience. Metallocene doesn't just lighten the load; it unlocks a new era of performance with every gram shaved off. From engine components to body panels, the potential applications are vast, paving the way for a new generation of fuel-efficient and exhilarating vehicles. The future of driving is lighter, cleaner, and more exciting due to the transformative power of metallocene.

Asia-Pacific Metallocene Market Challenges and Restraints:

Competition from established players is hindering market growth.

The towering presence of established players like ExxonMobil and Dow Chemical casts a long shadow over the metallocene market, posing a significant challenge for new entrants. These giants boast extensive experience, economies of scale, and well-established distribution networks, making it tough for newcomers to gain a foothold. Their brand recognition and existing customer relationships further strengthen their position, making it difficult for new players to convince potential buyers to switch. Additionally, established players often control crucial patents and intellectual property, creating legal and technological barriers for those trying to innovate in the space. This can limit the diversity of offerings and hinder technological advancements in the market. However, this challenge isn't an unsurmountable wall. New entrants can find success by focusing on niche applications, offering specialized services, or developing unique value propositions that resonate with specific customer segments. Strategic partnerships with other players or leveraging innovative distribution channels can also help them carve out their own space. Ultimately, while the competition is fierce, it also creates opportunities for differentiation and innovation, driving the metallocene market forward.

Fluctuating raw material prices are the biggest hurdle.

The volatility of oil prices throws a wrench into the well-oiled machinery of metallocene production. Since key raw materials for these catalysts are derived from oil, any price fluctuations ripple through the entire supply chain. This creates many challenges due to sudden price hikes, which inflate production costs and decrease profits. Additionally, supply-chain disruptions and shortages will occur later. This uncertainty makes budgeting and forecasting complex for manufacturers as they grapple with volatile costs while trying to maintain competitive pricing. Furthermore, profit margins, often slim in the competitive world of plastics, can be severely squeezed by unexpected oil price surges. To mitigate this risk, manufacturers might resort to hedging strategies or exploring alternative, more stable feedstocks. However, these options come with their complexities and costs, highlighting the ongoing challenge of balancing affordability with the unique performance benefits metallocene catalysts offer.

Stringent regulations are hindering market growth.

Stringent rules on waste disposal, often requiring specialized infrastructure and processes, can significantly increase operational costs for producers and recyclers. This can be particularly challenging for smaller players who might lack the resources to comply. Additionally, evolving safety standards for handling metallocene catalysts themselves, due to their potentially hazardous nature, necessitate additional investments in training and safety protocols, further straining budgets. Beyond cost, regulations can also act as entry barriers, with complex licensing procedures and certifications creating hurdles for new players trying to access the market. This can stifle innovation and limit competition, potentially hindering the overall growth and development of the metallocene industry. Striking a balance between environmental protection, responsible waste management, and fostering a vibrant and accessible market remains a key challenge for policymakers and industry stakeholders alike.

Market Opportunities:

Asia-Pacific paints a vibrant picture of metallocene market opportunities. Its packaging film industry, particularly in China, India, and Japan, presents a goldmine. These nations' booming economies propel the demand for high-performance films, perfectly fitting metallocene's strengths: superior toughness, moisture resistance, and eco-friendliness. Expanding applications in automotive, construction, and food & beverage further amplify the market. Rising environmental concerns create lucrative avenues for bio-based metallocene catalysts, aligning with the region's readily available raw materials. While established players like ExxonMobil and Dow Chemical dominate, regional competitors are emerging, injecting fresh ideas and competition. Overall, Asia-Pacific's focus on innovation and growing demand for advanced materials position it as a prime hunting ground for metallocene market ventures.

ASIA-PACIFC METALLOCENE MARKET REPORT COVERAGE:

|

REPORT METRIC

|

DETAILS

|

|

Market Size Available

|

2023 - 2030

|

|

Base Year

|

2023

|

|

Forecast Period

|

2024 - 2030

|

|

CAGR

|

8%

|

|

Segments Covered

|

By Application, enduser, and Region

|

|

Various Analyses Covered

|

Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities

|

|

Regional Scope

|

China, Japan, South Korea, India, Rest of the Asia-Pacific |

|

Key Companies Profiled

|

Univation Technologies , ExxonMobil, Dow Chemical, Mitsui Chemicals, SK Chemicals , China Petroleum & Chemical Corporation, Prime Polymer Co., Ltd., Daelim Chemical , LyondellBasell Industries N.V., SABIC (Saudi Basic Industries Corporation)

|

Asia-Pacific Metallocene Market Segmentation

Asia-Pacific Metallocene Market Segmentation: By Application

- Films

- Sheets

- Injection Molding

- Extrusion Coating

- Others

Based on application, the film category is both the largest and the fastest-growing. mPE films are employed in a variety of end-use sectors, including food and beverage packaging, building and construction, and automotive. Throughout the forecast period, the remarkable qualities of mPE films, such as their increased toughness and high moisture characteristics, are anticipated to drive the segment revenue market.

Asia-Pacific Metallocene Market Segmentation: By End-User

- Packaging

- Consumer Goods

- Automotive

Packaging is both the largest and the fastest-growing end-user in the metallocene market, with a rough share of 40% in 2023. Superior qualities, including puncture resistance, toughness, clarity, high-performance, lightweight, and crystal-clear films, and sealability, make metallocene-based polyethylene (mPE) and metallocene polypropylene (mPP) suitable for a variety of packaging applications. Metallocene-based materials are likely to be increasingly used because of the growing need for flexible packaging solutions in industries including food and beverage, healthcare, and personal care. While automotive parts like bumpers and fenders benefit from metallocene's touch for improved fuel efficiency, safety, and durability, consumer goods like toys and appliances see a quality, performance, and aesthetic boost due to this technology.

Asia-Pacific Metallocene Market Segmentation: Asia-Pacific Regional Analysis:

- China

- Japan

- South Korea

- India

- Australia and New Zealand

- Rest of Asia-Pacific

China reigns supreme, its growth fueled by a booming automotive and consumer goods industry, urbanization, and government support. Furthermore, there are well-known companies in this market that engage in bulk manufacturing. These businesses generate more money because of their worldwide reach. Prominent companies include Sinopec, PetroChina, Sinochem Corporation, and China National Offshore Oil Corporation (CNOOC). India is the fastest-growing, driven by its expanding middle class, automotive sector, and infrastructure development. This nation's economy has made considerable strides. Funding and investments have therefore grown. Additionally, programs and other government efforts have aided in the growth. Japan shows promising growth due to rapid economic development, a rising population, and a focus on sustainability with bio-based catalysts.

COVID-19 Impact Analysis on the Asia-Pacific Metallocene Market

The initial shockwaves of COVID-19 sent the Asia-Pacific metallocene market reeling, mirroring the broader economic slowdown. Supply chain disruptions hampered production, transportation, and logistics, while lockdowns dampened demand across key end-use industries like automotive and packaging. People lost their jobs due to economic uncertainty. Most of the funding was shifted towards healthcare applications like ventilators, hospital beds, oxygen tanks, masks, etc. This caused losses for the industry. Most of the collaborations and launches were delayed or canceled. However, the impact wasn't uniform. China, a major producer and consumer, saw a faster rebound, fueled by government stimulus and reviving domestic demand. Other countries experienced varying degrees of recovery, with some even witnessing increased demand for hygiene and medical applications using metallocene. Overall, the market displayed resilience, adapting to new consumption patterns and exploring opportunities in sectors like food packaging and e-commerce. While the long-term impact remains to be seen, the Asia-Pacific Metallocene Market is expected to emerge from the pandemic with a renewed focus on agility, diversification, and catering to evolving regional needs.

Latest trends/Developments

The Asia-Pacific metallocene market pulsates with exciting trends and developments. Bio-based catalysts, fueled by environmental concerns and readily available raw materials in the region, are on the rise, offering sustainable solutions for eco-conscious consumers. Innovation, particularly in film development, reigns supreme, with a focus on enhanced functionalities like flame retardancy and anti-microbial properties. Emerging regional players are challenging established giants like ExxonMobil and Dow Chemical, injecting fresh ideas and competition. Digitalization is creeping in, with players exploring AI-powered production optimization and e-commerce platforms to streamline operations and reach new customers. Additionally, the convergence of metallocene with other technologies, like nanotechnology, is opening doors to next-generation materials with exceptional properties. Overall, the Asia-Pacific metallocene market is a dynamic landscape brimming with potential, poised to shape the future of plastics in the region and beyond.

Businesses in this sector are driven to grow their market share through a variety of tactics, such as investments, joint ventures, and acquisitions. Companies are investing a lot of money in the development of strategies to maintain competitive pricing. This has led to more growth.

Key Players:

- Univation Technologies

- ExxonMobil

- Dow Chemical

- Mitsui Chemicals

- SK Chemicals

- China Petroleum & Chemical Corporation

- Prime Polymer Co., Ltd.

- Daelim Chemical

- LyondellBasell Industries N.V.

- SABIC (Saudi Basic Industries Corporation)