Counter-UAS Systems Market

In 2025, the Global Counter-UAS Systems Market was valued at approximately USD 3,214 million and is projected to reach around USD 8,472 million by 2030, expanding at a CAGR of about 21.4% during 2026–2030.

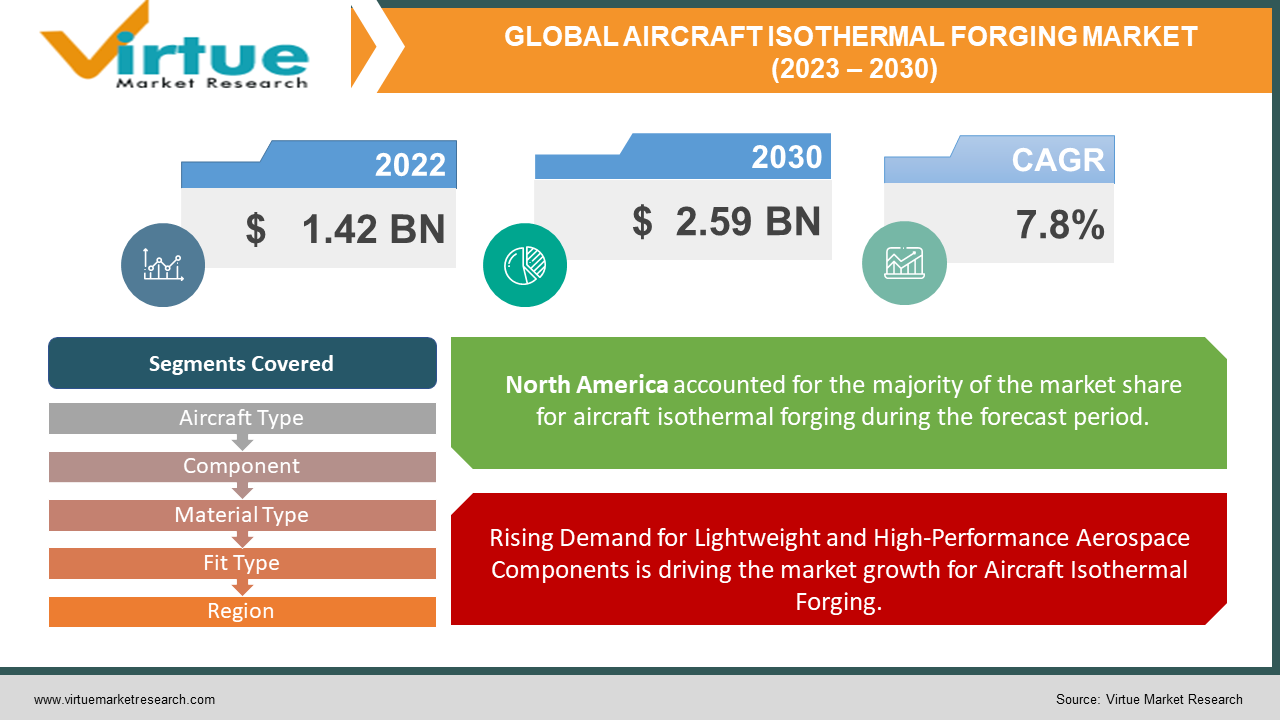

Explore reportThe Global Aircraft Isothermal Forging Market was estimated to be worth USD 1.42 Billion in 2022 and is projected to reach a value of USD 2.59 Billion by 2030, growing at a steady CAGR of 7.8% during the forecast period 2023-2030.

Aircraft Isothermal Forging is a critical and pivotal manufacturing process within the aerospace sector, involving the shaping of essential components at elevated temperatures, ensuring a uniform distribution of heat. This technique holds a vital role in guaranteeing the desired mechanical properties and structural integrity of crucial aircraft parts, including turbine disks, fan blades, landing gears, and structural components. The benefits of this forging method are manifold, encompassing improvements in material properties, reduced porosity, and enhanced resistance to fatigue. As the aerospace industry incessantly strives for heightened performance and efficiency, there has been a substantial surge in the demand for advanced isothermal forging technologies. In response, manufacturers are proactively investing in innovative forging techniques, exploring novel materials, and adopting cutting-edge equipment to meet the stringent requirements of modern aerospace applications. This relentless pursuit of advancement in isothermal forging not only caters to the industry's high standards but also contributes significantly to the progression of aviation technology. By producing aerospace components of unparalleled quality and safety, this forging process empowers the industry to push the boundaries of flight capabilities, ushering in a new era of progress and innovation in aviation.

Global Aircraft Isothermal Forging Market Drivers:

Rising Demand for Lightweight and High-Performance Aerospace Components is driving the market growth for Aircraft Isothermal Forging.

The aerospace sector's unceasing quest for lightweight materials to boost fuel efficiency and performance has led to rising demand for isothermal forging. This forging technique enables the creation of high-strength components with reduced weight and enhanced mechanical properties. This trend holds particular significance in aviation, where saving even a single kilogram can result in substantial fuel savings and operational cost reductions. As the aviation industry strives to meet the challenges of modern aviation and align with sustainability objectives, there is a growing need for advanced isothermal forging techniques that can produce lightweight, high-performance aerospace components.

Advancements in Material Science and Metallurgical Research are propelling the adoption of Isothermal Forging in Aerospace Manufacturing.

The aerospace industry has witnessed significant advancements due to the development of cutting-edge materials like high-strength alloys and superalloys, which have revolutionized the potential of isothermal forging in manufacturing. Metallurgical research efforts have been instrumental in identifying and optimizing materials with exceptional properties, including high-temperature strength, corrosion resistance, and fatigue resistance. Isothermal forging plays a vital role in efficiently shaping these advanced materials, ensuring precise microstructure and properties that perfectly align with the stringent requirements of aerospace applications.

Increasing Focus on Engine Efficiency and Performance is boosting the demand for Isothermal Forged Aerospace Components.

Aircraft engines stand as a crucial element significantly influencing fuel efficiency, performance, and emissions. In this context, isothermal forging plays an indispensable role in manufacturing top-tier engine components like turbine blades and disks, subjected to extreme temperatures and mechanical stresses during operational usage. By enabling meticulous regulation over the material's microstructure, isothermal forging yields components boasting exceptional fatigue resistance, thermal stability, and mechanical strength.

Rapid Growth in the Aviation Industry and Aircraft Fleet Expansion are fuelling the market growth.

The global aviation industry is currently undergoing a period of rapid expansion, fuelled by a growing number of airlines seeking to meet the increasing demand from passengers. As a result, there is a heightened requirement for isothermal forged components. Both new aircraft introductions and fleet modernization efforts are driving the surge in demand for these high-quality components. Aircraft manufacturers and component suppliers are making substantial investments in advanced isothermal forging technologies to cater to the ever-expanding aviation market.

Global Aircraft Isothermal Forging Market Challenges:

The complexity and Cost of Isothermal Forging Equipment and Processes are hindering market growth.

Isothermal forging necessitates specialized equipment, such as high-temperature furnaces and precision controls, to ensure uniform temperature distribution during forging. However, the initial investment and operational expenses linked to this equipment can be considerable, particularly for smaller and medium-sized manufacturers. Moreover, the isothermal forging processes may prove more intricate and time-consuming than conventional forging methods, potentially affecting production efficiency and cost-effectiveness. Addressing these challenges calls for strategic investments in advanced forging equipment and process optimization to enhance the overall cost-efficiency and scalability of isothermal forging in aerospace manufacturing.

Stringent Quality and Safety Standards in the Aerospace Industry necessitate strict process control and certifications.

Aerospace components produced through isothermal forging are subject to rigorous quality and safety standards imposed by aviation authorities and industry regulations. Meeting these high demands for material properties and performance necessitates precise process control and strict adherence to manufacturing specifications. Any deviation from these standards can lead to component rejection, resulting in increased costs and production delays. To ensure the consistency and reliability of their products, aerospace manufacturers engaged in isothermal forging must invest in comprehensive quality control measures and obtain necessary certifications. This task can be particularly challenging for some companies, especially those entering the aerospace market, as it requires significant resources and commitment to uphold the stringent requirements and maintain a high level of quality assurance.

Global Aircraft Isothermal Forging Market Opportunities:

Growing Demand for Additive Manufacturing (AM) in Aerospace presents a complementary opportunity for Isothermal Forging.

Additive manufacturing, or 3D printing, is becoming increasingly popular in aerospace manufacturing due to its capacity to fabricate intricate geometries and lightweight structures. While AM holds advantages for specific components, isothermal forging provides unique benefits in the production of high-strength, load-bearing parts, and critical components. The synergy between AM and isothermal forging offers a complementary approach to aerospace manufacturing. AM can be utilized to create complex shapes, which can then be further enhanced through isothermal forging to improve material properties and mechanical performance. Manufacturers who integrate both AM and isothermal forging in their production processes can offer a wider array of aerospace components while optimizing efficiency and overall performance.

Growing Focus on Sustainability and Circular Economy in the Aerospace Industry to Drive Demand for Isothermal Forged Components from Recycled Materials.

The aerospace sector is showing a growing commitment to sustainability and circular economy principles, aiming to reduce waste and environmental impact. Isothermal forging emerges as a key player in sustainable aerospace manufacturing by enabling the use of recycled or reclaimed materials for component production. The capacity to forge components from recycled sources, such as discarded aerospace parts and scraps, offers a significant contribution to creating a more sustainable and environmentally friendly aerospace supply chain. Manufacturers embracing eco-friendly practices and adopting isothermal forging techniques for recycled materials can respond to the increasing demand for sustainable aerospace solutions, supporting the industry's overall sustainability goals.

Increased Collaboration between Aerospace Manufacturers and Research Institutions to drive Innovation and Technology Advancements.

The aerospace industry can foster innovation and drive technological advancements in isothermal forging through collaborative efforts between manufacturers and research institutions. By working together, they can focus on research and development initiatives aimed at exploring new materials, refining forging techniques, and optimizing process efficiency. Engaging with academia and research organizations ensures that aerospace manufacturers remain at the forefront of technological advancements, enabling them to offer state-of-the-art isothermal forging solutions that cater to the ever-evolving needs of the aerospace sector. These collaborative endeavors have the potential to lead to significant breakthroughs in materials science, metallurgy, and forging technologies, ultimately bolstering the growth and competitiveness of the isothermal forging market within the aerospace industry.

AIRCRAFT ISOTHERMAL FORGING MARKET REPORT COVERAGE:

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2022 - 2030 |

|

Base Year |

2022 |

|

Forecast Period |

2023 - 2030 |

|

CAGR |

7.8% |

|

Segments Covered |

By Aircraft Type, Component, Material Type, Fit Type, and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regional Scope |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Key Companies Profiled |

Anchor Harvey, ATI, Aubert and Duval, Bharat Forge, Arconic Corp. |

Commercial Aircraft

Military Aircraft

Business Jet

Others

Based on market segmentation by aircraft type, the Commercial Aircraft segment dominates the Aircraft Isothermal Forging Market. Commercial Aircraft is witnessing substantial growth, driven by increasing passenger demand and aircraft fleet expansion. Moreover, the Manufacturers in this segment are focusing on producing lightweight and high-performance components for commercial aircraft engines and airframes, contributing to fuel efficiency and operational cost savings.

However, the Business Jet segment is witnessing growth at a rapid pace, driven by the rising demand for private and corporate aviation solutions. Isothermal forging offers a solution for producing critical components in business aircraft, such as landing gears and structural elements, which require exceptional material properties and fatigue resistance.

Fan Blade

Turbine Disks

Shafts

Connector Rings

Others

Based on market segmentation by component, the Turbine Disks segment dominates the Aircraft Isothermal Forging Market. Turbine disks are critical components in aircraft engines, exposed to high temperatures and mechanical stresses during operation. Isothermal forging ensures the desired mechanical properties and fatigue resistance of turbine disks, making them suitable for high-performance and efficient aircraft engines.

However, The Fan Blades segment is the fastest growing segment, due to an increasing demand for lightweight and aerodynamically efficient fan blades in modern aircraft engines. Isothermal forging offers the necessary material properties and structural integrity to produce fan blades that meet stringent aviation requirements while contributing to fuel efficiency and performance improvements in aircraft engines.

Titanium Alloys

Nickel-Based Alloys

Steel Alloys

Others

Based on market segmentation by Material Type, the Nickel-Based Superalloys segment holds the largest market share. Nickel-based superalloys are favored in aerospace for high-temperature strength and corrosion resistance. Isothermal forging enables precise control over their microstructure, ideal for critical aerospace components. Rising demand from engine manufacturers and structural suppliers is fueling isothermal forging market growth.

However, The Titanium Alloys segment is experiencing the fastest growth due to the increasing use of titanium components in modern aircraft structures. Moreover, Titanium alloys offer an excellent strength-to-weight ratio, making them ideal for lightweight and high-performance aerospace components.

Line Fit

Retro Fit

Based on the market segmentation by Fit Type, Line Fit is having the highest market growth because of the increase in demand for new aircraft from commercial airliners. However, the Retro-Fit growth is also on the rise because of the increase in the replacement of hydro-mechanical systems with fly-by-wire systems

North America

Europe

Asia-Pacific

Middle East and Africa

South America

Based on market segmentation by region, North America dominates the Aircraft Isothermal Forging Market as the region is a key hub for the aerospace industry, with several leading aircraft manufacturers and component suppliers based in North America. The region's emphasis on technology, innovation, and R&D drives isothermal forging adoption in aerospace. A growing aircraft fleet and demand for fuel efficiency boost its dominant market position.

However, Asia-Pacific is having the fastest growth in the market, driven by the expansion of the aviation industry and the increasing demand for air travel in the region. Countries here are witnessing significant investments in aircraft fleet expansion and modernization, creating a substantial demand for isothermal forged components in this region.

Global Aircraft Isothermal Forging Market Key Players:

Anchor Harvey

ATI

Aubert and Duval

Bharat Forge

Arconic Corp.

The Global Aircraft Isothermal Forging Market was estimated to be worth USD 1.42 Billion in 2022 and is projected to reach a value of USD 2.59 Billion by 2030, growing at a steady CAGR of 7.8% during the forecast period 2023-2030.

Rising demand for lightweight and high-performance aerospace components, advancements in material science and metallurgical research, increasing focus on engine efficiency and performance, rapid growth in the aviation industry, and aircraft fleet expansion are the market drivers for the Global Aircraft Isothermal Forging Market.

Turbine Disks, Fan Blades, Landing Gears, Structural Components, and Other Components are the segments under the Global Aircraft Isothermal Forging Market by component.

North America dominates the market in the Global Aircraft Isothermal Forging Market.

Asia-Pacific is the fastest-growing region in the Global Aircraft Isothermal Forging Market, driven by the expansion of the aviation industry and the increasing demand for air travel in the region.

Joining thousands of companies around the world committed to making the Excellent Business Solutions.

Specify your preferred Countries, Segments, or timeframes

Unlock Country Level Outlook, Trends, Cross-country Comparability, or supply Chain Variations.

Analyst Support

Every order comes with Analyst Support.

Customization

We offer customization to cater your needs to fullest.

Verified Analysis

We value integrity, quality and authenticity the most.